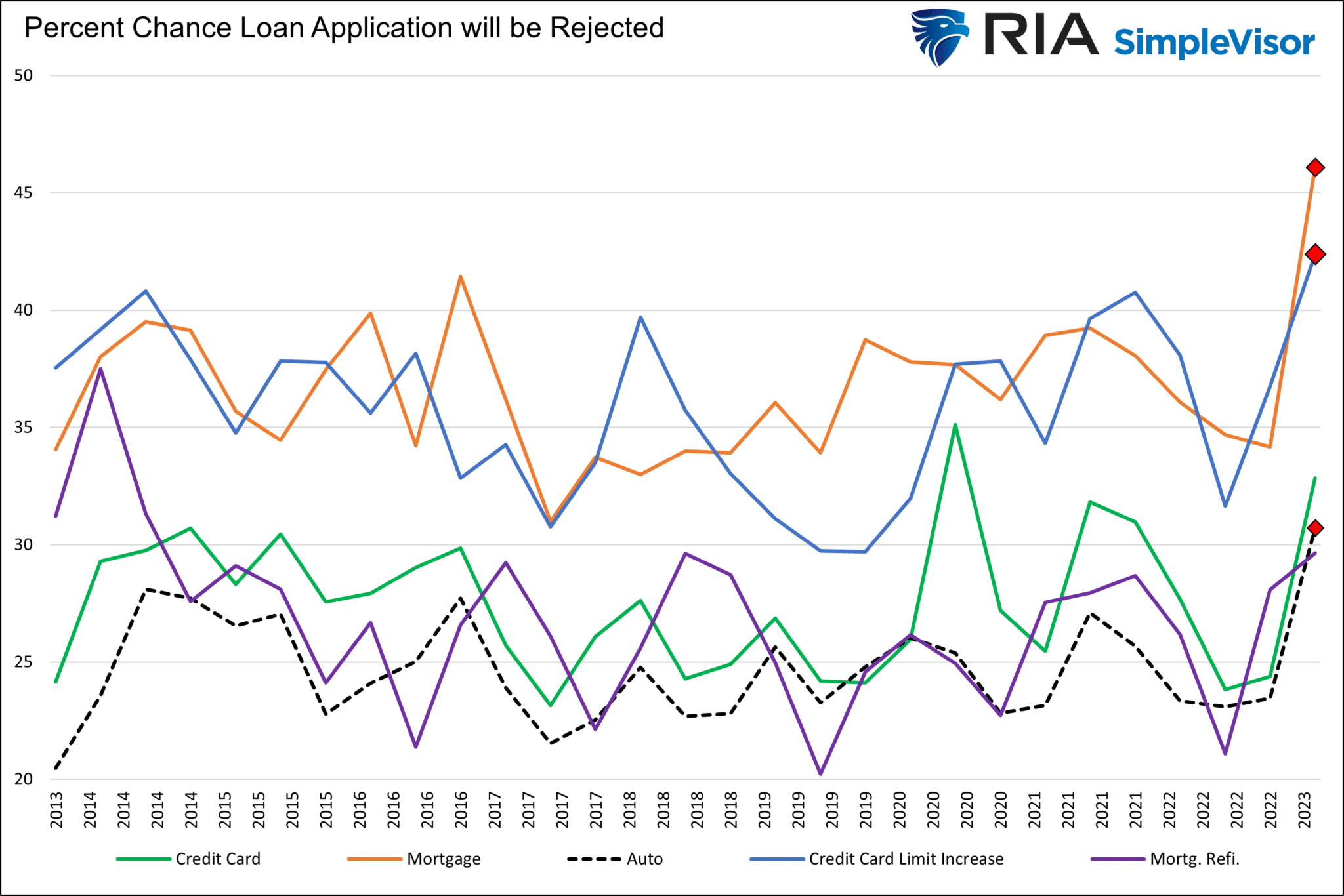

The recent New York Fed Credit Access Survey report shows consumer borrowing is becoming more difficult. As we have been discussing for a few months, the fallout of the March regional banking crisis and the inverted yield curve is causing banks to tighten lending standards. The Fed report is based on a survey taken every four months. Therefore the most recent information is the first since the crisis. It shows that in June, consumer borrowers faced the most challenging time attaining credit in years. Further, it also appears that the consumer borrowing binge is abating. Per the Fed: The application rate for any kind of credit over the past twelve months declined to 40.3 percent from 40.9 percent in February, its lowest reading since October 2020.

