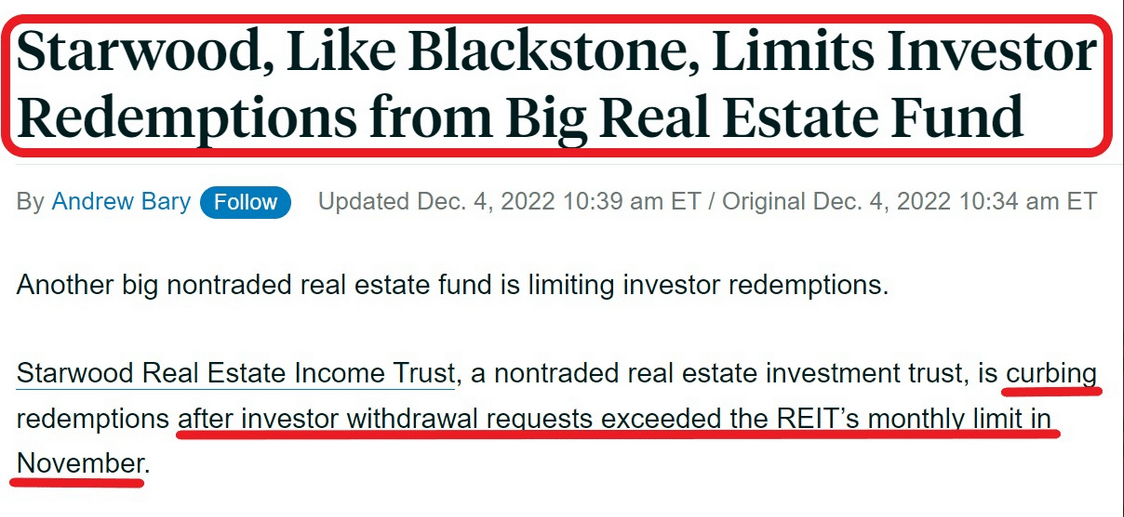

As the Fed pulls liquidity from the financial system, those using too much leverage and or holding speculative assets are usually the first to feel the effects. The demise of FTX and overleveraged English pension funds are two examples. As liquidity continues to decline, liquidity and lower asset prices start to weigh on more traditional asset classes. Private REITs and their sponsors may be the next victim.

Unlike publically traded REITs, private REITs do not trade on open markets. With sporadic NAV updates, private REIT prices tend to be very stable. As a result, investors are often not alert when problems start arising. In many cases, the NAV is determined by periodic appraisals of the underlying property, resulting in higher-than-appropriate prices. Blackstone dominates the private REIT industry, reportedly raising about 70% of all capital raised for private REITs in 2021. As lower real estate prices become a reality, private REIT investors are trying to sell. Unfortunately, liquidity in the underlying real estate investments prevents Blackstone from fulfilling investor demands. Other private equity-like investments may face similar paths as liquidity continues to drain. If these investors need liquidity, they will have to sell more traditional asset classes.

What To Watch Today

Economy

- 8:30 a.m. ET: Initial Jobless Claims, week ended Dec. 3 (230,000 expected, 225,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended Nov. 26 (1.618 million expected, 1.608 million prior)

