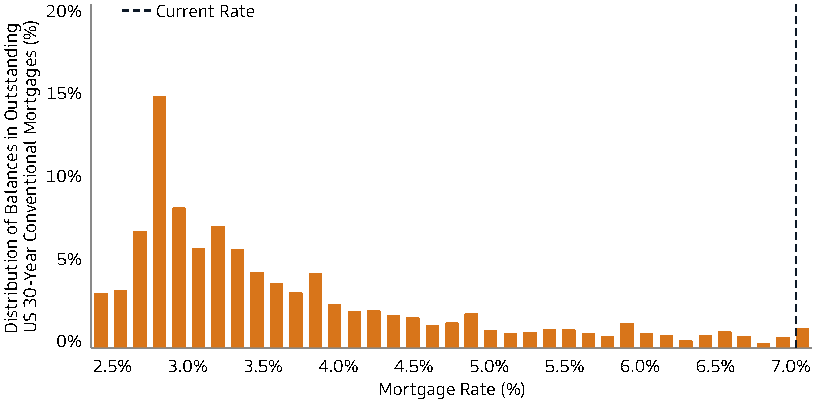

Over the last thirty years, the Fed has relied on lower interest rates to pump the economy when it slowed. Lower rates helped wide swaths of the economy. But quite often, the most immediate benefit was from the housing market. Lower rates made housing more affordable, thus increasing the ability for potential buyers to buy homes and pay more for houses. Maybe, more importantly, existing homeowners refinanced their mortgages in troves at lower rates. The result was reduced mortgage payments, leaving more money to consume goods and services. While stimulating the housing market was a robust policy tool, its effectiveness going forward may be much more limited.

The graph below from Goldman Sachs Asset Management (GSAM) highlights the Fed’s future problem. Mortgage holders have mortgage rates well below current levels. Per GSAM, “less than 2% of conventional borrowers pay more than the current market rate on a 30-year fixed rate mortgage, potentially limiting motivation to refinance even if rates fall.” Further, a third of all outstanding mortgages have a rate of 3% or less. Unlike prior periods of easy monetary policy, the Fed will find it will much lower rates to stimulate the housing market and spur refinancing activity. Such doesn’t mean they can’t stimulate the economy through housing. It means that zero Fed Funds and sub 3% mortgages will be needed to have the same stimulative effect as decades past.

What To Watch Today

Earnings

Economy

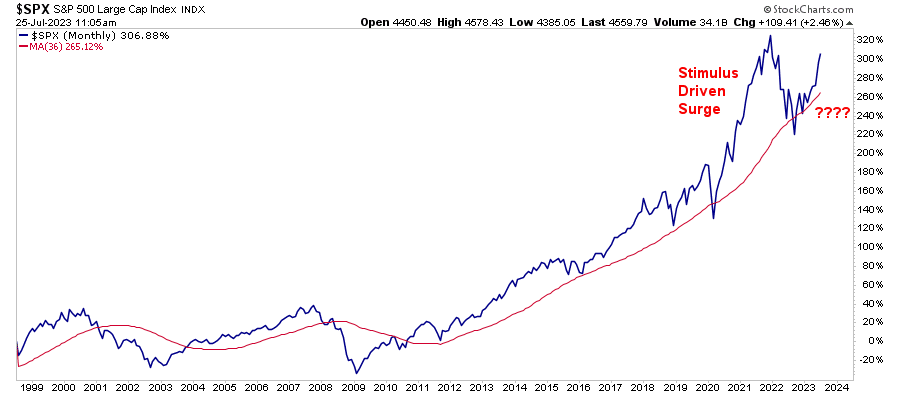

Market Trading Update

The market has been on a massive bullish run this year. However, the sharp ascent in prices is rather unique compared to the past 25 years, with the exception of the stimulus-fueled surge following the pandemic-driven shutdown. As shown, following the correction of that stimulus-driven spike back to the 36-month moving average in 2022, a correction with the long-term running bull market from 2009, the market is once again moving higher in a more parabolic fashion. However, while there is currently no QE from the Federal Reserve, there are clearly strong money flows into assets chasing higher returns.

