In yesterday’s Commentary, we shed light on why permits and starts for new house construction were increasing rapidly despite high mortgage rates. To wit: “Consequently, it appears that the stagnant market for existing homes is creating an opportunity for builders to fill the void and meet some of the demand.” As a result, we theorized that, eventually, lower mortgage rates would make selling existing houses more financially practical. As such, “the added supply of existing houses with the coming supply of new homes may create a glut of houses on the market. The only question at that point- is the pent-up demand to purchase homes strong enough to meet the supply.“

After writing that commentary, we stumbled across data that offers additional concern about the potential of a growing supply of houses on the market and consequently increased chances for lower home prices. The following graph from John Burns Research and Consulting shows it is now more expensive to own a house than rent at any time in at least 20 years. Further rental prices may come under pressure shortly due to robust multifamily construction. Per CBRE, “More than 750,000 multifamily units are currently under construction—the highest amount since the housing boom of the 1980s.”

Lower mortgage rates should help close the own versus rent financial gap. But it also allows “trapped” sellers to put their houses on the market, potentially pressuring house prices.

What To Watch Today

Earnings

Economy

Market Trading Update

As noted in yesterday’s commentary, seeing the market bounce yesterday after several days of selling pressure heading into the month’s end was unsurprising. While Technology stocks got sold off on Monday, they rallied back on Tuesday as investors continued to buy dips aggressively. Furthermore, the rally yesterday held the first level of important support at the 20-DMA, keeping the current market momentum intact.

Currently, the market is still overbought and on a MACD sell signal which suggests more consolidation or corrective action is likely. Furthermore, despite the recent pullback, the market remains well deviated from the 50- and 200-day moving averages which suggests that at some point this summer, we will see a deeper correction.

For now, there is no reason to be bearish on the market, so continue to use pullbacks to increase exposure accordingly.

Auto Prices are also at Risk

Yahoo Finance recently wrote an article titled New Car Market: Prices are About to Plummet. The article cites a UBS report forecasting global car production will exceed sales by 6% this year. Accordingly: “leaving an excess of five million vehicles that will require price cuts to get sold off the lots.”

Per the article:

“The price war has already started unfolding in the EV space, and we expect it to spread into the combustion engine segment [during the second half of 2023].”

Meanwhile, there is already evidence that car prices across all segments have softened. The latest data from Cox Automotive, released on Friday, April 7, showed that wholesale used-vehicle prices in March fell 2.4% from a year earlier, although they did tick up 1.5% from the previous month.

A March 23 report from Kelley Blue Book found that new vehicle prices dropped for three straight months, and that “it’s starting to look like a sustained trend.” Even so, prices remain “historically high.”

The graph below from Cox Automotive shows that new car prices have fallen slightly. However, they remain well above their pre-pandemic trend.

Hedge Funds Betting on “Higher for Longer”

Per the most recent data from the CFTC, “Large speculator and hedge fund” short positioning in 2-year U.S. Treasury note futures are at their most extreme level since at least 1990. It appears those investors are betting heavily that the Fed will raise rates further and keep short-term rates higher for longer. We are working on an article showing investors tend to underestimate the Fed. Does this mean investors do not appreciate the Fed’s possibility to cut rates? The second graph, from that coming article, shows the market continually underestimates the Fed and during rate cuts by 2-3%.

Corporate Profits Heavily Rely on Monetary & Fiscal Policy

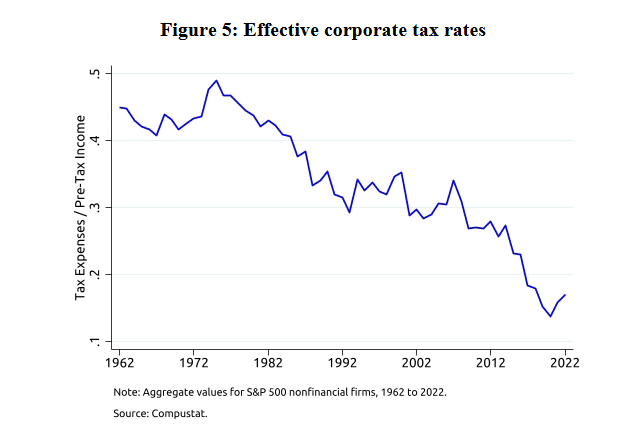

“Lower interest expenses and corporate tax rates mechanically explain over 40% of the real growth in corporate profits from 1989-2019.”

The sentence above is from a Federal Reserve white paper written by Michael Smolyansky. Since 1980, corporate interest rates have fallen from the low double digits to the low single digits. At the same time, the amount of leverage corporations employed more than doubled. Further aiding corporate profits, effective corporate tax rates fell from nearly 50% of pre-tax income to nearly 15% from 1962 to current. While lower taxes and interest rates signficantly boosted profits, neither will be able to help much going forward.

Per the article, the implications for the future are not good.

It may be tempting to assume that the exceptional stock market performance over the last three decades will continue indefinitely. My analysis, however, indicates otherwise. Both stock returns and corporate profit growth are very likely to be substantially lower in the future. This conclusion follows from the minimal assumption that interest rates and effective corporate tax rates have very little scope to fall below 2019-levels

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.