The rejection rate for consumer borrowing applications rose to 21.8%, the highest since 2018. Auto loan rejections rose sharply to 14.2% from 9.1%, a series high. The consumer borrowing survey also has a forward-looking indicator that puts odds on the chance a loan application will be rejected. This gauge also rose. Per the Fed: “It rose to 30.7 percent for auto loans, 32.8 percent for credit cards, 42.4 percent for credit limit increase requests, 46.1 percent for mortgages, and 29.6 percent for mortgage refinance applications.” As we share below, this forward-looking indicator is at 10-year highs for auto loans, mortgages, and credit card limit increases, as signified by the red diamonds. The remaining forms of credit, credit card, and mortgage refinance are near ten-year highs. More burdensome access to credit may slow personal consumption in the months ahead.

What To Watch Today

Economy

Earnings

Market Trading Update

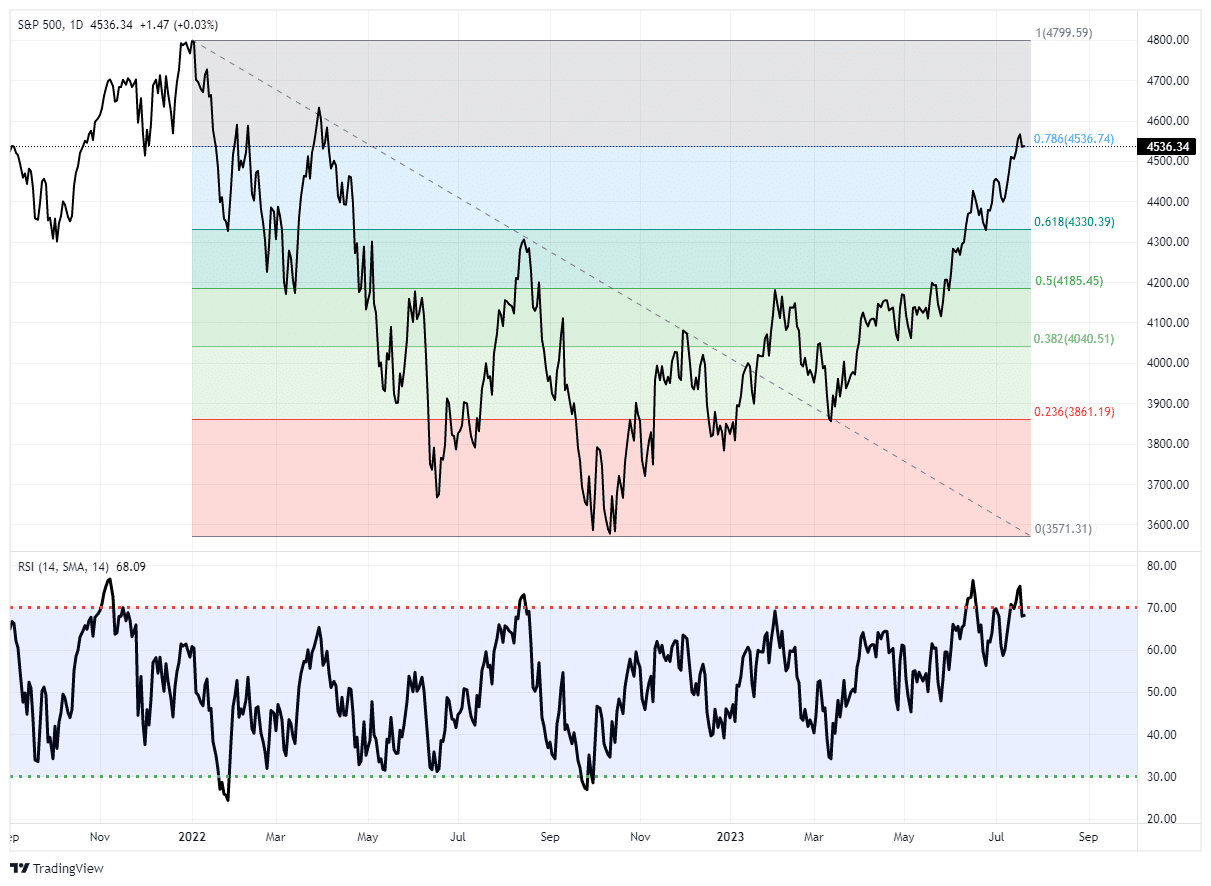

