Volatility in the equity markets has fallen significantly over the last few weeks. The graph below compares two popular measures of equity volatility. Realized volatility is the annualized volatility based on recent actual changes in the S&P 500. Implied volatility, using options pricing, gauges expectations for expected equity volatility. Realized and implied annualized volatility are at or near the lowest levels since the downward trend started. Consider that the average daily price change over the last five days is only .58%. In 2022 the average daily price change was double that at 1.19%.

The critical question is, what does low volatility mean for equity prices going forward? For starters, it means the tug-of-war between buyers and sellers (bulls and bears) has found a happy medium. Such a stable condition can last a while, but new data or news can motivate buyers or sellers and cause volatility to spike from its complacency. Enjoy the stability for now, as volatility will spike again. Such does not necessarily mean stocks will move lower, although volatility is often negatively correlated with equity prices. Given the large divergence between what the market thinks the Fed will do and what the Fed says it will do, heightened volatility is sure to spike again.

What To Watch Today

Economy

Earnings

Market Trading Update

As noted below, inflation did cool at the headline, but both the core and “sticky price” inflation measures remained….sticky.

Such means the Fed will likely hike rates again at the next meeting as inflation is still not near its 2% goal. Given the runup in the markets has been on the “hope” of a Fed pause, yesterday’s data does little to push the Fed in that direction. Such is especially the case given the still strong employment reports.

While the market did stumble into the close yesterday, the previous leaders were taking the brunt of the hit. As noted recently, 10 stocks comprised about 80% of the market’s advance this year. Those extremely overbought areas of the market are now rotating off some of that overbought condition.

The market’s weakness over the last few trading sessions is weighing on our recent buy signal. If the market fails to hold support at the downtrend line from April, we will likely see a reversal to the 50-DMA. Such would likely reverse the buy signal into a “risk off” mode for the markets suggesting a lower equity exposure.

While maintaining our current equity exposure, we do not recommend adding exposure here until the market exhibits some relative strength. Remain cautious for now and maintain risk management accordingly.

