Powell testified before the Senate Banking Committee Wednesday morning. He reaffirmed the Fed’s commitment to lowering inflation but admits that achieving a soft landing will be “very challenging”.

Powell also uttered the “R” word as he acknowledged the possibility that rate hikes could trigger a recession. Powell’s comments sent bond yields lower across the curve and put a halt to stocks’ advance on the day. In contrast to the light-footed messaging by Powell, Bill Dudley authored an opinion piece declaring that a recession is inevitable within the next 12 to 18 months.

What To Watch Today

Economy

- 8:30 a.m. ET: Current Account Balance, Q1 (-$275.0 billion expected, -$217.9 billion prior)

- 8:30 a.m. ET: Initial Jobless Claims, week ended June 18 (226,000 expected, 229,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended June 11 (1.320 million expected, 1.312 million prior)

- 9:45 a.m. ET: S&P Global U.S. Manufacturing PMI, June preliminary (56.3 expected, 57 prior)

- 9:45 a.m. ET: ET: S&P Global U.S. Services PMI, June preliminary (53.5 expected, 53.4 prior)

- 9:45 a.m. ET: ET: S&P Global U.S. Composite PMI, June preliminary (53.6 prior)

- 11:00 a.m. ET: Kansas City Fed Manufacturing Activity, June (23 prior)

Earnings

Pre-market

- FactSet Research (FDS) to report adjusted earnings of $3.21 on revenue of $476 million

- Rite Aid (RAD) to report an adjusted loss of 66 cents on revenue of $5.7 billion

- Apogee Enterprises (APOG) to report adj earnings of 55 cents on revenue of $326.22 million

Post-market

- FedEx (FDX) to report adjusted earnings of $6.86 on revenue of $24.57 billion

- BlackBerry (BB) to report an adjusted loss of 5 cents on revenue of $163.5 billion

Market Trading Update – Stocks Recover Early Losses

After yesterday’s strong rally, stocks opened lower ahead of Jerome Powell’s testimony before the Senate. Shortly after the open stocks staged a strong rally back into positive territory and remained above breakeven the rest of the day. The good news is that action confirms we are likely to see some more buying over the next few days. The bad news is that volume and conviction remain very weak and whatever rally we currently get to end just as quickly as it began.

Use the price advance over the last couple of days to start taking profits and raising cash. If we get some more follow-through we will look to add our short S&P index position back into portfolios.

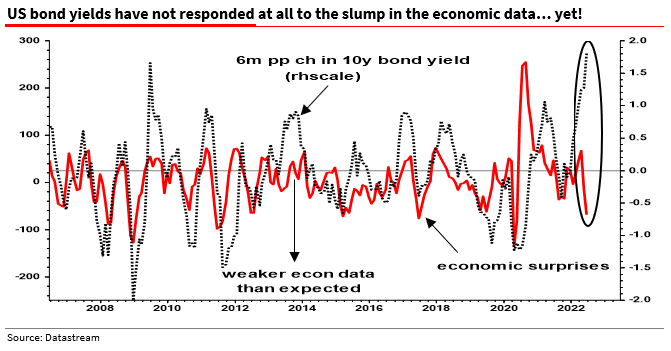

Bond Yields Are About To Catch Down

My colleague Albert Edwards from Societe Generale had a great note out yesterday showing that bond yields have yet to “catch down” to economic growth. (Such is why we remain long bonds as a hedge.)

“Perhaps the more interesting question is not how deep the recession will be, but how large the fall in yields will be? The recent inflation surge broke the close link between the real economy data and bond yields (see chart below). Will a recession dispel inflation fears (temporarily) and drive bond yields substantially lower?