Earnings season is underway, and so far, corporate outlooks remain fairly upbeat, suggesting the economic cycle might just be improving. While it is too early to tell for sure, as we will discuss in more detail today, some evidence may support that view and the potential for the market to eclipse all-time highs by next year.

As we discussed in Thursday’s Daily Market Commentary (subscribe for daily email):

“New all-time highs are coming. Given the fundamental and economic backdrop, I know that seems hardly logical, but that is what the technicals now suggest. The market has decisively cleared its 78.6% retracement of last year’s decline. Historically, when that occurs, new highs are a likely outcome. The combined momentum of the market, rising bullish sentiment, and the need to chase performance by managers are contributing to the seemingly unstoppable rally from the October lows.”

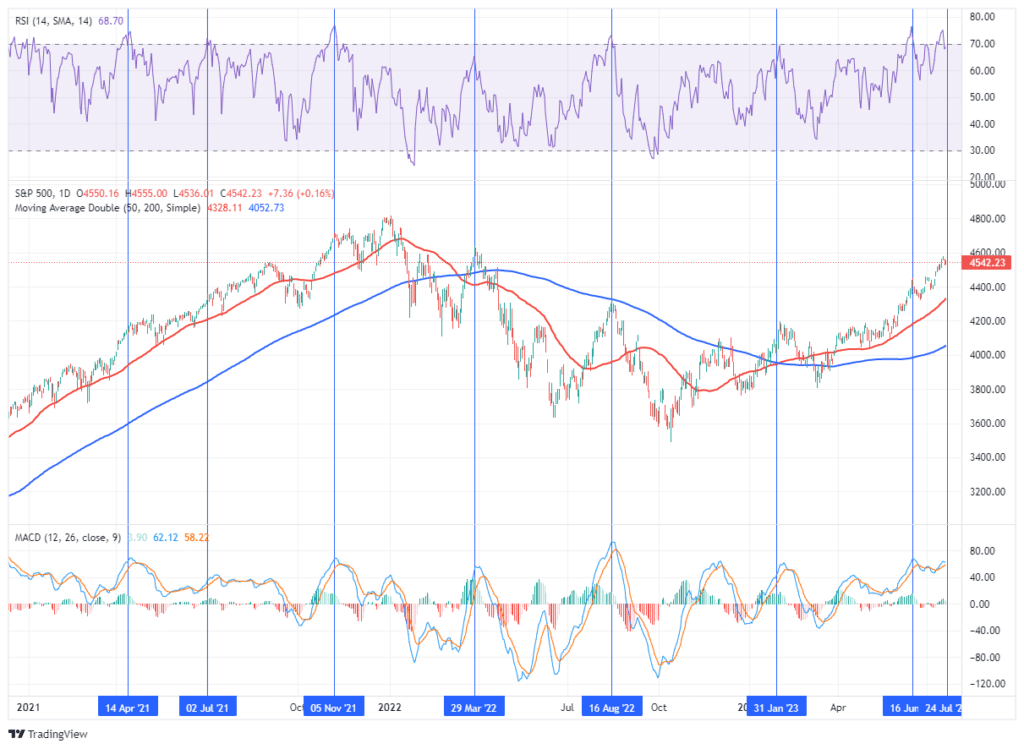

However, we must remember that market advances can only go so far before an eventual correction occurs. My best guess is that if the markets are to reach all-time highs this year, we will likely have a correction to reset some of the more extreme overbought conditions, as shown below.

