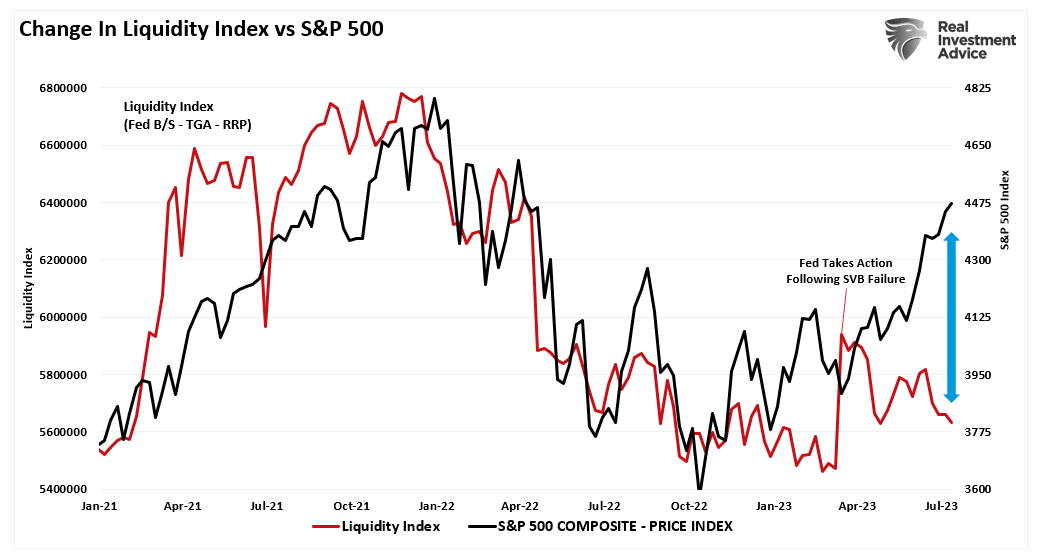

The federal debt cap was lifted on June 3, 2023. The Treasury immediately flooded the markets with large debt issuance to meet its massive borrowing needs. Most investors presumed market liquidity would decline as net positive Treasury issuance pulls money from other investments. As shown below, the Treasury has since added about $450 billion to its TGA account at the Fed. Yet, while the Treasury removed said liquidity, the Fed’s reverse repurchase program (RRP) also fell, which provides liquidity to the markets. The program balances fell because of the slew of bills available to repo participants, as well as the rate the Fed accepts repo at. Per the graph, when the two liquidity factors are netted, liquidity only fell by $143 billion, about $300 billion less than many expected. Therefore, we must ask, are the Fed and Treasury managing liquidity as it appears?

Such doesn’t seem preposterous given the recent banking challenges that, while being arrested, are not resolved. Further, the Fed skipped a rate hike while the Treasury was draining liquidity. Higher short-term rates reduce liquidity as leverage becomes more expensive. The Fed is expected to hike rates on July 26th. Consequently, might the Treasury drain its TGA account balances and issue less short-term debt to help counteract the higher rates? We presume the Fed and Treasury are closely watching liquidity. As a result, they have a moderate amount of control over how the stock market performs. Suppose the Fed offers concern that higher stock prices drive inflationary imbalances. In that case, this may be a cloaked warning that the Fed and Treasury will reduce liquidity via more QT or the levers we discuss above.

