- Market Advance Stalls

- Portfolio Position Review

- MacroView: Elites View World Through “Market Colored” Glasses

- Financial Planning Corner: 2-Things Advisors Shouldn’t Do

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Catch Up On What You Missed Last Week

Market Advance Stalls

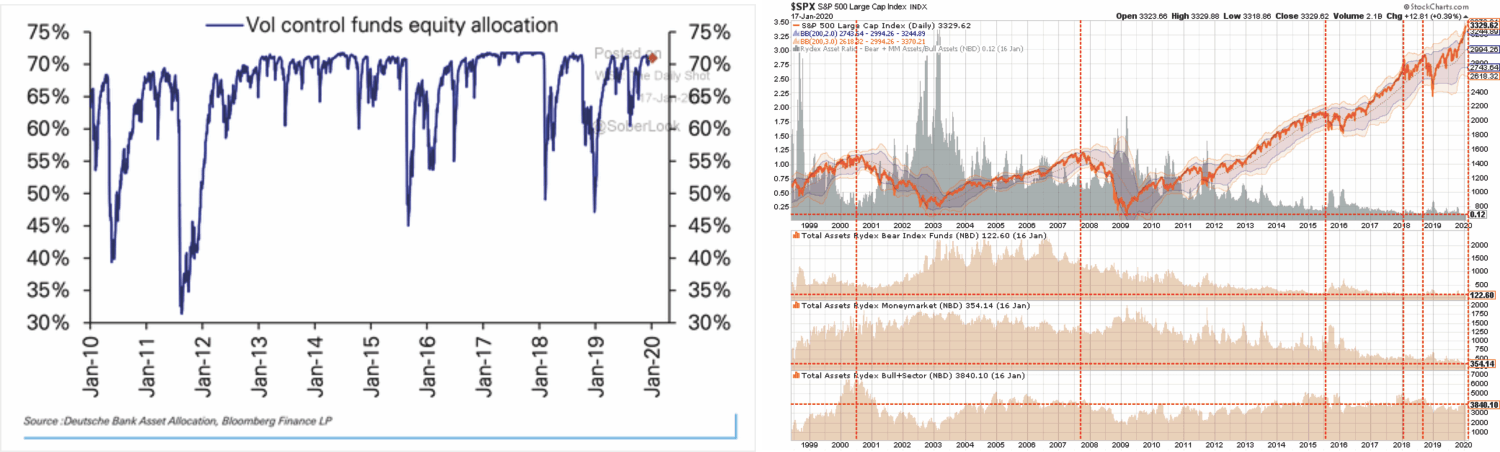

As noted last week, there have only been a few points over the previous 25-years where the market has been so overbought, extended, and bullishly optimistic. To wit:

“This is particularly the case given how extreme positioning by both institutions and individual investors has become. With investor cash and bearish positions, at extreme lows, with prices extremely extended, a reversion to the mean is likely and could lean toward to the 10% range.”

Importantly, this was the repeated message over the last few weeks as the Federal Reserve’s “repo” operations continue to fuel the market’s non-stop advance. As Howard Marks once quipped:

“Being right, but early, is the same as being wrong.”

Clearly, we were early in reducing some of our long-equity exposure in portfolios two weeks ago, but we tend to lean toward the adage; “you never go broke taking profits.” We remain comfortable with our positioning, given the imbalance of risk and reward currently.