With only minor resistance between here and the previous high. Any pullback to the 50-DMA is likely a good entry point to increase exposure on a better risk/reward basis.

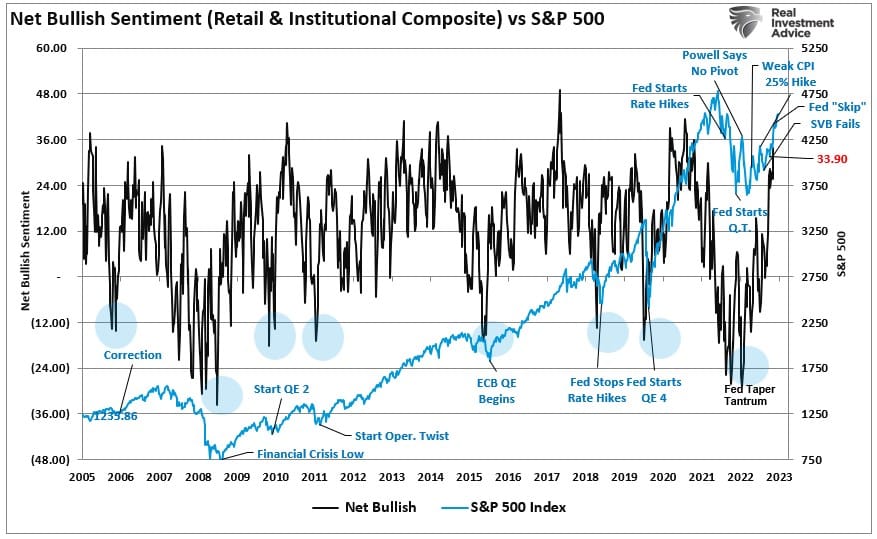

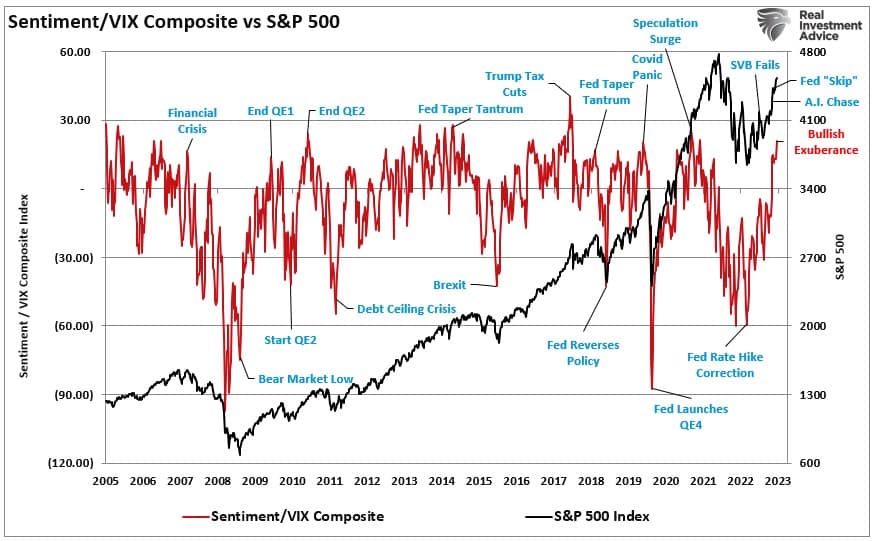

Furthermore, the sentiment of both retail and professional investors is getting rather extreme, along with the drop in volatility, which also suggests a correction is likely. Both charts below show that these indicators often align with short-term market peaks.

