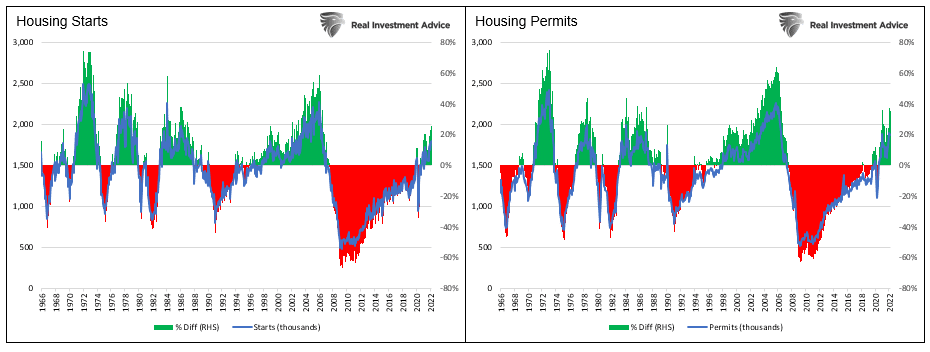

Despite mortgage rates nearing 5.50%, new homebuilders continue to file for building permits, and they are starting construction of new houses at a robust pace. New Housing Starts for March beat expectations and edged higher than last month, with an annual rate of 1.793 million new homes going under construction. Building Permits, an indicator of future housing starts, also speak to confidence among homebuilders.

There are permits for 1.873 million houses, up from 1.859 last month. The graphs below provide some historical context for the new homebuilder data. Both starts and permits are moderately above the 50-year average but below prior peaks. It is also worth noting that all periods in which homebuilders exceeded the average were followed by lengthy periods in which they fell short.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended April 15 (-1.3% during prior week)

- 8:30 a.m. ET: Existing home sales, March (5.78 million expected, 6.02 million in February)

- 2:00 p.m. ET: Federal Reserve releases Beige Book

Earnings

Pre-market

- Anthem (ANTM) to report adjusted earnings of $7.73 on revenue of $37.47 billion

- Nasdaq (NDAQ) to report adjusted earnings of $1.95 on revenue of $892.00 million

- Baker Hughes (BKR) to report adjusted earnings of 19 cents on revenue of $5.00 billion

- Procter & Gamble (PG) to report adjusted earnings of $1.29 on revenue of $17.73 billion

- Abbott Laboratories (ABT) to report adjusted earnings of $1.47 on revenue of $11.00 billion

Post-market

- CSX Corp. (CSX) to report adjusted earnings of 37 cents on revenue of $3.31 billion

- Kinder Morgan (KMI) to report adjusted earnings of 28 cents on revenue of $3.72 billion

- Alcoa Corp. (AA) to report adjusted earnings of $2.84 on revenue of $3.44 billion

- Tenet Healthcare (THC) to report adjusted earnings of $1.03 on revenue of $4.70 billion

- Crown Castle International (CCI) to report adjusted earnings of $1.87 on revenue of $403.60 million

- United Airlines (UAL) to report adjusted losses of $4.23 on revenue of $7.67 billion

- Steel Dynamics (STLD) to report adjusted earnings of $5.66 on revenue of $5.32 billion

