Investment management can be silly, just like the title of this article. When researching potential investments, we often must choose between math and facts versus irrational human behavior. For instance, the rise of passive investment strategies has many investors favoring “value” stocks not on valuations or earnings trends but on self-serving Wall Street classifications. As a result, larger companies that meet vague categorizations attract more passive strategy dollars. This makes them even more prominent and further inflates their valuations.

For investors willing to do some work, this circular pattern leaves excellent value stocks in the wake of the behemoth passive value investment liner.

Benjamin Graham

In the words of value investing legend Benjamin Graham-

“The true investor will do better if he forgets about the stock market and pays attention to his dividend returns and to the operating results of his companies.”

As Graham states, value investing is not a popularity contest. It involves picking stocks that trade at cheap valuations and pay dividends. Despite his wisdom, value investing has morphed into buying the largest companies simply because they are labeled “value” by the banks and brokers that are heavily incentivized to grow their asset base on which they earn fees.

To help appreciate the warped investment world, we present two stocks.

Blind Taste Test

To appreciate what is truly value and what is considered value, we give you a blind investment scenario. Please choose between stock A and stock B.

Stock A is significantly more expensive than B using popular traditional valuation metrics. Stock B is growing its sales and revenues much faster than A. In fact, sales at A have declined slightly over the last ten years.

Before deciding, think about the question in another light. If you were investing in a private business, which would you choose?

We venture to guess that nearly 100% of our readers armed with that limited information would opt for stock B.

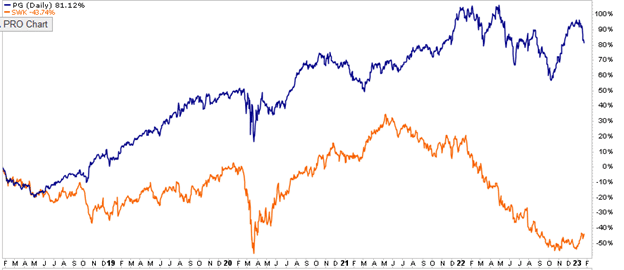

We provide one more piece of data. Stock A has a market cap of nearly $350 billion, 27 times that of stock B. Does that sway your decision?

Sadly, that makes all the difference for unknowing passive investors.

Analyzing A and B

Stock A is Proctor & Gamble (PG). The consumer staples company was founded in Cincinnati, Ohio, nearly 200 years ago. PG sells a wide range of well-known consumer products globally. Their top products include Tide, Pampers, Bounty, Gillette, Crest, and a slew of other brands you are likely familiar with.

Stock B is Stanley Black & Decker. The household and industrial tool company was founded in Connecticut and is nearly as old as PG. Like P&G, some of their products are well-known by households globally. They also make industrial tools that may be less familiar. Some of their most popular product lines include DEWALT, Black and Decker, Craftsman, and Cub Cadet.