Inflation Cools, but…

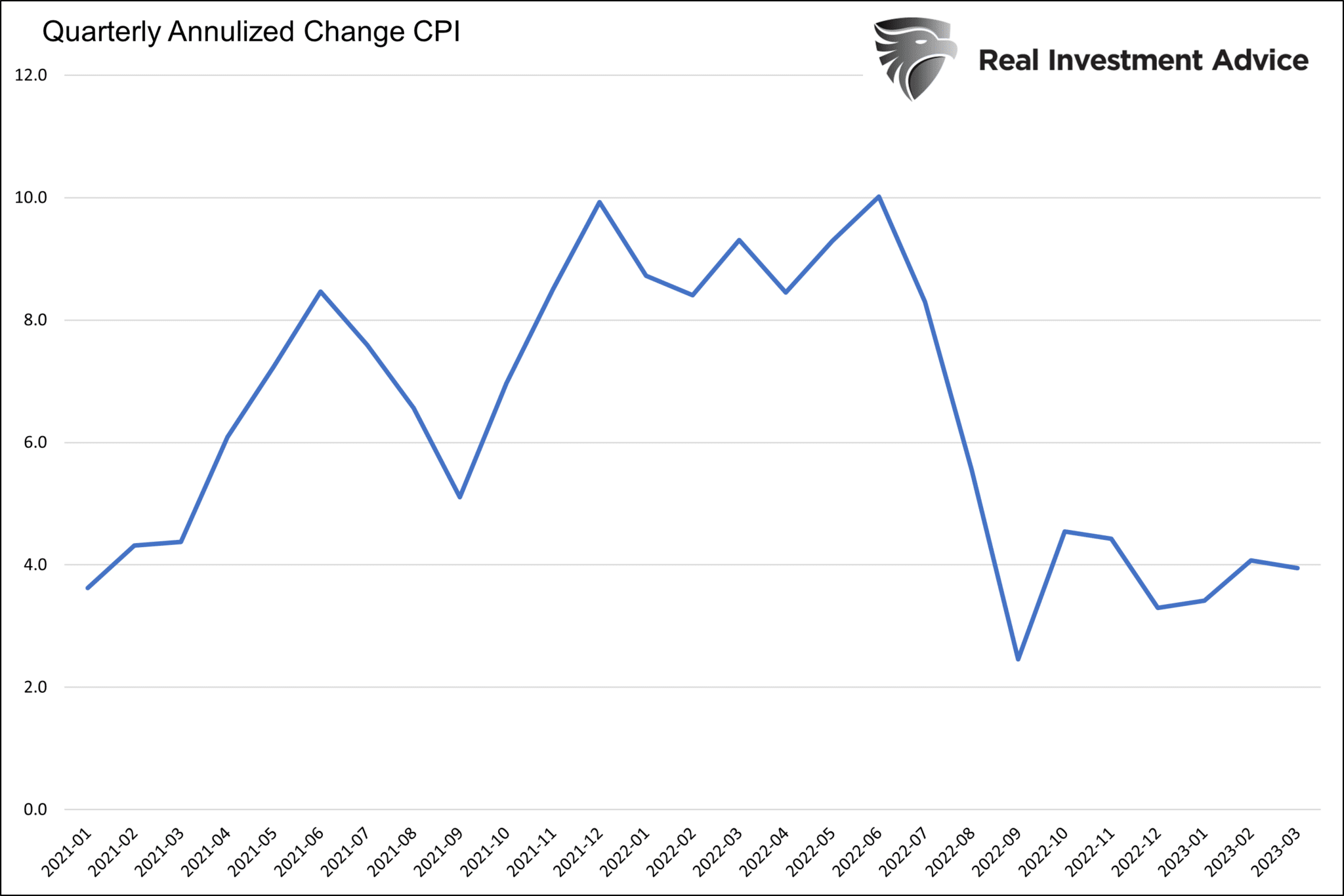

The latest round of CPI inflation data shows inflation is rising slower than expected. Monthly CPI only increased by 0.1% versus expectations for +0.3%. The year-over-year rate fell sharply from 6.0% to 5.0%. The decline is mainly due to monthly inflation running at 1% a year ago. As the calendar moves forward, the year-over-year calculation removes the 1% and replaces it with 0.1%. We prefer calculating the annualized quarterly rate of change in CPI to appreciate current trends better. The graph below shows CPI is currently running at 4% using this measure. While much better than in 2022, it has been stuck around 4% for the last six months.

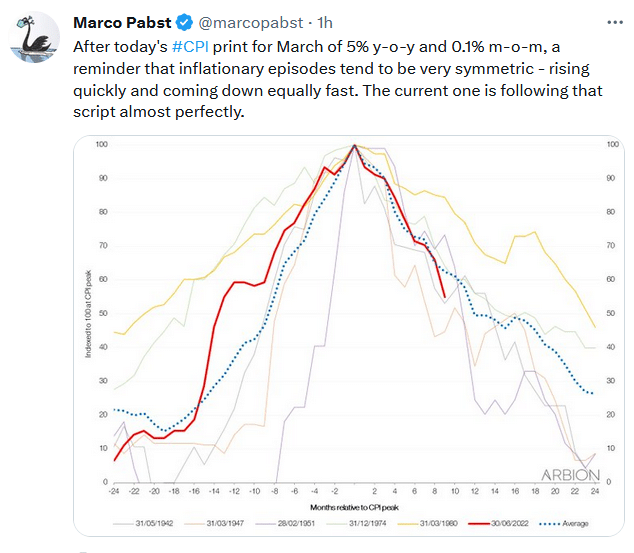

But, more importantly, is it low enough to change the Fed’s mind? While the equity and bond markets seem to like the CPI number, the Fed Funds futures market doesn’t seem to care. The odds of a 25bps rate hike at the May 3rd meeting are unchanged following the data. However, longer-term Fed Funds contracts are pricing in more easing. Currently, the December year-end contract favors 1.25% in rate cuts, assuming the Fed increases them by .25% in May. The Tweet of the Day below shows that it takes approximately two years for periods of high inflation to revert to the average. If that holds up, it may take over a year before the Fed reaches its 2% goal.

Bullishness is Missing

As we shared in yesterday’s Commentary, hedge funds hold record short positions. For their part, there is a lot to worry about. Many leading economic indicators point to a recession. Throw in a banking crisis, tightening lending standards, and declining earnings projections, and it’s hard to find fault with their logic. However, as the economic seers forecast a recession, a few reliable technical indicators signal the market will continue higher. To wit, in Tuesday’s Commentary, we wrote the following:

The graph below, courtesy of Ryan Detrick, shows the S&P 500 just triggered a Zweig Breadth Thrust. Since 1950, only 14 such episodes have occurred. On average, one-year returns are +23% after the indicator occurs.

