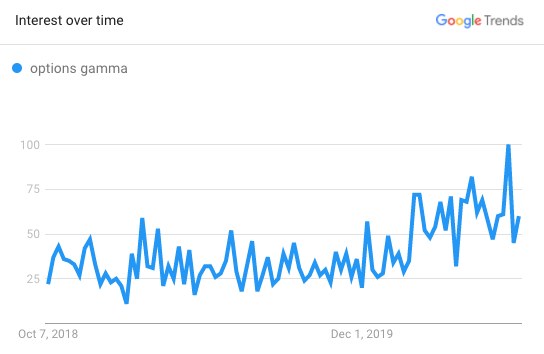

Options risk in the stock market? Over the past two years there has been a growing interest in “options gamma” in the markets. As shown below, Google trends show a surge in interest, spiking around the March 2020 sell-off.

Source: Google Trends

Option gamma is a concept that many find difficult to understand. For the purposes of this article, let’s put it in simple terms. “Gamma” means “options market risk.”

Gamma is risk, and risk moves markets.

There is ample evidence that high gamma and high volatility go together. One example is the crude oil market in 2018. In an article entitled Two Words That Sent The Oil Market Plunging: Negative Gamma, Alex Longley writes:

As oil suffered its biggest one-day slump in three years, it wasn’t OPEC or President Donald Trump that was shaking the market. Instead, trading desks were abuzz with chatter of “negative gamma.”

Late 2018 also saw large moves in the natural gas markets. Again, gamma played a significant role. The demise of optionsellers.com added fuel to the natural gas volatility fire as natural gas rose spectacularly on short-covering orders. It fell right back when the gamma quake ended.

There is consensus that options risk can move markets in big and small ways. Gamma can create a tidal wave, or it can also create smaller waves and strong temporary currents.