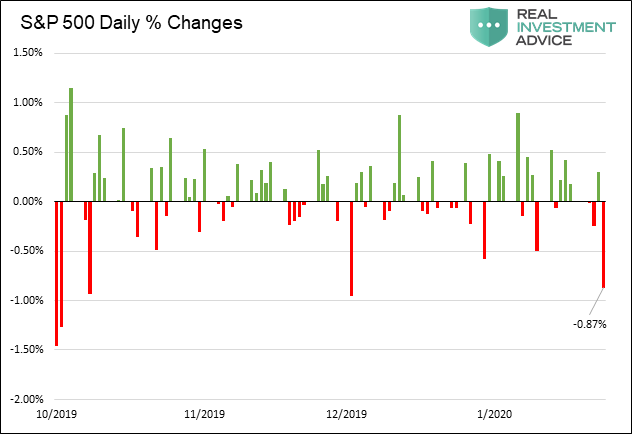

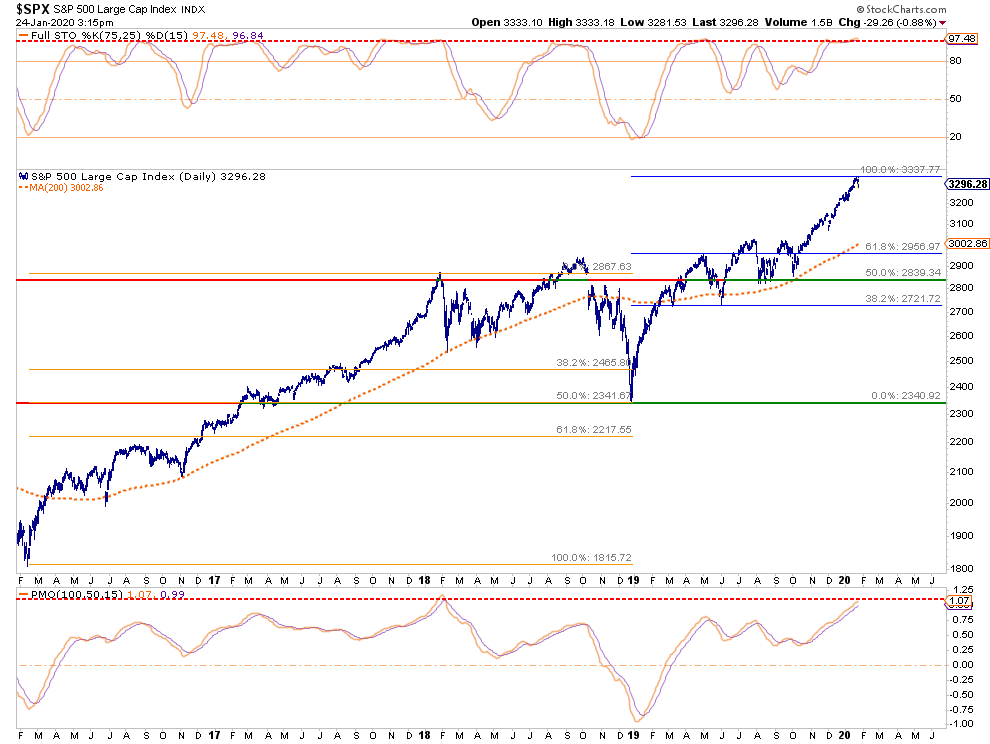

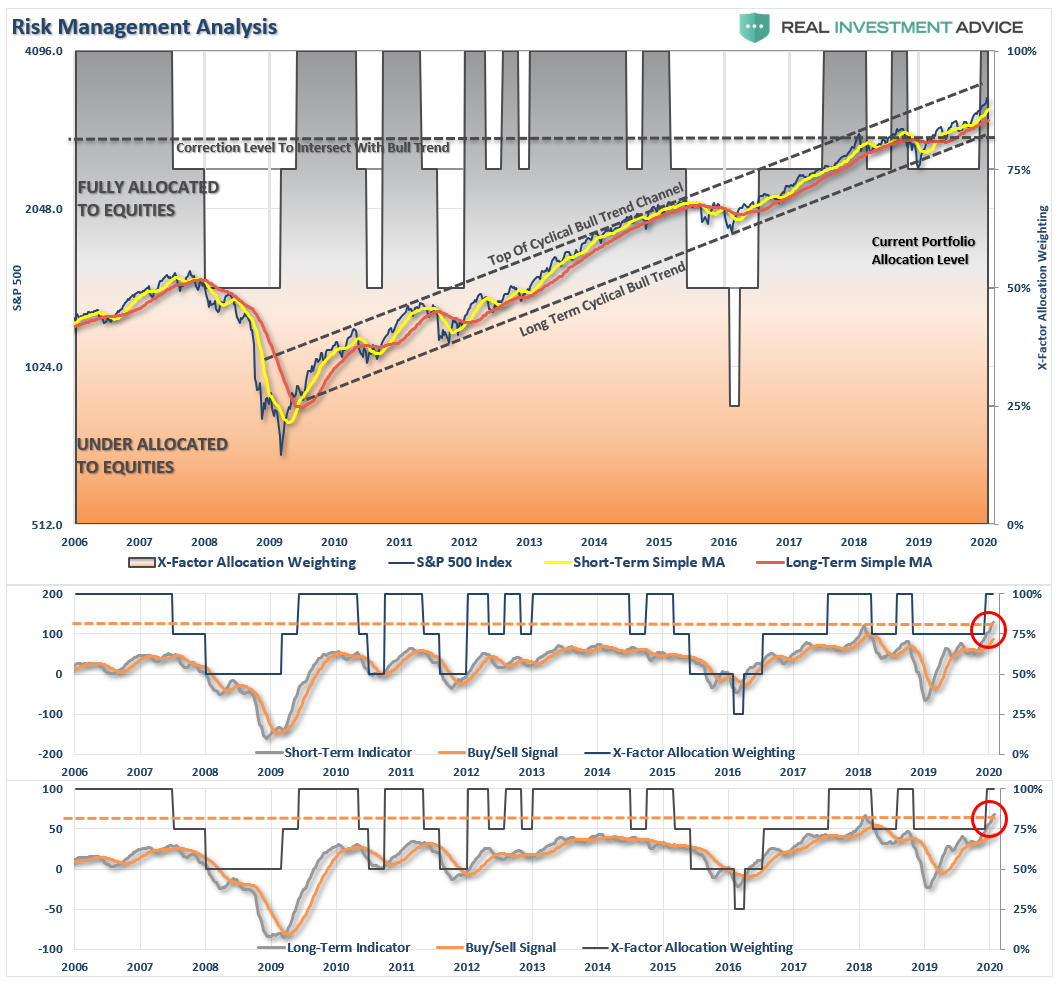

Friday, the market had its first real sell-off since early December. As shown in the chart below, the only other times were in early October before the Fed launched its current “Not QE” program. To put this into some context, since 1970, the market has averaged two 1% declines per month or about every 9-trading days. Since October 2nd, 2018, there have been ZERO days consisting of a 1% decline. Assuming historical averages apply, there should have been nine such events of a 1% decline, or more, by now.

While the media was quick to blame the “coronavirus” in China as the cause for concern, the reality is the markets just needed a reason to sell. As shown in the chart below, the market is so extremely extended, the sell-off barely failed to register.

There are two critical points to take away from the chart above:

- Notice both the overbought/sold indicator (top) and price momentum (bottom) are pegged at market extremes. The previous peak in both indicators was in January 2018.

- More importantly, from the 2016 low to the “blow-off” January 2018 high, the market had a 50% Fibonacci retracement. A similar correction from the December 2018 lows to the recent high would correspond with the January 2018 highs.

In other words, a somewhat typical 15% correction from such an extended, overbought, and bullish position would wipe out 100% of the 2019 gains.

Don’t Fight The Fed

I know, I know.

Such a correction can’t happen because the Fed is expanding its balance sheet. That is true, except the balance sheet expansion is beginning to slow. As recently noted by BMO (courtesy of Zerohedge):

“BMO expects the monthly sizes of $60 billion, or $30 billion post assumed taper, would be composed of both bills and short coupons, ‘helping to reduce expected pressure in the bill market.'”

