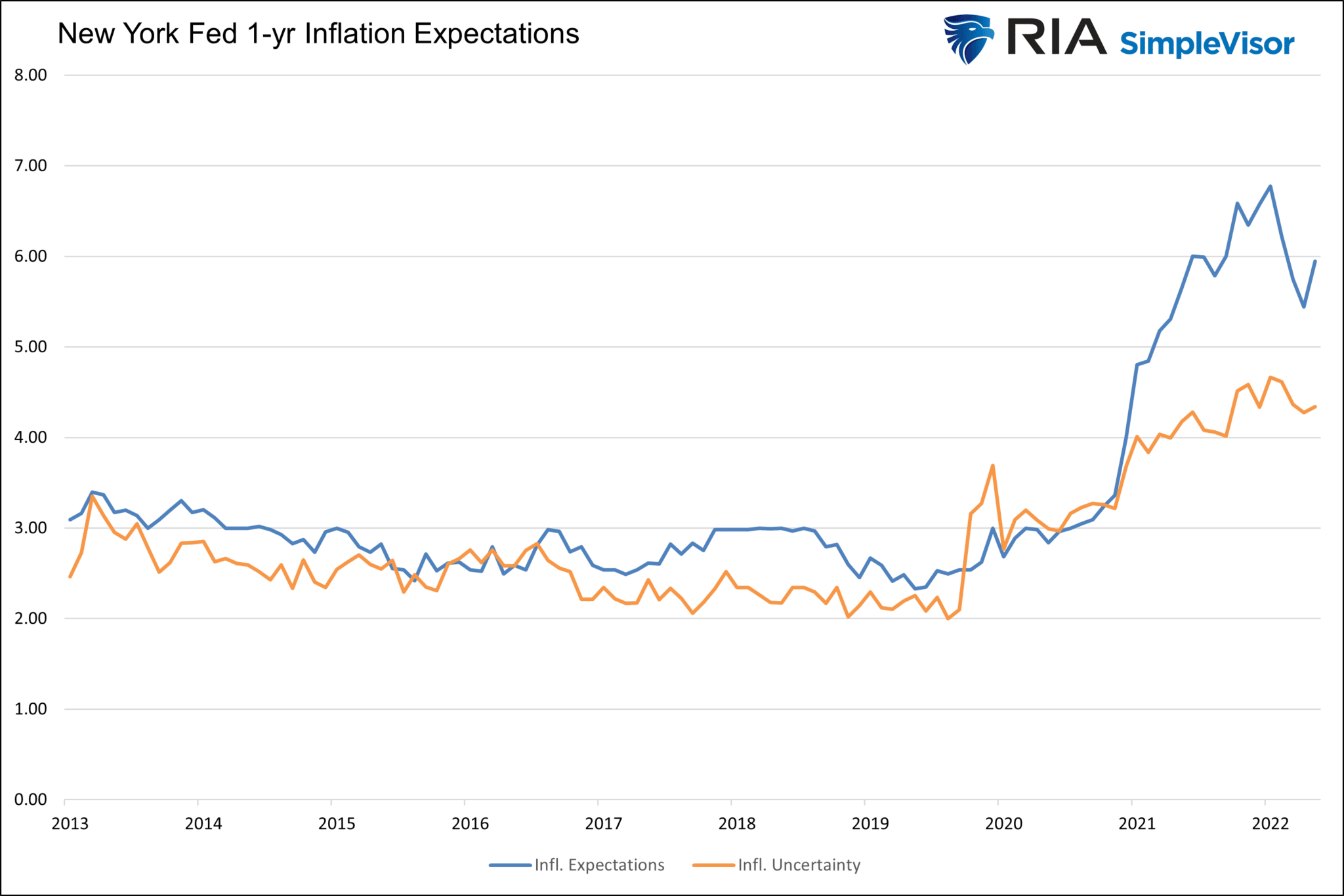

In addition to CPI, PPI, and PCE data, the Fed relies on consumer inflation expectations to guide its actions. The most recent round of data from the New York Fed’s Survey of Consumer Expectations should concern those who think the latest CPI and PPI reports warrant a change in the Fed’s mindset. The New York Fed survey points to higher inflation expectations. Per the survey: “Median inflation expectations increased at both the one- and three-year-ahead horizons in October, by 0.5 and 0.2 percentage points, respectively, to 5.9% and 3.1%. Both increases were broad-based across age, education, and income groups.” Equally concerning, the difference between the expectations of the top and bottom quartile of those surveyed decreased. There is less disagreement among consumers about higher inflation expectations.

