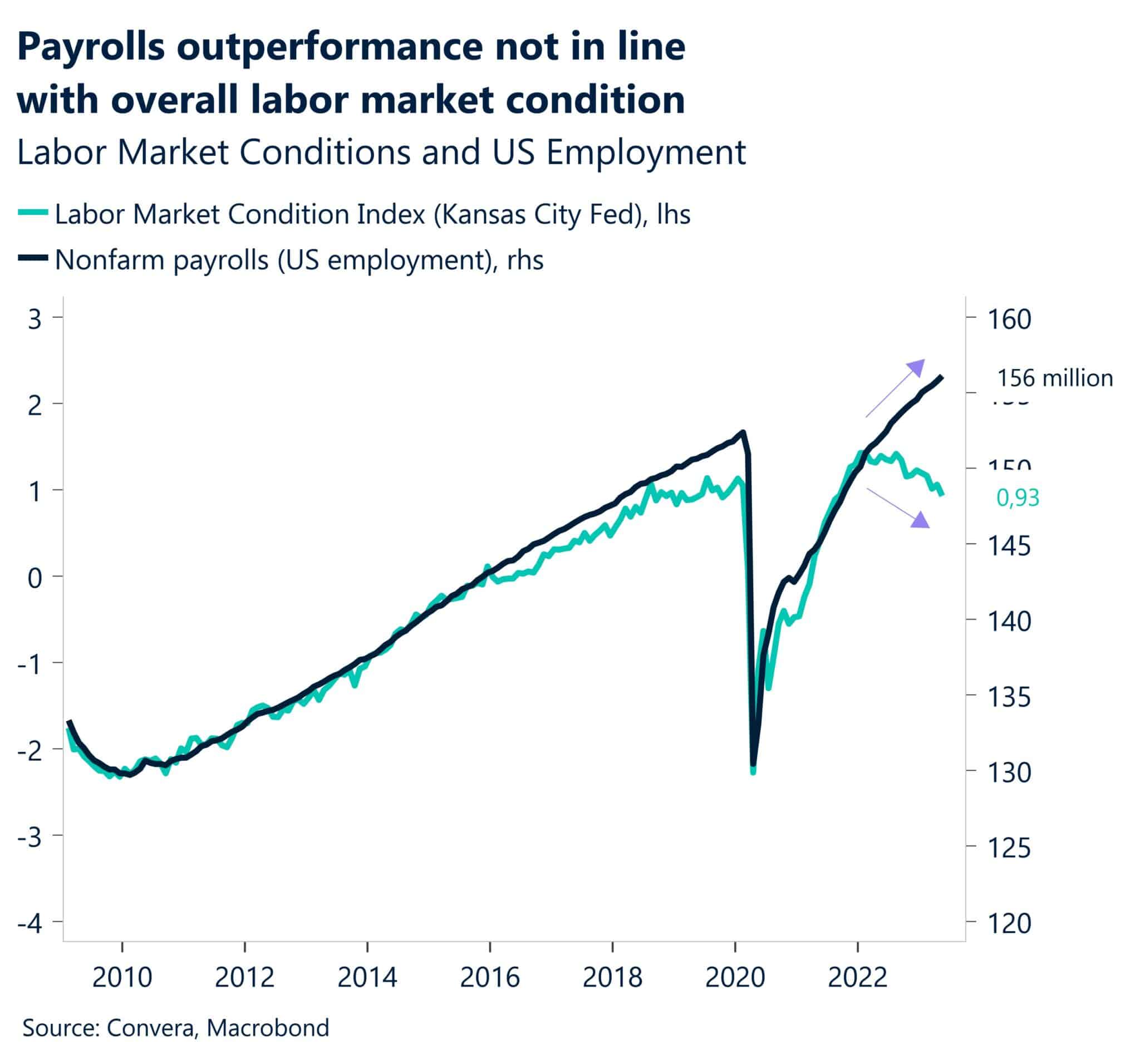

Since 1955 every recession was met with weak labor markets. On average, over the 75 years, unemployment rose by 2.7%. The lowest instance was 1.5%, and the highest, excluding 2020, was 4.8%. Periods of weak labor markets in non-recessionary periods have not occurred over this time. As such, it’s a safe assumption that the odds of a recession are nil unless the labor markets weaken materially. Given some signs of economic weakness, labor market indicators will be critical to follow to see if a recession is likely. Given the importance of employment to our economic outlook, we introduce the Kansas City Fed Labor Market Condition Index.

