At the recent Jackson Hole Economic Summit, Jerome Powell unveiled the Fed’s new monetary policy designed to create inflation. In today’s #Macroview, we will discuss the 5-reasons why the Fed will not get inflation, and why deflation is the bigger risk.

The current assumption is that the Fed’s new policy will lead to higher inflation.

“The new policy regime is an important evolution in our thinking about how to achieve our goals and another step toward greater transparency, The policy change positions us for success in achieving our maximum employment and price stability goals in the future.” – Fed Reserve Bank of NY, John Williams, via WSJ

What exactly is this new policy? Well, that’s the interesting part, no one actually knows. However, as noted by the WSJ:

“The Fed said it would now seek to hit its 2% inflation target on average, and that it wouldn’t raise rates just to ward off the theoretical threat of inflation posed by a strong job market. The Fed, however, didn’t say how it would determine the average, and several regional Fed officials suggested that a 2.5% jobless rate was as much as they would tolerate. At the same time, with the economy in deep trouble, there is little expectation inflation will test the Fed’s target for years.”

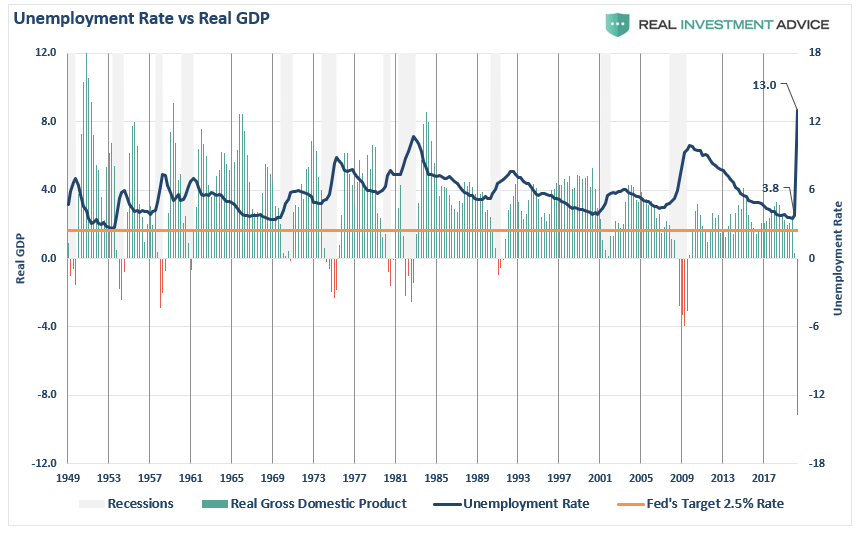

So, to be clear, the Fed’s new policy is simply to “average the inflation rate” over a period of time and let the unemployment rate fall to as low as 2.5%. The last time the unemployment rate was at 2.5% was for one quarter in 1953 just before the 1954 recession set in.

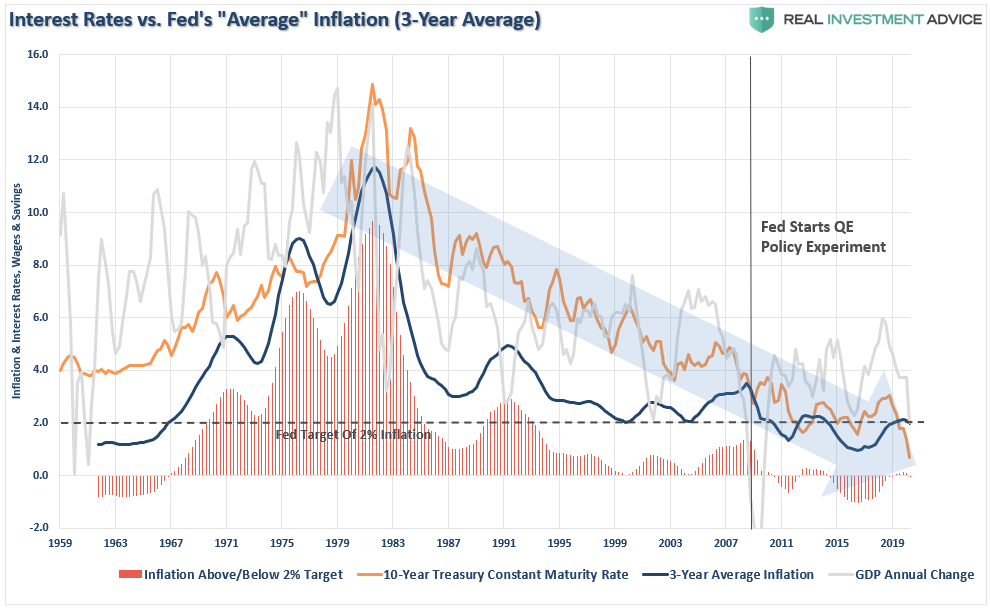

40-Years Of Falling Inflation

The entire premise behind the Fed’s “new policy,” and by being extremely vague about it, is to allow the Fed to maintain, and engage in, “ultra-accommodative” policies without any real limits. However, as shown below, the Fed’s monetary policies have not been successful at creating stronger economic growth or inflationary pressures.

