Ivana Trump, the first wife of Donald Trump, was recently found dead in her Manhattan residence. She was 73.

Known throughout her life as a dynamo socialite and dealmaker in heels, her death from a blunt trauma from a fall down the stairs in her multi-story townhome, was a shock to residents who perceived her as vibrant and full of life. So, her passing got me thinking about Ivana Trump’s money lessons for older Americans.

Listen, it’s tough to age, but don’t let the process get you down. It’s too hard to get back up! Get it?

Seriously, a great challenge is an acceptance of growing older. Aging can be a tough pill to swallow. Especially for those who are known for the travails of their younger days. I have friends who explain as they age, they ‘disappear.’ I hate to hear this.

Personally, I’m living my best self and wouldn’t change a thing. However, Ageism is a real societal challenge. Based on numerous surveys, white papers, and reports from health organizations, those who are 60 and older are subject to negative stereotyping and discrimination in the workplace. Also, to younger generations, they do disappear in a manner of speaking.

But I have news for you. I think that’s about to change for you ‘seasoned’ folks.

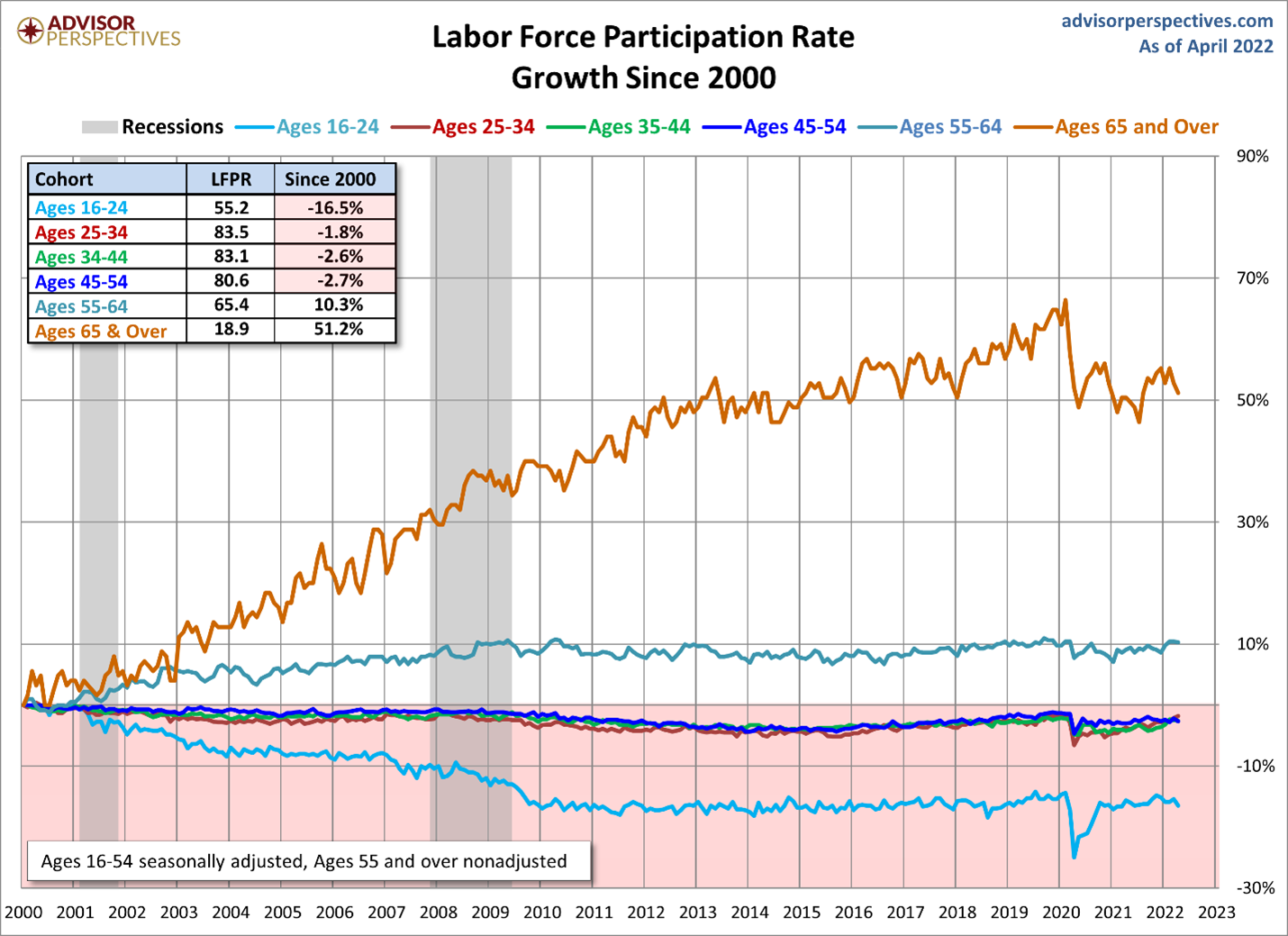

During the pandemic, the Labor Force Participation Rate collapsed and has yet to recover. For those who need a reminder, the LFPR represents the people age 16 and older employed or seeking employment. Older Americans decided to accelerate retirement. Younger cohorts decided to go out on their own or sit back – satiated by government stimulus.

I think many older Americans will seek to unravel their retirement decision and return to the workforce. Also, I believe they’ll be welcomed with open arms by employers eager for a generation that is timely, responsible, and willing to work!

Let’s kick Ageism where it hurts. Right in the work ethic!

One money lesson I’ve learned from Ivana Trump about older Americans is that the entire world is wrinkling.

According to Peter Zeihan in his latest book – The End of The World is just the Beginning, population, and spending shrinkages are realities the entire globe must embrace. Demographics outline that mass-consumption-driven economies have already peaked.

By 2030, the world will be populated with twice as many retirees. Therefore, we all better internalize the fact that we’re getting older and financially and emotionally prepare accordingly. Long-term, poor demographics are deflationary.

In my opinion, Ivana Trump refused to accept aging. Thus, I consider Ivana Trump’s money lessons for older Americans applicable to all of us.

Regardless of her immense wealth, she must have encountered anguish when it comes to getting older. Sure having money doesn’t hurt. Suffering in luxury isn’t bad. However, aging doesn’t care about a net worth statement.