The outlook for commodities is key, especially with the backdrop of the war in Ukraine. But I still see commodity prices plunging just like in Q4 2008, back then taking headline CPI inflation from +5% to -2% in just 12 months. Could we see sub-1% 10y yields once again? Now that would be one heck of a surprise.” – Albert Edwards

The Tale Of A Zombie Company

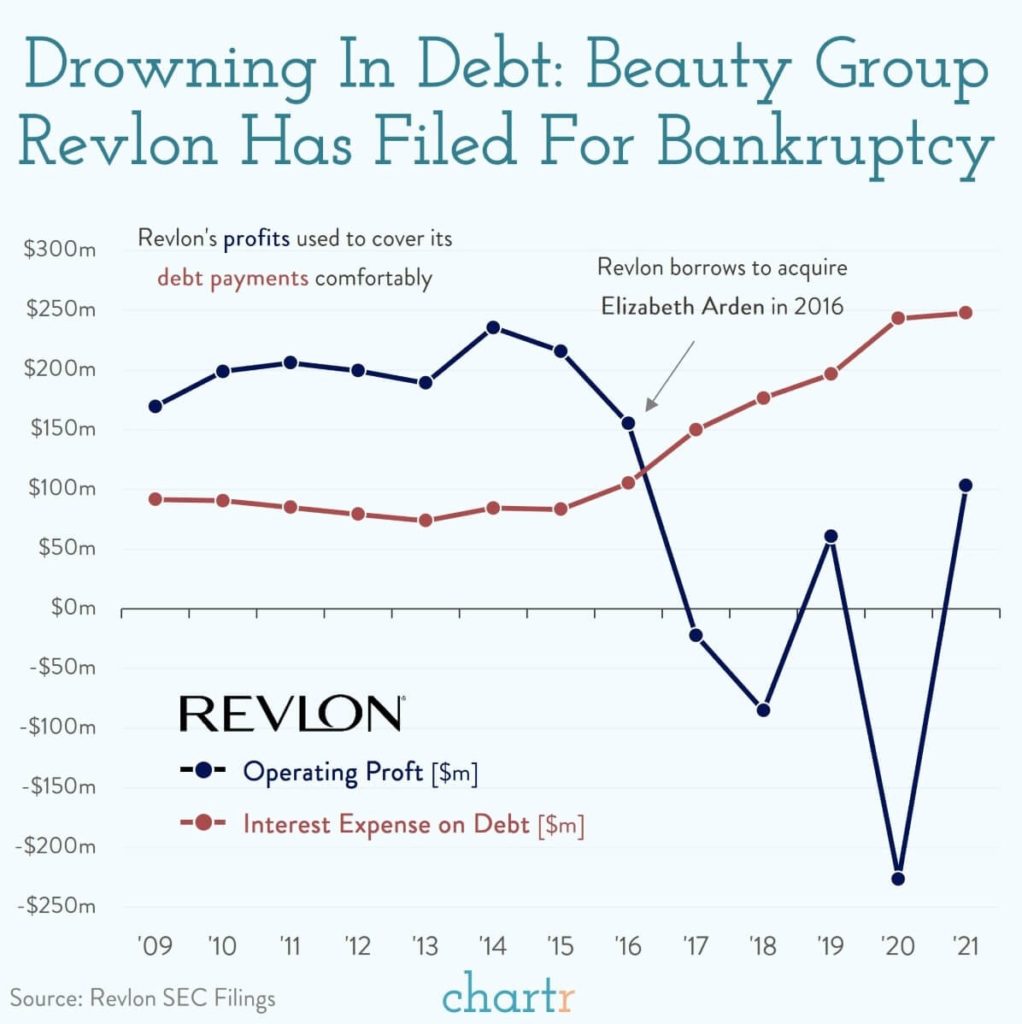

“Revlon, the beauty and cosmetics company first founded in 1932, has filed for bankruptcy. For years Revlon, which owns Elizabeth Arden and a number of fragrance lines (including Britney Spears and Christina Aguilera’s brands), has struggled with a growing debt pile. From 2009-2015, Revlon mostly had that debt under control, eking out enough of a margin to cover the annual interest expense every year.“

That last sentence is THE definition of a “zombie company.” Now back to the rest of the story.

“But then Revlon acquired Elizabeth Arden in a bid to buy its way to growth. That meant taking on more debt, at a time when competition in the beauty space was intensifying. Revlon started to struggle. Having been reliant on physical distribution in malls and shops for years, Revlon suddenly had to compete with upstart brands such as Fenty Beauty (by Rihanna) or Kylie Cosmetics (by Kylie Jenner).