While the growth of payrolls continues to surprise economists to the upside, the unemployment rate just ticked up from 3.4 to 3.7%. Other labor markets indicators, like ISM and Fed surveys, initial jobless claims, job openings, and hours worked, also point to a slight cooling off of employment. The Kansas Fed Labor Conditions Index uses 24 labor market indicators, including those mentioned, to assess the labor market. Unlike payroll growth, the index has been trending lower for over a year. The Kansas City Fed indicator also slowed before payrolls before the last few recessions.

What To Watch Today

Economy

Earnings

- No notable earnings releases today

Market Trading Update

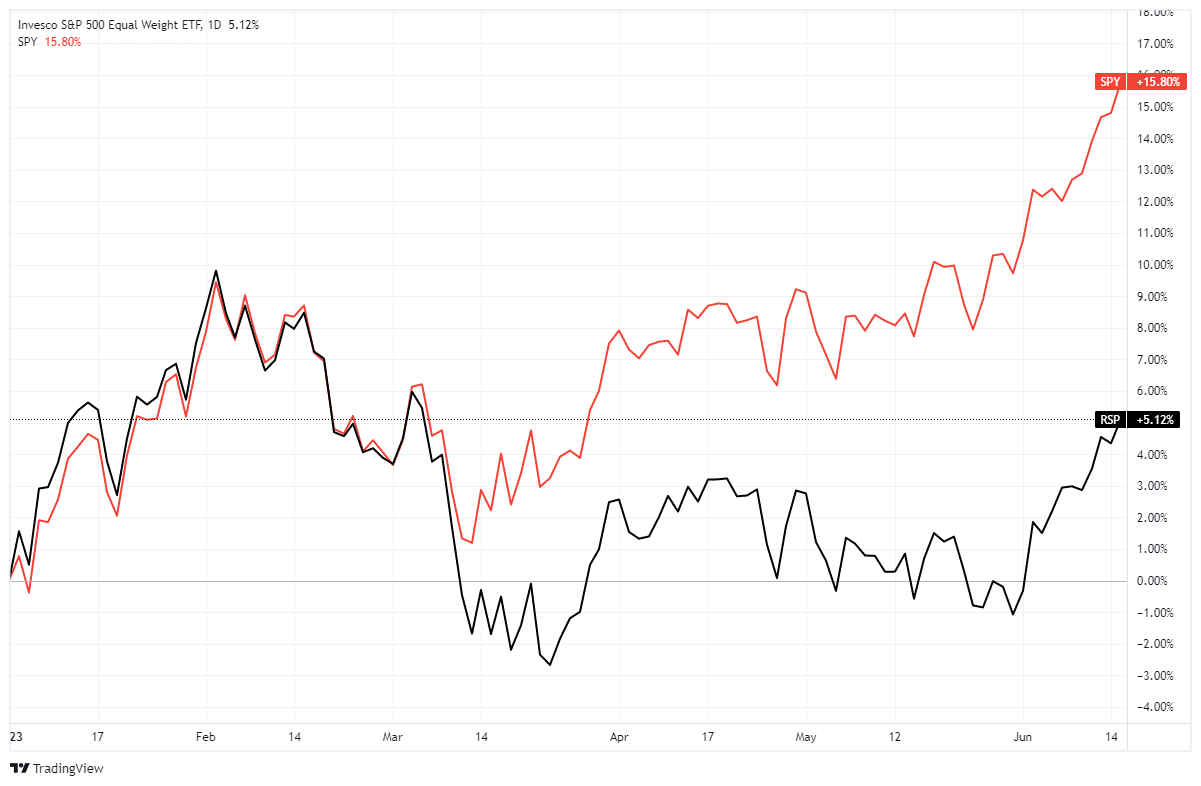

Over the last couple of weeks, we have discussed the issue of overall market breadth, which has been weak. We also suggested that we should see some rotation from the leaders to the laggards. That is indeed what we saw since the beginning of June as the S&P 500 Equal Weight Index has surged in performance even as the overall S&P 500 Market Capitalization Weighted Index continues to climb.

