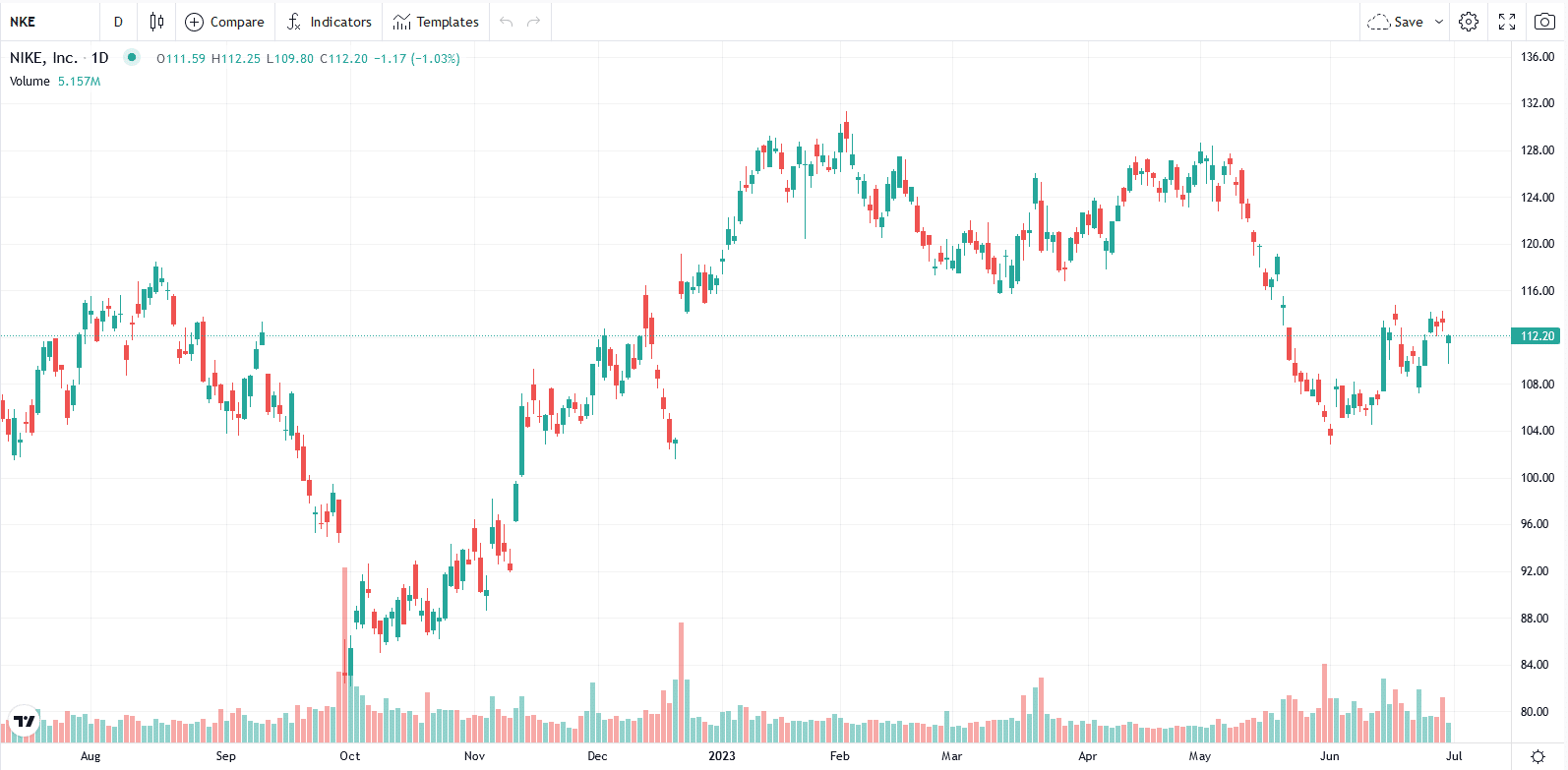

Last week Nike reported a fourth-quarter net income of .66 cents a share, down from .90 cents in the prior fourth quarter. Interestingly revenue rose by 4.8%. The culprit was a 1.40% decline in its profit margin. The company blames price markdowns and higher input costs. As we discussed with General Mills in last week’s Commentary, Nike also struggles to pass on higher inflation to its customers. Per MarketWatch: Nike said gross margins slipped 140 basis points to 43.6%, dragged by “higher product input costs and elevated freight and logistics costs, higher markdowns and continued unfavorable changes in net foreign currency exchange rates.” As we share below, Nike stock traded lower on the news but not materially. While its profits were weak, they were close to market expectations.

Looking ahead to the earnings slate that will start in a few weeks, investors will be looking to see if customers are finally hitting a limit with inflation. After absorbing higher costs, they are finally starting to curtail spending and shop around for deals. As we noted a month ago, Costco reported that sales of their own clothes brand Kirkland and cheaper meats like pork and chicken saw a pickup in sales versus higher priced alternatives. The other earnings line item that will be important to follow is interest expense. Most companies will be forced to refinance at higher interest rates as debt matures. How will such cost increases eat into profits? The answer will be company dependent based on when their new and rollover borrowing needs occur.