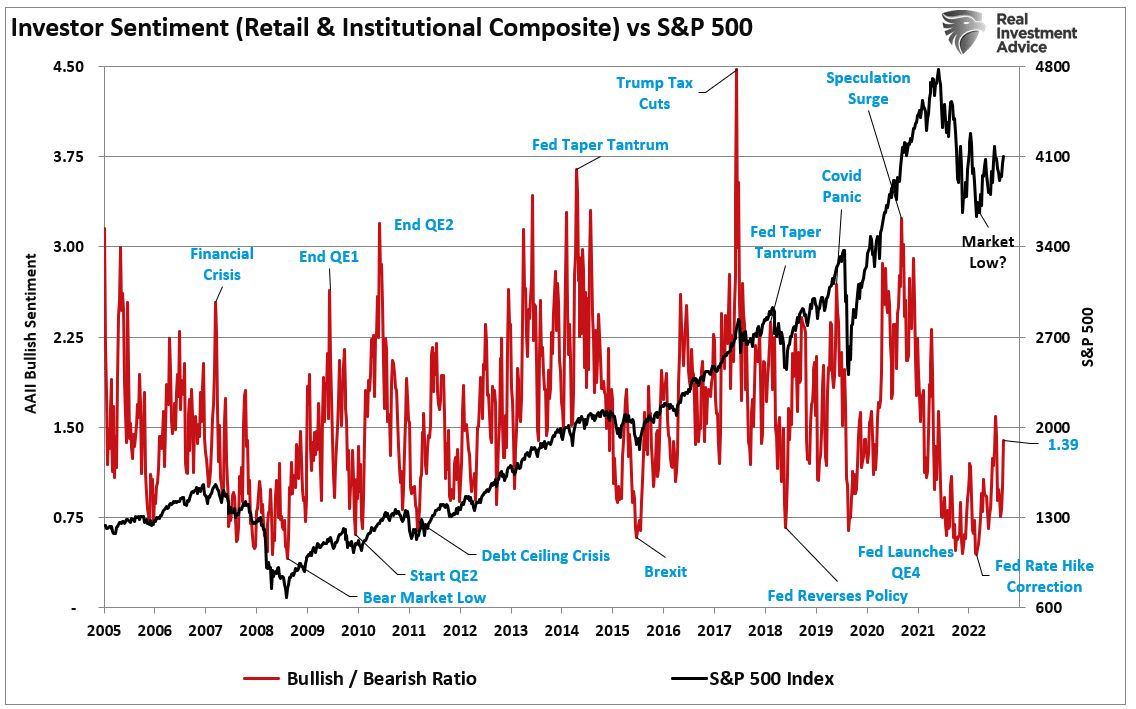

Lance Roberts further clouds the outlook as if the divergence of forecasts and opinions were not hard enough on investors. In his latest article, he discusses investor sentiment. Quite often, market tops occur when everyone is bullish, and market bottoms when everyone is bearish. Per his article, Bullishness Remains Missing:

Excessive bullishness is missing, while extreme bearishness is fading but still prevalent.

Is the current rally since the beginning of the year a return of the bull market? Maybe. It could also be a “bear market rally” sucking investors back in before “the next shoe falls.”

Unfortunately, we won’t know until after the fact. However, rising bullishness from extremely low readings has often suggested a more protracted market advance “climbing a wall of worry.”

While it is easy to allow the many headlines, podcasts, and media prognostications to spin up our “emotional biases,” it is essential to remain focused on what the market is doing versus what we “think” it should be.

The graph below from the article shows that investor sentiment is improving but remains relatively bearish.

Herd Bias – Behavioral Traits Part VII

The previous discussion on sentiment is based on herd bias. Herd bias is our tendency as humans to fit in with the crowd.

In life, “conforming” to the norm is socially accepted and, in many ways, expected. However, in the financial markets, the “herding” behavior is what drives markets to extremes.

As Howard Marks once stated:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, since momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that ‘being too far ahead of your time is indistinguishable from being wrong.’

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

In these whippy markets, the herd seems to change direction frequently. As we have noted in other traits in this series, be aware of both the technical and fundamental setup in the markets and trade accordingly. Try not to let herd mentality get the better of you. But be aware the herd can drive prices to extremes. Thus a bullish bounce in a bear market can go much higher than many bears think. Conversely, when the market is washed out, and everyone thinks stocks are going to zero, focus on the potential value offered.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.