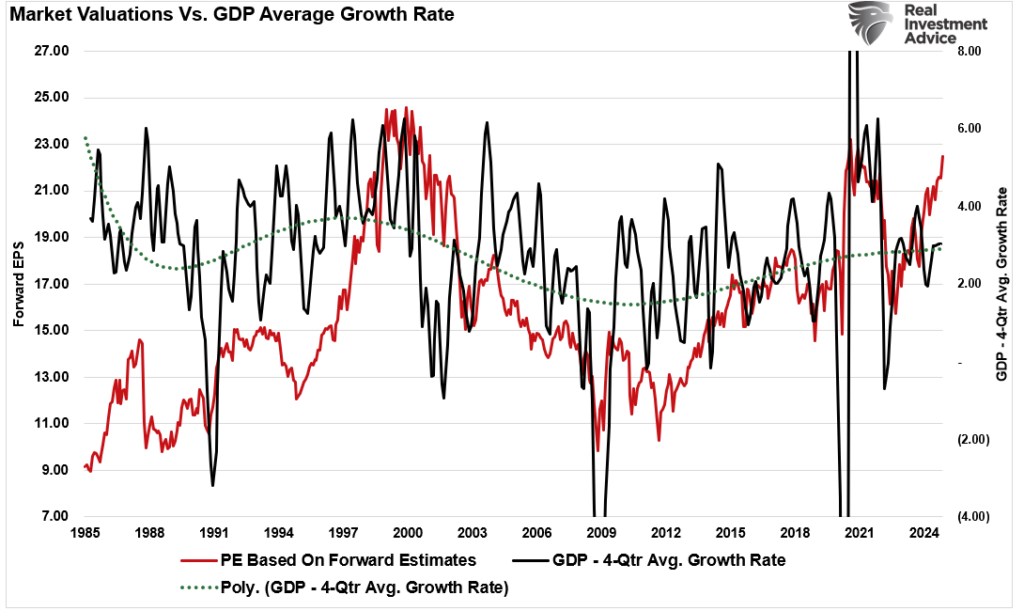

Bloomberg led its article “Credit Markets Signal Warning for a Relentless Equity Rally” with the following paragraph:

Stocks are close to the most overvalued against corporate credit and Treasuries in about two decades. The earnings yield on S&P 500 shares, the inverse of the price-earnings ratio, is at its lowest level compared with Treasury yields since 2002, signaling that equities are at their most expensive relative to fixed income in decades.

Corporate bond credit spreads represent the difference between a corporate bond’s yield and a similar maturity U.S. Treasury note. Currently, as shown on the left, credit spreads provide investors with the slimmest yield margin over U.S. Treasuries in over 25 years. The graph highlights the spreads for highly rated (AA), investment grade (BBB), and junk (B) bonds. That yield spread is tighter than usual due to an increasing term premium in U.S. Treasury securities. However, corporate spreads are still historically tight, even with the approximate 75bps term premium. For more details on Treasury term premiums and what it may mean for bond returns, check out our latest article: Why Are Bond Yields Rising?

Despite the tight corporate spreads, the difference between the S&P 500 earnings yield and corporate bonds is negative 2%. The Bloomberg graph on the right shows that the spread hasn’t been that tight since 2008. Stocks are riskier, yet corporate earnings yield less than corporate bonds. The graph further confirms very high equity valuations, suggesting investors’ earnings growth expectations are much loftier than historical earnings growth rates. Per the Bloomberg article:

“People are skewing toward assets that are giving you more and more upside,” Suzuki said. “You’re really just trying to see people hit home runs here more and more.”

