Economic growth metrics for the United States have recently shown surprising resilience; however, consumers’ economic sentiment has not. According to the Bureau of Economic Analysis’s advance estimate, real Gross Domestic Product expanded at an annualized rate of just 1.4%, well below expectations and a steep drop from the 4.4% pace in the third quarter. However, the record-long federal government shutdown, which ran from October 1 through November 12, subtracted roughly 1 full percentage point from growth, as federal outlays plunged 16.6%.

Stripping out that self-inflicted drag, underlying growth was closer to 2.4%, a pace more consistent with a healthy expansion. Consumer expenditures rose 2.4%, moderating from the third quarter’s 3.5% but still solid, while business investment climbed a healthy 3.8%, powered by the ongoing AI-driven capital spending boom. With the government now reopened, the shutdown’s drag is expected to reverse in early 2026, providing a tailwind to first-quarter growth.

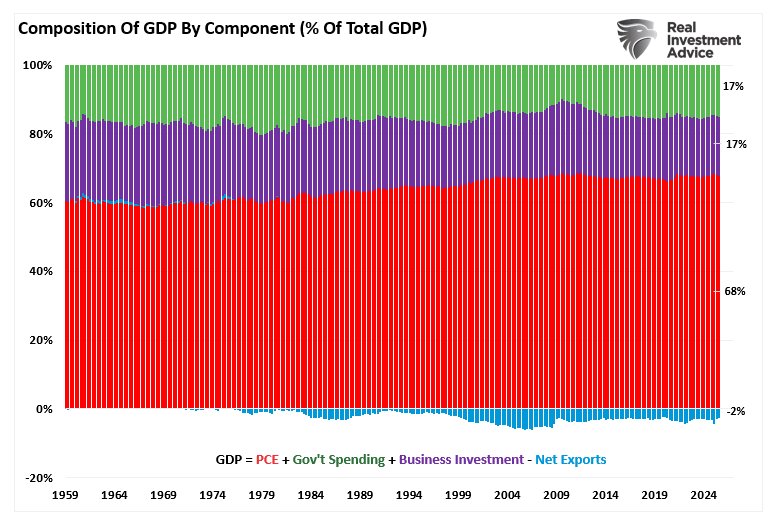

Notably, Gross Domestic Product (GDP) measures the total output of goods and services in the U.S. Of that total, personal consumption expenditures (PCE) comprise roughly 68%. In other words, so goes the consumer, so goes the economy.

When GDP climbs, it signals more economic activity (i.e., consumer demand), which then fuels broader expansion of production. Naturally, GDP growth rates are closely monitored by policymakers, investors, and corporate planners. There is much interpretation of GDP growth as evidence of potential for higher sales and profits going forward, but it does not tell the full story of individual households’ financial experiences.

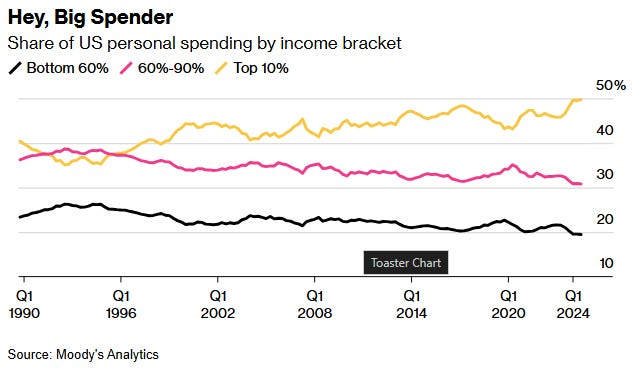

Crucially, economic growth numbers focus only on aggregate performance and do not capture income distribution, regional variations, or the lived experiences of millions of households. A good example of this is the share of U.S. spending by income bracket. Currently, roughly 50% of all consumer spending is driven by the top 10% of income earners, and is increasing, while it is falling for the bottom 90%.

