It’s no secret that mortgage rates have risen sharply. They now stand above those seen on the eve of the financial crisis. However, less appreciated, the difference between mortgage rates and U.S. Treasury yields is almost .75% more than in 2007. The predominant reason for the wider-than-normal gap is the status of the banks. Banks are rapidly tightening lending standards due to fleeing deposits and an inverted yield curve. Consequently, some banks cannot make mortgage loans even at current rates. Those able and willing to issue mortgages have pricing power and appear to be using it.

The Fed understands housing is a significant part of the economy and a driver of inflation. One of their objective in raising Fed Funds was to slow down double-digit housing inflation. That has been accomplished. Fortunately, as we saw in 2008, the fallout regarding home prices, mortgage- and asset-backed securities, and ultimately banks is not problematic. However, higher mortgage rates make home ownership difficult for many potential buyers. The “extra” 75 basis points of spread between mortgage rates and the 10-yr Treasury yield result in approximately 7.5% less buying power for a prospective home buyer. In November 2021, a 3% mortgage rate resulted in a monthly payment of $420 per $100,000 loan. Today, at 7.375%, it’s $690. The purchase price a homebuyer can afford today with the same 2021 payment has fallen by 39%!

What To Watch Today

Earnings

Economy

Market Trading Update

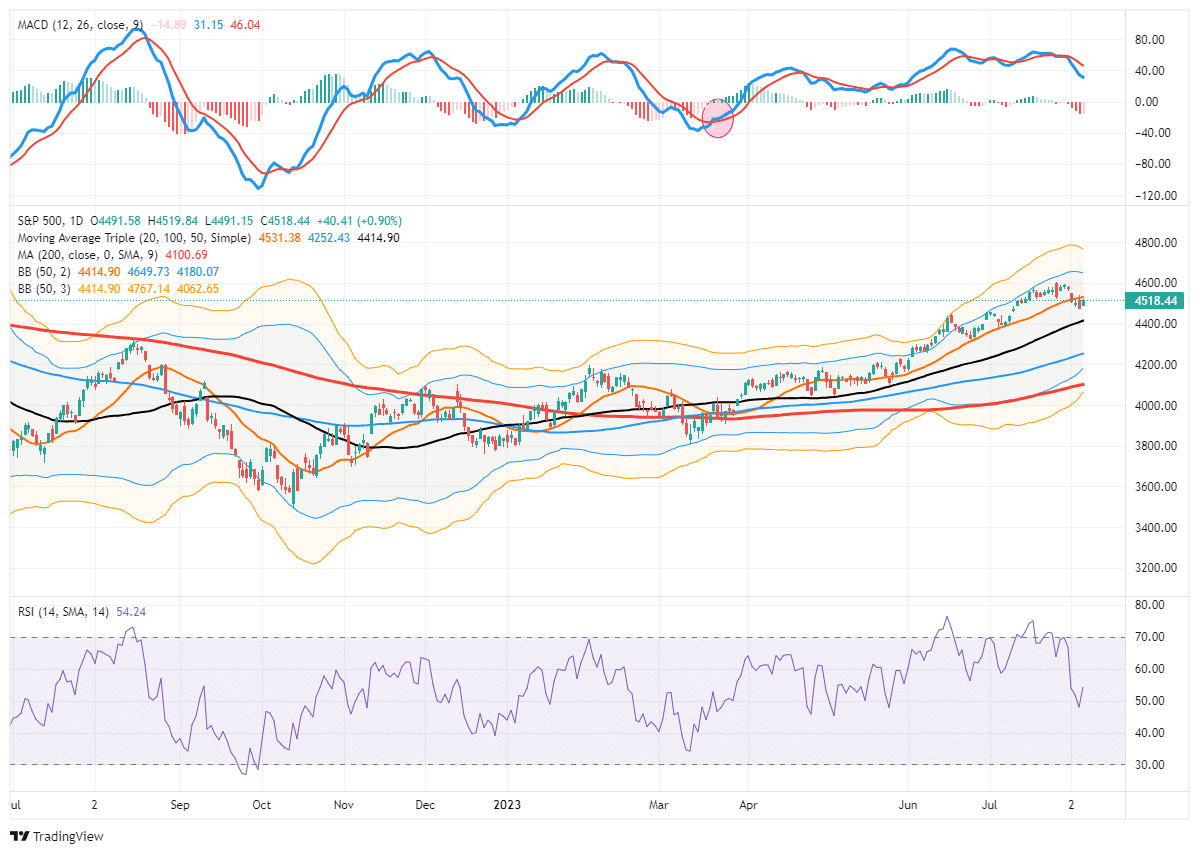

As noted in yesterday’s “Before The Bell” video, a bit of a rally was expected, given the recent correction process. The short-term oversold condition, as shown by the relative strength index (RSI), suggested a probable bounce. That bounce came yesterday. The key will be for the market to break above, and hold, the 20-DMA. If the market fails to climb above that current resistance level, a retest of the 50-DMA becomes more likely. With the MACD “sell signal” still intact and elevated, we would expect continued price weakness over the next few weeks. The recent more extreme overbought conditions can be resolved either by a deeper price correction or just “time” of the market going nowhere. Either outcome will provide a better risk/reward entry point to increase exposure heading into year-end.

