The travel and leisure sector is one of the hottest industries driving job growth. Since the pandemic, the travel and leisure industry added one million jobs, equating to 6% growth, about double the labor market’s growth over the same period. While the industry has greatly benefited from the resumption of regular travel and leisure activities, the airlines have yet to recover. TSA reports that the number of air travelers in the U.S. for 2023 to date is up less than half a percent versus the same period in 2019. Per the Department of Transportation, average airline fares in the first quarter of 2023 are up about 10% versus the same quarter in 2019. However, on an inflation-adjusted basis, they are down 8%. The graph below shows the major airlines are still down 30-60% from the pre-pandemic peak. Over the same period, the S&P 500 is about 40%.

Labor and fuel account for over 50% of airline expenses. Per the BLS, the number of workers employed in the airline industry is up by less than 10% since the pandemic. However, the median wages for pilots and engineers are up over 30%. Also problematic, jet fuel prices are up over 80% since January 2020, despite crude oil only rising 11%. The bottom line is profit margins for the airline industry are getting squeezed. Before the pandemic, the aggregate margin (net income to sales) for the four stocks graphed hovered between 7% and 8%. Over the last 12 months, it is a mere 2.25%, which compares favorably to the previous two years. While the travel industry has recovered, airlines continue to struggle.

What To Watch Today

Earnings

- No notable earnings releases

Economics

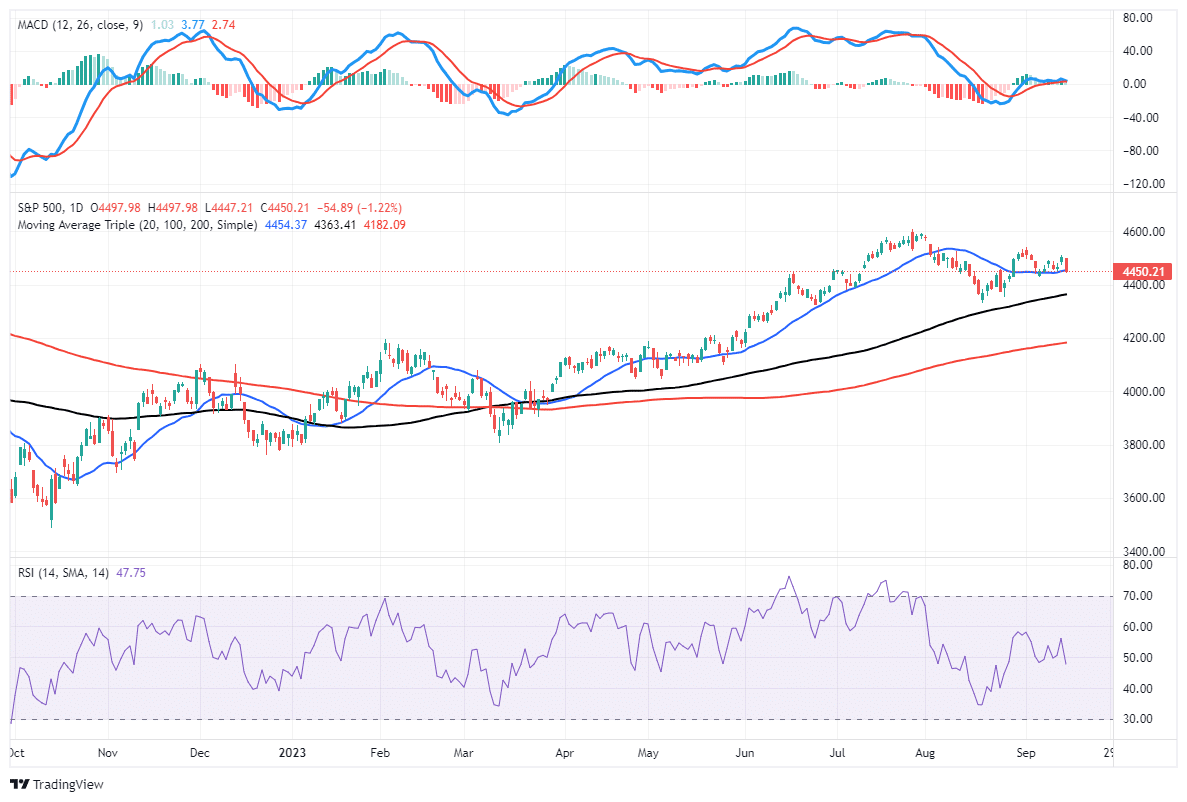

Market Trading Update

As we noted last week,

“The more extreme overbought condition is about halfway through a corrective cycle, suggesting we could see further “sloppy” trading next week. With the market holding within a consolidation range, a breakout to the upside should confirm the start of the seasonal strong trading period into year-end.”

