“Pigs get slaughtered.” Such is the subject of a recent article by Jason Zweig of the WSJ. To wit:

“Until recent decades, villages in Spain celebrated el día de la matanza, the Day of the Pigs’ Slaughter, early each December with singing, dancing and recitations of poetry. Similar festivals were common elsewhere.

All this puts me in mind of an old Wall Street proverb: “Bulls make money, bears make money, but pigs get slaughtered.”

The importance of “pigs get slaughtered” gets lost during a surging bull market advance, It gets thrown around in the media enough that it becomes “the boy who cried wolf.” As the market continues to rise unabated, and well beyond what valuations and logic support, the “fear of missing out” becomes an insatiable feeding fest of “pigs at the trough.”

Of course, that is all fine until the day of the slaughter arrives.

Such brings forth a couple of questions:

- What causes investors to become pigs?

- What can you do to avoid it?

Irrational Exuberance

Jason jumps into the “Wayback Machine,” to revisit the last time the market entered into a phase of “irrational exuberance.”

A quarter-century, then-Federal Reserve Chairman Alan Greenspan introduced the phrase “irrational exuberance” into the popular investing lexicon. In a speech, he fretted that the stock market might have risen too far, too fast.

To quote Alan Greenspan at the time:

“How do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decades?”

Importantly, at the time, he noted that sustained low inflation tends to be good for stock prices. Also, the Fed would NOT worry about a “collapsing financial asset bubble” if it didn’t negatively impact the economy.

Over two decades later we can confirm two things.

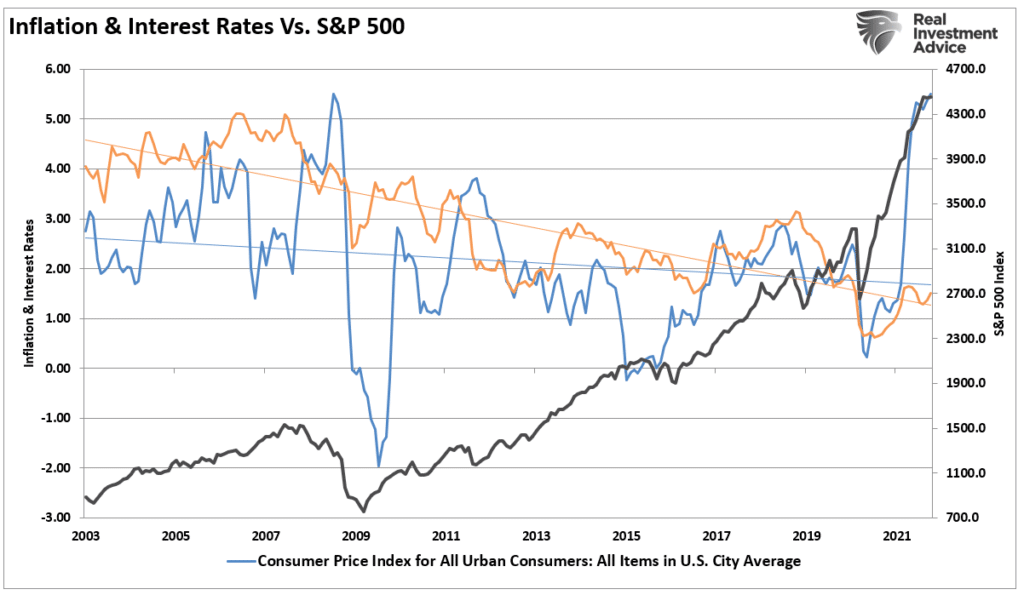

While falling inflation is good for stocks prices, both a surge or collapse in inflation is not. Furthermore, falling inflation is ONLY GOOD for stock prices when combined with an exorbitant amount of financial liquidity and artificially suppressed interest rates.

Secondly, the Fed is ALWAYS worried about a collapsing financial asset bubble. Such is why they repeatedly go to great lengths to avoid them, only after they cause them.