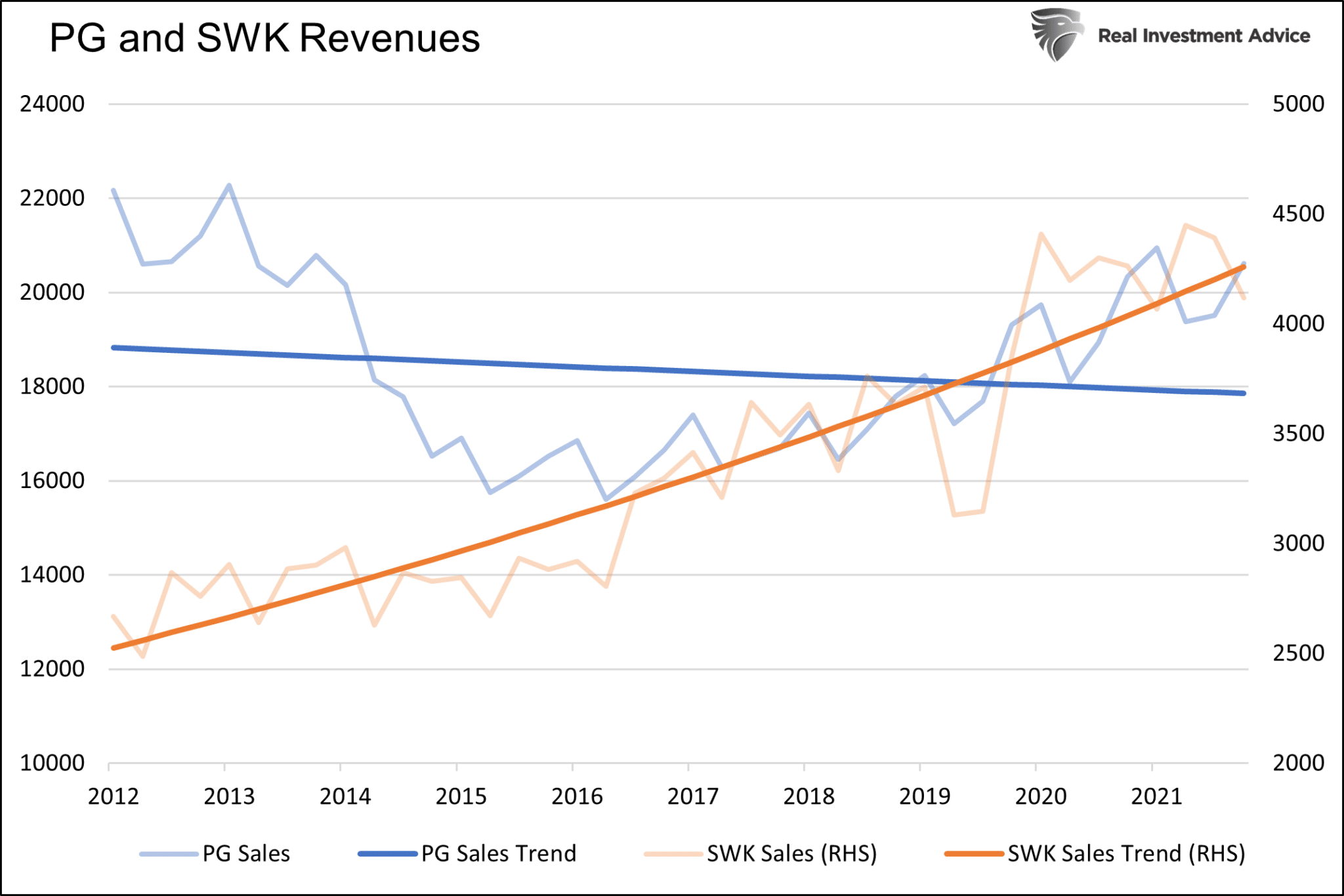

Before comparing valuations, it’s worth evaluating their revenue and earnings growth over the past ten years. The trend lines help smooth out quarterly gyrations and highlight prevailing trends.

Revenues at SWK have risen 5.4% annually over the last ten years. The growth has been remarkably predictable. On the other hand, PG experienced a -0.53% annualized decline in revenue over the period. Since 2015 it began trending higher at a 3% annualized rate, still moderately below SWK’s growth rate.