Such remained the case this past week. Friday was particularly choppy as one of the largest options expiration days on record. With nearly $3.2 Trillion in options expiring, stocks traded negatively for the day.

Unsurprisingly, given the recent performance of the mega-cap stocks, which has recently attracted most of the liquidity flows, the selling pressure was primarily contained within those names, with value stocks outperforming for the day. However, the market held support at the 50-DMA on Friday, with the overall price conditions remaining neutral. Like a groundhog that sees its shadow, the MACD signal is close to registering a “sell signal.” If the signal triggers it could signal a couple of additional weeks of sloppy trading action heading into October. Such would be consistent with seasonal weakness before heading into the last trading quarter of the year.

For now, there is no change to the bullish backdrop of the market, and nothing suggests a need to become more cautious near term. It is always possible that analysis could change over the next couple of weeks, and if it does, we will suggest reducing equity exposure and becoming more cautious.

The Week Ahead

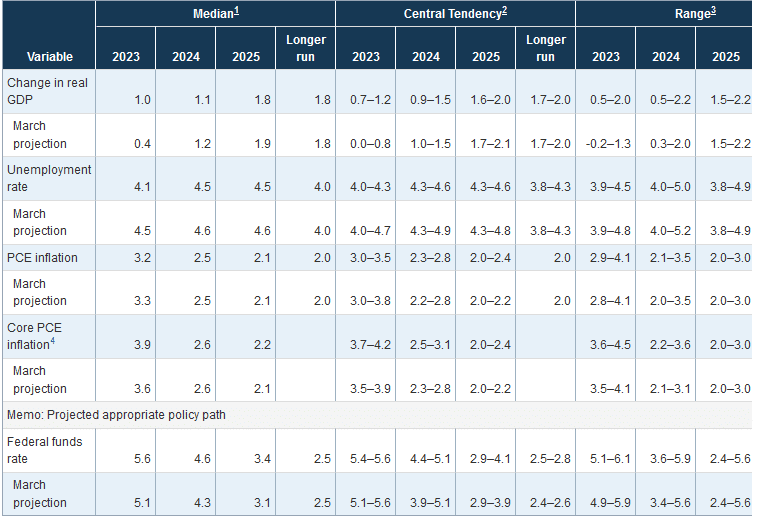

This week’s highlight will be Wednesday’s FOMC meeting statement and Powell press conference. Despite relatively strong economic data and inflation data slightly above expectations, the market continues to assign a near-zero chance they hike rates. The Fed will also update its projections for GDP, unemployment, inflation, and the Fed Funds rate. The table below shows the projections from June. Any changes to their inflation and Fed Funds forecasts are likely to have a market impact. Fed members will be open to speaking following the meeting. Accordingly, we suspect their thoughts will help better assess the odds of a November rate hike. Currently, it stands around 50%.

