Our recent article, Why Are Bond Yields Rising, explains that the recent 1% increase in yields, as shown below, is almost entirely due to negative sentiment. As we wrote, the bond market calls sentiment the term premium. Of the 1% yield increase, only 10% is due to fundamental factors, leaving 90% a function of bond investor concerns. Consequently, the term premium is at its highest level since at least 1990, and it’s perched three standard deviations above its norm. The article focuses on two culprits driving the premium: rising deficits and inflation. A Twitter user replied to our article saying, “It’s the Dollar, stupid!” Despite the rudeness, he is correct; the rising dollar is also to blame.

As such, let’s discuss the recent strong correlation between the appreciating dollar and rising yields and the reasons for the relationship.

The Dollar And Yields – Historical Context

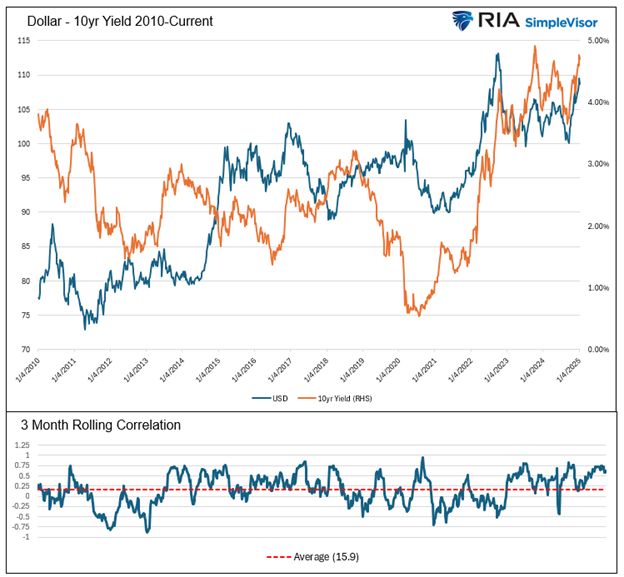

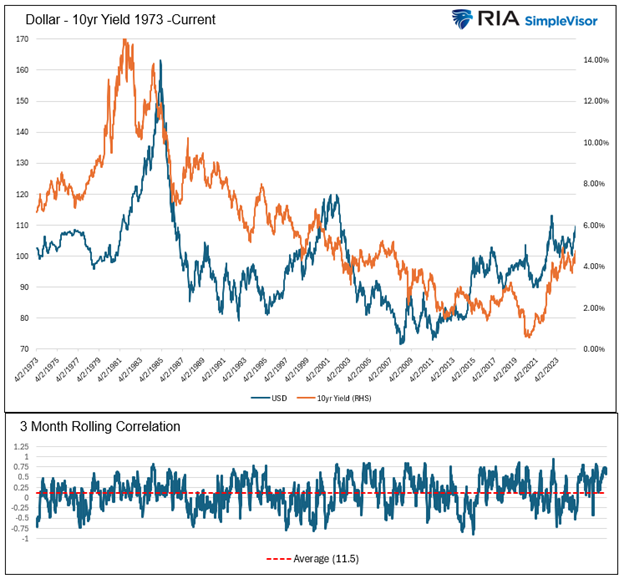

The graphs below chart the 10-year UST yield and US dollar over three different time horizons. Furthermore, we show the three-month rolling correlations for statistical context to the relationship.

The first graph, covering the last two years, shows a significant statistical relationship between the dollar and yields. Yields and the dollar over this period are not only visually tracking each other closely but are statistically as well. The rolling correlation has averaged 44.5% and, more recently, around 75%.

The second graph, spanning the post-financial crisis to the present, and the third, dating back to 1973, have positive correlations over their respective periods, but the relationships are not statistically significant. Furthermore, the correlation constantly shifts back and forth between positive and negative.

The first graph may lead some investors, as it did our Twitter commenter, to believe the dollar’s trend is crucial to forecasting yields. The other graphs show this is not necessarily true. A positive or negative relationship can persist for months or longer, but the likelihood of the recent strong positive relationship continuing is fleeting with time.

With that graphical context, let’s better understand what may be responsible for the recent strong positive relationship.

The Reserve Currency

The US dollar is the world’s reserve currency. That means that most international trade is transacted in dollars, whether a US-based customer is involved or not. Thus, the dollar’s value is a determinant of foreign economic activity. Moreover, many nations hold dollar reserves to transact more efficiently. Reserves are used to facilitate trade and, for liquidity purposes, primarily invested in Treasury securities. Lastly, many foreign nations and corporations borrow in US dollars because the US offers the cheapest financing in most cases, as it has the most liquid capital markets by a long shot.

Let’s dig into those statements to appreciate the impact they may be having on the dollar.

For more information on the dollar and its importance to global economic activity, we share articles we have written on the topic:

Our Currency, The World’s Problem Part 1 & Part 2

The Dollars Death, Not So Fast Part 1 & Part 2

International Trade in Dollars

The value of the dollar versus other currencies has a direct impact on foreign economies.

Consider, for example, a German exporter of widgets. If the euro’s value versus the dollar fell from 1.10 to 1.00, the widget producer would get paid 10% less from dollar-paying customers due to the euro’s decline. Similarly, the price of the widget would decline 10% for the purchaser.

Therefore, as we have recently been experiencing, an appreciating dollar weighs on foreign revenue and economic growth for exporters. The US runs consistent trade deficits; thus, recent dollar strength negatively impacts the economic activity of those countries exporting to us.

