Outliers can change our lives.

The pesky outposts of statistical warriors are situated at the far reaches of normality. When they breach boundaries, lives change, sometimes forever. In Part 2, I examine the investment and portfolio outliers that can make the difference between retiring or working indefinitely (not that work during retirement is such a bad thing. I’m talking about working INSTEAD of moving on to the next iteration of YOU).

We want to be told stories, and there’s nothing wrong with that – except that we should check more thoroughly whether the story provides consequential distortions of reality. Could it be that fiction reveals truth while nonfiction is a harbor for the liar?

Nassim Taleb, The Black Swan.

Yes, the outliers. Consider them unwanted houseguests, the nascent Fredo Corleones of the statistical world. Their impacts are minimized by the academics, social scientists, and Wall Street ‘know-it-all’ pundits who believe most American households have recovered from the Great Recession.

Outliers and most everything else in the investment world are ‘storied’ away. People often ask me how I can help people invest and yet write screenplays? Well, stocks are stories. Investments are stories. Do you think Robinhood traders put their money at risk using homework,, or do they scan the Reddit boards for the juiciest gambits?

Outliers just don’t get any respect but they demand it! In the face of household financial fragility, we all must think differently about risk mitigation, break away from the financial tenets designed to keep us enslaved in debt, and understand that on occasion, Fredo Corleone could possibly get us killed! (figuratively of course). Except in Michael Corleone’s case, it was literal… And close!

Watch for Black Swans!

Taleb touts ‘Black Swans’ as events outside the lines of normal expectations. Nothing in the past, especially the recent history, points to their emergence. Yet, when these pesky statistical nightmares decide to take over from the standard or bell curve of normal-probability territory, all hell breaks loose.

Although outliers are rare, they propel with enough flame and brimstone to turn our finances and, in some cases our lives, into cinders.

I spent the Texas winter apocalypse re-reading Taleb’s classic work by the warm white light of a fully-charged Kindle. For those who haven’t picked it up, The Black Swan: Second Edition: The Impact of the Highly Improbable: With a new section on robustness and fragility by Nassim Taleb, the paperback edition is worth every bit of $12 bucks. What you’ll learn about our illusion of understanding (especially in a world littered with social media) is worth ten times the book’s price.

You see, society (social media participants, especially) suffers from an incredible illusory gift. An electronic form of cerebral foreplay where most believe the world is understandable and more predictable than it is. In other words, users consider their opinions as gospel; they also overvalue factual information yet hold little regard for the ‘gray’ that clouds every fact.

I usually re-read my highlighted version of The Black Swan later in the year. This time, it kept me warm (my brain cells anyway) during one of the coldest Februarys on record for Texas. Re-reading Taleb keeps me grounded and humbled by uncommon events that seemingly occur every decade.

Most pundits discount the ongoing damage of outliers.

The pundits still stomp their feet and jump Evel Knievel canyon-leaps of defiance. They continue to tell us that outliers occur every 100, 1,000, 5,000 years (pick a number). Why people listen to these jokers is beyond me. The masses hope they’re correct. That way, we never need to prepare because there’s ZERO excitement in preparation. It’s too long term, too nebulous, takes too much discipline. Blah, blah, blah.

So, with that, I share with readers the outliers, the frontier fighters you most likely believe never will breach your main personal, financial boundaries until they do.

Here are the next two outlier statements that can change your life:

I need to save as much in taxes TODAY!

It’s all about deferring taxes until the tomorrow of retirement when supposedly, tax liabilities will fall. But will they? Probably not. Unfortunately, this is outdated advice still provided by the mainstream financial services industry.

At RIA, we believe growing household tax burdens will be a concern. The taxation of Social Security will not spare retirees from higher taxes. Due to the lingering effects of COVID, Medicare IRMAA charges will affect a larger population of lower-income Medicare recipients.

Either way, with massive fiscal stimulus imminent, taxes are inevitably headed higher for the majority. Therefore, a ‘save taxes today mentality’ will only lead to higher taxes later on in retirement when you can least afford to pay them.

Tax deferral benefits have lost some firepower.

The tax-deferred snowball story touted throughout the 80s, and early 1990s made sense as ten-year annualized returns on the S&P 500 ranged consistently between 10 to 15%. What a snowball, right? From the mid-90s to today, returns on the large company index have been half or less than half what investors previously realized.

Suppose we’re correct at RIA about forward-looking nominal stock returns closer to 3%. In that case, the attractiveness of socking every dollar away in tax-deferred accounts based on the compounding story is as small as a snowball in Texas (until recently).