The graph below shows the recent uptick in inflation expectations using New York Fed data. Further, consumers remain very uncertain of how much inflation to expect. Uncertainty, or fear that inflation remains high, will drive consumers to demand higher wages. The Fed remains fearful of a wage-price spiral, and the New York Fed survey data only heightens its concerns.

What To Watch Today

Economy

- 8:30 a.m. ET: Retail Sales, October (1.0% expected, 0.0% in September)

- 8:30 a.m. ET: Import Price Index, October (-0.4% expected, -1.2% in September)

- 8:30 a.m. ET: Export Price Index, October (-0.3% expected, -0.8% in September)

- 9:15 a.m. ET: Industrial Production (0.1% expected, 0.4% in September)

- 9:15 a.m. ET: Capacity Utilization (80.4% expected, 80.3% in September)

- 10:00 a.m. ET: Business Inventories (0.5% expected, 0.8% in September)

- 10:00 a.m. ET: NAHB Housing Market Index, November (36 expected, 38 in October)

- 4:00 p.m. ET: Net Long-term TIC Flows, September ($197.9 billion in August)

- 4:00 p.m. ET: Total Net TIC Flows, September ($275.6 billion in August)

Earnings

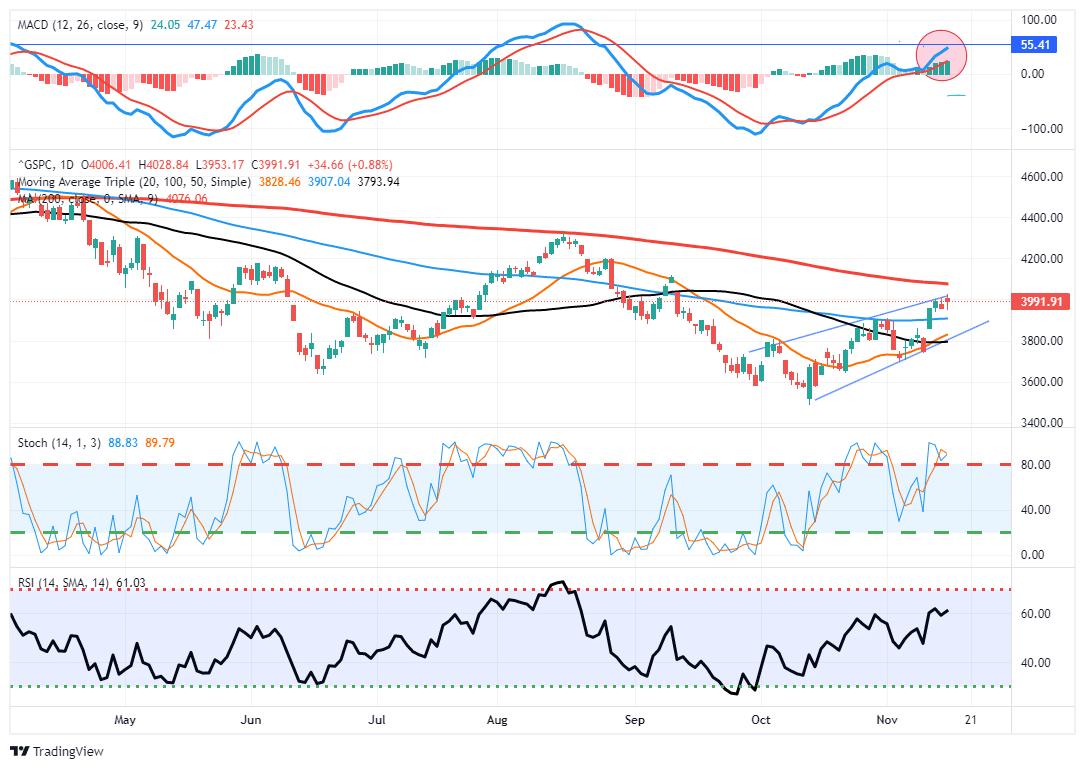

Market Trading Update

The market traded up strongly at the opening yesterday as the Producer Price Index (PPI) confirmed the inflation peak is likely behind us. However, the market sold off at about midday as missiles hit Poland, sending concerns about expanding Russia/Ukraine conflict. Russia quickly rejected the allegations, and the market recovered somewhat into the day’s close.

