In this edition of the Value Seeker Report, we analyze an investment opportunity in PetMed Express (NasdaqGS: PETS) using fundamental and technical analysis.

Overview

- The COVID pandemic has bolstered demand for e-commerce almost everywhere you look. For example, pet care has seen a significant increase in e-commerce traffic for products ranging from toys to medication.

- PetMed Express (PETS) is America’s largest pet pharmacy. Its market cap is $606.7M, which makes it a small-cap stock.

- PETS does all of its business direct-to-consumer through the e-commerce channel. Its primary competitor in this space is Chewy (NYSE: CHWY). However, PETS focuses mainly on prescription and over-the-counter (OTC) medications, while CHWY ships a broad spectrum of products.

- PETS’ stock is currently trading at $30.38 per share. Using our forecasts, we arrive at an intrinsic value of $41.14 per share. This implies an upside of 35.3% on the investment.

Pros

- The market had briefly priced in the benefit PETS will receive from the pandemic as early as March. Although, following PETS’ last earnings report, investors have tempered their expectations. As a result, PETS’ stock would need to appreciate over 38% in order to reach its August peak once again.

- The Firm has paid a quarterly dividend since 2015. In May, PETS raised its quarterly payout to $0.28 per share from $0.27 per share previously. The stock’s current dividend yield is 3.6%.

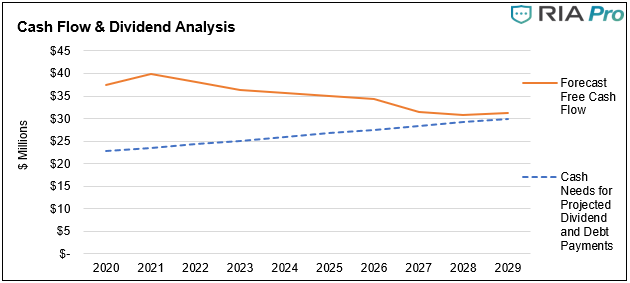

- As shown below, our forecasts indicate that PETS will produce the free cash flow necessary to raise its dividend by $0.04 per share annually over the forecast period.

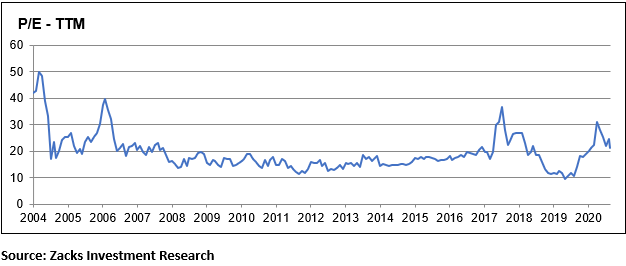

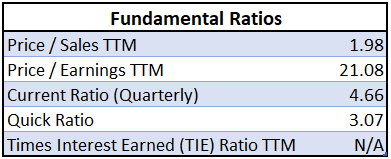

- The stock trades at a Price to Earnings (P/E) ratio of 21.1. This isn’t particularly low, but investors should view the recent dividend increase as an indication of higher future earnings expectations.

Cons

- PETS operates under a debt-free capital structure. With all the recent criticism of non-productive debt issuance, you may be thinking this point was misplaced. It wasn’t. Just as too much debt can be problematic, businesses that don’t utilize enough debt can destroy value for shareholders.

- The Company appears to be self-financing operations by keeping a substantial balance of excess cash. If PETS were to perform even a mini leveraged-recapitalization, equity holders would be better off.

- PETS is susceptible to increased future competition. It has seen increasing profit margins in the last few years and is now experiencing bolstered demand. Thus, this is an inviting situation for potential new entrants.

