In this edition of the Value Seeker Report, we analyze an investment opportunity in Spectrum Brands Holdings (NYSE: SPB) using fundamental and technical analysis.

Overview

- Spectrum Brands Holdings (NYSE: SPB) is a branded consumer products company with sales across the globe. With a market-cap of $2.5B, it’s a small-cap stock in the Consumer Staples sector.

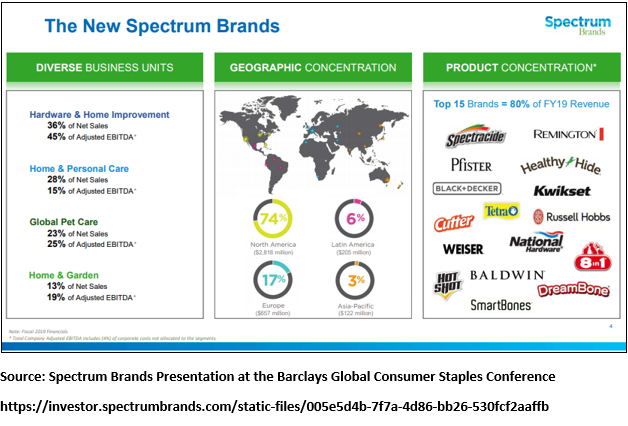

- Most of SPB’s sales are in North America (74%), followed by Europe (17%), Latin America (6%), and the Asia-Pacific region (3%). SPB’s customers mainly consist of large retailers, wholesale distributors, and residential construction companies.

- The firm reports sales in four diverse operating segments, all themed around the home. They are Hardware & Home Improvement (36%), Home & Personal Care (28%), Global Pet Care (23%), and Home & Garden (13%). Some of SPB’s most popular brands are shown below, courtesy of a slide from the company’s recent presentation at the Barclays Global Consumer Staples Conference.

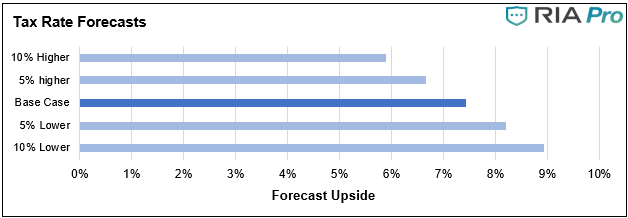

- SPB’s stock is currently trading at $56.96 per share. Using our forecasts, we arrive at an intrinsic value of $61.18 per share. This implies an upside of 7.4% on the investment.

Pros

- SPB has seen more recovery from its March lows than most small-cap stocks. Still, the stock still has over 13.6% to gain before recording a new 52-week high.

- The Company has paid a quarterly dividend of $0.42 per share since it began paying them in the second quarter of 2018. The stock’s current dividend yield is 2.95%.

- Although SPB has had a rough past, the firm is under new leadership which is implementing changes that should create value for shareholders.

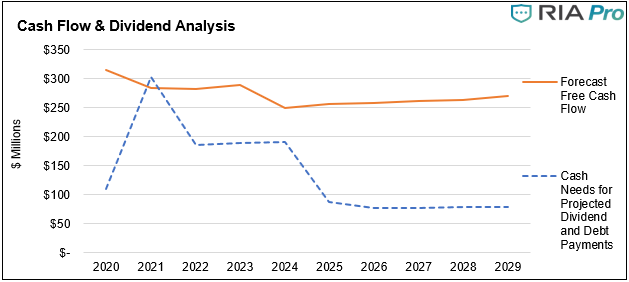

- As shown below, our forecasts indicate that SPB will produce the free cash flow required to cover its dividend and projected debt payments through 2029.

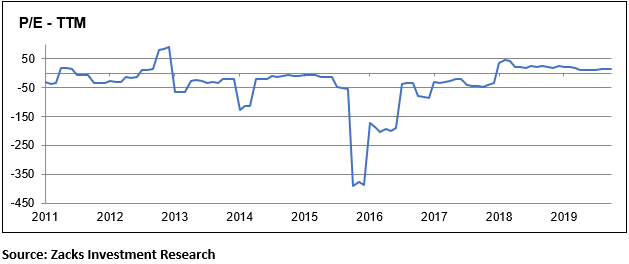

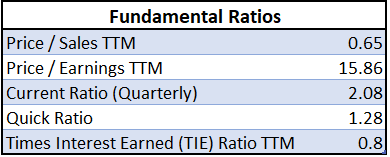

- The stock trades at a Price to Earnings (P/E) ratio of 15.2 as shown below. When put up against the broad market on a fundamental basis, SPB is inexpensive.