The market has now rallied to the top of the rising bullish trend channel and, while not extremely overbought, is approaching our initial 4000 targets. Notably, we see a little exhaustion in the rally as morning rallies fail to hold. Also, the MACD “buy signal” is moving toward the top of its channel range. All of this suggests that the rally could have some additional upside, but it is most likely becoming more limited. Continue to take profits and rebalance risk accordingly.

We sold half of our AMD and NVDA positions ahead of earnings tomorrow, so we will see how NVDA reports and plan our next trades.

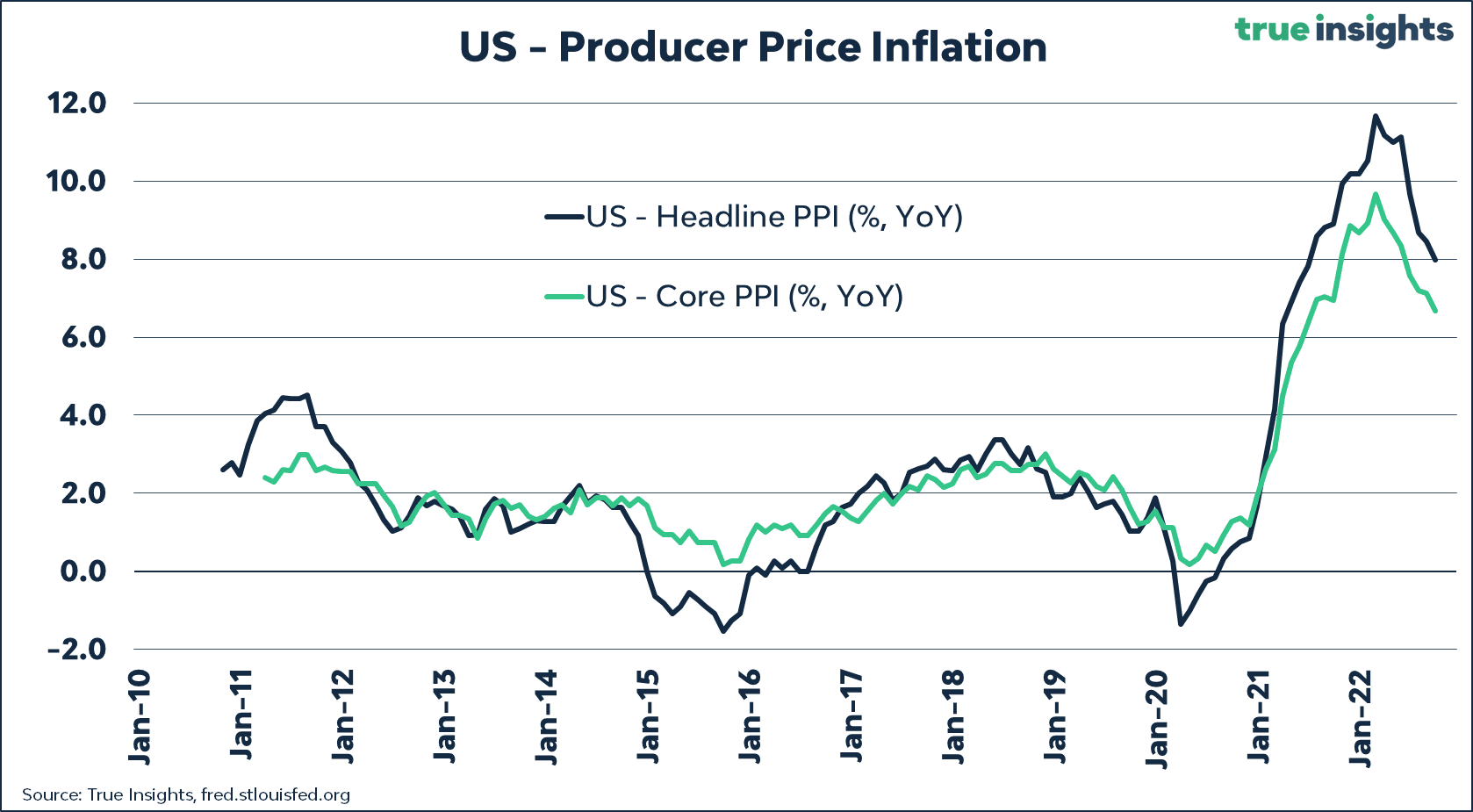

Another Good Inflation Reading

PPI, following last week’s CPI, was better than expected. Monthly PPI only rose 0.2% versus expectations of 0.5%. The year-over-year rate of producer inflation fell from 8.5% to 8.0%. Excluding food and energy, PPI was flat for the month. The data add credence that inflation is peaking. The bigger question, however, remains how fast inflation will fall to get the Fed comfortable it is no longer a problem.