We continue to suggest remaining patient and opportunistically increasing equity exposure as needed. While it may “feel” like you are missing the boat currently, the market will always give you another opportunity to get on board.

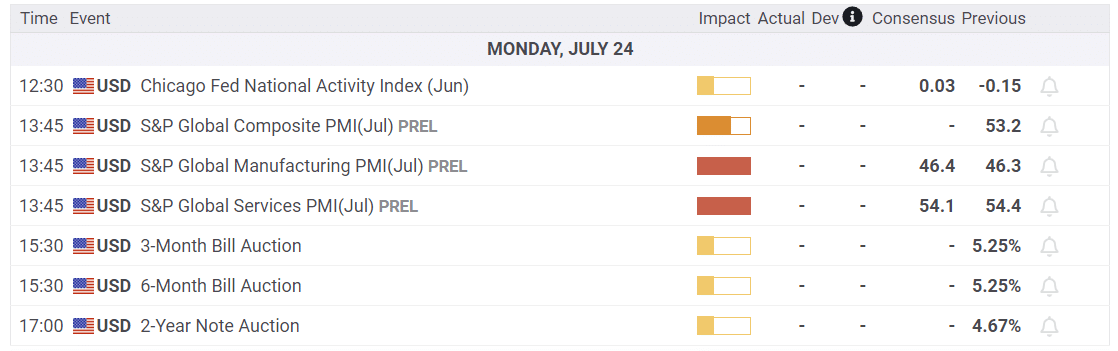

The Week Ahead

The Fed highlights the week with its FOMC policy meeting occurring on Wednesday. As shown below, the market implies a 99.8% chance the Fed will hike rates by 25 basis points. Will their comments and outlook push for another rate hike in September or November? Currently, the market only assigns a 28% chance of another rate hike. The first implied rate cut doesn’t occur until March. As you may recall, only a few months ago, the market thought the Fed could cut rates by over 1% by year-end.

Guiding the Fed will be Friday’s PCE price index. Like the June CPI report, the PCE index will fall sharply year-over-year. The current estimate is for a decline from 3.8% to 2.9%. The monthly rate is only expected to be 0.1%, or 1.2% annually. While the headline PCE estimates are good, Core PCE is expected to fall from 4.6% to 4.3% year-over-year. Such will likely keep the Fed concerned and stoke their desire to keep rates higher for longer.

The Nasdaq will rebalance today. We are unsure how much of the rebalance has already occurred versus what will happen today. More importantly for the Nasdaq will be a slew of earnings reports from its most prominent positions. On the slate this week are MSFT (7/25), AMZN (7/27), GOOG (7/24), and META (7/26). Apple reports next week, and the much anticipated Nvidia report will not be until August 23.

Good and Bad Economic News

While the stock market roars ahead, with many investors believing a recession is no longer in the cards, other indicators have mixed outlooks. This past week we had two opposing data points worth considering.

For the optimists, the Philadelphia Fed manufacturing survey showed a huge jump in expected future activity and, in particular, new orders. It is the largest two-month increase since March 1991. While encouraging, the Philadelphia Fed region is relatively small in geographic footprint and can be volatile. We would like confirmation of improving outlooks from other regional surveys and the broader national indexes.

While the Philadelphia Fed spreads optimism, the Conference Board’s Leading Economic Indicators continue to forecast a recession. The indicator is now down 9.9% from its recent peak. As the Bloomberg graph below shows, in the last 65 years, the index has never fallen as much as it has without a recession occurring. Will this time be different?