In other words, while we may see strong headline numbers, the numbers can mask pockets of stress in households and small businesses. Furthermore, growth driven by exports or government spending may fail to reach wide swaths of workers, further distorting the headline reading. A good example of that distortion was seen in 2025, when imports to get ahead of tariffs weighed heavily on the Q1 GDP reading, but then reversed sharply in Q2 as fears abated, leading to a sharp rebound. Those distortions had little impact on consumers as a whole.

However, while economic growth statistics paint a picture of a robust backdrop, other coincident indicators, such as the Conference Board Leading Economic Index (LEI), paint a different picture. For example, the LEI, which tends to lead the US economy by about six months, has remained in contraction for a very long period. Such is why the 6-month rate of change of the LEI has historically been one of the most accurate indicators of contractions and recessions. However, despite a contraction in the LEI, the economy never registered a recession.

Yes, based on headline economic growth data, the economy looks solid for now. However, if we dig deeper, we find mixed signals beneath the surface, which may explain the difference between economic headlines and economic sentiment.

The Disconnect Between Stock Market Gains And Current Sentiment

Historically, it is logical that stock markets and economic statistics should move together over the long run. As we discussed in “Return Expectations Are Too High,”

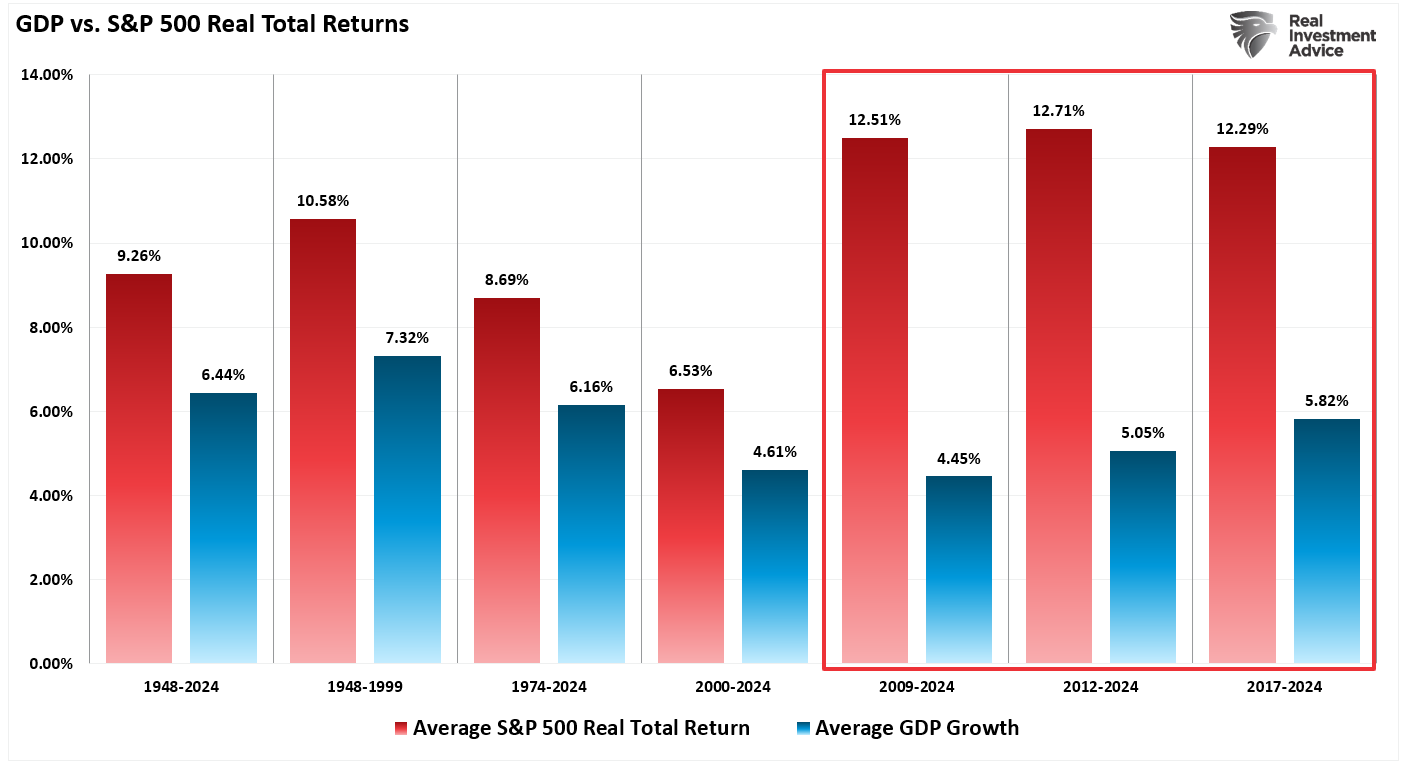

“The chart below shows the average annual inflation-adjusted total returns (dividends included) since 1948. I used total-return data from Aswath Damodaran at the NYU Stern School of Business. The chart shows that from 1948 to 2024, the market returned 9.26% after inflation. However, after the 2008 financial crisis, inflation-adjusted total returns jumped by nearly three percentage points for the last three observation periods.