Furthermore, while Wall Street is “buzzing” with talk of surging inflation, the reality is such is not likely to be the case. As we discuss below, the Fed’s policies are actually “deflationary” in nature.

Why Printing Money Won’t Create Inflation

“The Fed is printing money like crazy which is going to lead to inflation.”

For the last 12-years, this belief has remained a constant in the market. It stems from the idea that increasing the money supply is inflationary as it decreases the value of the dollar. There is indeed truth in that statement when considered in isolation. However, when the money supply is increasing, without an increase in economic activity, it becomes deflationary.

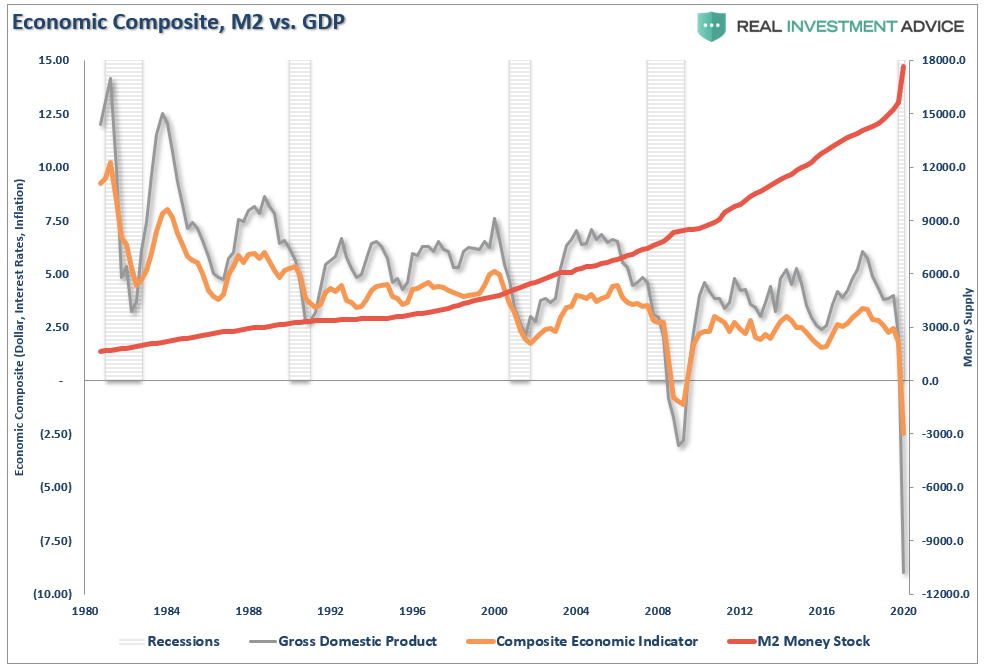

The chart below compares the money supply to GDP growth and our composite economic indicator which is comprised of inflation, wages, and interest rates which all have a direct correlation to economic activity.

Importantly, since 1980 as the money supply increased, economic activity slowed.

This is where monetary velocity becomes important.