Key Assumptions

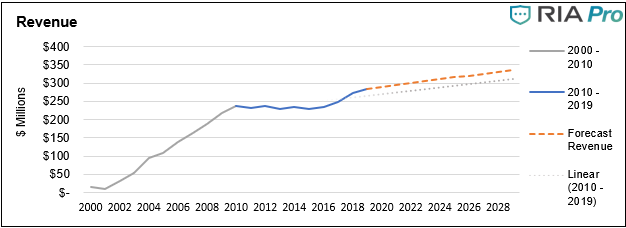

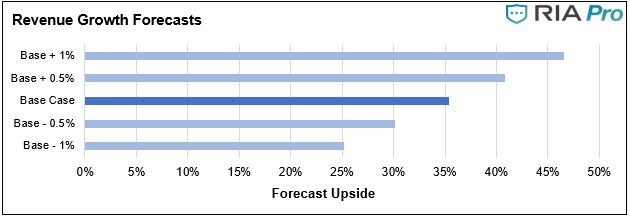

- PETS’ historical revenue growth has been anything but impressive. However, management has inspired modest growth with recent investmets. As shown below, we forecast revenue growth to remain modest yet steady over the forecast period.

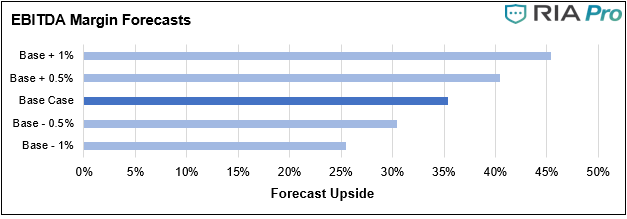

- We forecast PETS’ operating margins to increase slightly in 2020, then taper off rather quickly as competition builds. We expect margins to finally settle for the long-term near their 2015 level. Our forecasts of operating profit are shown below.

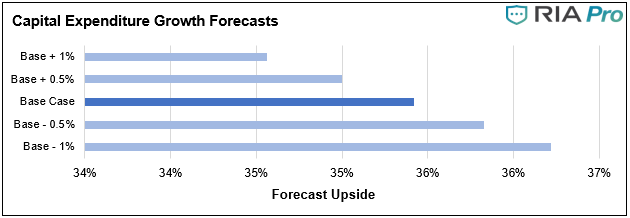

- PETS will begin reinvesting more capital in the business to facilitate modest growth over the forecast period.

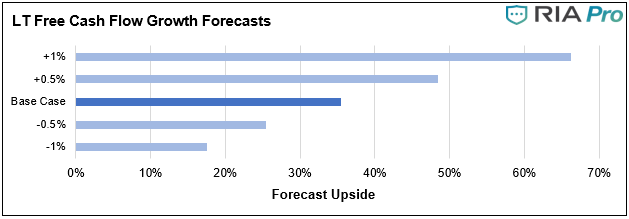

Sensitivity Analysis

- A brief note on why we present sensitivity analysis can be found here.

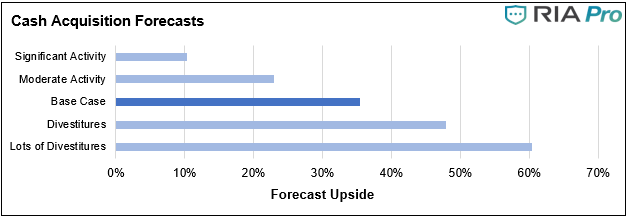

- Management’s efficiency in allocating capital will play a crucial role in determining the intrinsic value of PETS. Fortunately, there is a sizable margin for error.

Technical Snapshot

- PETS recently closed above its 200-day moving average after a brief violation of that level. If PETS holds above its 200-day moving average, it won’t face resistance until it tests the 50-day moving average just below $33 per share.

Value Seeker Report Conclusion On PETS

- Based on our forecasts, PETS offers 35.3% of upside at the current price.

- PETS is a good company with a convincing story, steady cash flows, and decent price. Having said that, we won’t be purchasing the stock, yet. It will remain on our radar, along with some other value stocks, and we may add it to our portfolios at a later date.

For the Value Seeker Report, we utilize RIA Advisors’ Discounted Cash Flow (DCF) valuation model to evaluate the investment merits of selected stocks. Our model is based on our forecasts of free cash flow over the next ten years.