Thursday’s Daily Commentary led with the story of the Bank of England’s (BOE) temporary purchases of British bonds (Gilts) to stem sharply rising rates. It turns out the root cause for the emergency action was not higher rates but irresponsible pension funds. Large U.K. pension funds were buying Gilts and likely U.S. Treasury bonds with leverage. Leverage requires the borrower maintains ample collateral to ensure repayment of the loan. As the price of Gilts fell, lenders required the pension funds to post more collateral. The speed and severity of the drop in Gilt prices forced pension funds to sell bonds in illiquid market conditions to raise money. These actions made yields rise further, making a bad problem worse. The situation also helps explain why U.S. Treasury bonds got slaughtered on Monday. In hindsight, it was likely U.K .pension funds selling U.S. bonds to meet margin calls.

The BOJ currency intervention a week ago and the BOE move Wednesday are important signals that financial instability is rising. The question facing U.S. stock investors is, will the Fed acknowledge instability with words and or actions? The graphic below, discussing how dire the situation was, is courtesy of the Financial Times.

What To Watch Today

Economy

- 8:30 a.m. ET: Personal Income, month-over-month, August (0.3% expected, 0.2% prior)

- 8:30 a.m. ET: Personal Spending, month-over-month, August (0.2% expected, 0.1% prior)

- 8:30 a.m. ET: Real Personal Spending, month-over-month, August (0.1% expected, 0.2% prior)

- 8:30 a.m. ET: PCE Deflator, month-over-month, August (0.1% expected, -0.1% prior)

- 8:30 a.m. ET: PCE Deflator, year-over-year, August (6.0% expected, 6.3% prior)

- 8:30 a.m. ET: PCE Core Deflator, month-over-month, August (0.5% expected, 0.1% prior)

- 8:30 a.m. ET: PCE Core Deflator, year-over-year, August (4.7% expected, 4.6% prior)

- 9:45 a.m. ET: MNI Chicago PMI, September (51.8 expected, 52.2 prior)

- 10:00 a.m. ET: University of Michigan Consumer Sentiment, September final (59.5 expected, 59.5 prior)