What To Watch Today

Economy

Earnings

- No Earnings Releases Today

Market Trading Update

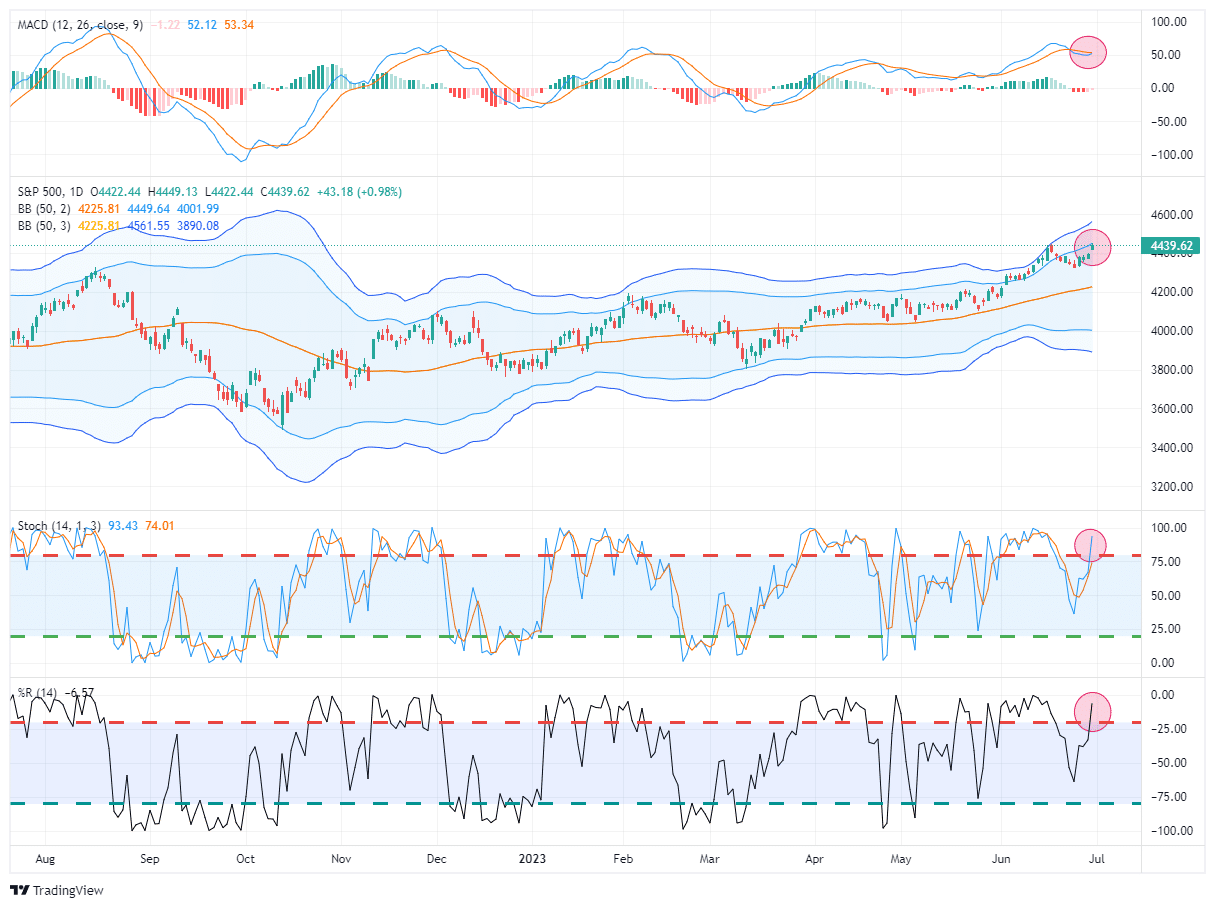

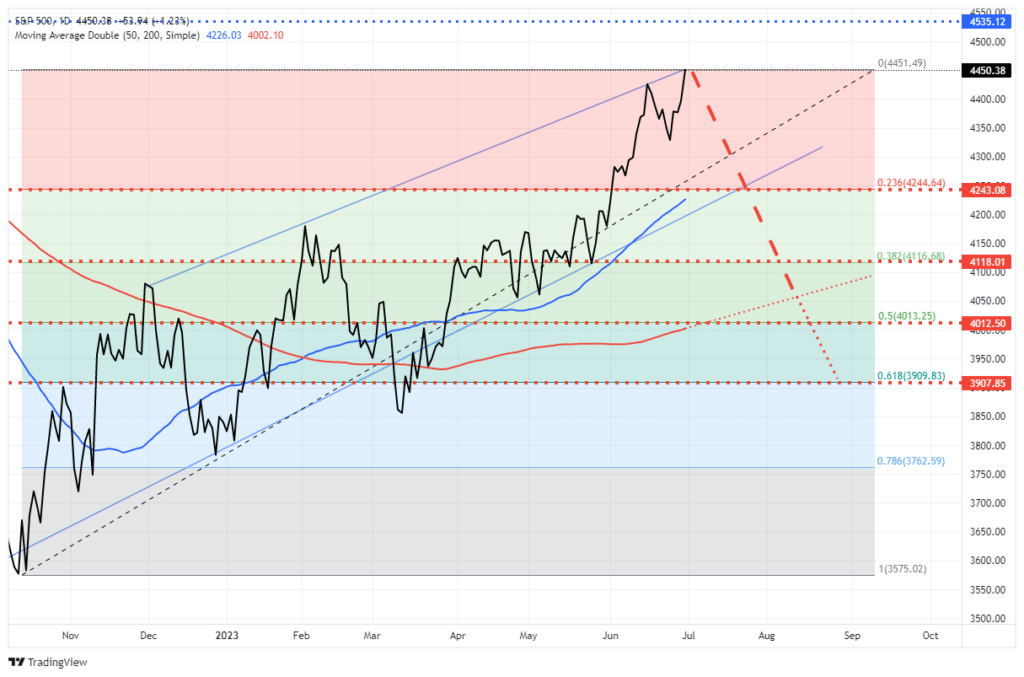

Last week we noted that the correction had triggered a market sell signal. As stated, when triggered from fairly elevated levels, these sell signals tend to suggest a more protracted correction or consolidation. However, the correction was shortlived as a successful test of the 20-day moving average brought traders back into the market. In a bullish advance, it is not uncommon for buy and sell signals to flip back and forth at elevated levels.