- Equifax (EFX) to report adjusted earnings of $2.14 on revenue of $1.33 billion

- Tesla (TSLA) to report adjusted earnings of $2.27 on revenue of $17.92 billion

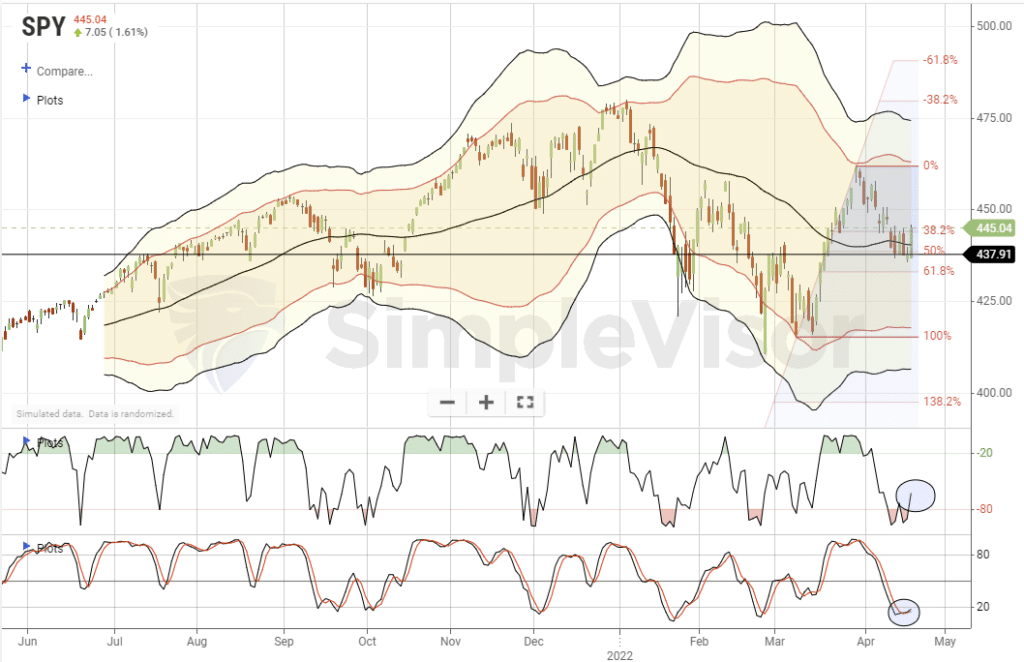

Market Trading Update

As noted yesterday, with “Tay Payment Day” behind us, the market staged an exceptionally strong reflexive rally as extremely light positioning, and negative sentiment created an optimal setup for a short-covering rally. With earnings season now underway, and a buy signal triggered yesterday, we could see a rally back to the highs from a couple of weeks ago. It won’t take long to reverse the oversold condition so the trading window is likely limited heading into the Fed meeting on May 3-4th.

The recent report by Netflix is souring the party this morning, however, if the market can hold the 50-dma and reestablish support, the potential for a further rally remains.

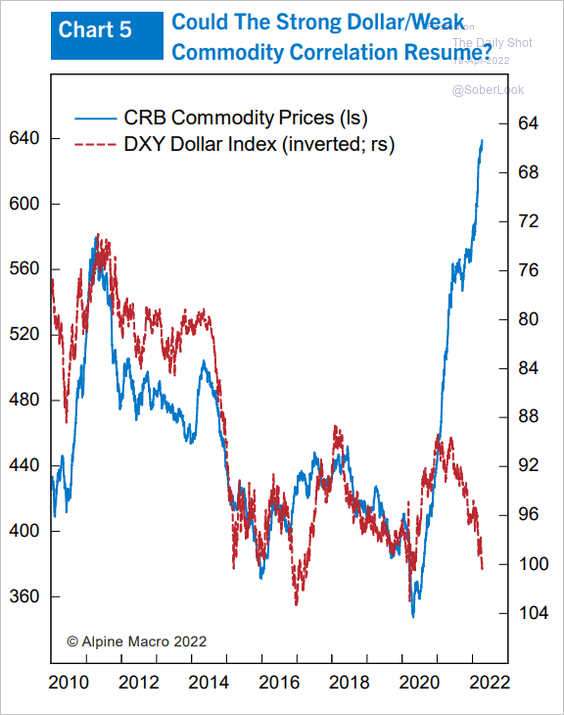

Another Strange Divergence

Last week we noted a few strange divergences in the markets. We add another to the list today, the dollar and commodity prices. The Daily Shot graph below shows the strong negative correlation between the CRB commodity index and the dollar. Starting in early 2021, when inflation started to rise rapidly, the correlation broke down. Over the last year and a quarter, the dollar has increased by over 10%, while the CRB is up about 50%. The trend may continue for a while, but the divergence will likelyclose once global economic activity stalls.

