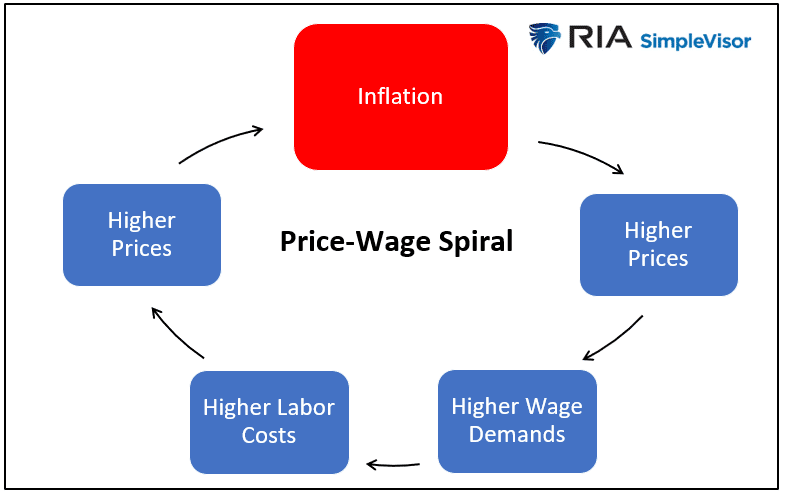

The nation’s supply lines were spared a massive blow as the rail workers union and management reached a tentative deal to avoid a strike. A rail worker strike would have pushed prices higher for many goods and further heightened the Fed’s inflation worries. While the risk of a rail strike was averted, the agreement may play into another Fed worry- a price-wage spiral.

Per CNN Business: “The deal gives the union members an immediate 14% raise with back pay dating back to 2020, and raises totaling 24% during the five-year life of the contract, that runs from 2020 through 2024. It also gives them cash bonuses of $1,000 a year. All told, the backpay and earlier bonuses will give union members an average of an $11,000 payment per person once the deal is ratified.” It’s highly likely rail companies will increase their freight rates. If so, a price wage spiral in rail shipping is upon us. Similar spirals are occurring in many other industries.

What To Watch Today

Economy

- 10:00 a.m. ET: University of Michigan Consumer Sentiment, September preliminary (60.0 expected, 58.2 prior)

Earnings

- No earnings releases today.