Denial of aging is real and one of Ivana Trump’s best money lessons for older Americans.

Who needs comprehensive studies to understand that denial of getting older is a reality? I see it in myself as I dramatically changed my diet and amped up my physical workouts years ago to fight or slow the inevitable.

Frankly, my graying hairline stresses me out.

I engage with people regularly who aren’t ready to deal with how someday they may move slower, forget things often and work through periodic illness or injury. Older clients and their adult children have a tough time facing that mom and dad are grayer, smaller, and frailer than they used to be.

Per a July 2022 analysis from the Center for Retirement Research, older Americans and retirees poorly assess the risks they face in retirement. Health and longevity risks (the risk of living longer than expected and exhausting financial resources) are underestimated.

Per the study: Perceived longevity risk and health risk rank lower because retirees are pessimistic about their survival probabilities and often underestimate their health costs in late life.

I cannot tell you how many clients inform me how sure they are about dying early. How do they know? So, I always ask the following question –

“What if you don’t?”

Ivana Trump’s friends were concerned about her home’s beautiful but dangerous staircase. They were worried about her falling. She had an elevator and rarely used it. The stairs at her home were steep, the carpet was worn. Although she had trouble walking, she regularly took the stairs. She had the money to remove or replace the carpet; the elevator would have been perfect, but she rarely used it.

Why?

In her halcyon days, Ivana was New York royalty. Young, vibrant. She could accomplish anything. How can someone like that stare into the mirror and face vincibility? How can you? Can I? Acceptance is the first step to a rich life as we age, to feel comfortable in different but richer skins.

That acceptance opens the door to preparation – eating right, exercising regularly, and preparing for the risks of aging through comprehensive planning and open communication with family and friends.

If I deny aging, then I’ll force everyone around me to deny it too. Or, at the least, family members and friends will discuss issues concerning me behind my back. Who wants that? Older Americans must be open to listening.

This leads to my next financial lesson for older Americans from Ivana Trump.

Communication. Another one of the money lessons Ivana Trump has for older Americans.

I wonder how many times Ivana was advised (perhaps delicately) by Ivanka and the other kids to update her place for aging, move to a one-story, or take the damn elevator. Whatever it is, would Ivana listen or just carry on like it was the 1980s? In her mind, it may have been decades ago, but her aging body lived in the here and now.

There’s a nuance and empathy to communicating with older loved ones.