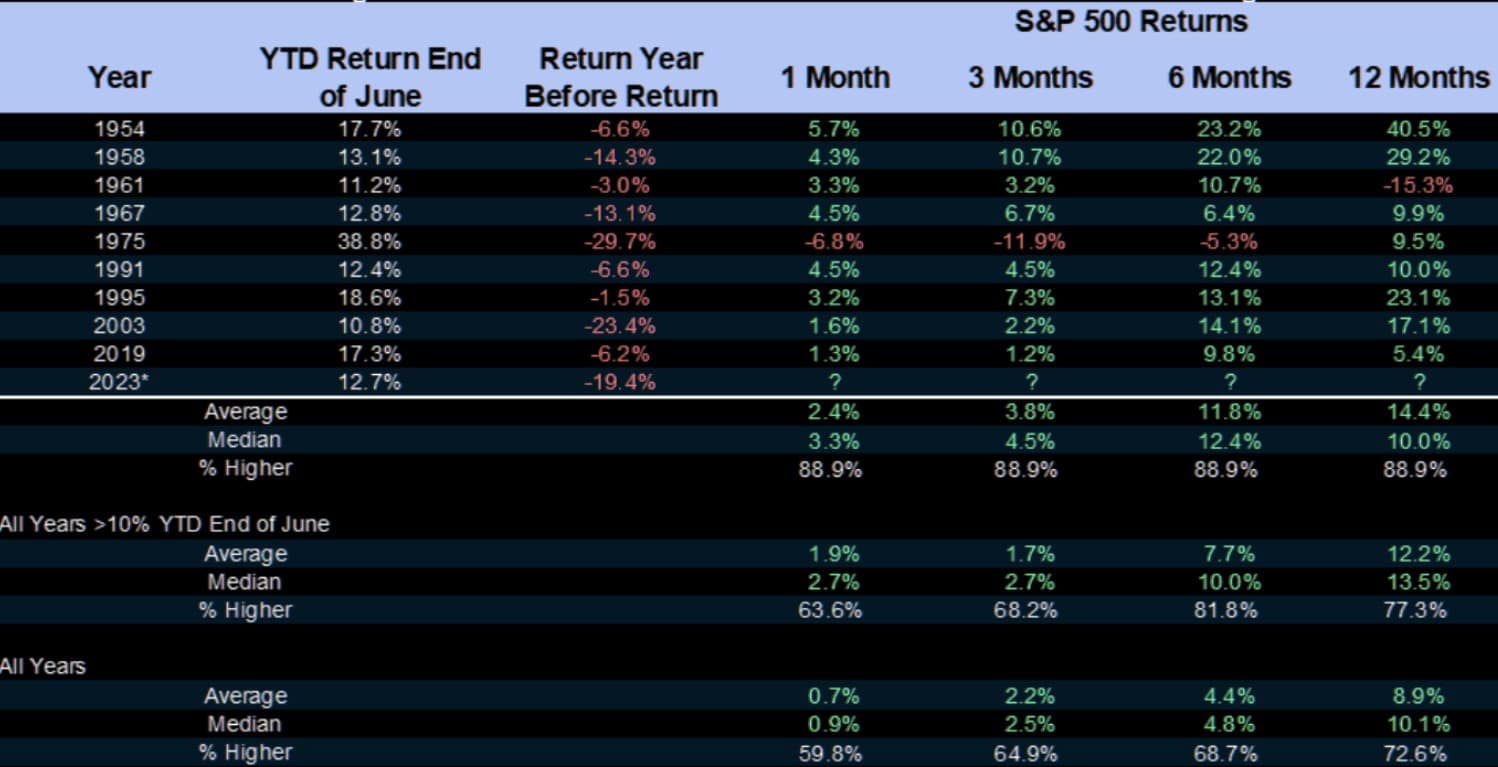

With the end of the quarter behind us, portfolio managers are now trying to play “catch up” with returns over the next six months. As shown in the table below, the second-half returns tend to be strong when the market is up 10% in the year’s first half.

With bullish optimism quickly returning to the market, the pressure to chase performance from the “Fear Of Missing Out” will continue to provide a “bid” under stocks for now.

However, such does not remove the potential for a 5-10% correction. Such corrections are entirely normal within any given year and will provide the best entry point to increase equity exposure near term. Using Fibonacci retracement levels, investors should consider adding exposure at 4250, down to the 200-DMA. A violation of the 200-DMA would suggest a larger corrective process at work, most likely coinciding with some market-related event.