Here is the issue. Total real (inflation-adjusted) stock market returns are easy to calculate. They are a function of economic growth (GDP) plus dividends less inflation. Such was the case from 1948 to 2000. However, since 2008, GDP growth has averaged roughly 5% with a dividend yield of 2%, yet returns have far surpassed what the economy can generate in earnings.”

That divergence over the last 15 years is unsurprising as we noted in “Pavlov Rings The Bell” in investing?

“Over the past 15 years, the markets were repeatedly bailed out of more serious corrections by either fiscal or monetary policy. That neutral stimulus (the interventions) was repeatedly paired with a reward-stimulus of markets going higher. As such, investors were “conditioned” to expect rescue whenever issues arise, to buy stocks on every decline, and to believe that this cycle will indefinitely continue. This was the point we made recently regarding “moral hazard.”

“The Federal Reserve’s well-intentioned interventions have created one of modern finance’s most powerful behavioral distortions: the conviction that there is always a safety net. After the Global Financial Crisis, zero interest rates and repeated rounds of quantitative easing conditioned investors to expect that policy support would always return during volatility. Over time, that conditioning hardened into a reflex: buy every dip, because the Fed will not allow markets to fail. What exactly is the definition of ‘moral hazard?’

Noun – ECONOMICS: The lack of incentive to guard against risk where one is protected from its consequences, e.g., by insurance.

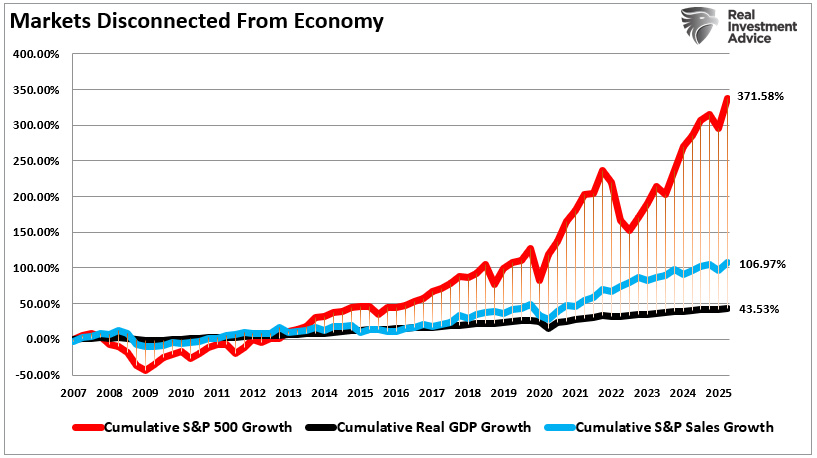

Those constant sustained supports in both the economy and the financial markets were the foundation behind the break between economic realities and financial returns.

