Yesterday’s CPI data and today’s FOMC meeting will guide monetary policy expectations for the summer months. As the FOMC debates whether to raise rates or pause, they will likely spend a reasonable amount of time reviewing the CPI report. The headline CPI number was good, with May prices only rising 0.1%. The year-over-year CPI fell to 4.0% from 4.9% last month. It has now fallen for 11 straight months, the longest streak since 1921! However, the core CPI (excluding food and energy) rose 0.4% and remains sticky. The Fed often reminds the public that they follow variations of core prices as they are better indications of inflation.

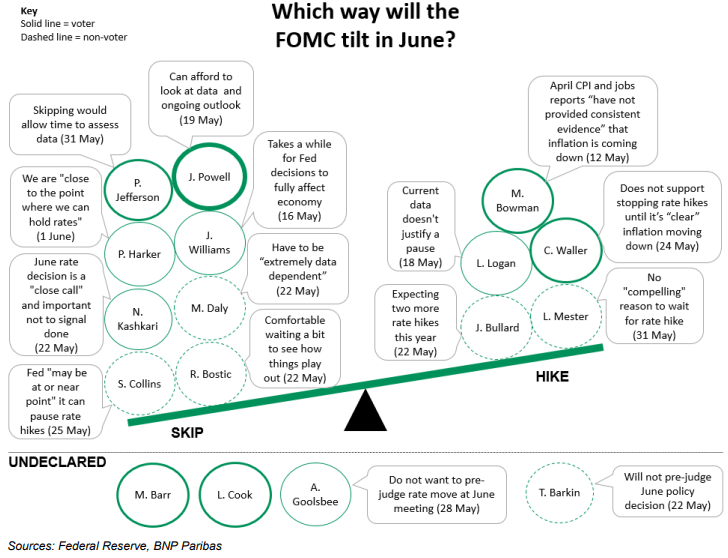

The mixed CPI data gives the FOMC an excuse to pause. The Fed may also take comfort as the two-year yield at 4.58% is now above the year-over-year CPI rate. Another FOMC consideration is that CPI core services, excluding housing, a data point Powell closely follows, is down to +4.60% year over year, the lowest level since February 2022. The Fed Funds market implies a near zero percent chance the FOMC will hike rates today but a 60% chance they will raise rates another 25bps at the July or September meeting. The graphic below from BNP helps us consider how various Fed members think about pausing or hiking. Four voting members join Jerome Powell on the pause side. That compares to three voting members that have vocally supported another rate hike and three that are undeclared.