Earnings

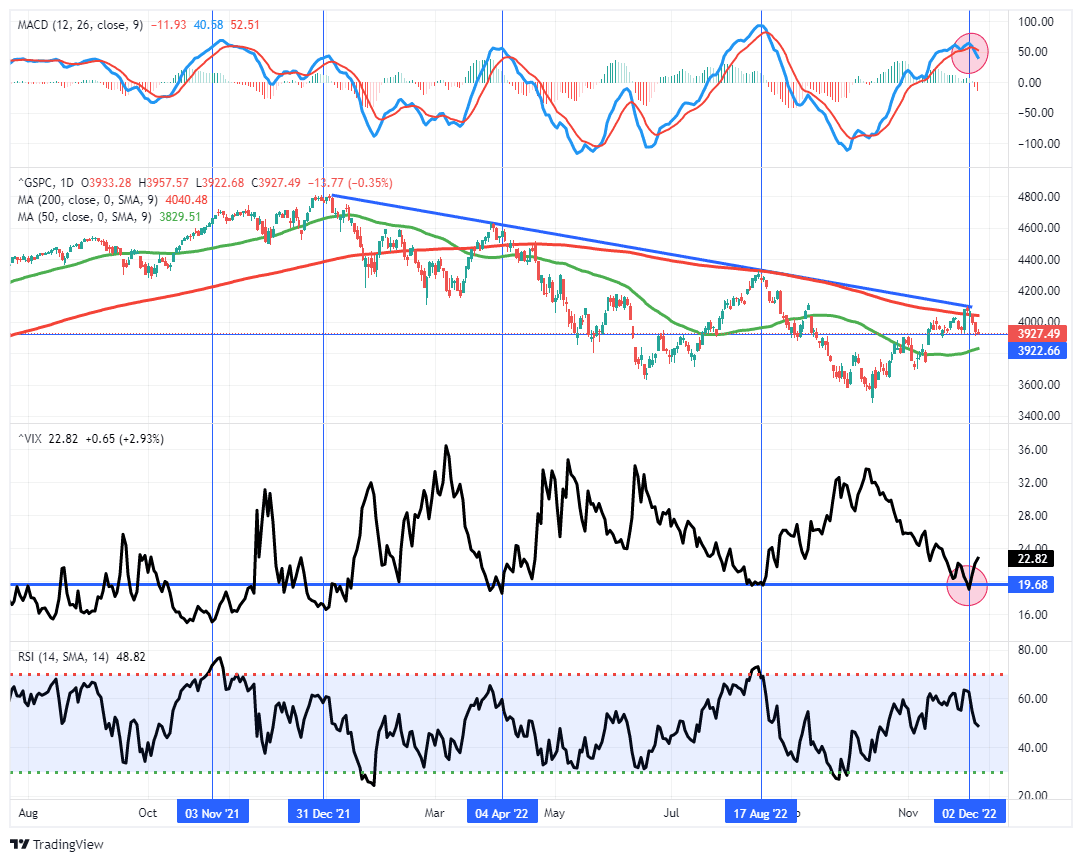

Market Trading Update

A couple of weeks ago, I presented the idea of some sloppy trading action in the first two weeks of December as Mutual Funds go through their annual distributions. So far, such is exactly what we have had. Yesterday, healthcare supported the market while Technology, Financials, Industrials, and Materials weighed on performance. For the day, the market ended lower, further deepening the MACD “sell signal.” Also, the 100-dma and bottoms going back to May lows, as support, remain under attack and must hold through the end of the week. A failure of the 100-dma will put the 50-dma quickly into focus. It is not too late to raise some cash and rebalance portfolio risk.