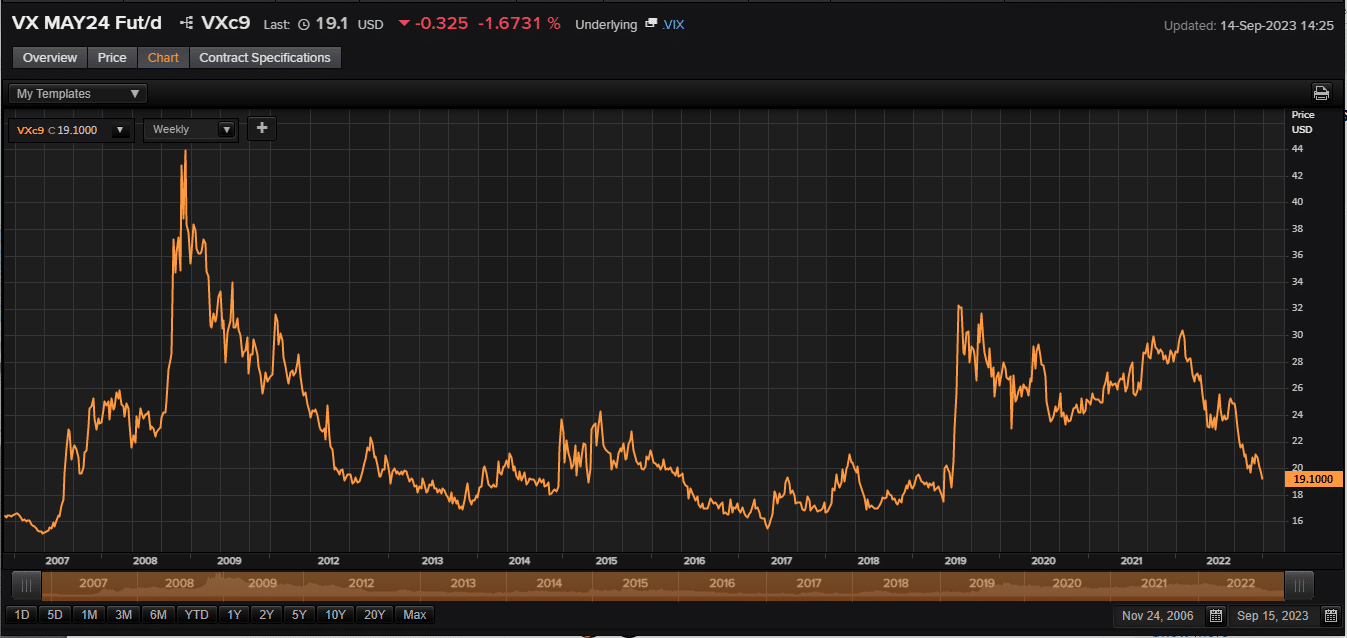

Volatility Is Back To Pre-Pandemic Levels

Volatility (VIX) has fallen to its lowest level since the pandemic started. While low volatility is a sign of complacency and is typically followed by periods of high volatility, it can remain suppressed for long periods. As shown below, the current VIX level preceded surges in the VIX. Yet it is also the norm for the better part of 2013 to 2019 and the two years leading up to the financial crisis.

The second graph shows the continuous ninth VIX futures contract. This contract covers the implied volatility for nine months forward. This contract is a key factor driving costs for longer-term option protection.

Treasury Return Scenarios

A reader asked us if we could quantify the potential performance of Treasury bonds given changes in yield levels. The table below shows the potential performance is skewed to the upside. This occurs because the high current yields cushion price declines if rates rise. The formula to approximate the one-year expected total return is the yield plus the change in rate times the bond’s duration.

As we show, two-year note yields can rise 2%, and the 5.01% yield offsets the potential decline in its price. At the other end of the maturity spectrum, a 2% decline in 10-year rates will result in a 20% gain, nearly double the potential loss if rates rise by the same amount.

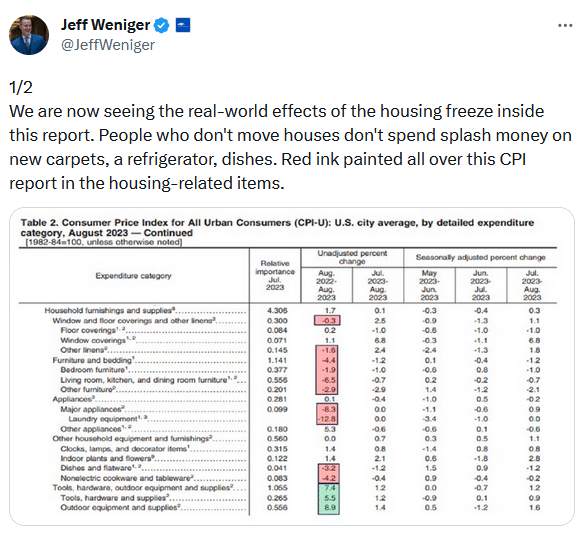

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.