This pick-up in overall breadth is a bullish turn for the market and supports the bullish market advance. While the performance gap is still wide, the improvement is important. I previously posted a chart of all stocks in the S&P 500 index that were positive for the year. At that time, less than 50% were “in the green.” As of yesterday, that number has improved to roughly 55%. However, as far as the number of stocks beating the index this year, that number is around 25%. (Click to enlarge)

The point here is that while breadth is improving, there is a very big difference between the handful of stocks crushing the market this year and those barely hanging on. It is also a different story than the S&P 500 advance/decline ratio suggests.

Stock picking remains important.

Mortgage Holders are Staying Put

The graph below comes from a recent article by Redfin. The gist of the article is that many homeowners have mortgage rates that are much lower than current market rates. Consequently, “Many would-be sellers are staying put rather than listing their home to avoid taking on a much higher mortgage rate when they purchase their next house. This “lock in” effect has pushed inventory down to record lows this spring.”

The “lock-in” effect and high mortgage rates for home buyers result in a shortage of listings and fewer sales. Per Redfin:

New listings of homes for sale and the total number of listings have both dropped to their lowest level on record for this time of year, which is fueling homebuyer competition in some markets and preventing home prices from falling further even amid tepid demand.

As if mortgage rates were not enough of a problem, also consider that nearly 60% of homeowners with mortgages have lived in their house for less than four years. So even if rates fell, many new homeowners may not be ready to move.

Courtesy Redfin:

- Below 6%: 91.8% of U.S. mortgaged homeowners have a rate below 6%, down from a record high of 92.9% in the second quarter of 2022, as noted above.

- Below 5%: 82.4% have a rate below 5%. That’s down from a peak of 85.7% in the first quarter of 2022.

- Below 4%: 62% have a rate below 4%, down from a record high (65.3%) in the first quarter of 2022.

- Below 3%: 23.5% have an interest rate below 3%, near the highest share on record. The highest was 24.6% in the first quarter of 2022.