What To Watch Today

Earnings

Economy

Market Trading Update

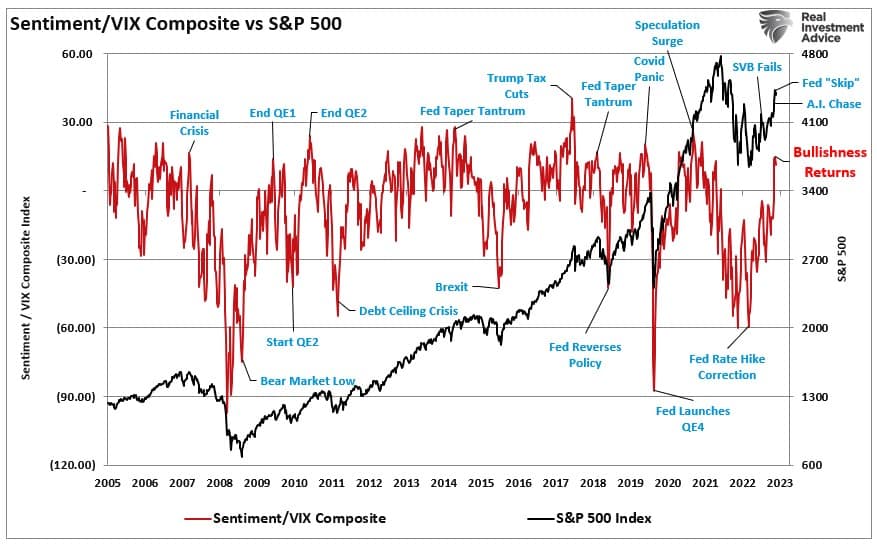

As the “earnings season” flood gets underway, market participants have to parse through a lot of data. However, so far, the big “fear” was further deterioration of the banking system which seems not to be the case. Yes, deposits have declined, but overall earnings align with estimates, and outlooks are mostly optimistic. However, behind the scenes, it is worth noting the bullish exuberance of the market has now detached from underlying liquidity. While such is not surprising in the short term, it is unlikely to remain that way indefinitely.

However, as noted in yesterday’s missive, the surge in sentiment and the collapse in volatility is currently supporting the market advance. To wit:

“To understand the relationship to the market, we created a composite index. The index combines retail and institutional investors’ net bullish sentiment and an inverted volatility index (1 minus the VIX reading). We overlaid the composite index against the S&P 500 index. Unsurprisingly, high index readings regularly associate with market events and corrections. Low readings occur near market lows.”

We continue to suggest that Investors should expect a correction with the combined index readings approaching higher levels. However, that correction can take some time to materialize amid a surge of bullish exuberance. It seems logical that investors should use the recent rally to rebalance risks and raise cash levels in order to take advantage of “buying the dip” when it eventually occurs.

BB-rated Credit Spreads Signal Good Times Ahead

Lisa Abramowicz of Bloomberg showed a graph similar to the top graph below of credit spreads and stated:

Spreads on high-yield bonds have fallen to the lowest since April 2022. If credit is a forward looking indicator, it’s suggesting we’re not going to see any kind of default cycle of note.

Her suggestion sounds logical, but credit spreads are not always a reliable leading indicator. The shaded circle in the first graph highlights the 2006-2008 period. As it shows, spreads in late 2006 were similar to current levels. They then dropped by a little more than half a percent. The spread, at the time, indicated nero zero stress in the system and an abundance of optimism among bond traders. Within six months, the spread surged by 4% and continued until BB-rated spreads hit 12%. Those believing the corporate junk bond market was sending an all-clear to take on risk paid dearly. We offer a similar warning today. While a financial crisis like 2008 does not seem likely, high-interest rates and an overly indebted economy are not factors we should sleep on.