Options Risk in Equity Markets

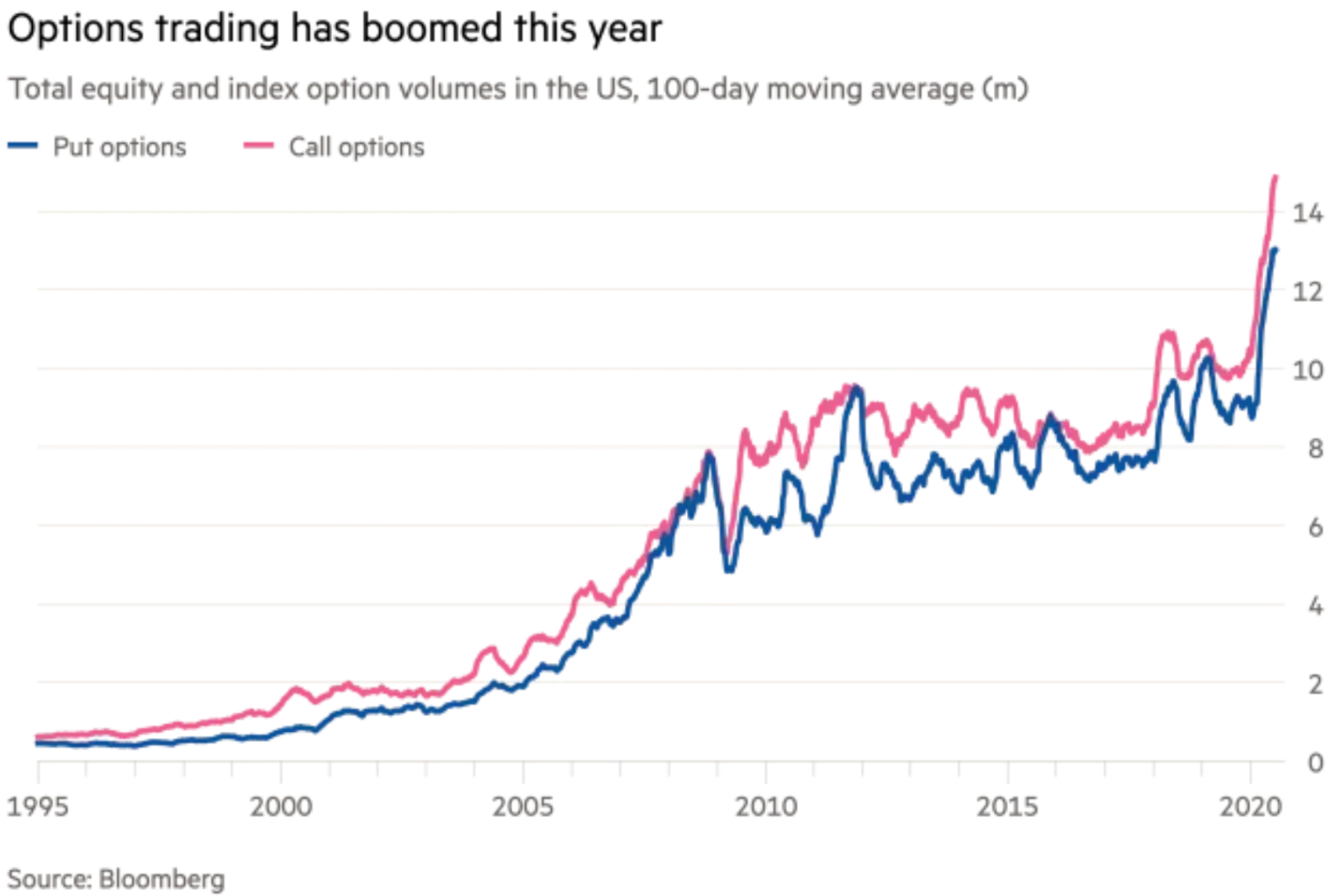

An increase in options activity leads to increased risk in the market, and options activity has increased significantly in 2020, as shown below.

Earlier this year, we embarked on a comprehensive study of options trading in the SPX since 1992. We have discovered patterns that show a connection between options trading volume and stock prices. There is solid rationale behind these patterns due to systematic delta hedging by market makers and other participants (which we won’t cover in detail here).

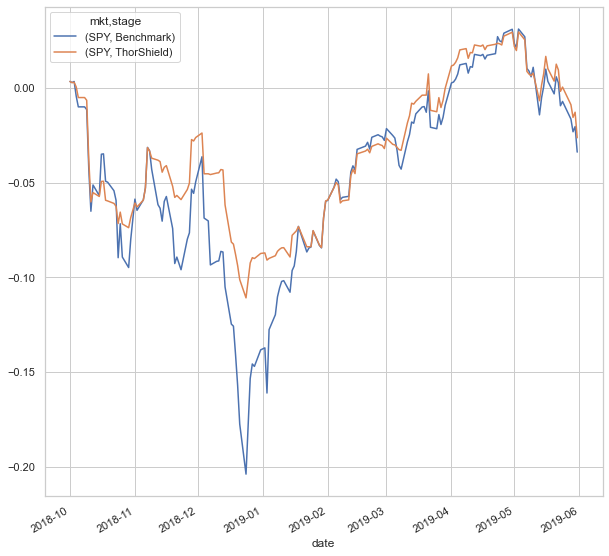

Our goal was to find actionable back-tested signals which would reduce equity draw downs. The three charts below show the performance of our options signal in reducing drawdowns in SPY during sell-offs in 2020, 2018 and 2008.

In the recent March 2020 sell-off, our model limited the draw-down in SPY significantly, as shown below. We call our first model Thor’s Shield because we are seeking to shield our retirement accounts from aggressive equity drawdowns.

In the late 2018 sell-off, our model also limited losses while maintaining upside potential when options data suggested it was safe to re-allocate to SPY.

In the late 2018 sell-off, our model also limited losses while maintaining upside potential when options data suggested it was safe to re-allocate to SPY.

Having avoided the heaviest draw-downs in 2008, our model was able to significantly out-perform SPY through the end of 2009.