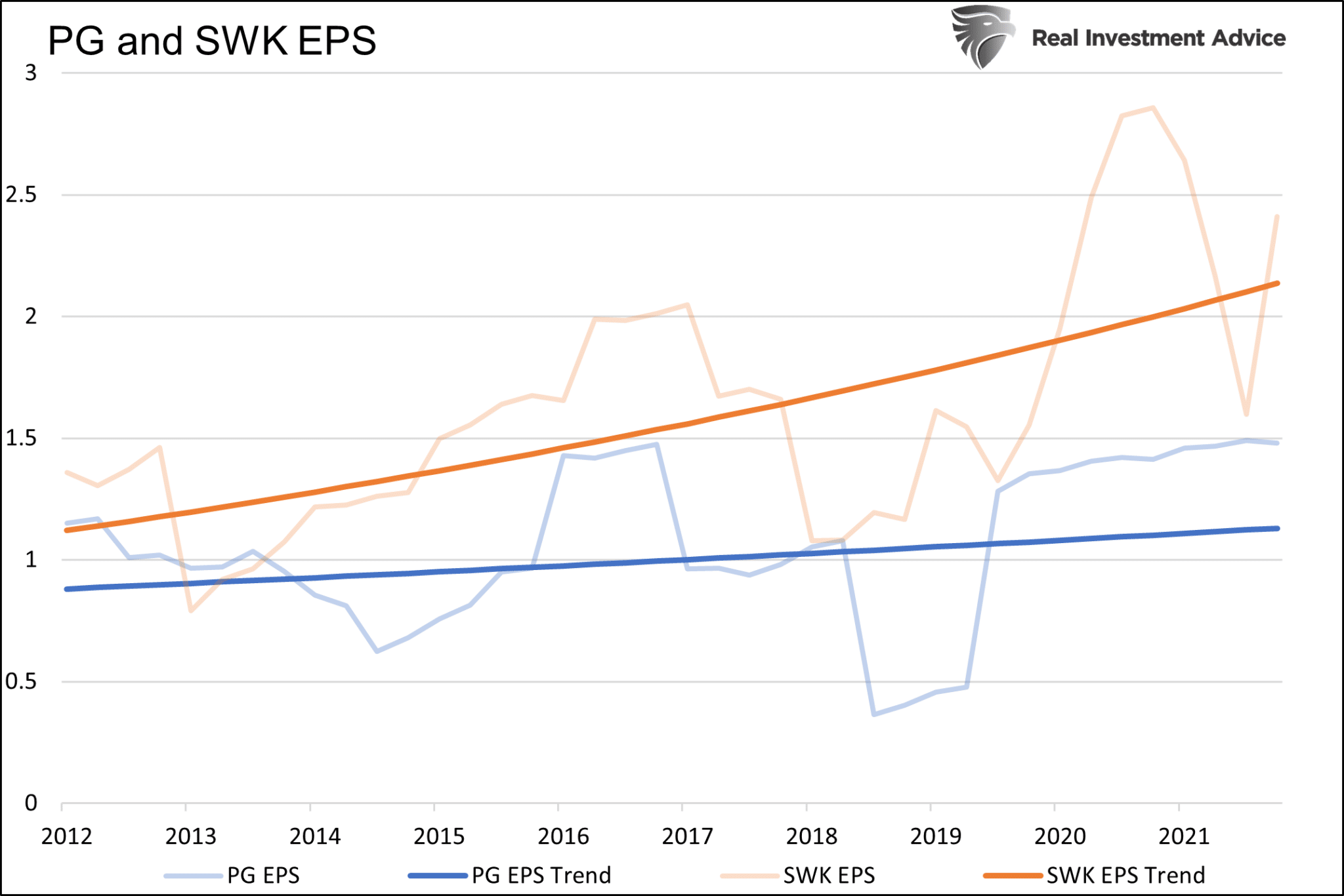

Evaluating earnings per share (EPS) tells a similar story. P&G has increased its EPS by 2.5% annually. Such compares poorly to SWK’s 6.7% annualized growth rate.

More telling, PG has repurchased almost 15% of its shares over the ten years. SWK has only repurchased 4% of its shares. PG’s EPS over the period would be close to flat without buybacks.

PG vs. SWK Valuations

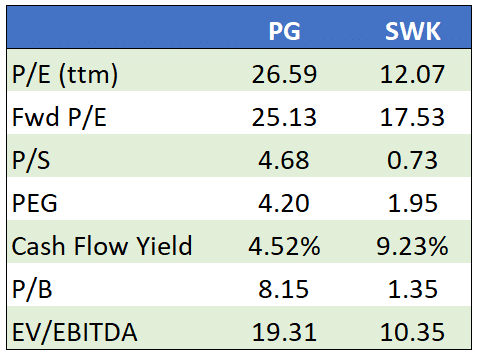

Revenue and EPS growth are important metrics, but they do not tell whether the stock price represents value. To take the next step, it is vital to compare fundamental valuations, or how much it costs investors to buy a stream of future sales and earnings. The table below shows seven popular valuation methods. In all cases, SWK is hands down significantly cheaper.

Value Funds

Based on our analysis, a value fund should greatly prefer SWK over PG. Further, consider that many of PG’s ratios are more expensive than the S&P 500. However, what a value fund should desire and what they own are often two different things.

Vanguard’s Value Index Fund ETF (VTV) has a market cap of 66 billion. It owns over 2% of PG and only 0.07% of SWK.

The well-followed iShares S&P 500 Value ETF (IVE) has a market cap of 21 billion. The fund holds 0.96% of PG and only 0.08% of SWK.

The story is the same for dividend-centric funds. SWK has a 3.73% dividend yield, about 1.25% more than PG. Despite the larger dividend, two of the more popular dividend ETFs, VYM and VIG, allocate 2.5% and 3.00% to PG, respectively. VYM does not hold SWK, and VIG only holds 0.09% of its assets in SWK.

For passive value funds to grow, they need securities with ample shares that can be bought without grossly affecting the price. The ETF and mutual fund business models financially reward the fund manager for the fund size, not how well they live up to their stated objective. To grow, many value funds stretch the meaning of “value” to increase the universe of acceptable stocks. Often broader definitions of value result in stocks like PG, which may be stable and conservative companies but do not trade at value-like valuations.

Summary

Any rational investor staring at valuations and fundamentals would likely choose SWK over PG. Any rational investor gauging where investor dollars flow would choose PG over SWK.

And that is the crazy environment we find ourselves. If passive strategies continue to dominate, stocks like PG may continue to outperform stocks like SWK, despite valuations and earnings and revenue growth. However, stocks like SWK offer an increasingly greater value proposition as the trend continues.

In an unstable market, as we may be approaching, SWK and other true value stocks may provide a port in the storm, leaving PG and others vulnerable to selling if the passive investment crowd has a change of heart.