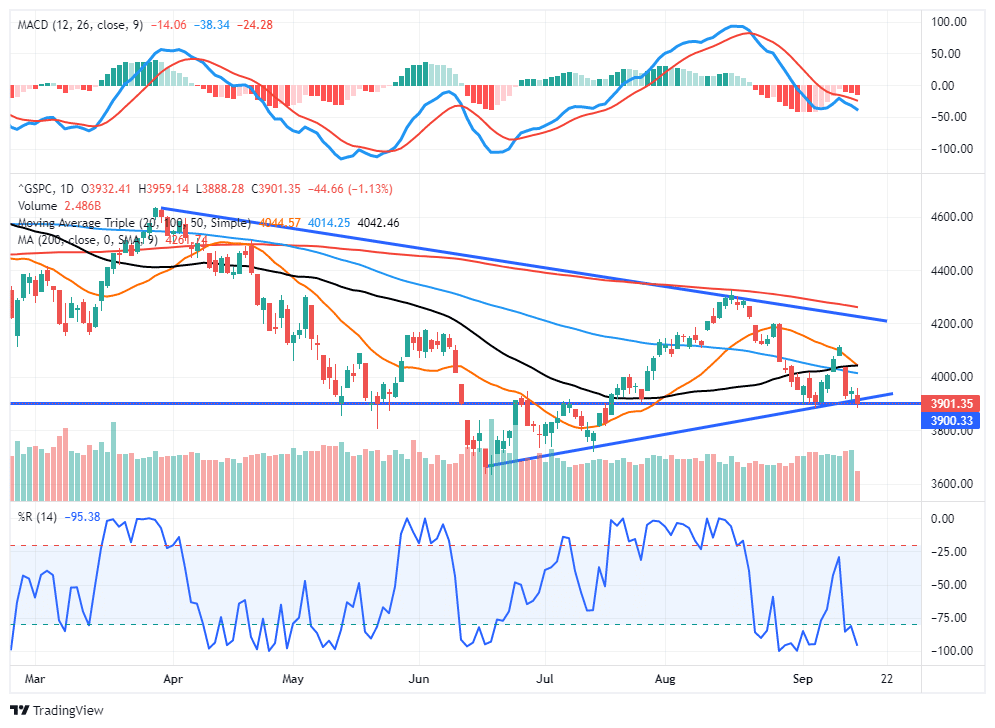

Market Trading Update

There isn’t a lot of good news to report. After the bullish advance last week that took markets onto a more bullish footing, that was completely reversed this week. Yesterday, the market did break the important bullish trend line. However, it did hold important support going back to the May lows. With the market back to more oversold levels, a bounce is likely.

Today is a large options expiration day, so market volatility will likely be high. As noted yesterday, the returns post options expiration day tends to be better, so if your inclination is to panic sell, you may want to wait for a bounce.

The MACD signal remains on a “sell signal,” which also continues to suggest downward pressure on prices, so rallies should continue to be used to raise cash and reduce risk.

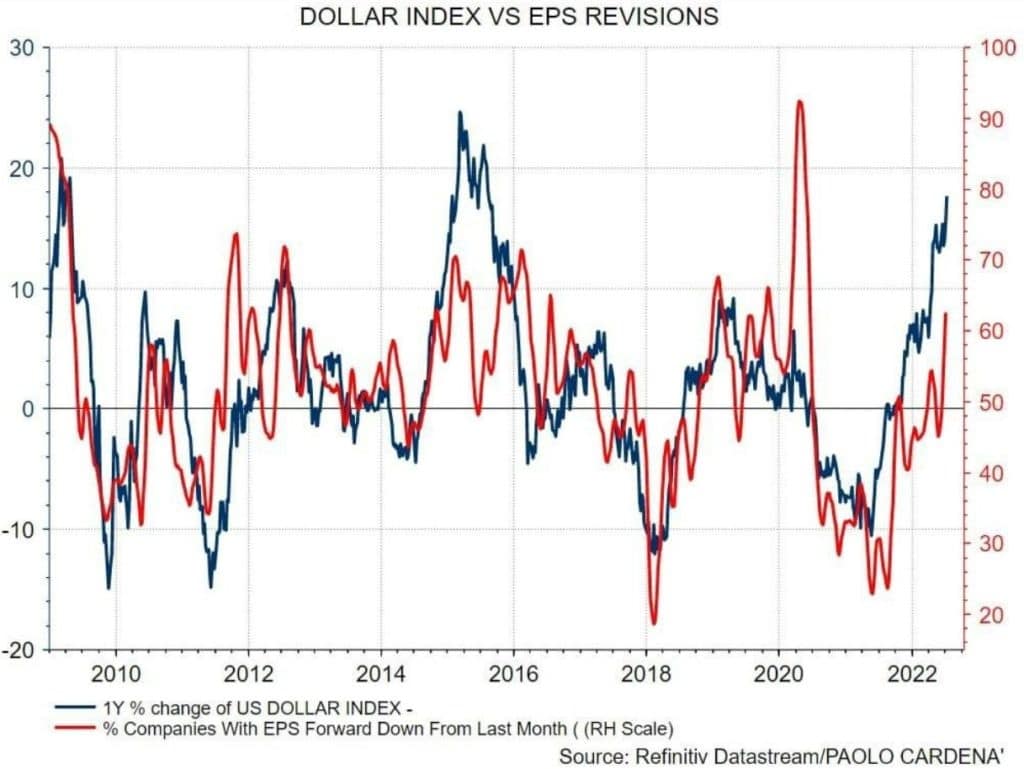

The Dollar and Earnings

Dollar strength has been on center stage and many investors are trying to figure out what it may entail. From an equity perspective, consider that approximately a third of S&P 500 earnings come from foreign countries. As a result, the link between profits and the dollar is strong. The graph below shows the strong correlation between changes in the dollar and earnings revisions. With the dollar index up about 20% over the last year and sitting at 20-year highs, we argue that earnings are even more sensitive to dollar strength than is typical.