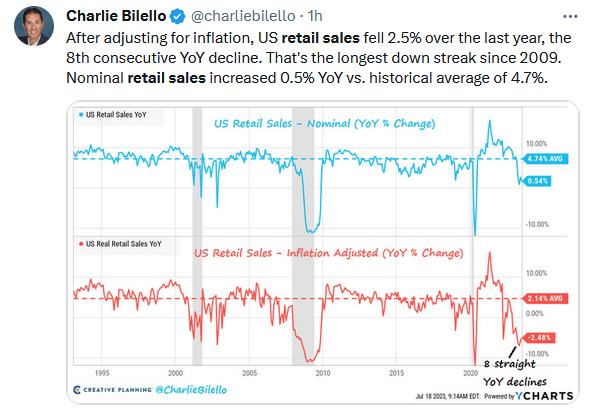

Retail Sales

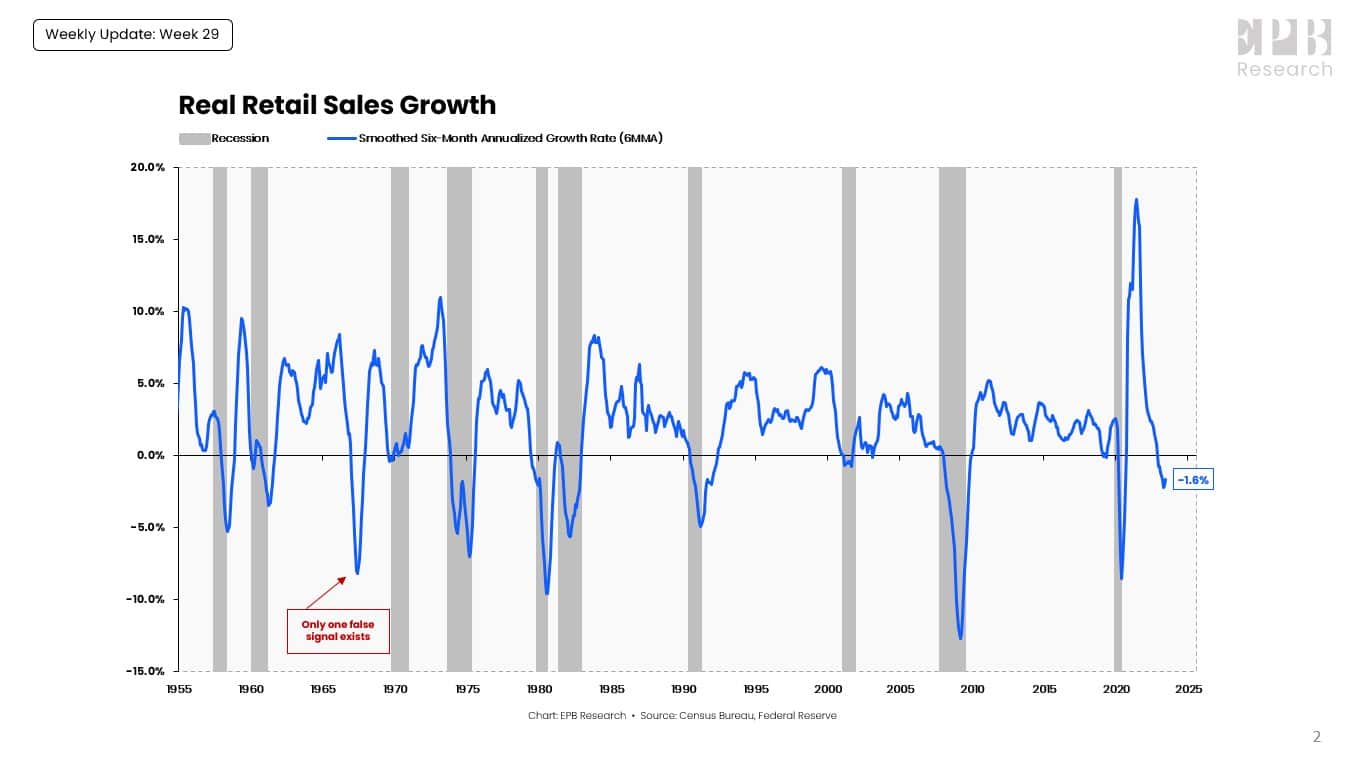

Retail sales grew by 0.2% last month versus expectations for 0.5% growth. Year-over-year retail sales growth is down to 1.49%. The tricky part of analyzing retail sales is inflation. As we share in our Tweet of the Day, retail sales are down 2.5% for the year after adjusting for inflation. Such marks the eighth consecutive decline. The graph below, courtesy of EPB Research, shows that since 1955 a sustained decline in real retail sales, as we have, has preceded every recession. The only false signal was in 1967.