While these vertical spikes can last longer than logic would predict, there are two questions that we should be asking as investors. First, if liquidity reduces, the current deviation from the long-term running bullish trendline is likely more difficult to maintain. Secondly, the entirety of the bull market from the 2009 lows was predicated on lower interest rates and repeated monetary interventions. Given the enormity of the advance in the financial markets since 2009, can that trend be continued in the future?

If the economy returns to 2% trend growth and inflation returns to 2% or less, it seems logical that creating outsized returns in the future will become increasingly difficult, given the relationship between economic growth, inflation, and interest rates.

We need to consider this carefully in our expected return rates going forward.

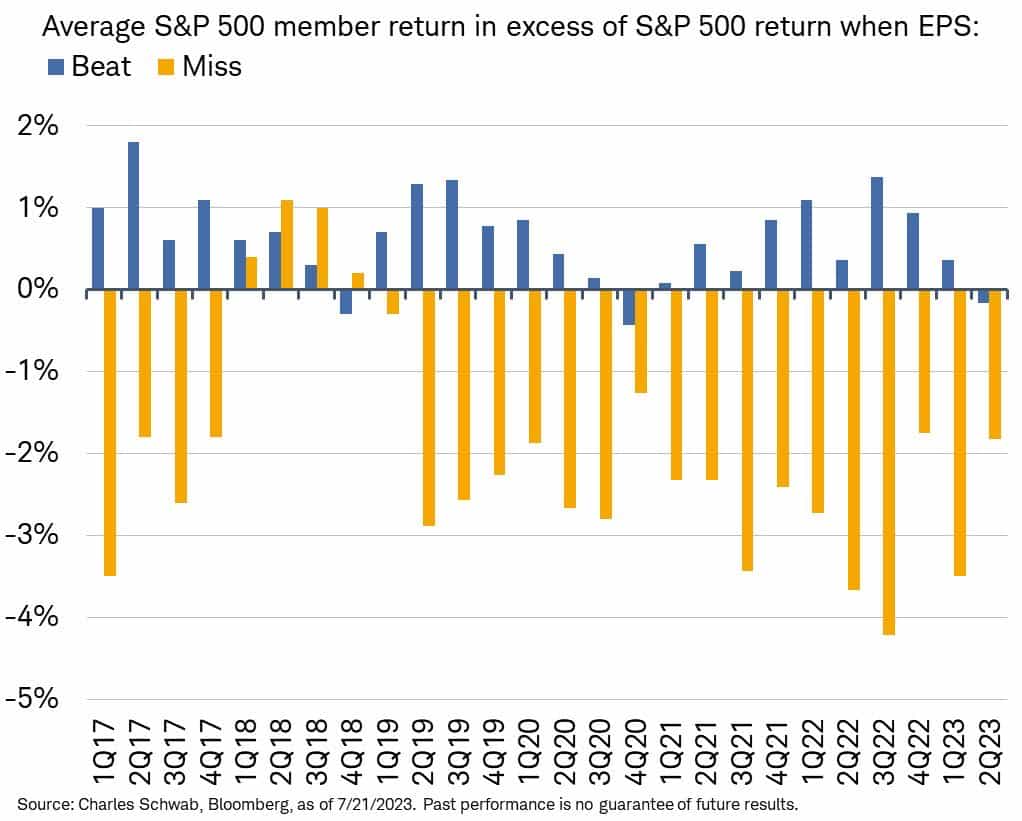

Investors Are More Demanding This Earnings Season

The current round of corporate earnings has elicited a different market response than is typical. The graph below, courtesy of Charles Schwab, shows that the average excess returns of those stocks reporting earnings have been negative. Negative excess returns are not just for those stocks that miss estimates but also for those beating estimates. While earnings season is far from over, it appears that earnings have been decent, but forward guidance has been underwhelming in many cases. Before rushing to judgment, the quarterly earnings cycle is still in full swing, with many of the largest companies yet to report.