Cons

- SPB had just completed multiple divestitures and used the proceeds to pay down its large debt burden when COVID hit. Since the pandemic, SPB’s debt has increased once again to less-than-desireable levels. Solvency still isn’t an issue, though.

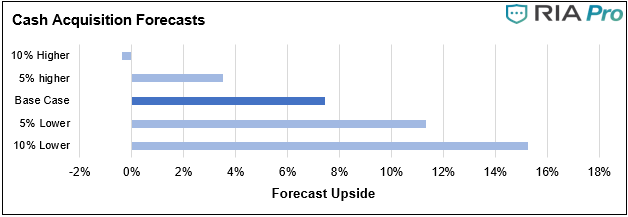

- SPB operates in a mature line of business, and thus has trouble stimulating meaningful organic revenue growth. Strategic acquisitions have been a part of SPB’s growth strategy, but if not prudent, the growth could work against Management’s productivity improvement plans.

Key Assumptions

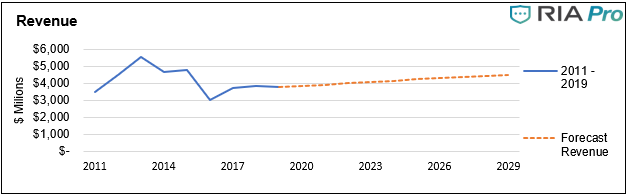

- Revenue will grow slightly in 2020 as the pandemic has provided unexpected tailwinds for the business. We assume growth will strengthen in 2021 and fall slightly to its long term rate over the remaining forecast period. The chart below illustrates our forecasts in relation to historical revenue.

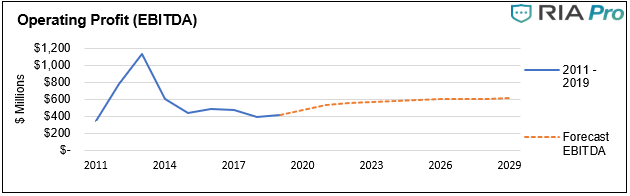

- We expect operating margins to increase as global restructuring plans begin to wrap up. Thereafter, margins will remain relatively steady, but drop slightly over the remainder of the forecast period. The chart below shows how our forecasts of EBITDA evolve over time.

Sensitivity Analysis

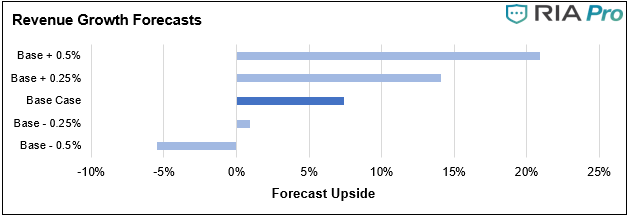

- A brief note on why we present sensitivity analysis can be found here. SPB marks the first time we are able to demonstrate the true value of sensitivity analysis in the Value Seeker Report.

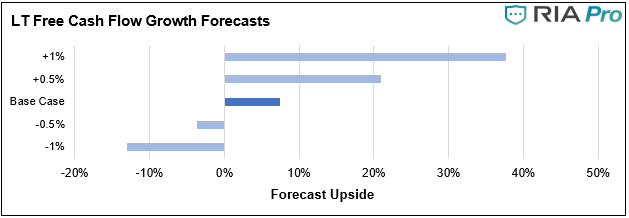

- The analysis reveals that all else equal, if realized margins are 0.5% below our forecasts, SPB is overvalued by roughly 4.6%. Coincidentally, our investment thesis is partially based on the effect SPB’s Global Productivity Improvement Plan should have on margins.

- Thus, we realize the stock could be overvalued if the Global Productivity Improvement Plan is less impactful than expected.

Technical Snapshot

- SPB is testing support at its 50-day moving average. If the stock can continue to hold that level until the market finishes correcting, it faces strong resistance around $61 per share.

- If SPB breaks below its 50-day moving average, it doesn’t encounter another level of support until its 200-day moving average, just above $50 per share.

Value Seeker Report Conclusion On SPB

- SPB is a bit of a comeback story. One about years of mismanagement coming to an end and the beginning of a new era for shareholders. SPB’s global restructuring plans aim to improve core competencies and harness technology with the purpose of delivering shareholder value. The large divestitures in recent years serve as a landmark for the beginning of the journey, now it’s up to Management to stick to its vision and deliver results.

- Based on our forecasts, SPB has 7.4% of upside remaining before reaching its intrinsic value.

- While we do not plan to add SPB to our portfolio at this time, it’s undervalued and we are keeping an eye on it. Things can change, and we like the company.

For the Value Seeker Report, we utilize RIA Advisors’ Discounted Cash Flow (DCF) valuation model to evaluate the investment merits of selected stocks. Our model is based on our forecasts of free cash flow over the next ten years.