Based on the CPI and PPI reports, a 75bps rate hike is likely off the table. Implied Fed Futures rates agree. They assign an 86% chance of a 50bps at the mid-December meeting. The next relevant inflation reading will be the monthly PCE report on December 1st.

Macro Alf and the Recent Rally

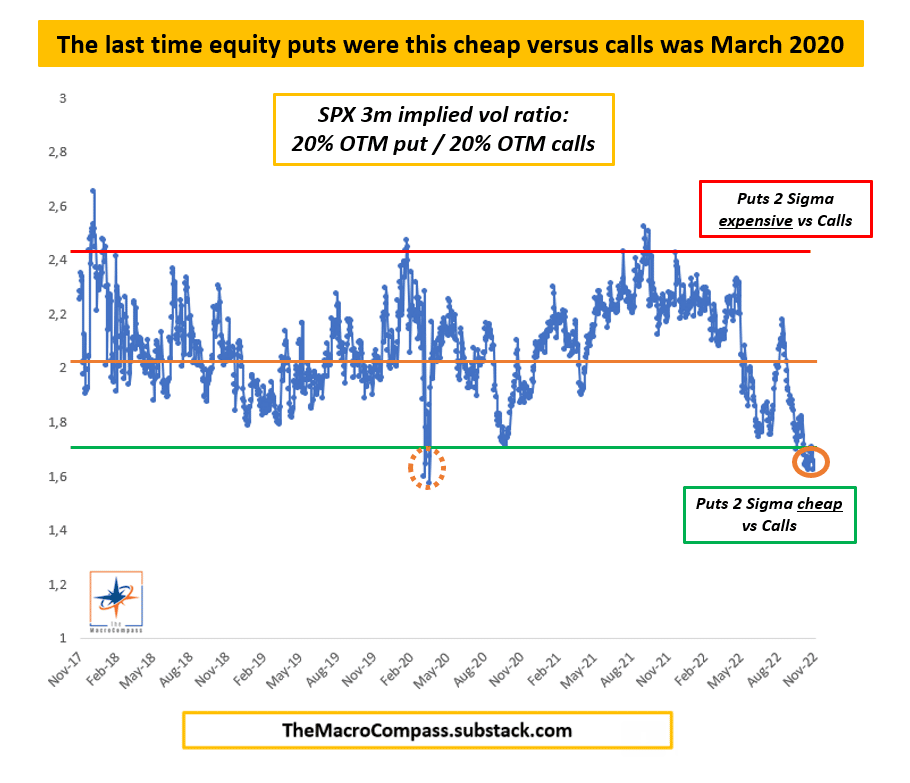

@MacroAlf, Alfonso Peccatiello, puts out some great work with his publication The Macro Compass. In his most recent article, Bear Market Rally or Turning Point (Again)?, Alfonso highlights a couple of charts that are worth considering. The first graph below shows the ratio of the implied volatility of out-of-the-money (OTM) puts versus calls. The ratio is now over two standard deviations cheap. Per Alf-

“In other words, at this point of the year, incentive schemes drive people to be much more willing to pay and chase upside moves than they are to chase downside moves.”