The good news is that the Control Group, which feeds GDP, rose 0.6%. The second graph below, courtesy of EY-Parthenon, breaks down the monthly change in retail sales by sector.

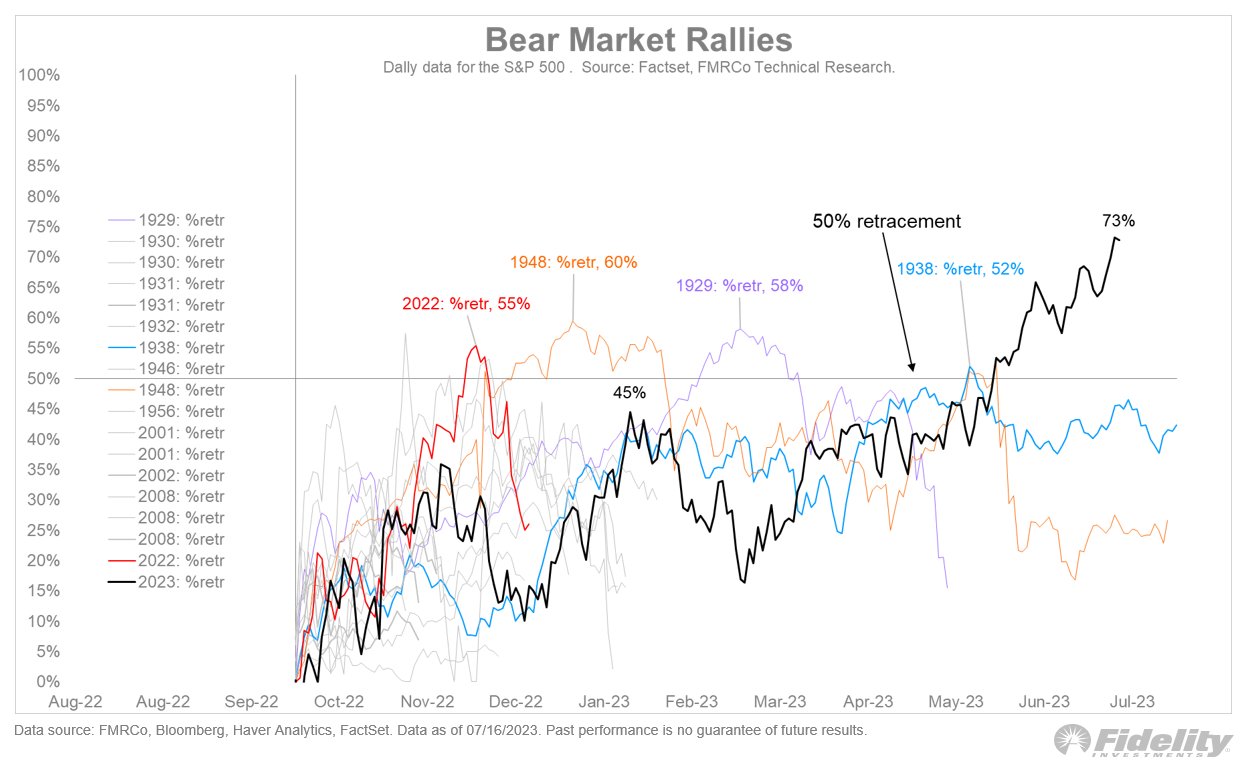

If it Doesn’t Look Like A Bear, is it?

The following graph and commentary from Fidelity’s Jurrien Timmer provide historical context for the recent rally. It’s hard to argue with his conclusion that we are no longer in a bear market rally.

The stock market has regained nearly three-fourths of the ground it lost last year. Bear-market rallies don’t retrace much more than half their preceding decline. When they do, they are usually new bull markets. With our current 73% retracement, history seems to be on the bulls’ side here. We could still be in a long trading range (like the 1940s), but the market has now spent a year and a half—a long time—bucking the long-term uptrend.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.