While such an event is unlikely, we can not entirely dismiss the risk of a larger contraction, given the more extreme deviations that currently exist from longer-term moving averages. What would cause such a contraction? Such would be an exogenous and unexpected event that changes market participants’ complacency about risk.

The Week Ahead

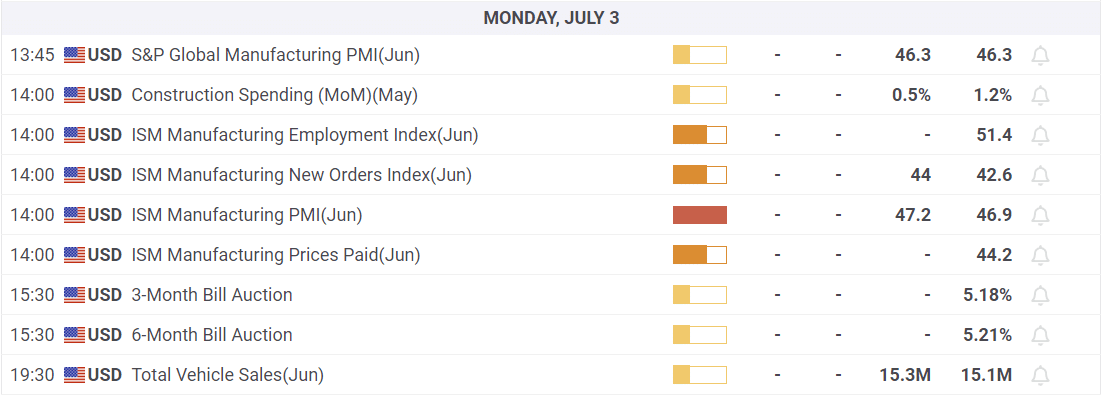

Employment data will garner the economic headlines this holiday-shortened week. After rising by 0.3% last month, the unemployment rate is expected to dip by 0.1%. Payrolls are expected to cool from 339k to 250k. While slower, 250k is still robust growth. JOLTs and ADP on Thursday will shine further light on the labor market.

The ISM manufacturing report on Monday and the services report on Thursday will be closely followed for indications of prices and labor. The ISM manufacturing index has been below 50 since last October. A reading below 50 denotes contraction. Despite weakness in manufacturing, services have stayed above 50, signaling expansion. However, the last service reading was just a hair above 50 at 50.3. Given the services sector accounts for about three-quarters of economic activity, many believe the manufacturing data is not a precursor to a recession. Might a decline below 50 change some of these opinions?