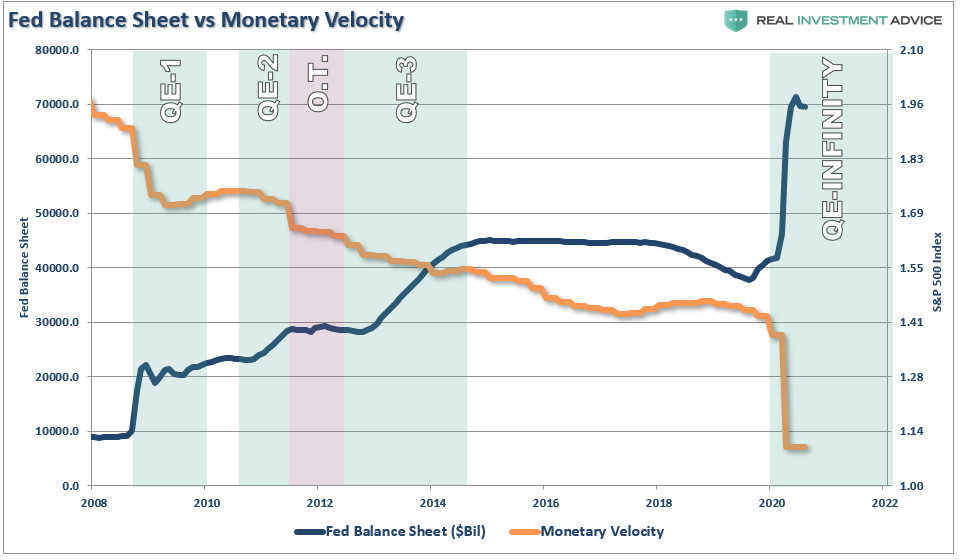

Monetary Velocity

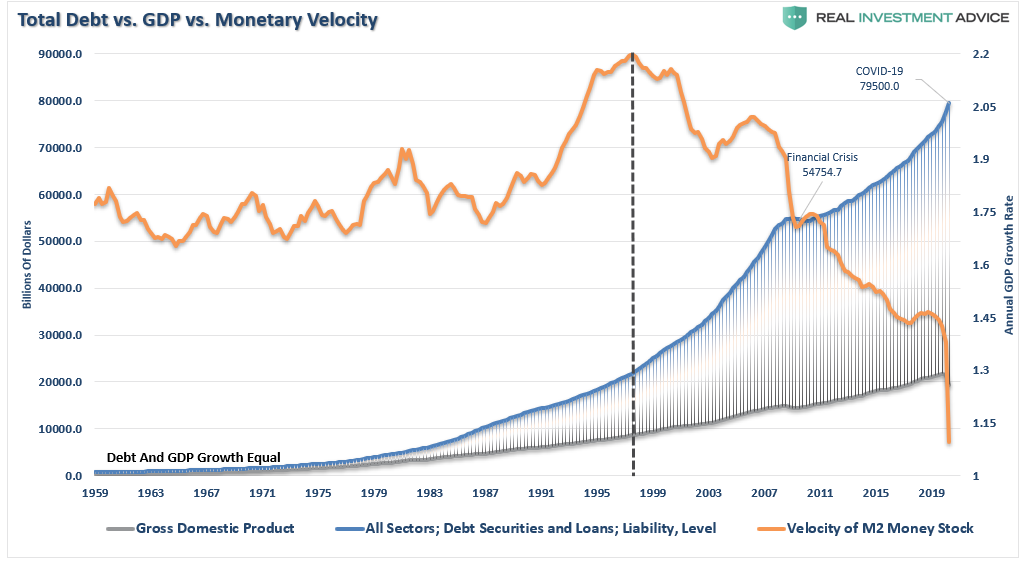

What the Federal Reserve has failed to grasp is that monetary policy is “deflationary” when “debt” is required to fund it.

How do we know this? Monetary velocity tells the story.

What is “monetary velocity?”

“The velocity of money is important for measuring the rate at which money in circulation is used for purchasing goods and services. Velocity is useful in gauging the health and vitality of the economy. High money velocity is usually associated with a healthy, expanding economy. Low money velocity is usually associated with recessions and contractions.” – Investopedia

With each monetary policy intervention, the velocity of money has slowed along with the breadth and strength of economic activity.

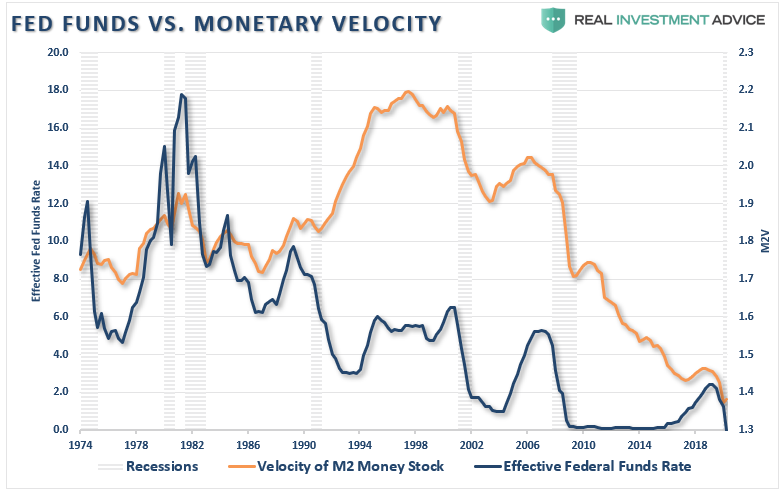

However, it isn’t just the expansion of the Fed’s balance sheet which is undermining the strength of the economy. It is also the ongoing suppression of interest rates to try and stimulate economic activity.