The blanket, irresponsible statement about how household incomes will drop to the lowest tax bracket in retirement is stubbornly alive and well. Please don’t fall for it.

Consider the diversification of accounts!

Maintaining pre-tax, after-tax, and tax-free accounts allows for greater lifetime tax control. It’s imperative throughout the retirement income distribution phase.

At RIA, we teach the importance of diversification of accounts. This way, retirees can maintain greater distribution flexibility and control over tax liabilities.

Recently, a client required $50,000 to pay off the mortgage on his primary residence. Thanks to account diversification, we withdrew $20,000 from his pre-tax rollover IRA, $10,000 from his Roth conversion IRA and the remainder from his after-tax brokerage account. This strategy helped reduce taxes he would have incurred if the entire $50,000 needed to be distributed solely from his pre-tax account.

Now is the time to give more respect for Roth IRAs, 401(ks), and conversions. We’ve been on the Roth bandwagon for close to four years. Currently, I’m hearing more mainstream financial pundits touting the benefits of Roth. As usual, they’re late with the message.

Consider tax-deferred accounts such as traditional IRAs and company retirement plans as the fatted calves. Government officials salivate just thinking of their slaughter.

I am a firm believer that fiscal stimulus has just begun. In the future, it’ll be ‘sneakier.’ The pandemic has encouraged lawmakers to realize how current social safety nets don’t provide adequate protection therefore, I expect to see bolstering of unemployment benefits and possibly the emergence of new safety nets such as universal basic income and universal child and eldercare.

Taxes are headed higher. It’s inevitable. Thus, less popular investing and saving methods, whether Roth or cash-value life insurance, will continue to grow in popularity.

Don’t be left out by the fairytale story of tax-deferral. You may not like the ending.

The stock market always rebounds.

Markets move in cycles. As much as the Fed and their cheap money antics seek to ameliorate market cycles, the demand for stocks will eventually shift. Headwinds for returns will occur. The bears will roar awake from hibernation, and with teeth exposed, investors will understand how it’s ‘not different this time.’

Retirees must think differently.

Young accumulators of stocks with maximum earnings years ahead can weather a bear attack (although still not pleasant). Seemingly, older Americans who require their investment assets to deliver a predictable paycheck shoulder the risk of bleeding (financially) to death even in the face of seemingly minor money wounds.

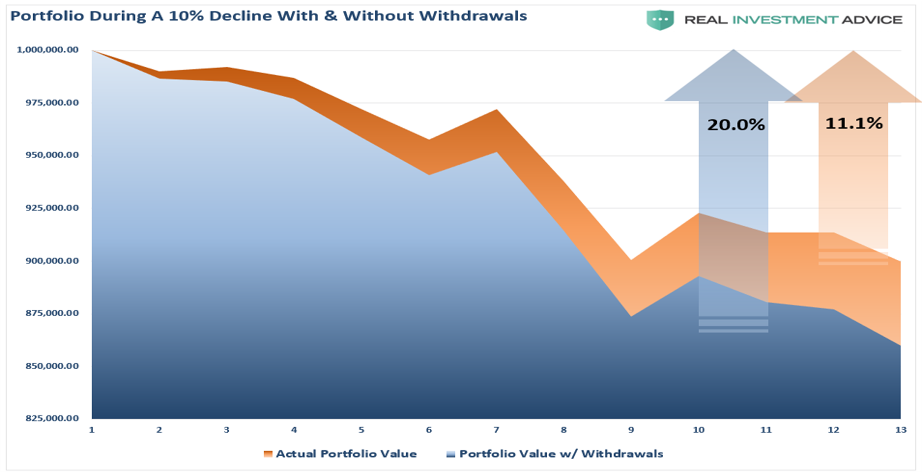

In other words, a distribution mindset must differ from an accumulation one. Even a 10% correction could be detrimental for retirees who depend on their investment portfolios to provide a predictable income rate. See Lance’s chart below. When taxes, fees, and withdrawal rates get considered, even a garden-variety correction turns into a lifestyle-changing episode!

Since 2018, our financial planning group (5 Certified Financial Planners® on staff) has been onboard with estimated lower future returns for every asset class. We adjusted our planning software accordingly as we believe investors are in for a long-term headwind for portfolio returns.

Thus, retirees in distribution mode must think creatively in the face of lower portfolio returns for longer. The steps to consider from year-to-year include: – A temporary reduction in the annual portfolio withdrawal rate, working a part-time job to maintain a retirement lifestyle, living smaller by downsizing, and tapping alternate sources for income, including reverse mortgages or cash value insurance policies.