What To Watch Today

Earnings

Economy

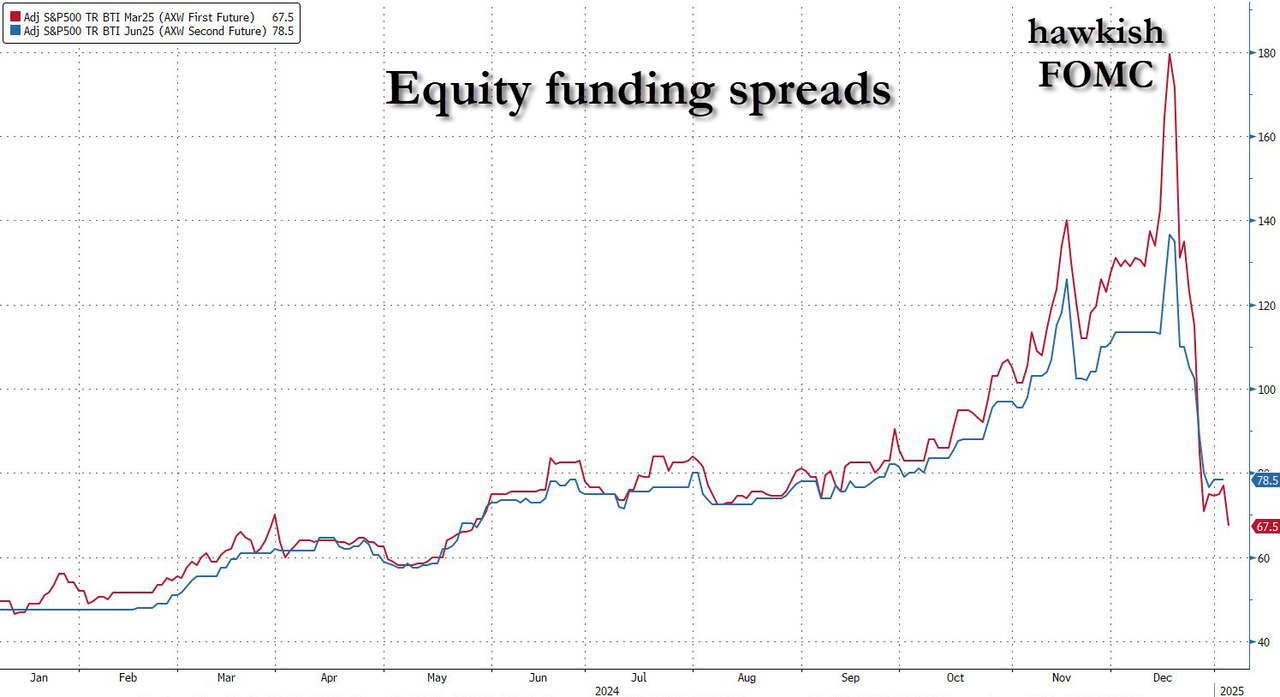

Market Trading Update

Yesterday, we discussed money flows’ impact on U.S. equity ETFs as households ramp up equity exposure. While money flows have been flowing into equities from households, hedge funds and professionals have been aggressively selling.

Starting December 18th, when the Federal Reserve began suggesting a “pause” to interest rate reductions, equity fund spreads cracked and began to reverse. Such is also the point where the market peaked and has struggled over the last several weeks.

While institutional selling pressure is not always a “be all, end all” indicator, it suggests there could be more to the recent market weakness than a temporary pause. As noted by Goldman Sachs, the recent selling of U.S. equities by hedge funds over the past five sessions has been the strongest in more than seven months. While valuations have been historically high for many months, this is the first time we see significant selling in hedge fund positioning.

Again, this isn’t an urgent “crash” warning, but it bears paying attention to. If the market continues to deteriorate, and we see continued stress in equity funding, we could see a much rougher start to the New Year than previously expected.