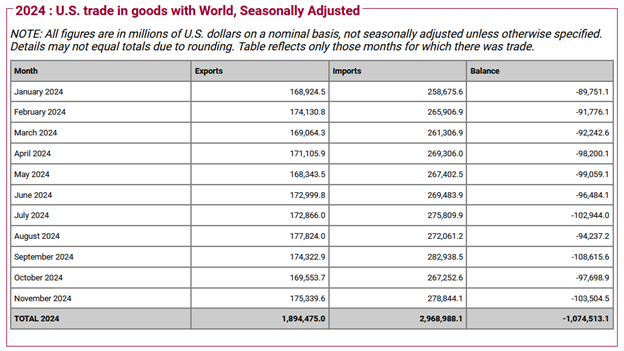

The table below, courtesy of the US Census Bureau, shows that through the first 11 months of 2024, the US has imported over $1 trillion more in goods than we have exported.

The US has sizeable trade deficits with the following nations and block of nations:

- China $270 billion

- European Union $213 billion

- Canada $55 billion

- Japan $62 billion

- Mexico $157 billion

Those nations and regions running trade surpluses with the US are witnessing weaker economic growth than would otherwise have had the respective currency relationships with the dollar stable. Furthermore, weakness in those nations and relative economic strength in the US incentivize foreign investors to buy US assets. Moreover, it often rewards US investors for investing their money domestically instead of in international assets. Such investment flows feed dollar strength to the detriment of other currencies.

Additionally, some foreign exporters hedge against adverse currency movements. While hedging helps protect profits against currency changes, it feeds the stronger dollar.

The economic and hedging impact of an appreciating dollar strengthens the dollar. Then, circularly, weak foreign economic activity and hedging further strengthen the dollar. Dollar strength begets dollar strength until the trend flips.

Dollar Reserves

To maintain the purchasing power of a nation’s reserves against a stronger dollar, the country will add to its reserves, thus owning more dollars.

As we noted in the prior section, here, too, dollar strength begets dollar strength.

Foreign Dollar Borrowing

When most foreign entities borrow in US dollars, they are not only responsible for the principal and interest payments but for the change in the currency value over the life of the debt.

Thus, if the dollar rose 10% versus a borrower’s home currency, the borrower must come up with an additional 10% of their currency to convert to dollars to make good on the interest and ultimate principal repayment.

Simply, a rising dollar pushes borrowing costs higher in foreign countries. Higher effective interest expenses result in reduced borrowing, which reduces liquidity and often weakens economic activity. Borrowers worried about rising debt costs due to the dollar may pay back their debt early. Doing so requires them to sell their home currency to buy the dollars necessary to pay it back.

Again, a similar theme: dollar strength begets dollar strength.

Currency Intervention

Outside of trade and trade-related activities, other factors can impact currency values. At times, central banks’ role in regulating currency values is among the most significant.

Central banks are notorious for intervening in the currency markets. Given the massive role currency values can have on economic and liquidity conditions, they aim for stable currency values versus the dollar. As an aside, Switzerland and Saudi Arabia peg their currency to the dollar. Such a strategy entails consistent intervention.

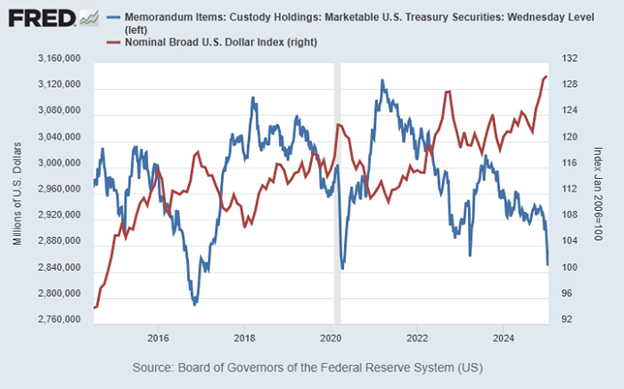

Today, it’s highly likely that foreign nations are selling dollars to support their depreciating currency. All dollars are invested. Thus, to sell dollars, they must sell assets. As we noted earlier, in most cases, the reserves are invested in Treasury securities. Accordingly, central bank intervention and associated selling of Treasury securities may push yields upward and keep dollar gains less than they otherwise might be. The graph below adds credence to the hypothesis.

Market Sentiment

Traders’ perceptions and market sentiment can drive a temporary but sturdy relationship between bond yields and the dollar. Such actions can create a feedback loop where shifts in one lead to movements in the other. As such, while some drivers of dollar strength may not directly affect bond yields, trader perceptions of the relationship between yields and the dollar may currently be the most significant driver of yields.

If the market believes a relationship exists, whether logical or not, the market will trade that relationship until it breaks.

Safe Havens

The dollar and Treasury bonds are both considered safe havens. In times of financial distress, money from abroad flocks to the dollar and often into Treasury bonds. Similarly, during distress, domestic investors divest foreign assets, repatriate their money back to the dollar, and frequently park the cash in the safety of Treasury bonds.

Accordingly, the rising dollar is causing economic and liquidity problems in foreign nations. If it persists, the dollar may catch a safe haven bid. Bonds could be the key beneficiary of the flow to dollars. In such a case, while the dollar may continue to rise, we may witness the positive relationship with bonds deteriorate as yields decline in step.

Summary

There is credibility to the fact that the strong dollar drives higher yields. But it’s also important to note that market psychology does as well. Traders are convinced that the dollar and bond yields are linked and will trade the pair accordingly.

However, sentiment will change at some point, traders will exit the trade, and the relationship will splinter.

We remind you that dollar and bond yields significantly influence the global economy. Thus, recent movements of both are likely to trigger economic and financial market changes in the opposite direction, which, in turn, could put pressure on the dollar and force lower yields.

Outsized returns lay in wait for those contrarians able to spot the change in sentiment and momentum.