The Bottom Line

We could continue to show historical examples that demonstrate how our model limits drawdowns by exiting SPY at the appropriate times.

The point we want to make is that we can see a repeatable connection between options order flow and price pressure on the underlying market. Gamma means “risk,” and price and risk often go hand-in-hand.

There has been a lot of interest in gamma lately, and also a lot of discussion about it. Even though we study options and gamma on a daily basis, sometimes we read articles on it and wonder, “what’s the action step?”

We are working to bridge the gap between analysis and investor decisions relating to gamma.

Thor’s Shield is the first product that translates our research into a decision tool. If you would like to learn more, please visit our website, or download a complimentary report.

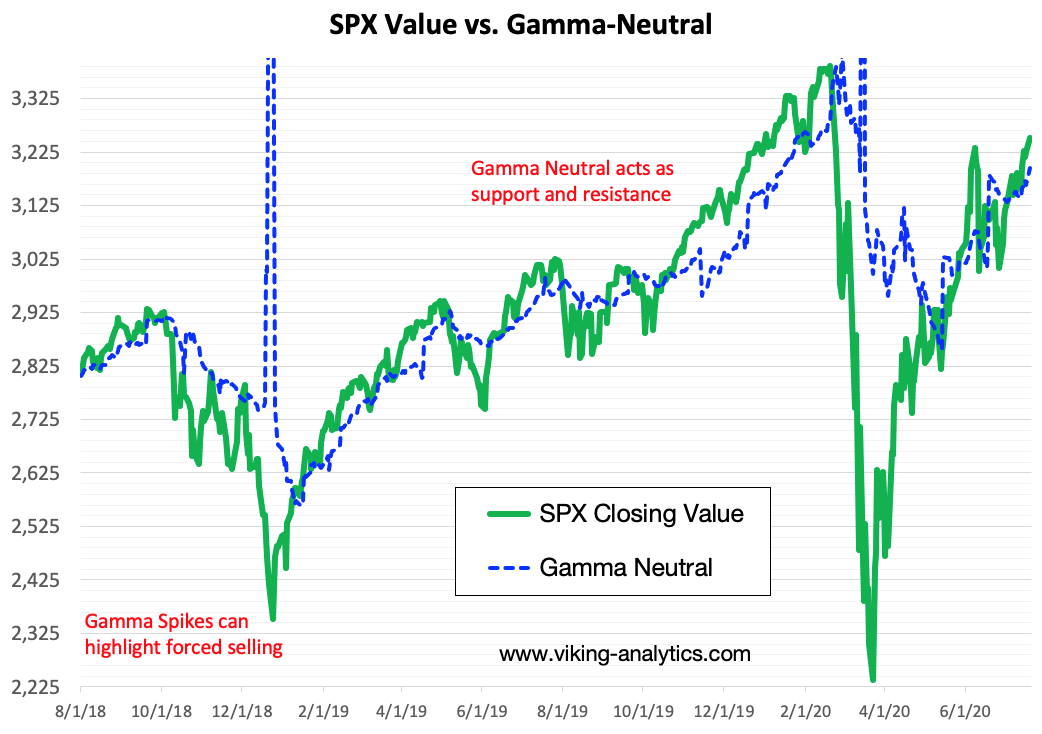

Gamma Neutral

From a longer-term perspective, we have a metric called “Gamma Neutral,” which has shown to act as support and resistance. We would generally maintain a long bias as long as SPX is above Gamma Neutral, which is currently near 3,200.

Authors

Erik Lytikainen, the founder of Viking Analytics, has over 25+ of experience as a financial analyst, entrepreneur, business developer, and commodity trader. Erik holds an MBA from the University of Maryland and a BS in Mechanical Engineering from Virginia Tech.

Rob McBride has 15+ years of experience in the systematic investment space and is a former Managing Director at a multi-billion dollar hedge fund. He has deep experience with market data, software and model building in financial markets. Rob has a M.S. in Computer Science from the South Dakota School of Mines and Technology.