Expect anemic long-term market returns.

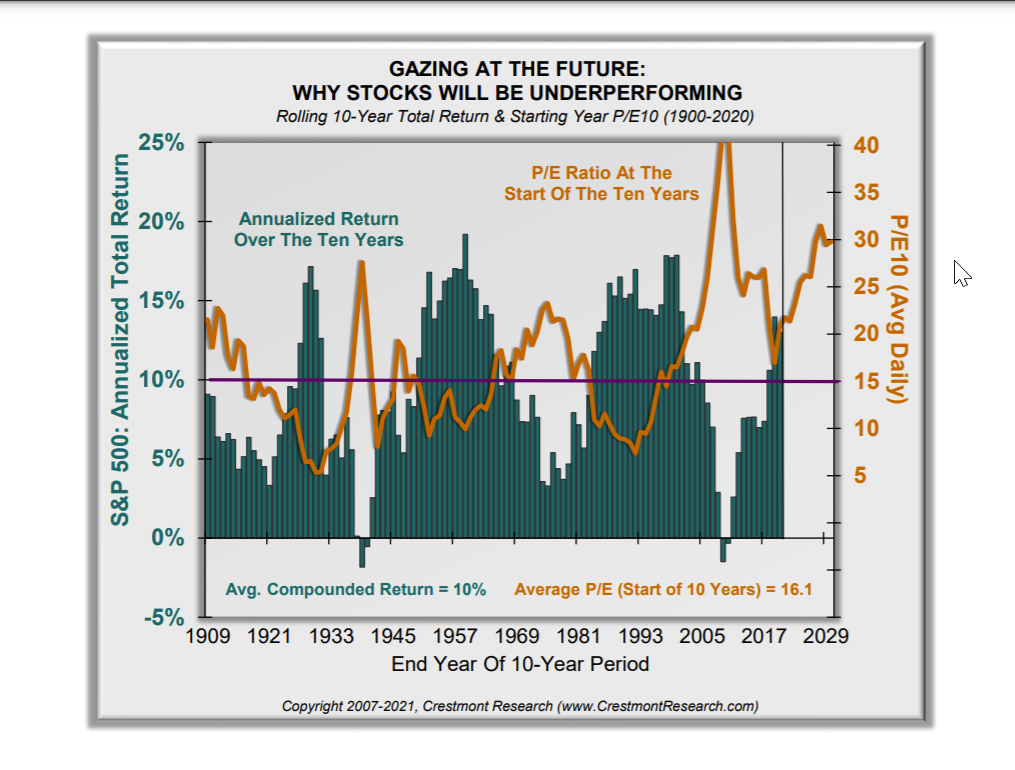

I always look forward to the multiple series of the Crestmont Research year-end analysis. Crestmont steers away from short-term cyclical market moves based on sentiment and momentum. Their research focuses on long-term or secular market cycles. In other words, they’re focused on decades, not days.

As a reminder, valuations are a lousy predictor of short-term returns. Eventually, however, valuations matter. Retirees with distribution portfolios must be acutely aware of valuations and their inevitable effect on their retirement lifestyles. Nosebleed stock values portend to lower future returns. Although frustrating to investment accumulators, investment distributors feel the adverse effects most of all.

Gazing at the future.

Using Crestmont’s rolling 10-year market returns (as represented by the S&P 500), along with P/E 10, a dismal outlook of future returns emerges. As we at RIA also believe lower returns for variable assets are inevitable, in 2018, we made a team decision to adjust lower every forward-looking asset class return for the foreseeable future.

The job of our financial planners is to provide practical information to our clients. Using 8-10% annual rates of return for plan inputs is downright ignorant and, in most cases, highly irresponsible.

As the Crestmont research showcases, the starting P/E is the most significant driver of future long-term returns.

“The chart helps investors to understand the expected level of return for the next ten years. Investors should avoid the temptation to extrapolate the past year or decade into the longer-term horizon. It will never be more true that past performance is not an indicator of future results.” – Advisor Perspectives.

Outliers aren’t pleasant.

Outliers aren’t fun. Take it from the people in Texas. Outliers don’t get much respect until their upon us. Shining a light into the dark corners of extreme probabilities can be the difference between survival and disaster.

Do you know how to expose outliers? Showcase them front and center through holistic financial planning. A comprehensive financial plan outlines the risks one can absorb and risks to mitigate.