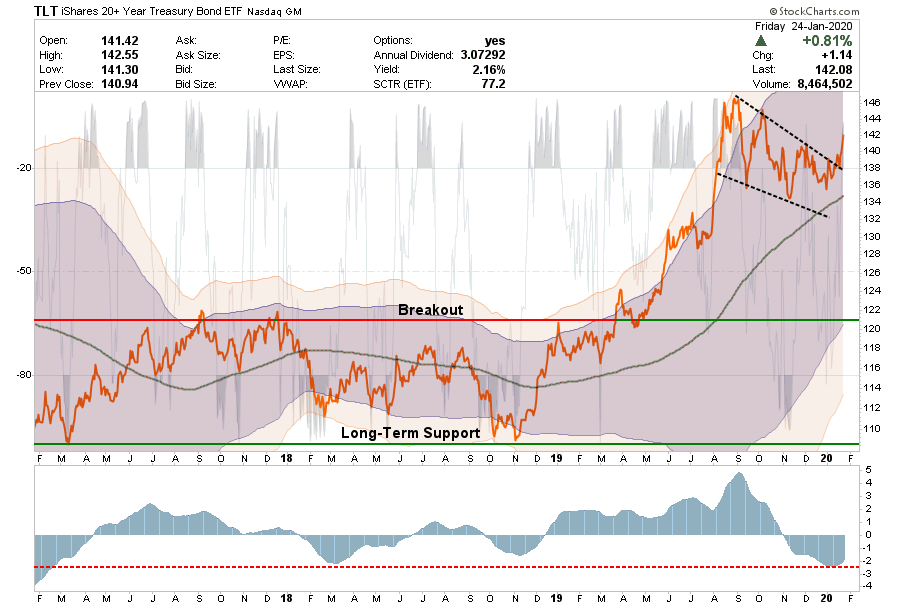

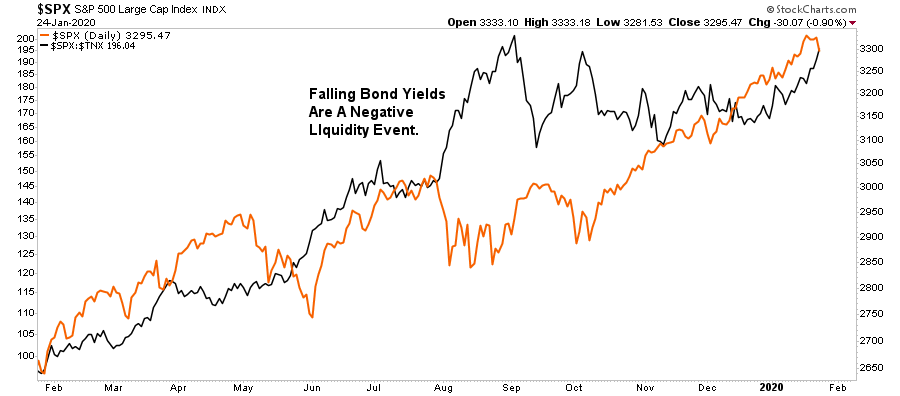

BMO is correct in its analysis; the Fed will convert its short-term bill purchases into longer-term notes to maintain the balance sheet at a higher level. However, maintaining the size of the balance sheet, and expanding it are two entirely different things. Moreover, the market has already been incorporating this reduction in liquidity in their positioning as noted by sharply falling bond yields.

As we discuss weekly with our RIAPRO subscribers (30-day Risk-Free Trial), the 10-year Treasury broke out of its downtrend last week and was signaling a “risk-off” market event. Last Monday we wrote:

“Bond prices rallied last week, again, and are testing downtrend resistance. For now bonds remain in a bearish channel, suggesting higher yields (lower prices) are still likely short-term. I suspect we are going to get some economic turmoil sooner, rather than later, which will lead to a correction in the equity markets and an uptick in bond prices.”

As noted above, with stocks extremely extended, all participants needed was an excuse to “sell.” With a “risk-off” event materializing, the rotation from “risk” to “safety” was completed. The sharp push higher in the stock/bond ratio also suggested a correction was forthcoming.

If we are correct, the Fed will begin to taper their purchases and move to stabilize its balance sheet, which will leave the market “starved for liquidity.” If economic and earnings growth remains weak, such will lead to concerns over current valuations, making that 10-15% correction more likely.

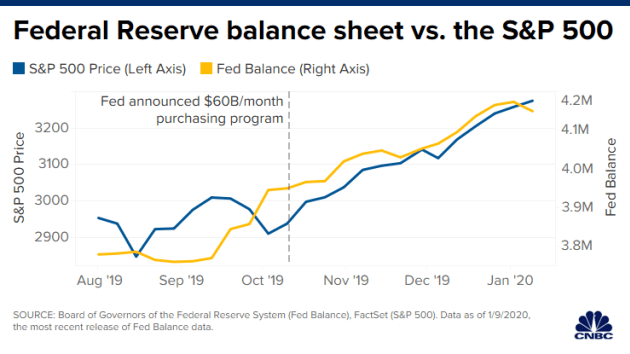

While we certainly have no intention of “Fighting the Fed,” do not dismiss changes to the balance sheet given its close correlation to the rise in equity prices as discussed last week. (Note the decline in the balance sheet which foretold of this week’s sell-off)

“On Oct. 11, the central bank announced it would begin purchasing $60 billion of Treasury bills a month to keep control over short-term rates. The magnitude of the purchases resembles the quantitative easing program the Fed conducted during and after the financial crisis.”

“The increase in the Fed’s balance sheet has been in near lockstep with the stock market’s climb. The balance sheet has expanded 10% since October, while the S&P 500 shot up 12%, including notching its best fourth quarter since 2013.” – CNBC

Given the extreme extension of the markets currently, it is quite likely we will see some more corrective action over the next week.

In other words, it may not be the time to “buy the dip,” just yet.

Economic Warnings

There is currently much hope that the economy is about to emerge from its sluggish growth over the past couple of quarters to support lofty earnings expectations and, potentially, a rise in corporate profitability. As noted previously, the last time the S&P 500 was this deviated from a period of “flat” corporate profit growth was from 1995-1999.