Remember, they were young like you once. Listen to your special older Americans. Never be condescending. A good idea may be to bring in an objective third party such as your financial advisor to assist with the discussions. I’ve witnessed adult children infantilize their parents, and that never works. Imagine approaching Ivana with that tone! Not good!

Remember, even mild cognitive impairment can drive a communication wedge between you, and your aging loved one. However, don’t give up sparking conversation. I work with clients who consistently need to nuance their speech with their parents. They get their points across eventually. Impaired older relatives eventually take action, but the process is like chipping away at an iceberg with a butter knife.

Don’t give up!

Genworth, a leader in long-term care insurance and research, maintains an impactful Conversation Starters page with helpful tips about what to talk about and how to maintain a dialogue. Check it out.

Use your financial plan to motivate others.

How can you discuss long-term care issues with loved ones if you’re personally in denial about aging? A risk mitigation plan as part of a comprehensive financial strategy validates your commitment to preparation. Actions forge your conversations with credibility.

According to AARP’s most recent Home and Community Preference Survey, 77% of adults 50 and older want to remain in their homes or age in place. The number has been consistent for over a decade. Aging in place requires planning – whether it’s to eventually downsize to a one-story home, renovate kitchen and baths or install easy access ramps for items of mobility such as wheelchairs. It would be worth practicing financial openness and sharing this information with aging parents. In other words, if you’re preparing for these expenses, they should be too.

Don’t forget long-term care insurance as one of Ivana Trump’s money lessons for older Americans.

Ivana didn’t need long-term care insurance. You probably need to consider it.

Unfortunately, nearly half of individuals who apply for traditional long-term care insurance after age 70 have their applications declined by an insurer, according to Jesse Slome, director of the American Association for Long-Term Care Insurance. However, loved ones in good health in their 50s and 60s can still consider long-term care insurance. The sweet spot for looking into long-term care coverage is generally between ages 55 and 65, per Jesse Slome.

Three out of every five financial plans I create reflect deficiencies in meeting long-term care expenses. Medical insurance like Medicare does not cover long-term care expenses – a common misperception. Nearly 60% of people surveyed in various studies falsely believe that Medicare covers long-term care expenses.

The Genworth Cost of Care Survey has been tracking long-term care costs across 440 regions across the United States since 2004.

Genworth’s results assume an annual 3% inflation rate. In today’s dollars, a home-health aide who assists with cleaning, cooking, and other responsibilities for those who seek to age in place or require temporary assistance with daily living activities can cost over $54,912 a year in the Houston area. We use a 4.25-4.5% inflation rate for financial planning purposes to reflect recent median annual costs for assisted living and nursing home care. Candidly, I fear that I’ll need to increase this inflation rate in 2023.

As I examine long-term care policies issued recently vs. those 10 years or later, it’s glaringly obvious that coverage isn’t as comprehensive, and costs are more prohibitive.

One option is to consider a reverse mortgage, specifically a home equity conversion mortgage. The horror stories about these products are overblown. The most astute planners and academics understand how incorporating the equity from a primary residence in a retirement income strategy can help with the burden of long-term care costs. Those who talk down these products are speaking out of lack of knowledge and falling easily for pervasive false narratives.

Reverse mortgages have several layers of costs (nothing like they were in the past), and it pays for consumers to shop around for the best deals. Also, to qualify for a reverse mortgage, the homeowner must be 62, the home must be a primary residence, and the debt limited to mortgage debt. There are several ways to receive payouts.

One of the smartest strategies is to establish a reverse mortgage line of credit at age 62, leave it untapped, and allow it to grow along with the home’s value.

The line may be tapped for long-term care expenses if needed or to mitigate the sequence of poor return risk in portfolios. Simply, in years where portfolios are down, the reverse mortgage line is used for income while portfolios recover. Once assets recover, rebalancing proceeds or gains may be used to repay the reverse mortgage loan, restoring the line of credit.

RIA’s approach to helping older Americans age comfortably in place.

Our planning software allows our team to consider a reverse mortgage in the analysis. Those plans have a high probability of success. We explain that income is as necessary as water regarding retirement. For many retirees, converting the glacier of a home into the water of income using a reverse mortgage will be required for retirement survival and especially long-term care expenses.

Ivana Trump’s money lessons for older Americans are lessons for us all, regardless of age.

Planning to age gracefully and healthfully will lead to a prosperous retirement attitude.

As George Burns said: You can’t help getting older, but you don’t have to get old.

The longer I live, the more I realize how true that quote is.