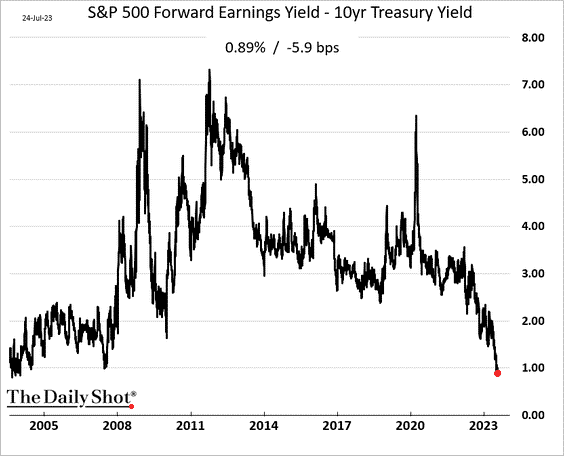

In a couple of weeks, when most stocks have reported earnings, it will be interesting to revisit this graph and consider what it may mean for share performance going forward. For instance, is the post-earnings performance a sign that investors are becoming more demanding of good news, given valuations are high? The second graph shows that the differential between the expected earnings yield and 10yr U.S. Treasury notes is the lowest in 20 years. Investors should have high standards given the relatively high yield on risk-free bonds.

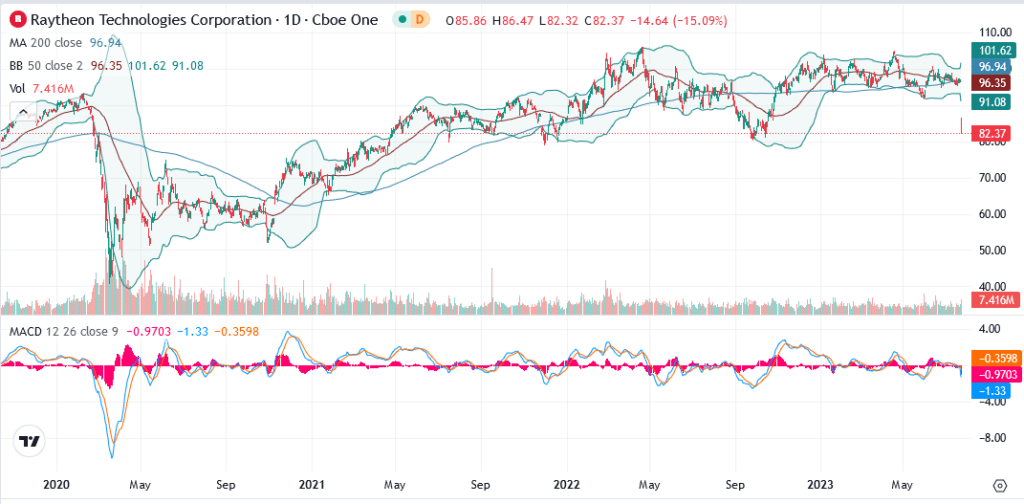

Raytheon Hits It Out Of The Park, But Its Stock Strikes Out.

Defense contractor Raytheon (RTX) posted better-than-expected earnings and upped its forward guidance. Despite the good news, the stock is trading about 15% lower. in addition to good earnings, guidance, and a growing large backlog of orders, the company stated: “Pratt & Whitney has determined that a rare condition in the powdered metal used to manufacture certain engine parts will require accelerated fleet inspection. This does not impact engines currently being produced.”

- Adjusted EPS $1.29 (est $1.18)

- Sales $18.32B (est $17.67B)

- New guidance FY FCF About $4.3B – Old guidance About $4.8B (est $4.82B)

- New guidance FY Adj EPS $4.95 To $5.05, Old guidance $4.90 To $5.05

- New guidance FY Sales $73.0B To $74.0B, Old guidance $72.0B To $73.0B

With the double-digit price decline, RTX is back to the support which has held well for the last two years. It is also below pre-pandemic levels. We will wait to learn more about the potential financial impact of their announcement and potentially add to our holdings if it turns out the market is overreacting.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.