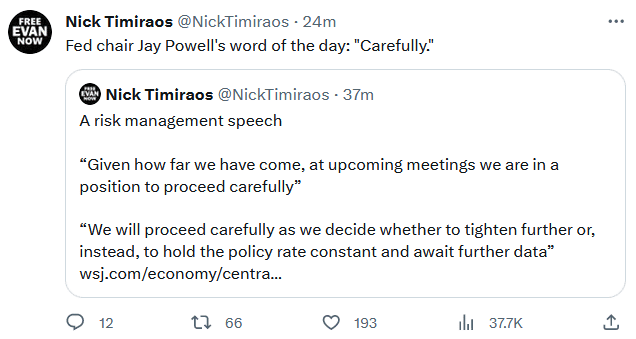

The much-anticipated speech by Chair Powell at the annual Fed Jackson Hole Symposium shed little new light on the course of monetary policy. Chair Powell opened the address by stressing their number one goal: “It is the Fed’s job to bring inflation down to our 2 percent goal, and we will do so.” His statement squashes comments from other Fed members about potentially raising the neutral rate. The Fed and Chair Powell are willing to raise rates if needed but remain aware of the risks of what the Fed has done and of compounding said risks by increasing rates further. He concludes the speech by highlighting their uncertainty: “As is often the case, we are navigating by the stars under cloudy skies. In such circumstances, risk-management considerations are critical.“

The key takeaway in our mind is that Chair Powell harbors deep concern that the lag effects of prior rate hikes will be a significant drag on the economy. WSJ reporter Nick Timiraos sums the speech up well in our graphic below. Simply, the Fed and Chair Powell must “carefully” balance what they have done with what they might do.

“That assessment is further complicated by uncertainty about the duration of the lags with which monetary tightening affects economic activity and especially inflation. Since the symposium a year ago, the Committee has raised the policy rate by 300 basis points, including 100 basis points over the past seven months. And we have substantially reduced the size of our securities holdings. The wide range of estimates of these lags suggests that there may be significant further drag in the pipeline.” – Chair Powell