What To Watch Today

Earnings

- No notable releases today

Economy

Market Trading Update

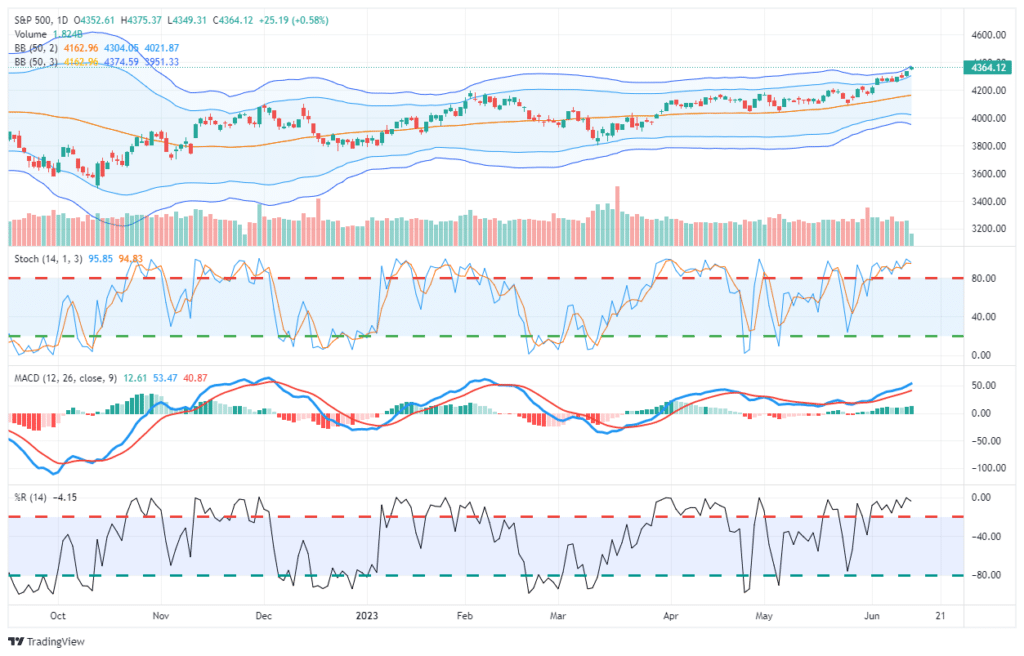

Yesterday’s post-CPI rally was unsurprising as the sharp decline in the headline gave the bulls hope that the Fed will permanently “pause” rate hikes at today’s FOMC announcement. However, the market is due for a correction in the short term as the market is now trading 3-standard deviations above the 50-DMA. Historically, such is unsustainable for long, but can last longer than expected.

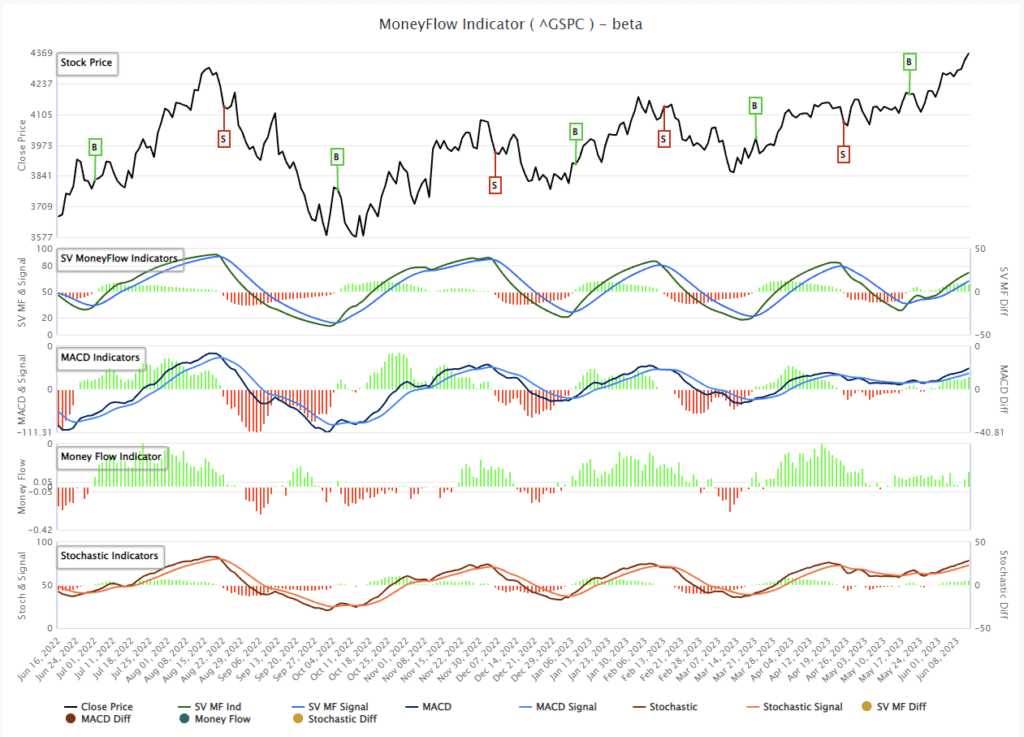

Furthermore, our money flow indicator is highly overbought and suggests a short-term correction is likely.

What will trigger a short-term reversal is unknown. It could simply be a market rotation or a financial or economic event. However, when it occurs, the correction will likely be fairly swift, lasting a few days to a few weeks. However, once that correction runs its course, it will be a buying opportunity to increase equity exposure in portfolios.

For now, the bear market is over. As investors, we need to become more bullish in our allocations.

GDP and GDI Divergence

GDP, or gross domestic product, is what most investors use to track economic activity. Lesser tracked is GDI. GDI, or gross domestic income. Per Wikipedia, GDI is as follows:

the total income received by all sectors of an economy within a state. It includes the sum of all wages, profits, and taxes, minus subsidies. Since all income is derived from production (including the production of services), the gross domestic income of a country should exactly equal its gross domestic product (GDP).