Earnings

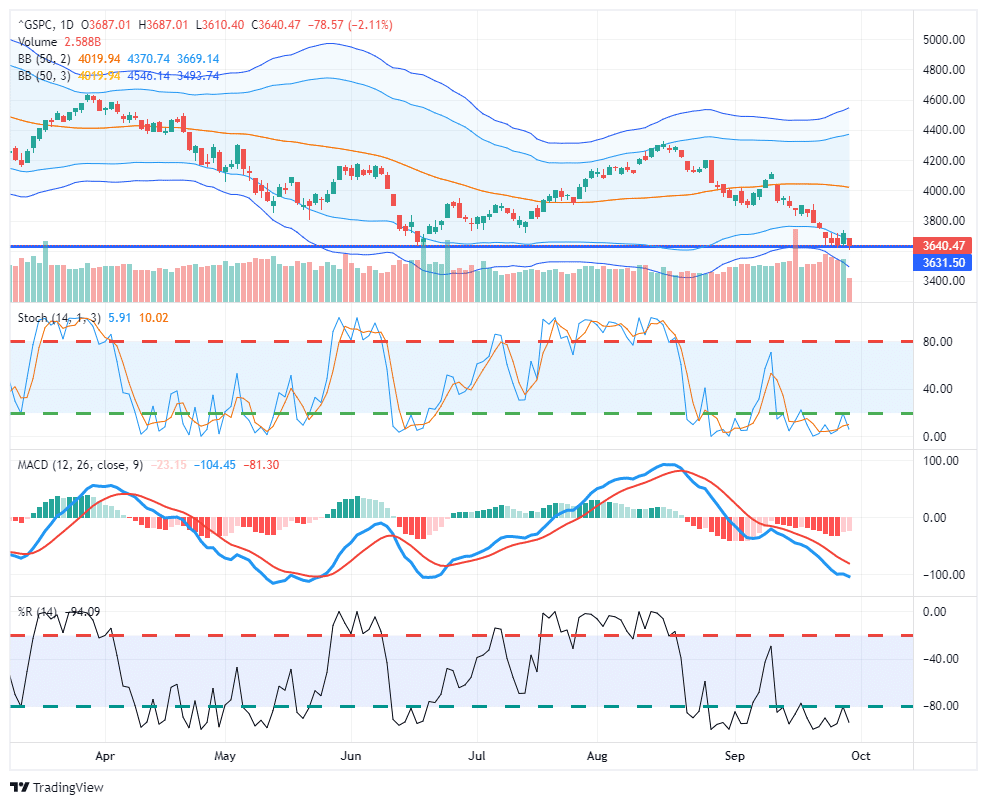

Market Trading Update

Another day of disappointment for the markets. After a sharp rally yesterday on the back of BOE market interventions, the market reversed course yesterday, once again testing the June lows. For the week, despite a wild ride, the market remains mostly unchanged heading into today’s trading. Part of the reason for yesterday’s volatility likely rests on quarter-end portfolio rebalancing. With the market extremely oversold on multiple levels, as noted in Tuesday’s blog, “The Big Short Squeeze,” a reflexive rally is likely. I would expect better price action as we enter the month of October, which historically tends to denote the end of bearish market action, at least in the short term. We look to use that rally to raise additional cash levels in portfolios for now.

The Big Short Bounce

The Bloomberg graph below strongly argues that stock prices may bounce soon. Essentially it shows that speculators are making a record number of short bets against the S&P 500. The short bets have been profitable over the last few weeks, but they will have to buy back their shorts at some point. Either they are happy with their fans and cover, or the market starts rising, forcing them to buy. Short covering rallies can be powerful when the market is as short as it is today.

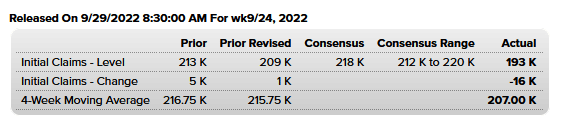

To the Fed’s Dismay, Jobless Claims Fall Again

Jobless Claims fell last week to 193k. Jobless Claims have been falling steadily over the previous two months. Since 1967 there have been 2908 weekly jobless claims reports. Over that period, there have only been 68 other times jobless claims were below yesterday’s figure.

While this appears to be great news, the Fed may think otherwise. The Fed is concerned that tightness in the labor market contributes to higher inflation. They have openly stated they would like to see joblessness rise. The latest data argues the Fed may need to remain very hawkish in the coming months to ease the labor shortage and ultimately tame inflation.