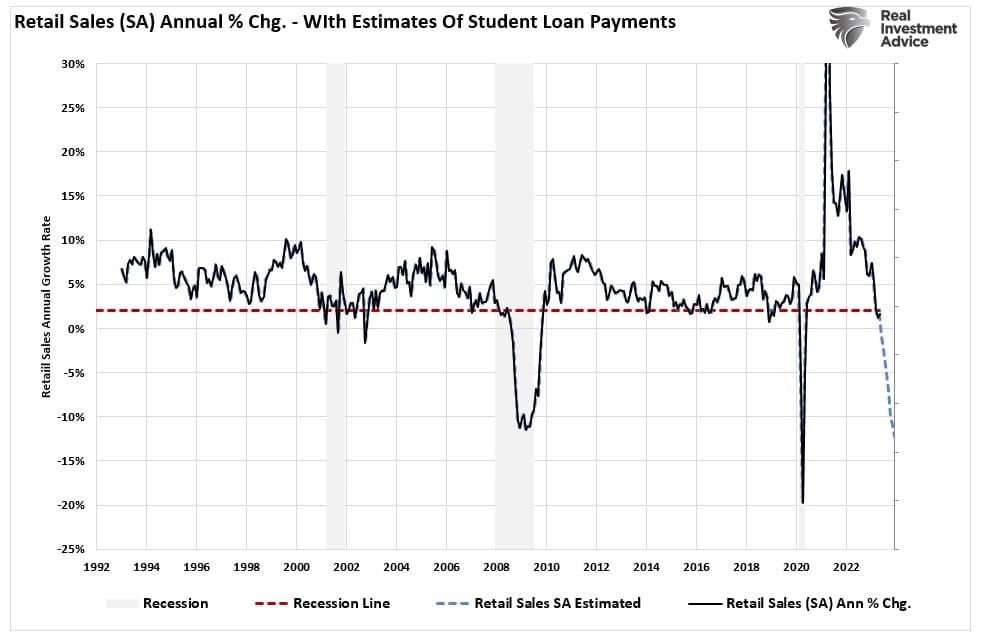

Student Loan Repayments Are Starting Back Up

One of the more challenging economic forecasting issues we have dealt with in the aftermath of the pandemic is calculating when and how the surge in interest rates will dampen economic activity. Part of the problem, as we have discussed, is forecasting financial lags. Simply it takes time for higher interest rates to affect new and existing borrowers. The pandemic-related stimulus was enormous and difficult to appreciate how and when it was spent. One such stimulus, initiated in March 2020, was the moratorium on student loan repayments.

That stimulus will disappear next month, barring unlikely Supreme Court action. To help quantify how the moratorium on payments benefited the economy and how the coming lifting of said moratorium will hamper economic activity, we wrote Student Loan Repayments, Will It Start The Recession?

Per Barclays:

“Compared to a median pre-tax personal annual income of ~$57k, this payment represents an approximate 8% headwind to monthly income. In aggregate, this amounts to an “additional” (or rather, original, as the payments were there and then three years ago, they just stopped) $15.8bn in monthly payment for federal student loans affecting approximately 15.5% of the U.S. adult population (and 32% of the 25- to 34-year-old cohort).”

If Barclay’s Bank is correct in its assumptions, removing the student loan moratorium on payments will significantly impact retail sales. The chart below projects the average retail sales growth less the student loan payments. If Barclay’s is correct in its assumptions, the impact on retail sales could be significant.

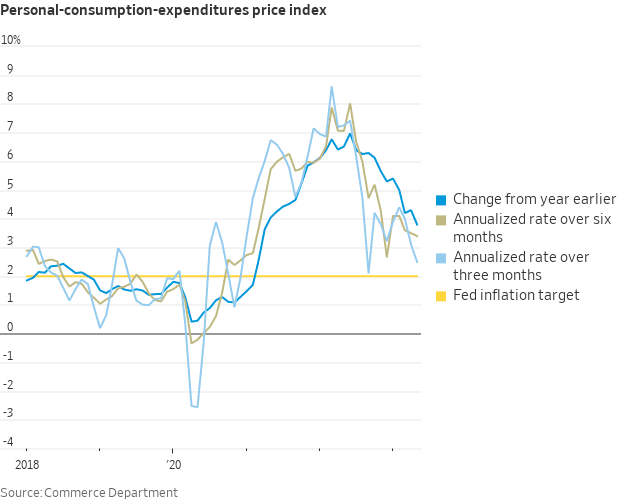

PCE Inflation Continues Downward

PCE, the Fed’s preferred gauge of inflation, continues to decline. The year-over-year reading was 3.8%, its lowest level in over two years. The monthly change was +.13%, which annualizes to 1.56% inflation.

Powell has mentioned that his favorite inflation indicator is core PCE Services Ex-Shelter. In 2023, the 3-month annualized rates by month for this gauge are January 5.0%, February 5.2%, March 4.8%, April 4.4%, and May 3.8%. Yes, it’s still high, but the trend is indeed favorable.

BofA had the following advice following the data:

“.. our advice for the PCE deflator release today is simple. Look past the headline, the core, the super core, and the super-duper core. Focus instead on the trimmed mean. The latest releases show easing on a monthly basis. If that continues, it would be super news.”

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.