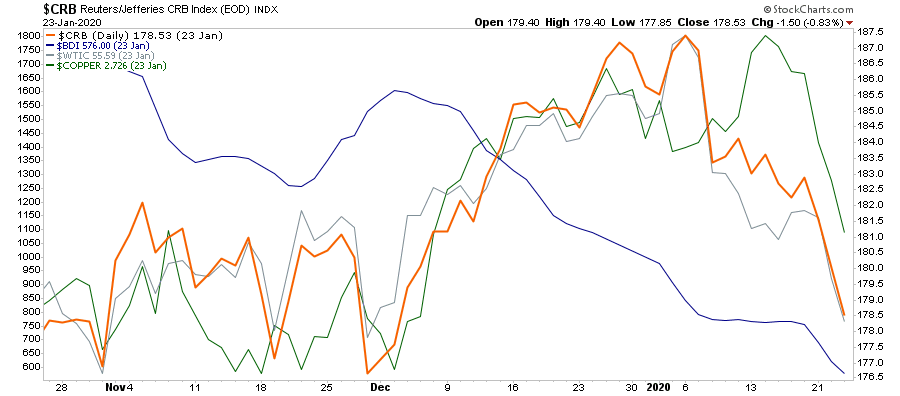

There are a few indicators which, by their very nature, should be signaling a surge in economic activity if there was indeed going to be one. Copper, energy prices, commodities in general, and the Baltic Dry index, should all be rising if economic activity is indeed beginning to recover.

Not surprisingly, as the “trade deal” was agreed to, we DID see a pickup in commodity prices, which was reflected in the stronger economic reports as of late. However, while the media is crowing that “reflation is on the horizon,” the commodity complex is suggesting that whatever bump there was from the “trade deal,” is now over.

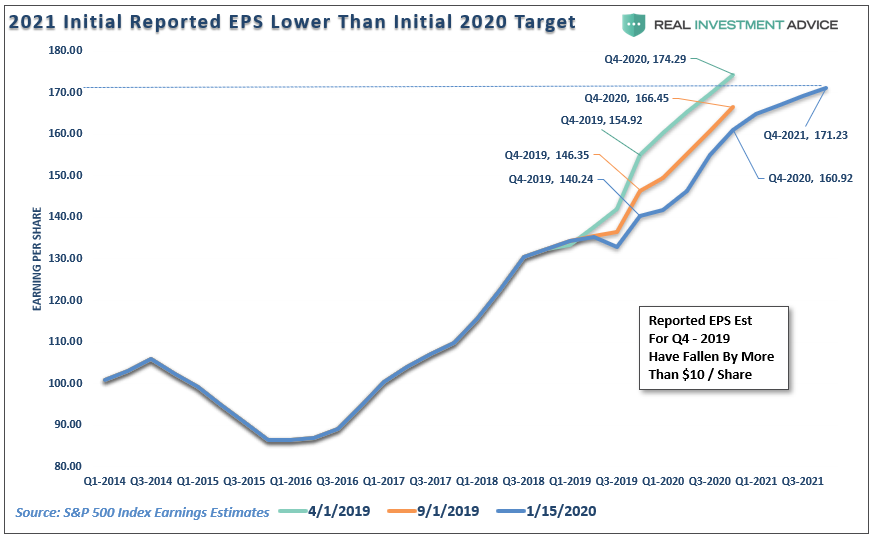

If economic data doesn’t significantly improve, the risk to further corporate profit weakness is of concern. It also puts extremely optimistic projections for S&P earnings through 2020 and 2021 at risk. (Estimates for 2020 have already collapsed, and 2021 is lower than initial 2020 estimates.)

Pay attention to the amount of risk in your portfolio. It will matter more than you think and always at the worst possible time.

Portfolio Positioning

After previously reducing exposure “slightly” to equities, we did not make any further changes to portfolios over the last few days. Given we have shortened our duration in our bond holdings and raised cash levels to roughly 10% of the portfolio, we can afford at the moment to allow our existing long positions to ride the market higher.

This positioning paid off well on Friday, as portfolio drag was about 1/3rd of the market overall. Rate-sensitive holdings (bonds/reits) performed as rates fell, and defensive positions held their ground.

As we move into next week, the market is still going to be “betting on the Fed” until ultimately “beaten into submission,” so we will use rallies to rebalance equity risk as needed, but also add to our fixed income exposure.