Further bolstering the relationship, bond yields and the dollar are recently showing high levels of correlation. As the dollar and yields rise, the present value of corporate profits declines. Additionally, higher bond yields increase corporate borrowing costs, thereby reducing earnings.

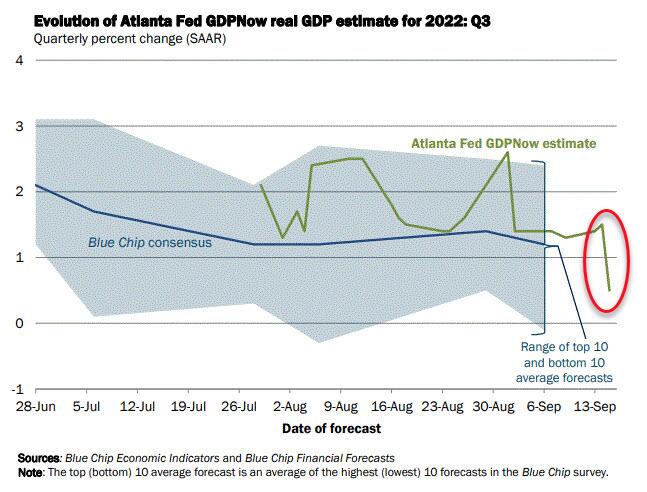

The Economy Is Sick

“Echoing Jim Cramer’s infamous 2007 “they know nothing” rant, a far more calm and eloquent Barry Sternlicht, Chairman and CEO of Starwood Capital, warned the co-anchors on CNBC this morning that if the Fed doesn’t pump the brakes on its rate hikes, the US economy is facing a serious downturn.” – Zerohedge

“The economy is braking hard,” Sternlicht told the outlet.

“If the Fed keeps this up, they are going to have a serious recession and people will lose their jobs.”

He was proved right quickly as The Atlanta Fed cut its GDP forecast for Q3 to just +0.5%.

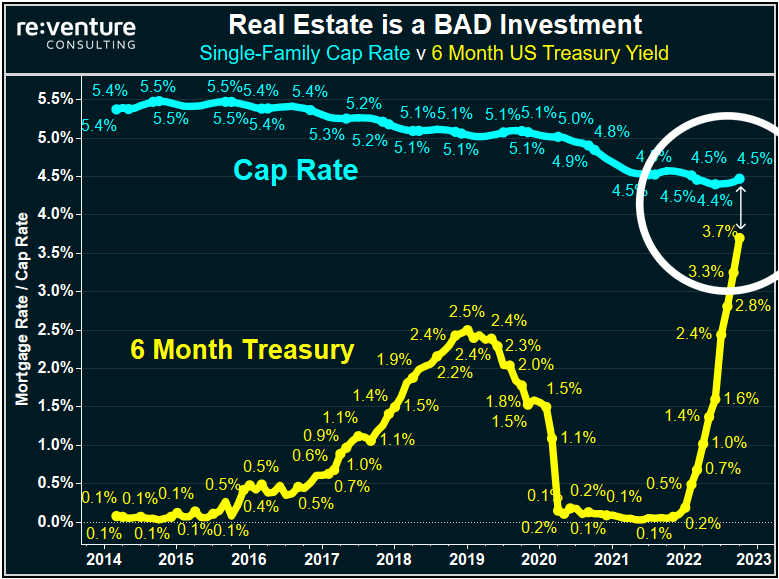

Buy and Rent or Buy a T-Bill?