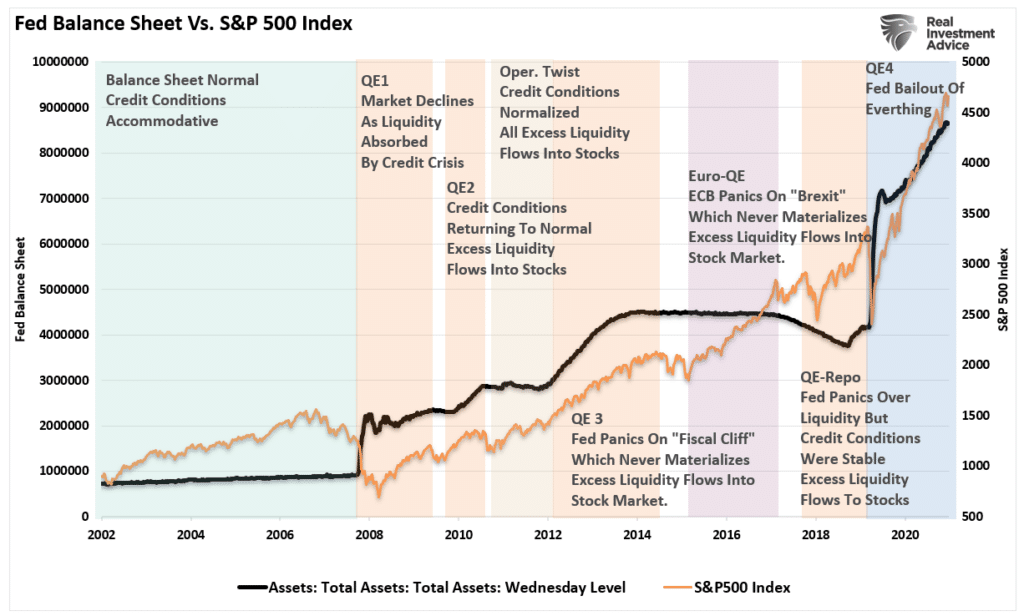

Clearly, after two decades of ongoing monetary interventions, investors have become “piggish” as the “trough” continues to get refilled. There seems to be “no risk” with continuing to gorge on assets, and investors have grown “fat” with confidence.

But why not? As Jason concludes:

So “how do we know when irrational exuberance has unduly escalated asset values”?

As I’ve written, spotting a market bubble seems easy and obvious. With hindsight, we know. With foresight, we can only guess.

It’s hard to imagine a less satisfying answer. And impossible to have a more accurate one.

Thankfully, you don’t need an accurate answer.

Be A Bull Or A Bear

Such brings us to our second question. How can we avoid becoming a “pig getting led to slaughter?”

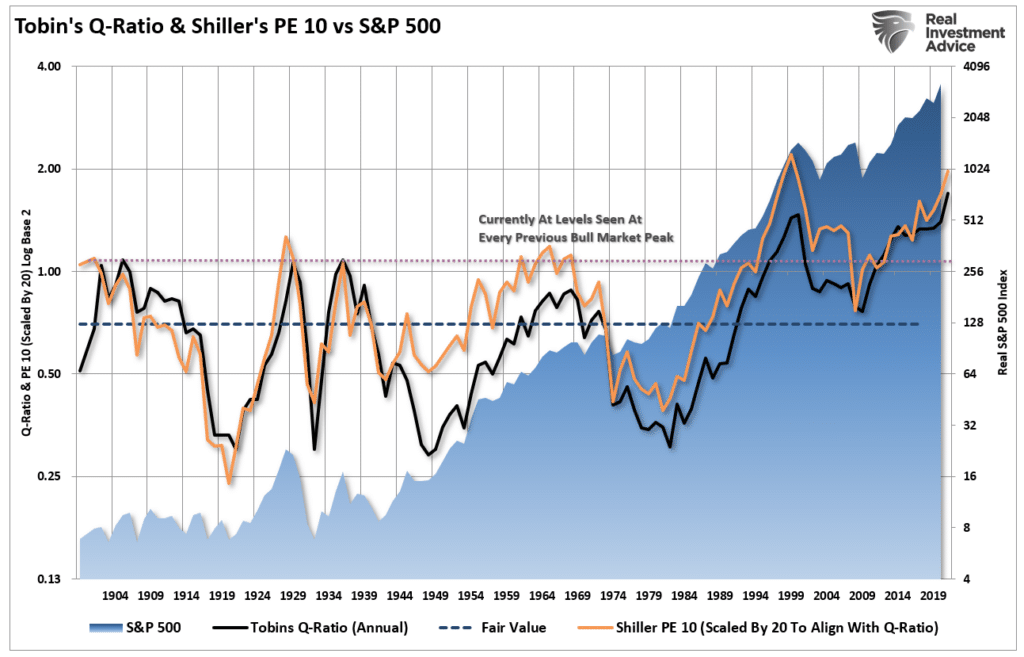

It doesn’t take a lot of work to realize the financial markets have gotten overvalued by virtually every meaningful measure. From price to earnings at nearly 40x CAPE, price to sales above 3x, and market-capitalization to GDP at more than 2.5x. Even the more obscure Tobins-Q ratio, which measures the cost of replacement, is suggesting more extreme over-valuation.

Such doesn’t mean you should sell everything and go to cash. Not at all.

In the short term, all that matters is price. As discussed in “Pet Rocks & Other Signs:”

Valuations are a terrible market timing indicator. However, in the short term valuations tell you everything about market psychology. In the long term, they tell you everything about expected returns.

Currently, every measure of valuation suggests investors have thrown all “caution to the wind.”

Looking at the chart, it indeed suggests that investors should be selling everything immediately. However, given this is annual data, the turns can take much longer than expected.