What To Watch Today

Economics

Earnings

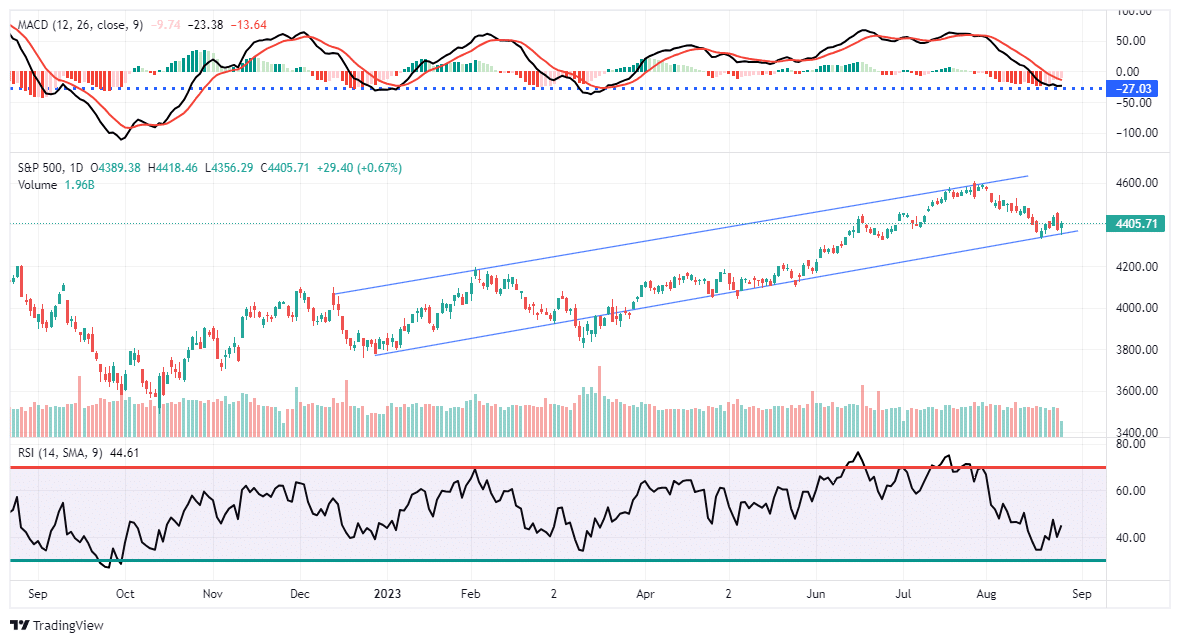

Market Trading Update

After Jerome Powell’s “Nothing Burger” speech on Friday, investors returned their focus back to earnings as the season winds down. While the August correction continues, so far, that correction remains orderly without a sharp increase in volatility. The markets are now reaching more oversold short-term levels, so a counter-trend rally is becoming more likely in the short term. We continue suggesting using this particular sell-off to add to equity positions as needed but use counter-trend rallies to sell into as needed to rebalance holdings.

As we move into Q4, we currently still expect to see portfolio managers chase the market to lock in returns for year-end reporting. However, once we get into 2024, the outlook becomes much more “Cloudy With A Chance Of Meatballs.”

The Week Ahead

It’s employment week!

The latest round of jobs data starts on Tuesday with the JOLTs report. The number of job openings is expected to be the same as last month at 9.58 million. The ADP report on Wednesday and the BLS employment report on Friday will further clue us into the health of the labor markets. Current expectations are for the number of jobs to increase by 180k, slightly below last month’s 187k. The unemployment rate is expected to be unchanged at 3.5%.

In addition to jobs data, we will get the Fed’s preferred inflation indicator, PCE, on Thursday. The monthly rate is expected to be 0.2%. Chicago PMI and ISM on Thursday and Friday, respectively, will update us on the state of manufacturing.

The week before Labor Day is often sleepy in terms of market activity and economic releases. This one may be different!

Employment, Recessions, And The NBER

The two graphs below show that sharply increasing jobless claims and unemployment are timely recession indicators. However, for those trying to forecast a recession, there is a problem with that statement. The National Bureau of Economic Research (NBER), the official arbiter of recessions, post-dates recessions well after they actually started. For example, the NBER declared the pandemic recession started and ended two months after the recession ended by their declaration.

It’s not just NBER that is late to call a recession. In December 2008, the NBER declared the financial crisis recession started in December 2007. By the time the NBER declared recession, the labor market was reeling. In fact, one month after the recession started, then-Fed member Janet Yellen was not even sure we were in a recession. To wit:

The possibilities of a credit crunch developing and of the economy slipping into a recession seem all too real …. I am particularly concerned that we may now be seeing the first signs of spillovers from the housing and financial sectors to the broader economy– Courtesy of The Atlantic

Summers Uses Trickery To Warn Of More Inflation

The tweet below from Lawrence Summers, in which he warns of a longer-term inflationary phase, like the 1970s, is misleading. As he shows, inflation over the last ten years seems to be nearly perfectly correlated with 1966 through 1975. The graph is very misleading. First, he appears to have randomly chosen dates to find similar data. Federal deficits started to rise sharply in the mid-60s. However, the culprit of today’s inflation was fiscal spending in 2020 and 2021, not 2013.

Second, he plays the oldest trick in the book for chartists. The left axis being used for recent CPI scales from 0 to 10. The right axis for the 60s and 70s goes from 2 to 14. The second graph compares the two periods using the same axis. CPI spiked from 2 to 6 in the lead-up to the early 1970s inflation outbreak. In the period before the recent bout of inflation, CPI was relatively flat at 2%. The inflation spikes on his graph occurred over similar periods, but the recent peak was almost 4% less than in the early 70s.

To ascertain if the two periods are comparable, one must compare fundamental similarities and differences between those periods. In the 60s/70s, Federal spending was high due to Vietnam and the surge in social spending. However, the nation’s debt-to-GDP ratio was only 40. Today, it is three times that amount. Household and corporate debt is also significantly higher since then. Further, nominal GDP during the late ’60s and early ’70s averaged around 8%. Therefore, higher inflation is not shocking. Until the recent pandemic-related surge, GDP has been running at about half of that rate.

We could go on and on, but the bottom line is that those two periods are incomparable.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.