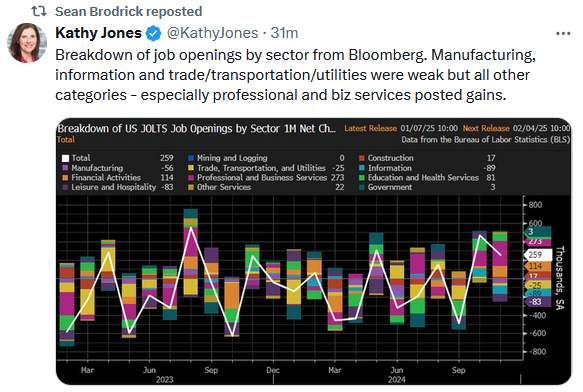

JOLTS

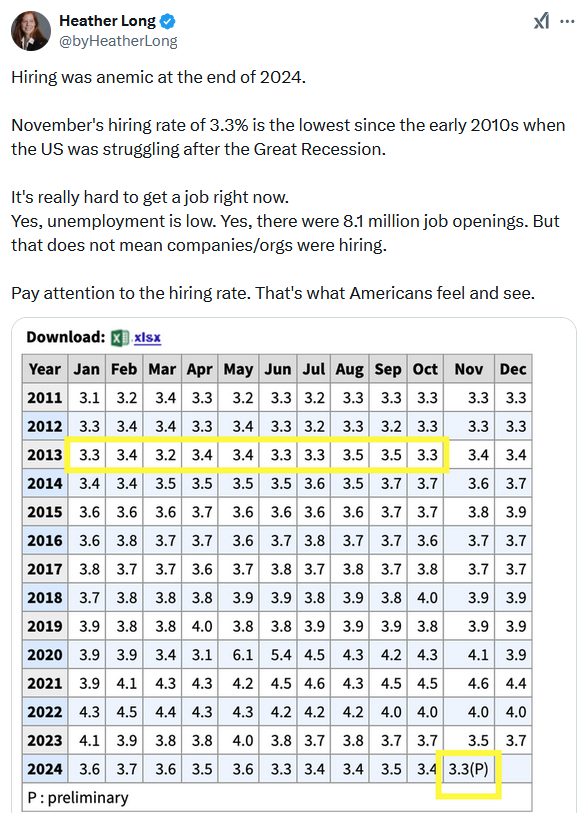

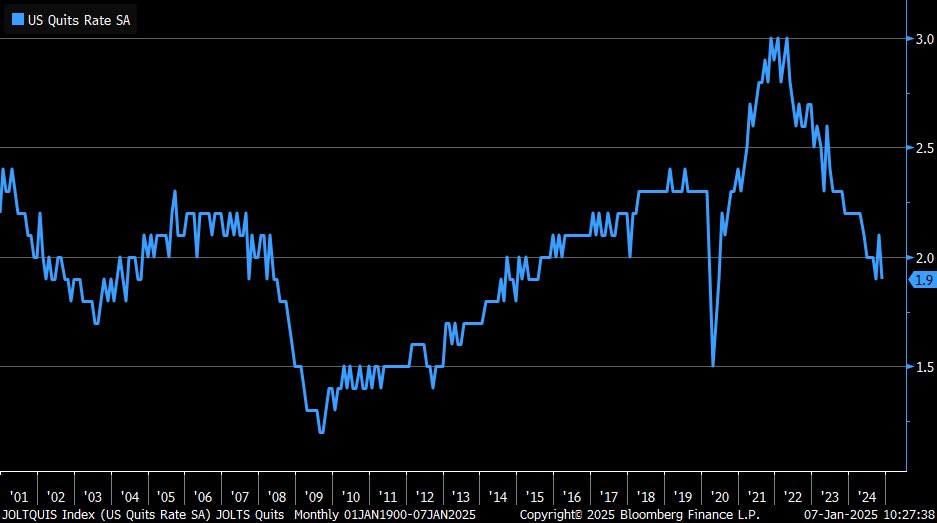

The number of job openings for November was higher than expected at 8.1 million. While more job openings portend a healthy labor market, the hires and quits rates point to trouble beneath the surface. Per Heather Long’s tweet below, the hiring rate is now the lowest in over ten years. Despite job openings, employers are not hiring. Furthermore, the quits rate continues to decline. Quits are voluntary job separations and are a good indicator of employee confidence. When quits are high, employees are more confident in the labor market and their ability to find a new, higher-paying job. Based on the quits rate, employees are not very confident today.

Remember that the JOLTS data lags this Friday’s employment report by one month. Furthermore, November has significant seasonal effects due to temporary holiday employment, which can result in misleading data. This holds for the BLS report on Friday as well.

“Curb Your Enthusiasm” In 2025

“Curb Your Enthusiasm,” which ran its series finale last year, starred Larry David as an over-the-top version of himself in a comedy series that showed how seemingly trivial details of day-to-day life can precipitate a catastrophic chain of events. The show never failed to deliver a laugh but also reminded me that unexpected events can derail the most certain of outcomes.

As we enter 2025, the financial markets are optimistic. That optimism is fueled by strong market performance over the last two years and analyst’s projections for continued growth. However, as “Curb Your Enthusiasm” often demonstrates, even the best-laid plans can unravel when overlooked details come to light. Here are five reasons why a more cautious approach to investing might be warranted in 2025.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.