As we share below, GDP and GDI track each well. However, the most recent data shows GDI declining by 0.9%, following a 0.2% decline in the fourth quarter of 2022. At the same time, GDP rose 0.9% in the fourth quarter and 1.6% in the latest quarter. Since 1950 the current 2.5% difference between the two is only matched by an equal difference in 2007. In the third and fourth quarters of 2007, GDI was negative while GDP was positive. It turns out GDI was signaling a recession. Might today’s divergence between GDI and GDP be an omen?

More CPI Lags

In Tuesday’s Commentary, we showed data indicating that used car prices in CPI lag the real used car market by 2-3 months. As such:

“Used cars make up about 4.50% of the CPI index. If the CPI-used car prices index catches down to the Manheim index, CPI will be .35% lower. As we have discussed with rental prices, CPI often uses lagging indicators. While they may prove to be accurate, they are less timely.”

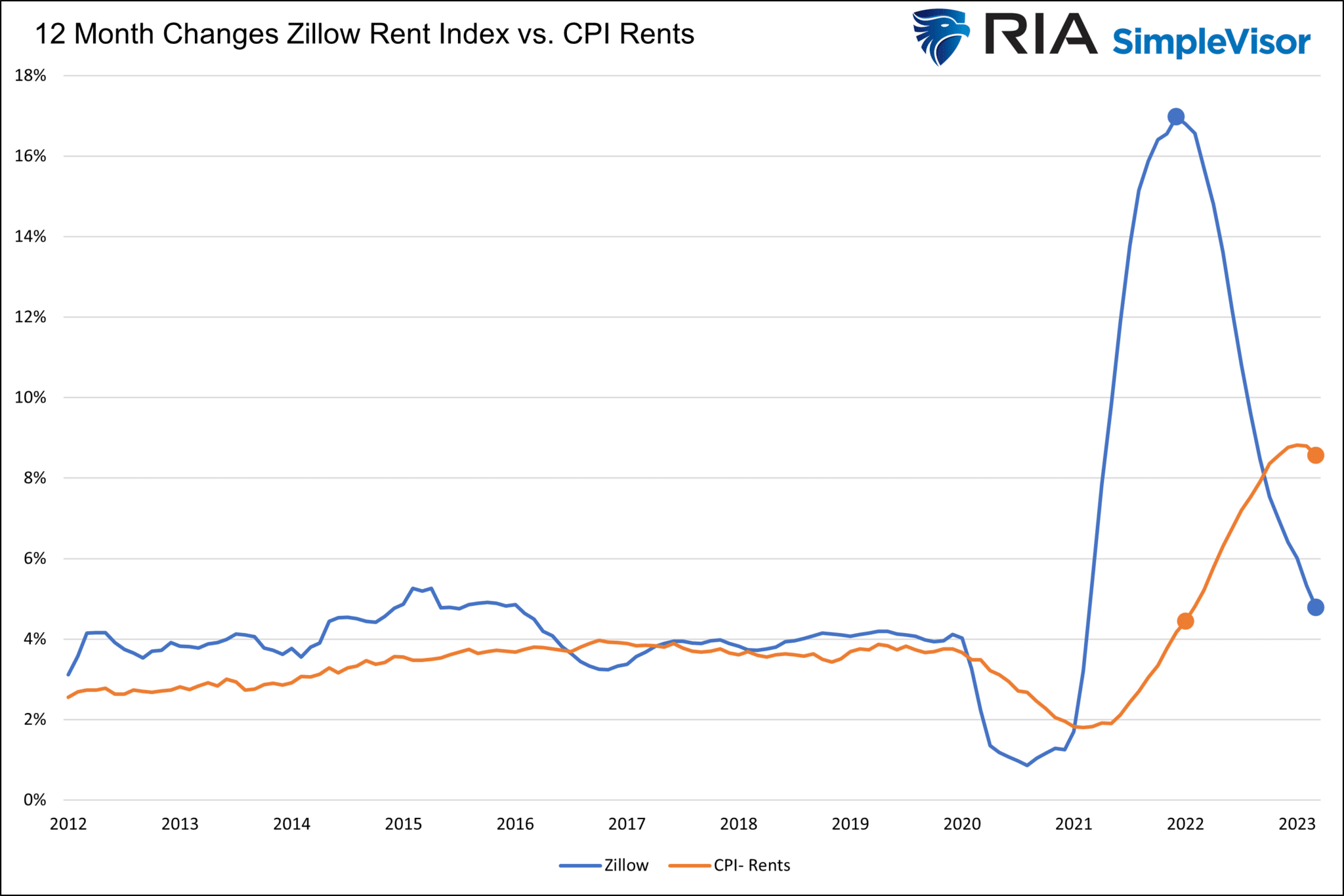

A reader asked if we could do the same analysis on real-estate prices within the CPI index. With yesterday’s latest CPI report in hand, we present a similar lag effect. Since rents account for 7% of CPI, and rents play a role in calculating OER, which is another 25% of CPI, this correlation is more important when forecasting inflation than used cars.