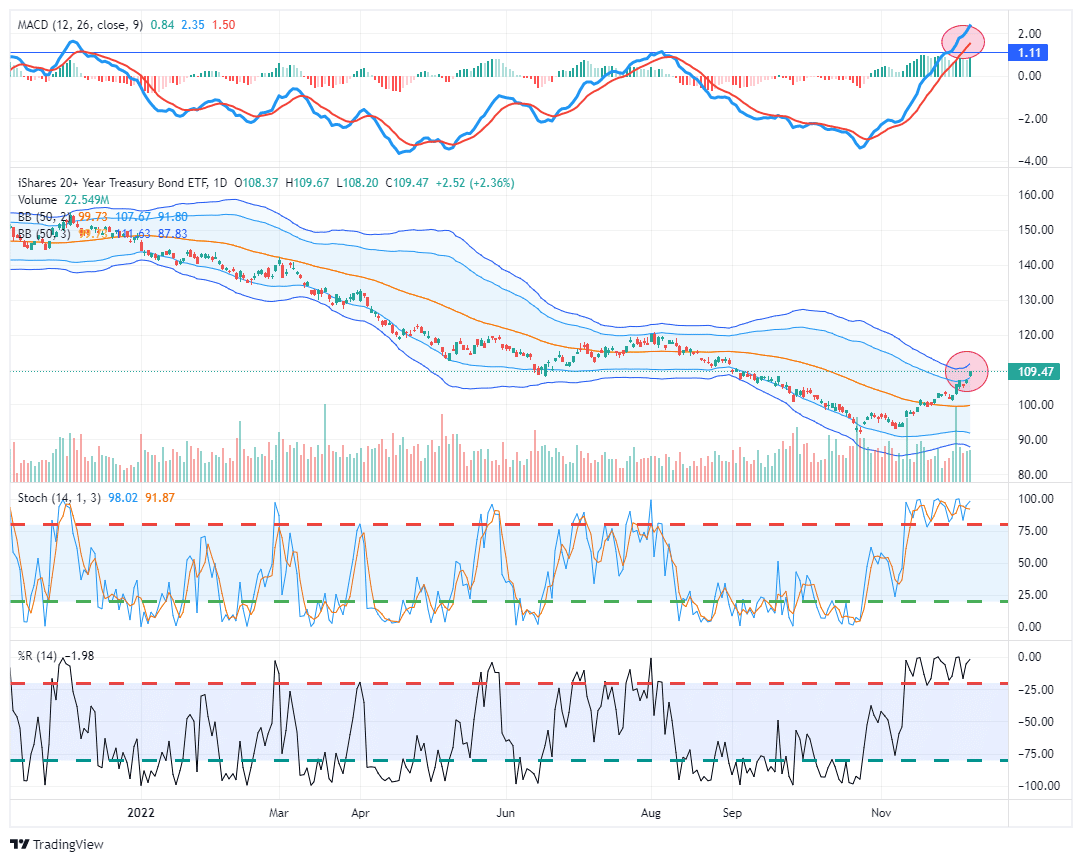

Bonds are now TOO overbought to add to portfolios. Bonds need a pullback to work off the 3-standard deviations extension above the 50-dma, and the overbought conditions. The MACD “buy signal” on TLT is extremely overdone. However, it now appears the bottom for bonds has been made as recessionary risk increases. Look for a pullback to support for adding to current holdings.

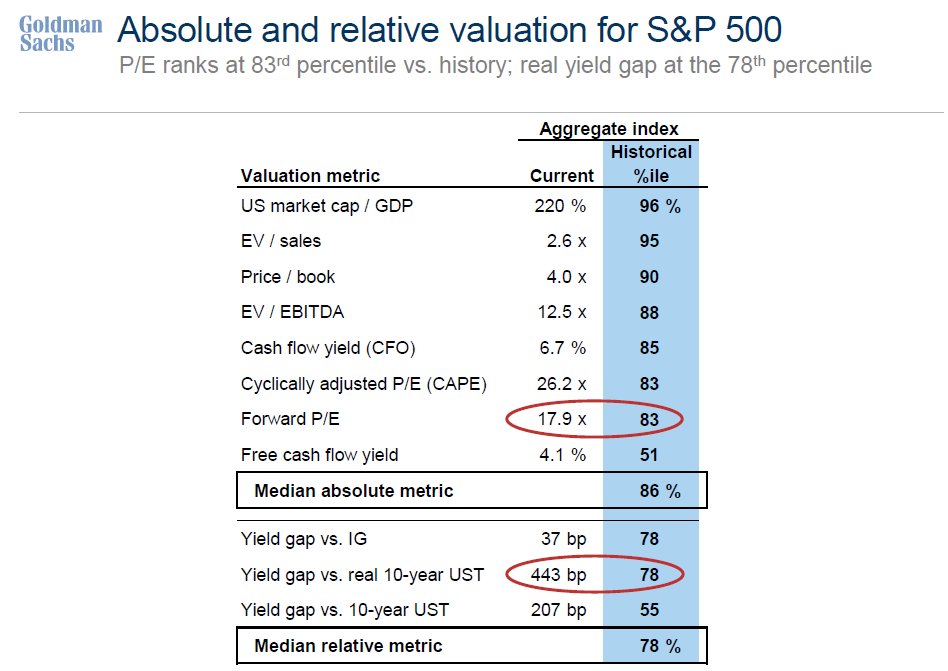

Valuations Remain High

Other than free cash flow yield, equity valuations are still extremely high. If earnings fall next year, these valuations will likely come down, which is only accomplished through lower prices. Valuations are not in the upper 90% range as they were a year ago, but they are still way too high, especially given the Fed’s monetary policy.