Option activity helped fuel the market higher last week. With calls now so expensive versus puts, it will be hard for options traders to continue to fuel the rally. That said, the current level is at a similar point as the beginning of the 2020 bull run.

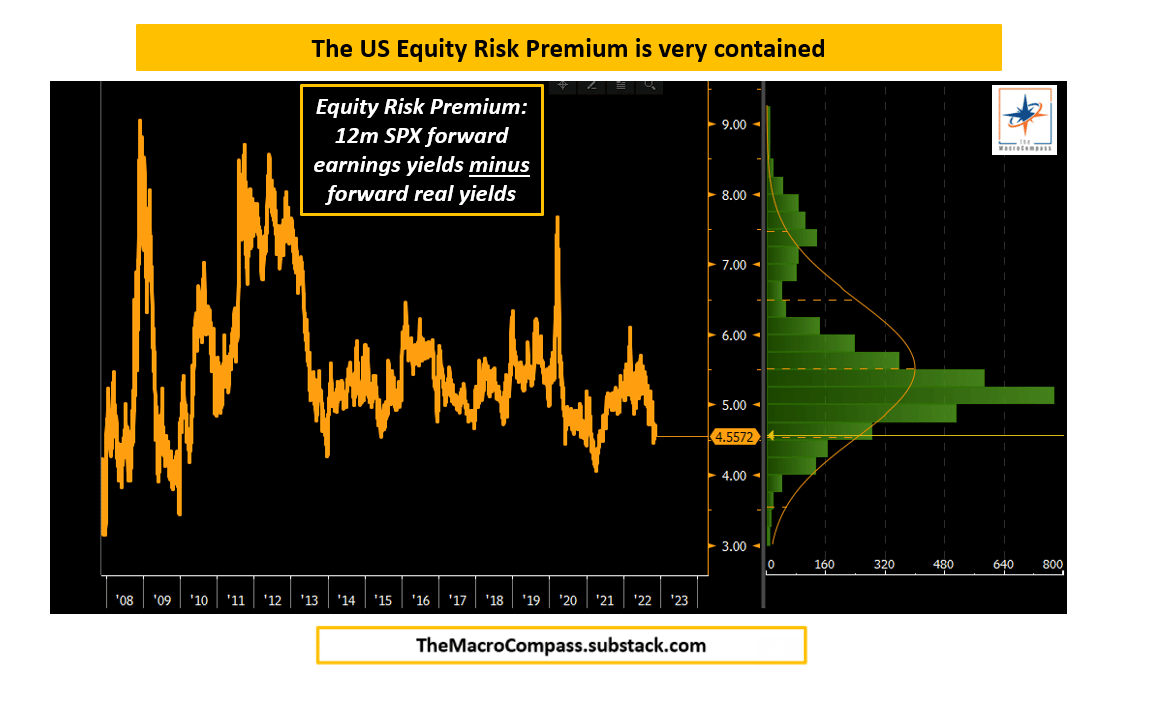

Alf’s second graph shows that last week’s rally drove the S&P 500 equity risk premium to its lowest level in over a year. The equity risk premium (the implied extra yield stock investors should expect to earn versus buying bonds) is about 1% below the average for the last fifteen years. Given the market’s economic and monetary uncertainty, investors should demand an above-average risk premium for buying stocks. In Goodbye TINA, Hello BAAA, we also noted that expected stock returns are too low versus guaranteed bond yields. To wit:

Expected stock returns are on par with risk-free Treasury yields but woefully below the premium spread investors should demand.

Stagflation Says BofA

The chart below from BofA shows that stagflation is the expectation of professional fund managers. The last time such an expectation occurred was in mid-2008. In July 2008, CPI peaked at 5.50% and a year later was -2%. Profession investors were wrong about inflation at that time. However, they were correct that economic activity would slow appreciably. We think inflation will continue to fall from its peak, and economic activity will likely slow. While the circumstances today are very different from 2008-2009, we expect the light blue line, signifying below-trend growth and inflation, will become the new expectation as it did then.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.