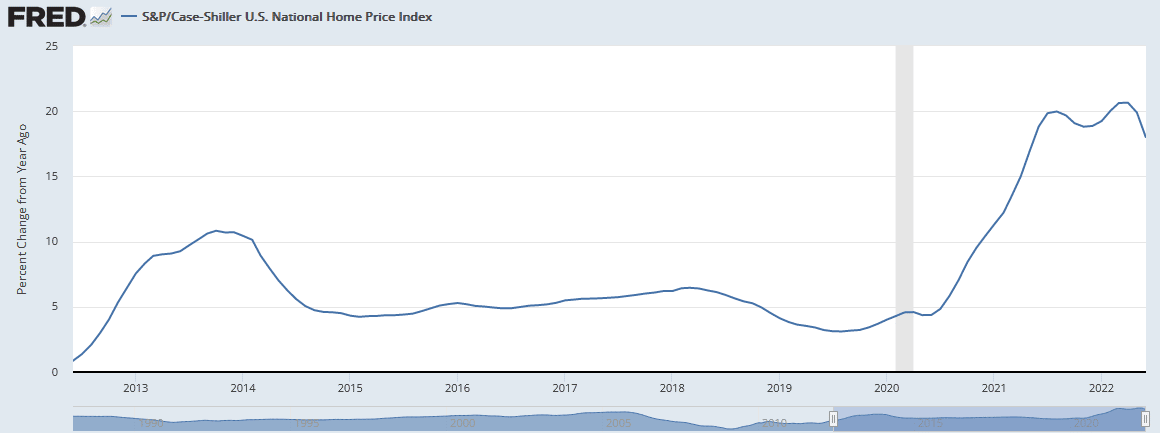

Buying a single-family home and renting it out should provide a much better return than buying no-risk Treasury bills. The graph below shows that over the last ten years, such an investment strategy would yield an additional 2.5% to 5% more than a six-month Treasury bill. Today the reward for buying and renting is less than 1%. Now consider that for less than 1%, someone doing a buy and rent strategy runs the probable risk that home prices depreciate over the short run, maintenance costs are higher than expected, and you can not rent the property 100% of the time. Either bill yields are too high, or house prices are too high. The second graph below helps answer the question.

Mixed Economic Data

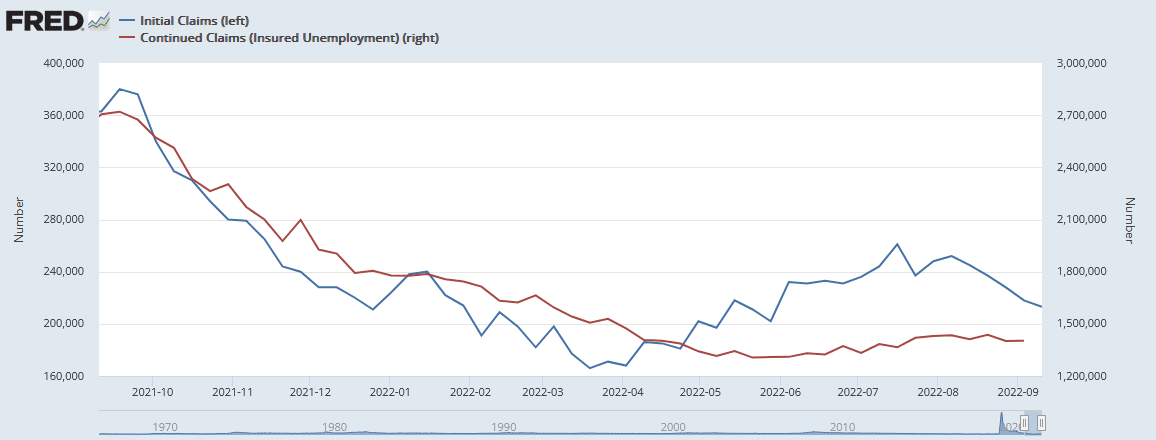

Jobless Claims continue to decline. This week claims fell to 213k, well below the recent high point of 261k in mid-July. Continuing claims are not dropping. This is potentially a sign that the recently laid-off workers are finding it hard to get a new job. That said, continuing claims can often lag jobless claims by a few months.

Retail sales were a mixed bag. The headline number was +0.3% versus expectations of 0.0%. However, July was revised lower by 0.4%. Further, if we strip out volatile auto sales, retail sales were down 0.4%.

The Philadelphia Fed and Empire State Manufacturing Indexes were also mixed. Philly Fed was much weaker than expected at -9.9 versus +2.3. Empire state was negative at -1.5, but it was much better than expectations of -13.5. Both had good news on the inflation front as they both recorded the lowest levels of prices paid since December 2020.

Economists closely follow new orders within the surveys as they are robust leading economic indicators. Despite the proximity of New York to the Mid-Atlantic, the new orders data is strikingly different. New order fell sharply in the Philly survey from -5.1 to -17.6. New orders in the Empire survey rose from -29.6 to +3.7

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.