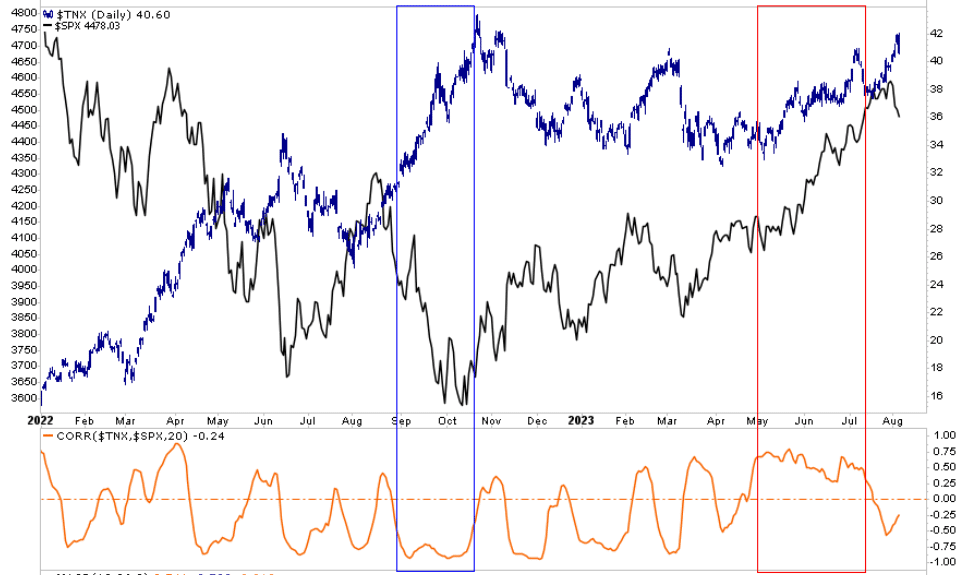

Are Higher Yields Starting To Weigh on Stocks?

In 2022, the last time bond yields were as high as current levels, stocks were aggressively selling off. At the time, the market feared higher borrowing rates would stifle economic growth and lead to a recession. A year later, the market appears more comfortable that higher rates won’t detract from economic activity. The blue box in the graph below highlights that ten-year Treasury yields rose sharply last year while stock prices plummeted. As such, the correlation (lower graph) between the two was sustained at a deeply negative level. Recently, yields drifted higher, albeit not as steeply as in 2022, and stocks rose. Consequently, the correlation was sustained at a high positive level for over two months.

The correlation between stocks and bond yields is returning to a normal negative reading. It appears higher yields are starting to weigh on stock market sentiment. If yields continue higher, it’s hard to imagine stock investors will ignore the bond market and head for record highs.

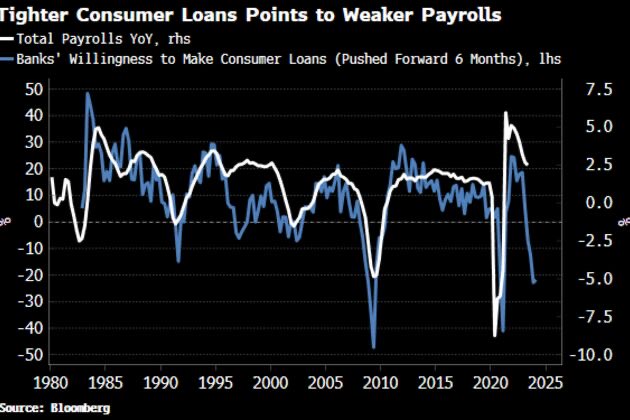

More On The Jobs Labor Market

As we wrote on Monday, the labor market appears to have finally normalized. Now we must assess future data to see if the weakening trend in job growth maintains at pre-pandemic averages or if it keeps trending lower. To help, are the following charts.

The first one below from EPB Research shows that almost two-thirds of the recent job growth is from government, education, and health services sectors. Most of the job growth in those sectors is unrelated to economic activity. Further, if we add in lower-paying and often temporary jobs in the leisure, restaurant, and hospitality sectors, the concentration of new job growth is over 100%. Those sectors are related to economic activity, but they are very volatile. The takeaway is that job growth is solid but not coming from the sectors that would breed confidence that it is sustainable.

The second graph from Bloomberg shows a strong correlation between bank lending standards and payrolls. Lending standards, which are tightening rapidly, tend to lead payroll growth by six months. The banking crisis in March forced banks to reduce loan growth. Consequently, if the correlation holds, we should see payroll growth go negative over the next few months.

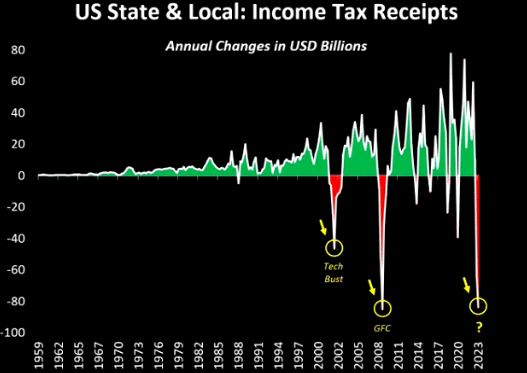

The last graph is confounding. Despite strong payroll growth and above-average interest and capital gains income, state and local income taxes are declining. The only logical explanation is that higher-paying jobs are declining while lower-paying ones increase. Therefore the number of employees rises, but the aggregate income and tax payments fall.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.