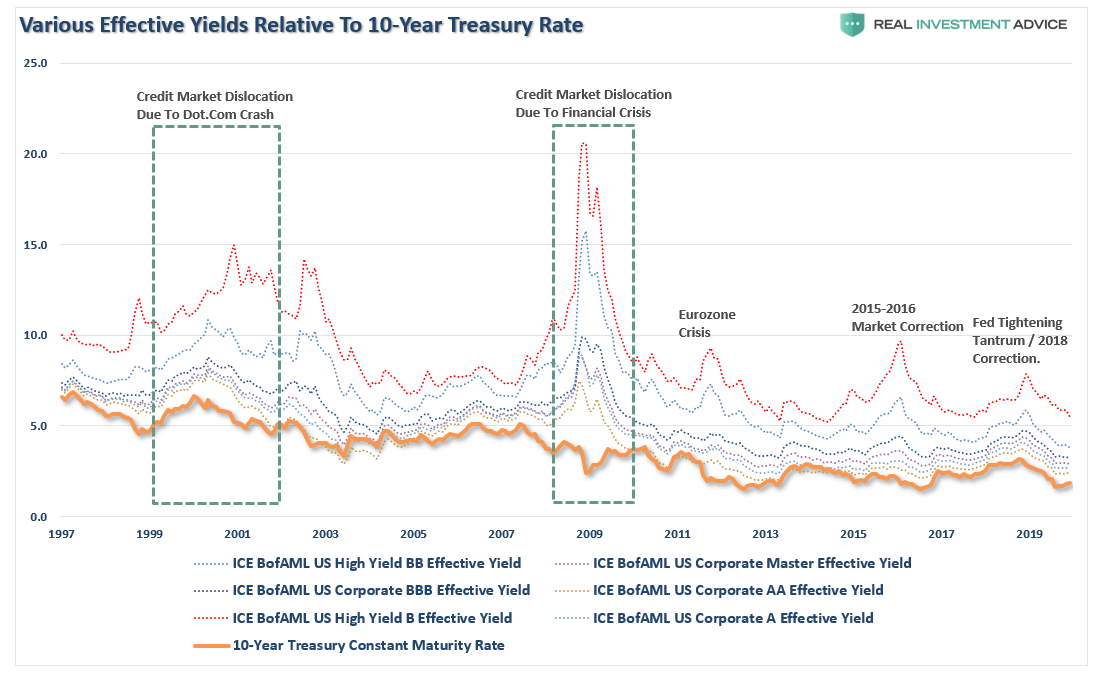

With respect to bonds, make sure you are focusing on “credit quality,” rather than “chasing yield.” As shown in the chart below, and as discussed this past week, when the recession hits, you want to be in Treasuries, and literally nothing else.

While that is hard to believe, just remember its happened twice before.

The Macro View

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Financial Planning Corner

REGISTER NOW for our most popular workshop: THE RIGHT LANE RETIREMENT CLASS

- The Westin, Austin at the Domain- 11301 Domain Drive, Austin, TX 78758

- February 8th from 9-11am.

You’ll be hearing more about more specific strategies to diversify soon, but don’t hesitate to give me any suggestions or questions.

by Richard Rosso, CFP®, CIMA®

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

MISSING THE REST OF THE NEWSLETTER?

This is what our RIAPRO.NET subscribers are reading right now!

- Sector & Market Analysis

- Technical Gauges

- Sector Rotation Analysis

- Portfolio Positioning

- Sector & Market Recommendations

- Client Portfolio Updates

- Live 401k Plan Manager

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation simplified, it allows for better control of the allocation, and closer tracking to the benchmark objective over time. (If you want to make it more complicated, you can, however, statistics show simply adding more funds does not increase performance to any significant degree.)

If you need help after reading the alert; do not hesitate to contact me.

Click Here For The “LIVE” Version Of The 401k Plan Manager

See below for an example of a comparative model.

Model performance is based on a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. This is strictly for informational and educational purposes only and should not be relied upon for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

401k Plan Manager Live Model

As an RIA PRO subscriber (You get your first 30-days free) you have access to our live 401k p

The code will give you access to the entire site during the 401k-BETA testing process, so not only will you get to help us work out the bugs on the 401k plan manager, you can submit your comments about the rest of the site as well.

We are building models specific to company plans. So, if you would like to see your company plan included specifically, send me the following:

- Name of the company

- Plan Sponsor

- A print out of your plan choices. (Fund Symbol and Fund Name)

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.