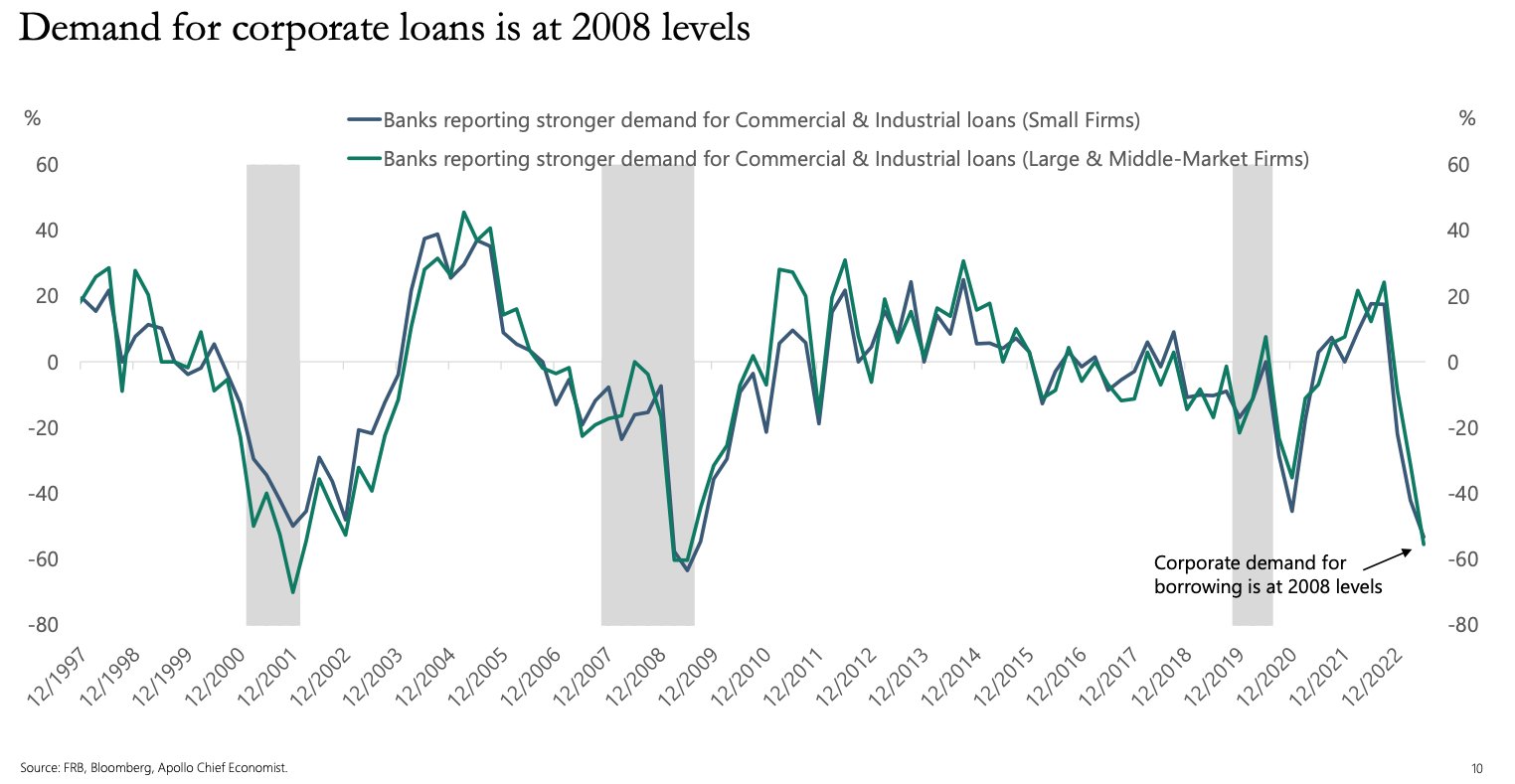

Corporate Loan Demand is also Weak

The graph below from Apollo shows it’s not just consumer borrowing slowing. Demand for Business loans (C&I) is at its lowest level in 15 years. While the graph is daunting, it’s unclear what this may mean. Did many of these firms borrow at dirt-cheap borrowing rates in 2020 and 2021 and still hold excess cash? Or is this an indicator that they expect business to slow in the coming quarters?

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.