Currently, while GDP growth has surprised to the upside and some macro data show economic resilience, major equity indices such as the S&P 500 have also risen to new heights, driven by investor expectations for future earnings growth rather than the current consumer mood. The problem, as shown above, is that the markets are very detached from actual revenue growth.

Another problem with the headline data is that while stock market performance has exceeded historical expectations, its impact on the overall economy has become more muted. While equity values have surged, creating a “wealth effect” that supports consumption, that effect remains primarily confined to the top 10% of the population that owns 87% of the equity market. As noted above, the top 40% of income earners currently account for roughly 80% of total consumption.

That divergence helps explain the gap between weak consumer sentiment and strong economic data.

Consumer Sentiment Surveys Weak Despite Strong Data

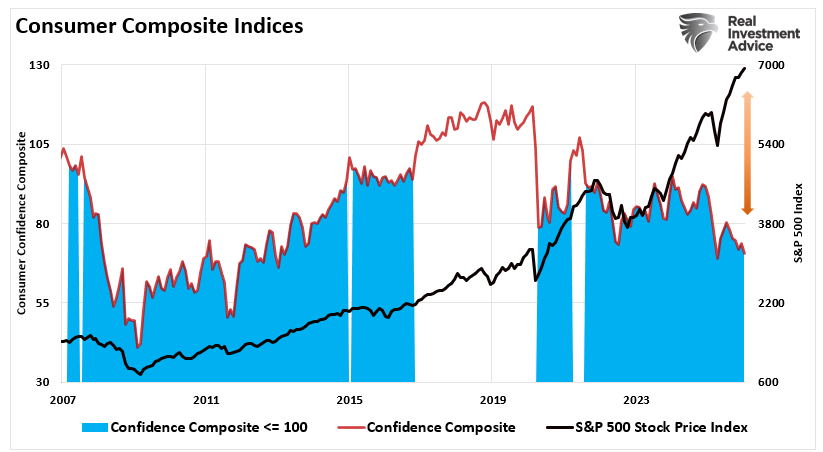

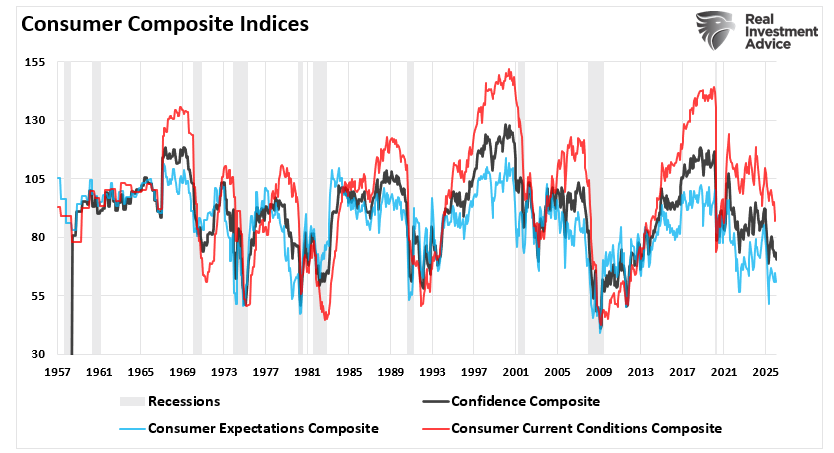

In stark contrast with macro indicators and stock market performance, consumer sentiment surveys have shown marked weakness. Both the Conference Board Consumer Confidence Index and the University of Michigan Surveys have dropped sharply over the last two years, while the stock market has risen sharply. As shown, when markets are rising, consumer sentiment tends to rise with them, which makes sense. The chart below is a composite indicator of both primary consumer sentiment measures.