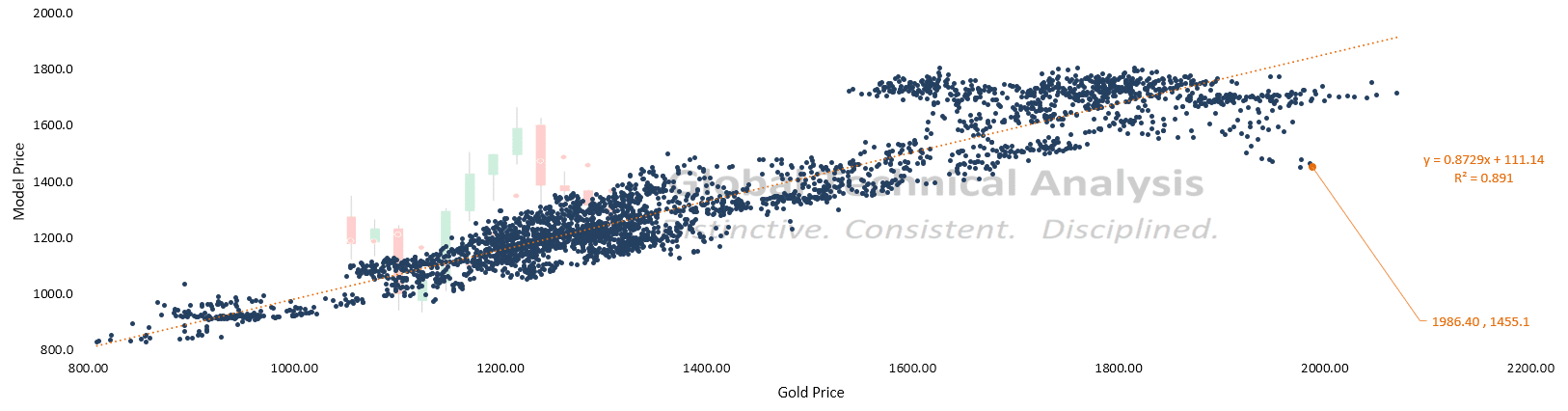

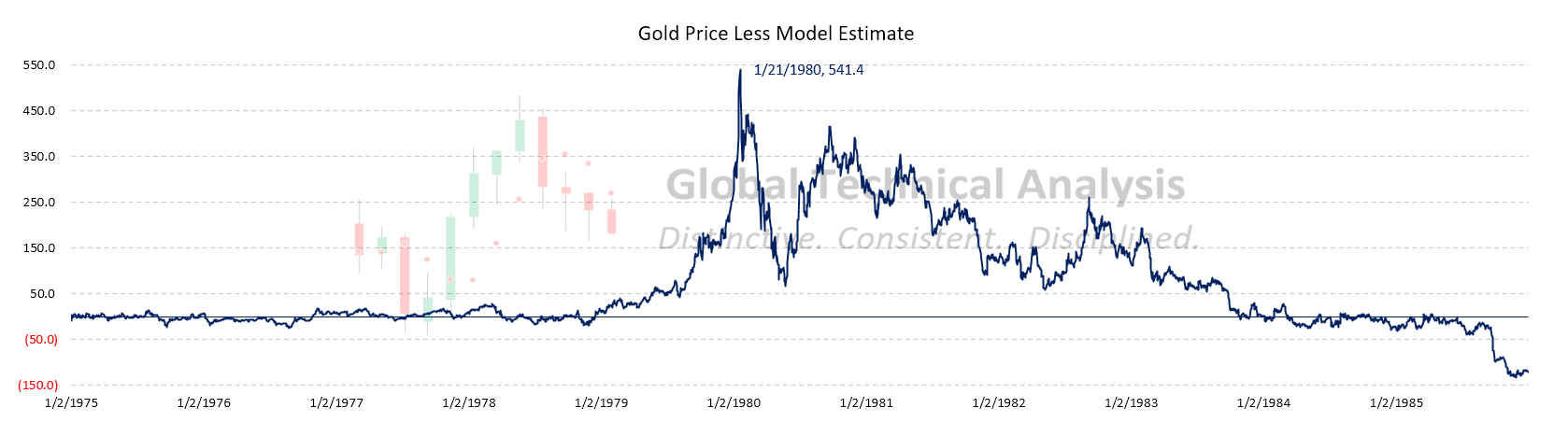

Warnings for Gold Investors

The correlation between gold and real interest rates and the yen is statistically strong, with an r-squared of .891. Using the three factors, Brett Freeze created a model to help show if gold is rich or cheap versus the historical correlation. His model shows the current gold price of $1986 is $531 above the model rate. The second graph shows that during the last bout of high inflation in 1980, the difference between the price of gold and the model was $541. While the divergences are nearly identical on a dollar basis, they are far off percentage-wise. In 1980 gold had risen 156% above the model’s fair value price. Today it sits 36% above fair value. A percentage divergence similar to 1980 would put the price of gold at $3640, assuming the current fair value price ($1455).

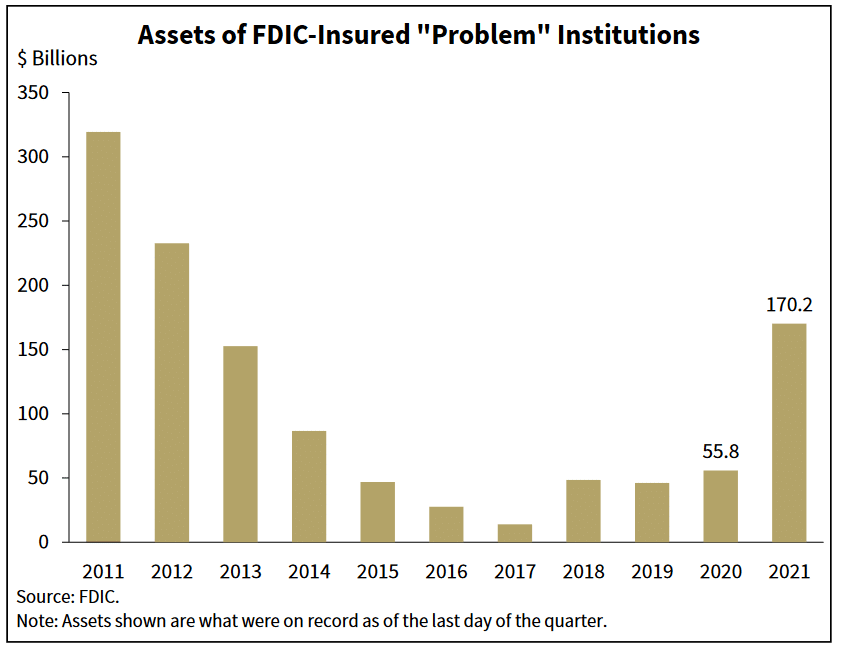

Banking Trouble Ahead?

The following graph is from the latest FDIC quarterly banking profile report. While the information was just released, it is stale as it uses data from the fourth quarter of 2021. As such, it doesn’t take the recent sharp increase in interest rates and flatter yield curve into consideration. Standing out in the report is that the number of assets at problem institutions rose sharply. However, the number of problem institutions fell to a ten-year low of 44. One or more of the “problem” banks must be a “good-sized” bank.

The report notes that aggregate income is down for four quarters in a row but is still above pre-pandemic levels. The decline is partially due to shrinking net interest margins resulting from the flattening yield curve. It is also noted that provisions for credit losses declined. As we saw in the latest round of bank earnings, banks increased loss reserves in the first quarter. The combination of weakening margins, rising provisions for credit losses, and trading losses due to higher yields will keep pressure on the banking sector.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.