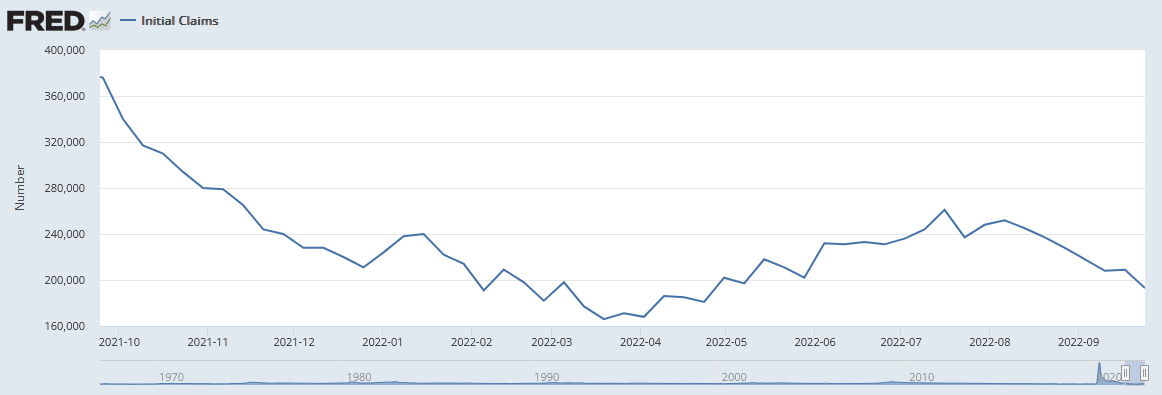

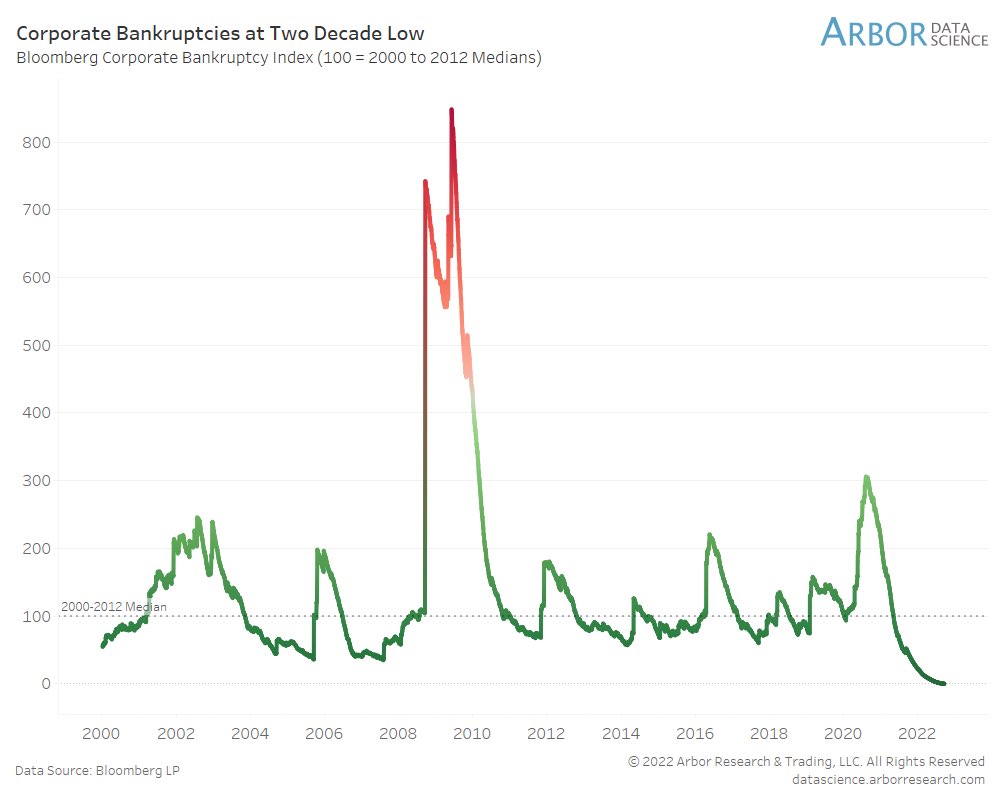

Are Zero Corporate Defaults Sustainable

The corporate bond market trades at low yield premiums to risk-free U.S. Treasury bonds despite the recent economic and financial turmoil. The first graph shows that the yield difference between investment grade corporate bonds and Treasury bonds has risen recently but remains in the lower end of the range of the last 25 years. The second graph below helps explain why. As it shows, corporate bankruptcies have been non-existent over the last year. The problem with expecting that to continue is the economy; therefore, defaults are cyclical. As you can see, the number of bankruptcies troughs and peaks every four years or so. Simply, corporate defaults will increase over the coming few years.

The economy is weakening, and corporate profits, or their ability to make good on the debt, are likely to struggle as the economy weakens. As investors, we must ask if the additional yield we get for buying a corporate bond fully incorporates the risk of default.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.