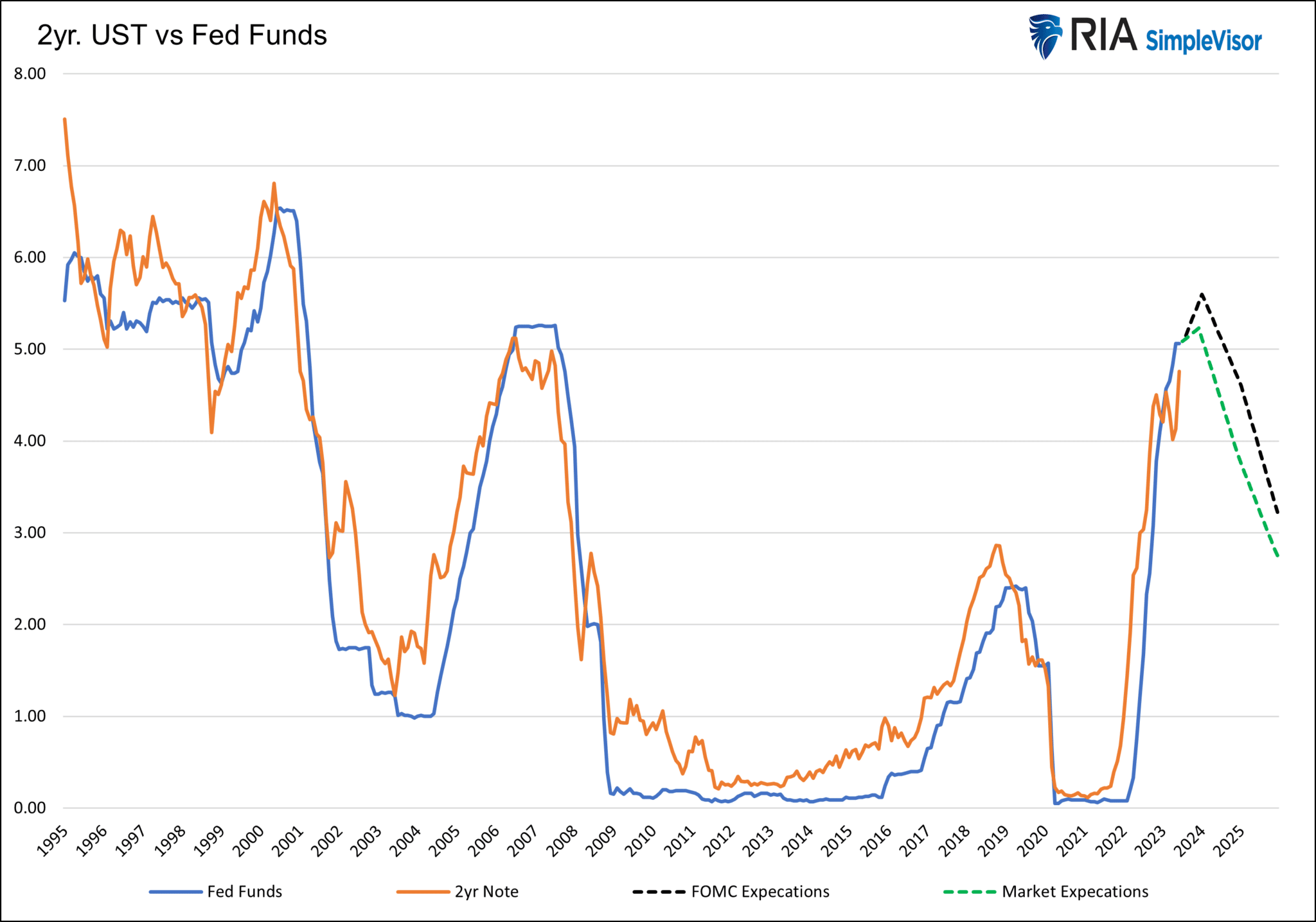

Two-Year Treasury Notes Are Looking Tasty

The graph below shows that the 2yr UST note tends to lead the Fed’s Fed Funds rate when the Fed is actively increasing or decreasing rates. This occurs because the two-year note yield is based on the current Fed Funds rate and expectations for future Fed Funds rates. As the graph shows, market and FOMC expectations for Fed Funds over the next two years are lower. Both predictions provide a reasonable expectation of two-year yields over the next two years. Of course, if the Fed cuts rates at a pace similar to the last three recessions, Fed Funds may be much lower than both expectations.

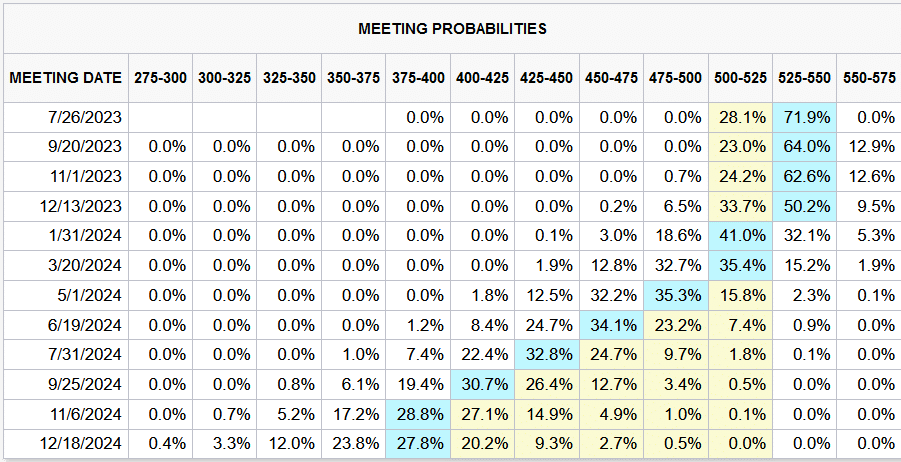

Fed Funds Futures

Following the Fed’s hawkish pause, the Fed Funds futures market implies the Fed is not cutting rates this year. If you recall, in the first quarter, Fed Funds futures implied they might cut by as much as 1.25%. Instead, as we share below, the odds of a 25bps cut by December are a mere 6.5%. At the same time, the market implies a 71.9% chance they will raise rates by another 25bps and a 12.9% chance it will increase twice by a total of 50bps. If the Fed follows the odds, Fed Funds will end the year at 5.25-5.50% and cut rates by 1.50% during 2024. The most recent Fed forecast, as shared in yesterday’s Commentary, expects Fed Funds to end 2024 at 4.60%. The market implies the odds of that occurring are 2.7%.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.