The graph below shows that the Zillow rent index peaked in February 2022 and has fallen steadily. The year-over-year rent inflation rate is only slightly above the pre-pandemic running rate. On the other hand, the year-over-year rate of the CPI-rent index just fell for the first time in over two years. Assuming CPI rent and OER prices follow a similar path as the Zillow index and the Case Shiller Home price index, we should expect the year-over-year CPI rate to pull CPI lower by 1.75% over the next year. For more context, please see the Tweet of the Day below.

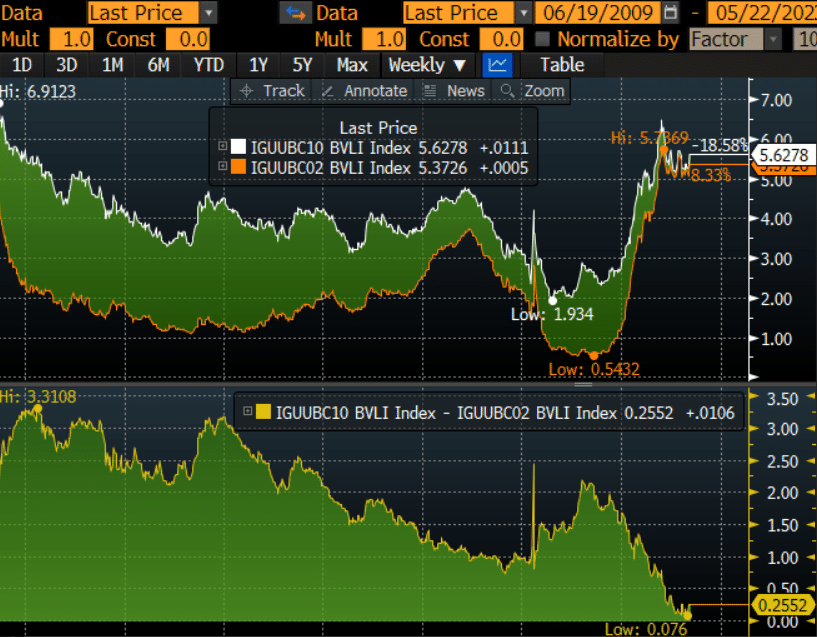

Credit Complacency or Odd Yield Curve Consequences

The Bloomberg graph below charts two- and ten-year BBB corporate bond yields. As you might notice, and highlighted in the bottom graph, the yield difference between the two bonds is approaching zero. The difference is partially due to the 1.18% inversion of the U.S. Treasury yield curve.

The graph is stunning. Investors are implying that the credit risk of holding a two-year corporate bond is the same as holding a ten-year bond. According to Moody’s, BBB-rated bonds have a 0.3% annual default rate. As such, the odds of a two-year bond defaulting are 0.6% versus 3% for a ten-year bond. The yield curve accounts for 1.18% of the difference, but investors should demand 2.40% in yield for eight more years of default risk. With those two inputs, the BBB-rated spread should be approximately +1.20%, not +.25%. Like the implied volatility (VIX) pricing in the equity markets, the credit markets also seem a bit complacent.

If you are wondering why the default rate is so low, bonds are often downgraded from BBB before they default.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.