These were digitally-native brands with huge followings that shipped straight to consumers, meaning cheaper marketing and distribution. Fenty Beauty has 12.9m followers across social media platforms Instagram and TikTok, Kylie Cosmetics has 28.9m.

Revlon has 3m.

As debt piled up Revlon shifted some assets into a new holding company, in an attempt to attract new lenders. That was fine except it wasn’t — Revlon’s long-time lenders sued, alleging that the company had breached their loan agreements. That’s complicated enough but it became comically complicated when Citibank — which was acting as a loan agent — accidentally paid off $900m of Revlon loans with its own money. Citi said, “oops sorry can we have that back”. Some of the counterparties said yes, but others weren’t so keen to forgive and forget, leaving Citi out of pocket for Revlon’s loans… and now Revlon is going bankrupt.” – Chartr

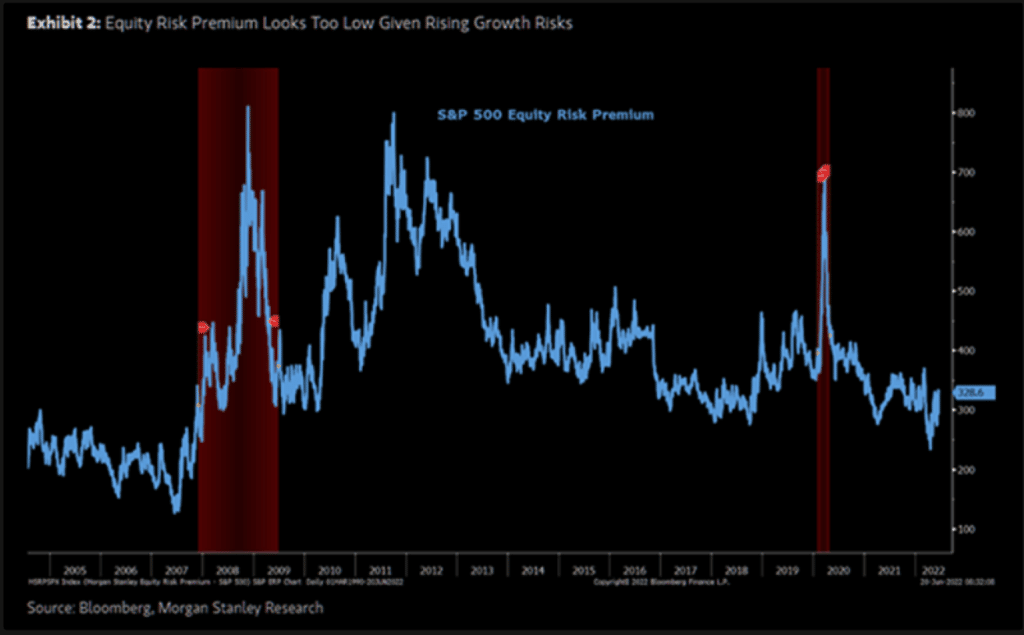

Equity Risk Premium Is Too Low To Suggest Recession Risks Are Over

“With Michael Wilson’s view for lower multiples and earnings now more consensus, the markets are more fairly priced. However, it does not price the risk of a recession, in his view, which is 15-20% lower, or roughly 3000. The Bear market will not be over until the recession arrives or the risk of one is extinguished. What do forward EPS contractions look like in the absence of a recession and during a recession?

Forward EPS contractions over 2% are fairly rare. During non-recessionary times, the median EPS contraction is about 5%. During recessions, EPS contractions ramp up to 14%. Such a decline would take the consensus of $239 today down to $206; putting a 14/15x trough multiple on this implies a price range of 2,900 to 3,100.” – The Market Ear

Powell’s Testimony

Here are some headlines from Powell’s testimony yesterday:

- “Powell: Fed Rate Hikes Won’t Bring Down Gas or Food Prices”

- “Powell Says US Economy Very Strong, Can Handle Tighter Policy”

- “POWELL: ONGOING HIKES APPROPRIATE, DECISIONS MEETING BY MEETING”

- “Powell Says Fed Strongly Committed To Returning Inflation To 2%”

- “Powell: Rate Rises Should Impact House Prices Fairly Quickly”

- “Powell: We Are Seeing a Slowing in Housing”

- “POWELL: OUR GOAL IS FOR A SOFT LANDING, GOING TO BE VERY CHALLENGING“

- “POWELL: CERTAINLY A POSSIBILITY OF RECESSION, NOT OUR INTENTION“

- “Fed’s Powell When Asked About A Rate Hike Of 100 Basis Points: I Will Never Take Anything Off The Table.”