However, in both cases, the current situation assessments and future expectations remain very weak, with the expectations component falling below levels historically associated with recession signals.

The decline reflects growing pessimism about job prospects, business conditions, and future income, and consumers cited concerns about inflation, high prices, food and energy costs, affordability of health insurance, and geopolitical or political uncertainty. While the surveys captured widespread unease, GDP continued to expand.

Notably, the divergence between sentiment and economic data is not unique to this moment. Analysts have long noted that consumer mood often lags hard data, and we hope to see sentiment turn higher if the economy continues to expand. It is worth stating that in the short term, surveys often reflect fear and uncertainty, which may depress sentiment even if actual spending behavior remains relatively strong. However, while nominal data suggests that consumer spending remains resilient, that resilience has not been a function of “buying more” products, but simply buying the same amount, or less, at higher prices, which certainly explains the decline in sentiment readings.

Crucially, understanding that if consumer sentiment drives consumption, and consumption makes up 68% of the economy, that consumption is the demand for small and large businesses. Therefore, if economic growth is robust, we should see demand reflected in increased sentiment across the spectrum. However, as the combined composite shows, those sentiment readings remain weak. Note the correlation between sentiment and the future direction of economic activity.

These weak sentiment readings do not automatically translate to immediate economic contraction. But they indicate a cautious mood among households and business owners. That caution may lead to reduced spending on both sides of the GDP equation. Such a slowdown seems logical if economic sentiment remains subdued.

Why the Divergence Matters and What It Signals for the Future

The split between improving economic statistics, rising markets, and weak consumer sentiment has important implications. First, it suggests an economy operating on multiple tracks. Macro data points to expansion, supporting the rise in stock prices and earnings expectations. However, the drivers of that expansion and earnings feel insecure and pessimistic.

That divergence raises several questions.

- Is growth sustainable if sentiment remains weak?

- Will strong corporate profits continue if consumers pull back?

- Could widespread pessimism eventually feed into economic behavior, causing slower spending and slower growth?

History offers cautionary examples of negative sentiment preceding downturns. Such is not because the data was wrong, but because mood eventually influenced real behavior.

Secondly, the divergence also highlights distributional issues. As noted above, aggregate growth does not capture income and wealth disparities. While high-income households account for 50% of spending, lower-income households are less likely to fully benefit from macroeconomic expansion. That reality contributes to weak sentiment. This leaves the markets exposed to events that cause high-income earners to cut spending. Such is particularly the case when there is no buffer between the “haves” and “have-nots.”

From an investment standpoint, this mixed picture calls for increased risk management. While the market is rising on higher earnings expectations, those expectations are subject to rapid shifts as economic realities emerge. As such, investors should assess risk precisely, considering both macro signals and consumer behavior.

- Evaluate valuations carefully. Rising indices do not rule out overvaluation. Focus on companies with strong balance sheets, stable cash flow, and pricing power.

- Diversify across sectors. Performance may vary. Defensive sectors like utilities, consumer staples, and healthcare often outperform during sentiment-driven slowdowns.

- Monitor leading indicators. Pay attention to leading economic indexes, employment data, and consumer credit trends. Weak sentiment may foreshadow slower growth.

- Keep liquidity. Maintain cash reserves to deploy when conditions change. Divergence creates volatility.

- Consider hedges. Bonds or volatility-linked strategies may reduce risk if sentiment shifts markets.

- Focus on quality. Quality companies with competitive advantages are more likely to weather shifts.

This divergence between data, markets, and sentiment is a critical economic signal. How this all works out, no one knows for sure. While there are currently plenty of valid reasons markets can only go higher and that investors should “buy the dip,” it seems prudent to consider the other side of those arguments.

To steal a line from Bob Farrell:

Historically speaking, when “all experts agree,” it has paid dividends to stay disciplined and prepare for the possibility that “something else tends to happen.“