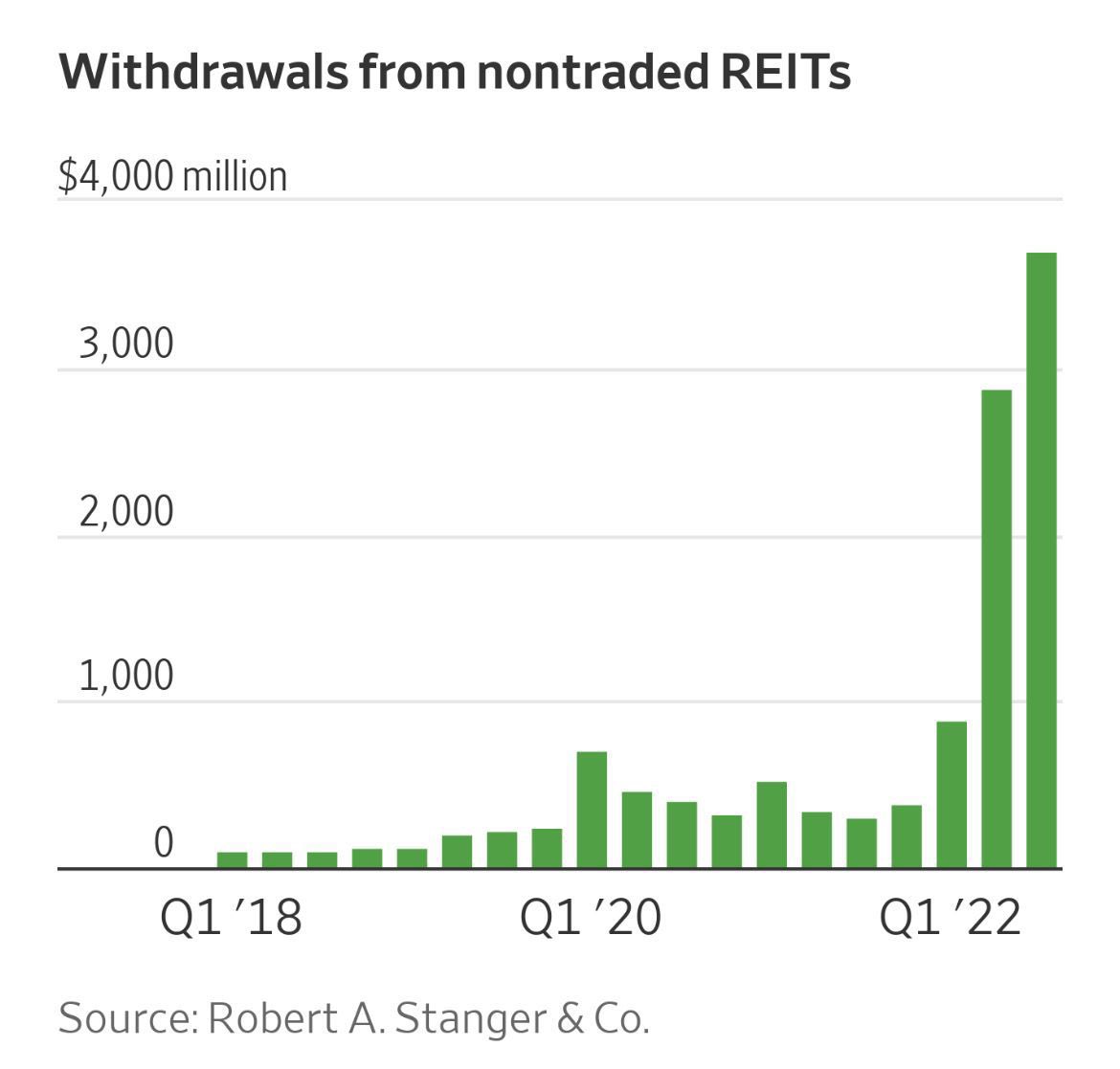

Exodus from Private REITs

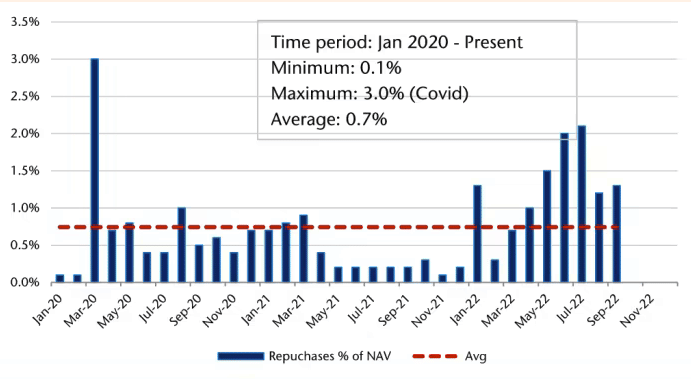

As we note in the lead section, investors are pulling money out of private REITs such as Blackstone’s BREIT. The first graph below shows that redemptions from nontraded REITs totaled $3.7 billion in Q3. Such is a significant increase versus the last few years. The second graph from FT shows redemptions from BREIT. As shown, they are picking up but below the level seen during the height of the pandemic panic. Keep in mind Blackstone is limiting withdraws from its fund to just .3% of the fund’s value. The numbers would likely be much higher if they allowed investors to redeem their investments fully. The reason to gate the funds is twofold. First, they would be forced to liquidate real estate into an illiquid market resulting in price declines and possibly more redemptions. Second, as we discuss below, they would lose significant fee income.

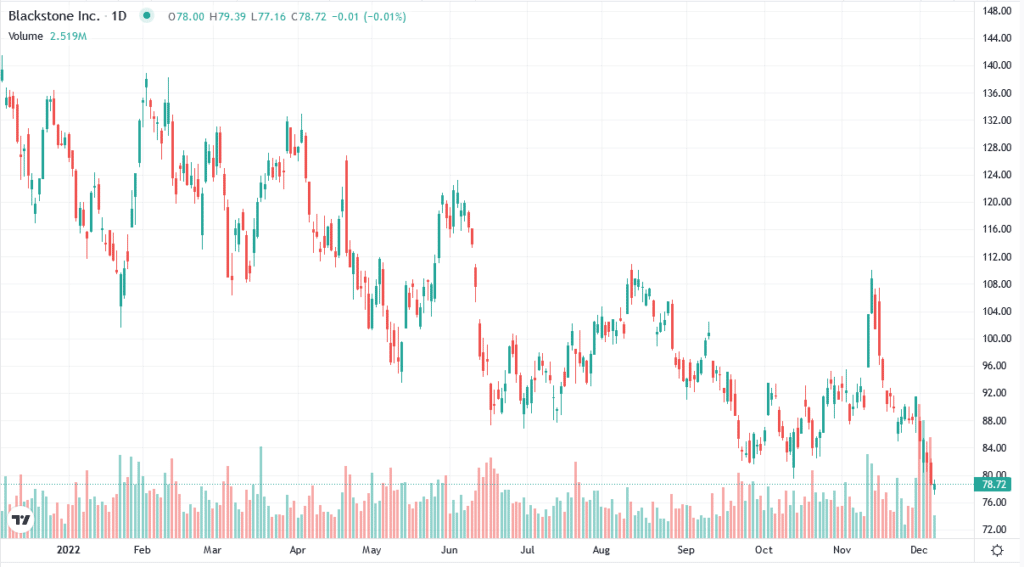

Blackstone

Continuing on today’s private REIT theme, we now discuss how this affects Blackstone, the investment management company. The following data, regarding Blackstone’s BREIT fund, comes from Phil Bak:

Blackstone earns a selling fee of 9.06% spread out over 7 years. They also earn a performance fee of 12.5% of net profits after a 5% hurdle rate. Lastly, Blackstone receives an annual management fee of 1.25%. Per Phil, that comes to 3.62% a year, $2.46 billion a year in fees.

Any wonder why the stock was down 7% when its investors heard about BREIT’s redemption gate?

The possibility of contagion within the real estate industry and other Blackstone funds becomes apparent when considering the situation. If Blackstone liquidates some of its holdings into such an illiquid market, real estate prices could fall rapidly. While BREIT investors and Blackstone shareholders would feel the brunt of it, other public and private REITs and real estate investors would also face the consequences. Further, if investors get spooked because they can not sell their funds, private equity investors may start withdrawing from other funds.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.