Dudley Signals Doom

Bill Dudley, Former President of the New York Fed, said a recession is inevitable within the next 12-18 months in an opinion piece published yesterday. We summarize his thinking as follows: Price increases have clearly forced the Fed to shift focus to price stability, with employment taking a back seat for now. The last thing the Fed wants is to fail at controlling inflation. If inflation expectations become unanchored, the situation becomes a lot harder to fix.

He then contends that it will take time and considerable tightening for significant demand reduction and supply adjustment. When that time comes, the economy will downshift abruptly due to tight conditions, a damaged consumer, and fading tailwinds. Finally, Dudley refers to history. He claims the Fed has never tightened enough to push unemployment up by 0.5% or more without triggering a recession. However, this is exactly what the FOMC members forecast at their last meeting. Although, the Fed rhetoric is quickly morphing as Powell now admits that recession is a possibility. Dudley’s conclusion is clear:

“Much like Wile E. Coyote heading off a cliff, the US economy has plenty of momentum but rapidly disappearing support. Falling back to earth will not be a pleasant experience.”

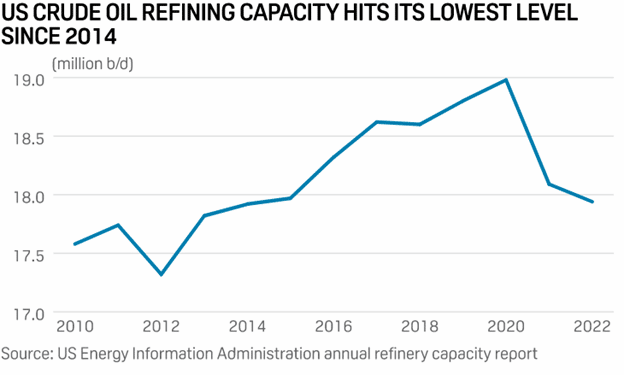

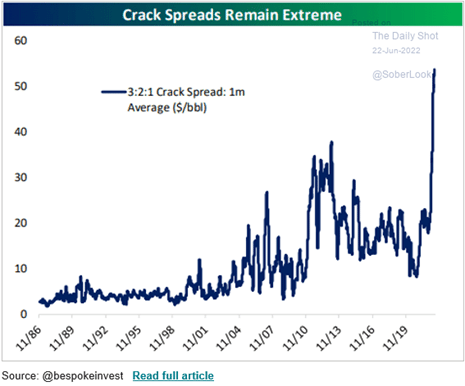

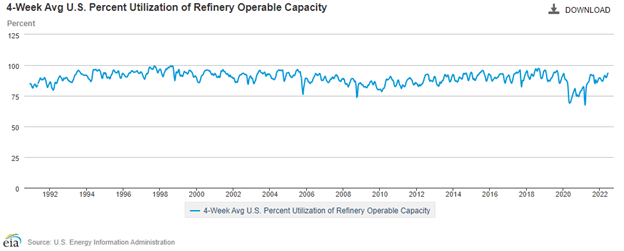

US Refining Capacity Dips Further

According to the federal government’s annual refinery capacity report, US capacity fell to the lowest level since 2014 at the beginning of this year.

“The dip comes amid refinery closures in recent years and the recent surge in oil prices as retail gasoline and diesel costs hit record highs earlier this year. The new pricing records are coming from a combination of factors, including demand recovery from the pandemic and the ongoing war in Ukraine.”

The crimped refining capacity and demand recovery have led to record crack spreads for refiners as shown below. The 2nd chart below illustrates that refiners have been increasing capacity utilization this year, and it’s approaching levels seen pre-pandemic.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.