It is the “lag” that leads investors in the short-term to believe that “valuations” no longer matter. That belief leads investors to continue to gorge on risk assets assuming “this time is different.”

However, such is a dangerous assumption and one that repeatedly led “pigs to the slaughter.”

What individuals choose to forget is that being bullish in a rising market, or bearish in a declining market, does not mean throwing caution to the wind. As discussed in “An Investors Guide To Trading”, every successful investor in history has a basic set of rules to navigate the markets.

- Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

There is a reason why all great investors have these same rules in one form or another. They all learned from experience that markets will slaughter you when you least expect it.

It’s Dangerous To Be A Pig

Brett Arends wrote a great piece in 2010, entitled “The Market Timing Myth.” in which he focused on managing risk. To wit:

For years, the investment industry has tried to scare clients into staying fully invested in the stock market at all times, no matter how high stocks go or what’s going on in the economy. “You can’t time the market,’ they warn. ‘Studies show that market timing doesn’t work.‘

There’s just one problem. It’s hooey.

They’re leaving out more than half the story.

And what they’re not telling you makes a real difference to whether you should invest, when and how.”

The part the financial media leaves out, as always, is the second-half of every bull market which investors capital. As Brett concludes:

Can’t time the market? It was clear as a bell that investors should have gotten out of stocks in 1929, in the mid-1960s, and 10 years ago. Anyone who followed the numbers would have avoided the disaster of the 1929 crash, the 1970s or the past lost decade on Wall Street. Why didn’t more people do so? Doubtless, they all had their reasons. But I wonder how many stayed fully invested because their brokers told them ‘You can’t time the market.

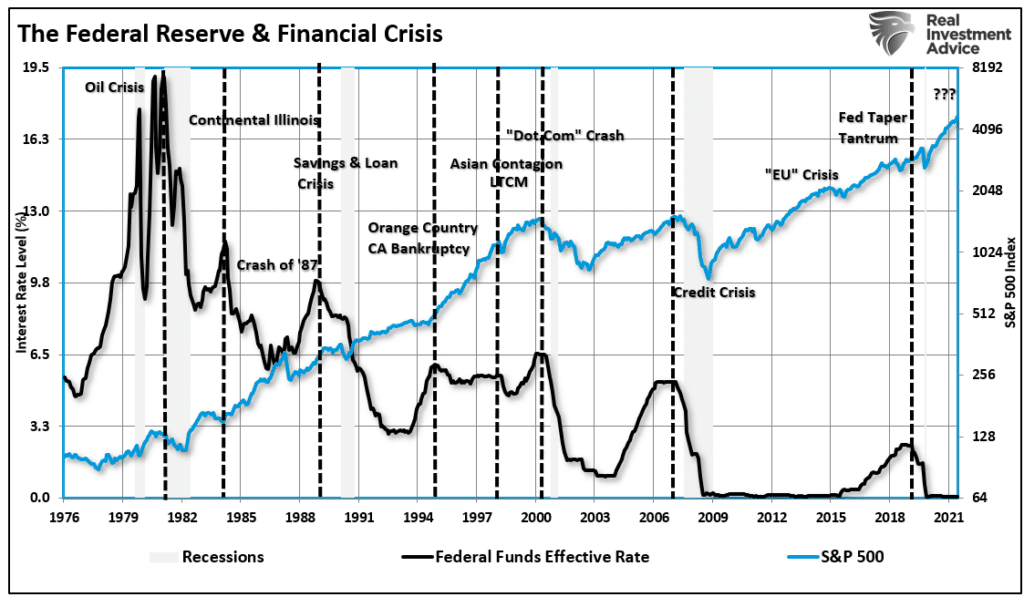

As Jason noted above, bubbles are indeed easy to spot in hindsight. But, for investors, it is not impossible to navigate “bubbling markets.”

Currently, there are numerous indicators we are in the second major market bubble of this century from record IPO and SPAC issuance of faulty companies, to record levels of leverage and speculative behaviors. However, such doesn’t mean the “bubble” will burst tomorrow. Therefore, for now, we must continue to participate in the bull market. But, critically, such does not mean we have to take excessive levels of reckless risk to do so.

Sure, we may not capture 100% of the upside. However, one day in the not-so-distant future, the Fed will hike rates one too many times. When that occurs, the deflation of the bubble will happen quickly. For those that have hedged risk, reduced speculative investments, and controlled exposures, they won’t be one of the pigs getting slaughtered.

How do we know? Because history tells us so.

Yes, as Gordon Gecko once quipped in Wall Street: “Greed is good.”

But that didn’t work out well for him either.

My favorite modern version of the saying comes from the financier André Kostolany: “I can’t tell you how to get rich quickly. I can only tell you how to get poor quickly: by trying to get rich quickly.”

It can pay to be a bull, and it can pay to be a bear. But it’s always dangerous to be a pig.- Jason Zweig