In 2000, the Fed “crossed the Rubicon,” whereby lowering interest rates did not stimulate economic activity. Instead, the “debt burden” detracted from it.

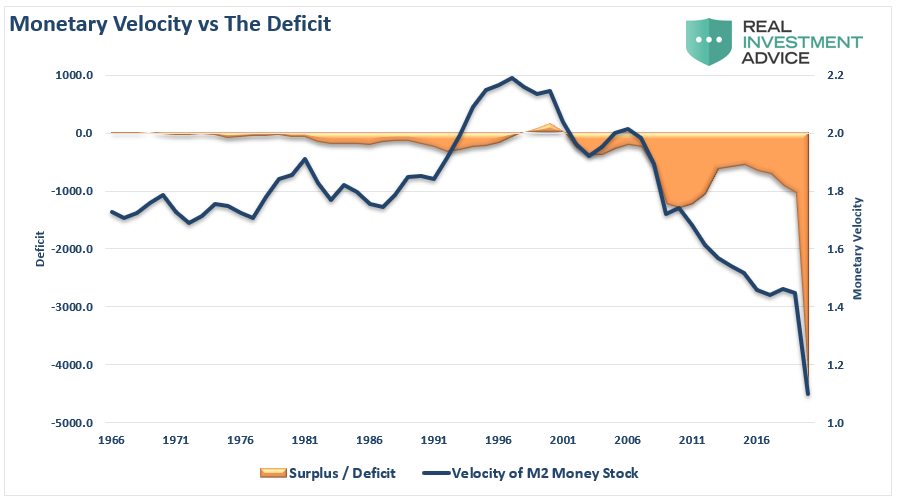

To illustrate the last point, we can compare monetary velocity to the deficit.

To no surprise, monetary velocity increases when the deficit reverses to a surplus. Such allows revenues to move into productive investments rather than debt service.

The problem for the Fed is the misunderstanding of the derivation of organic economic inflation

Why Inflating Asset Prices Won’t Create Inflation

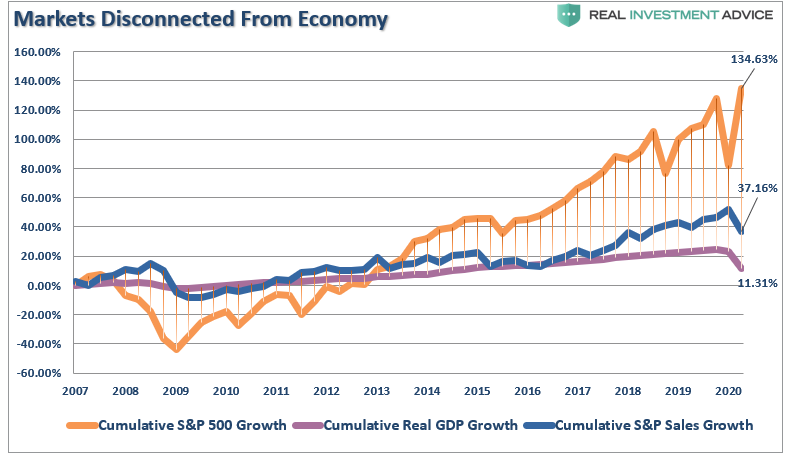

The one thing the Fed has done very successfully is to create “boom and bust” cycles within the economy which has continued to erode the economic prosperity of the masses.

The only reason Central Bank liquidity “seems” to be a success is when viewed through the lens of the stock market. Through the end of the Q2-2020, using quarterly data, the stock market has returned almost 135% from the 2007 peak. Such is more than 12x the growth in GDP and 3.6x the increase in corporate revenue. (I have used SALES growth in the chart below as it is what happens at the top line of income statements and is not AS subject to manipulation.)

Unfortunately, the “wealth effect” impact has only benefited a relatively small percentage of the overall economy. Currently, the Top 10% of income earners own nearly 87% of the stock market. The rest are just struggling to make ends meet.

In order for the Fed to achieve actual inflation, they need an economy that is growing strongly enough to generate increased production to support stronger consumption. Only when there are self-sustaining increases in consumption can you achieve higher sustained rates of inflation.

Creating a “wealth gap” where 10% have the ability to consume while the bottom 90% struggle to make ends meet, continues to apply deflationary pressures on the economy as a whole.

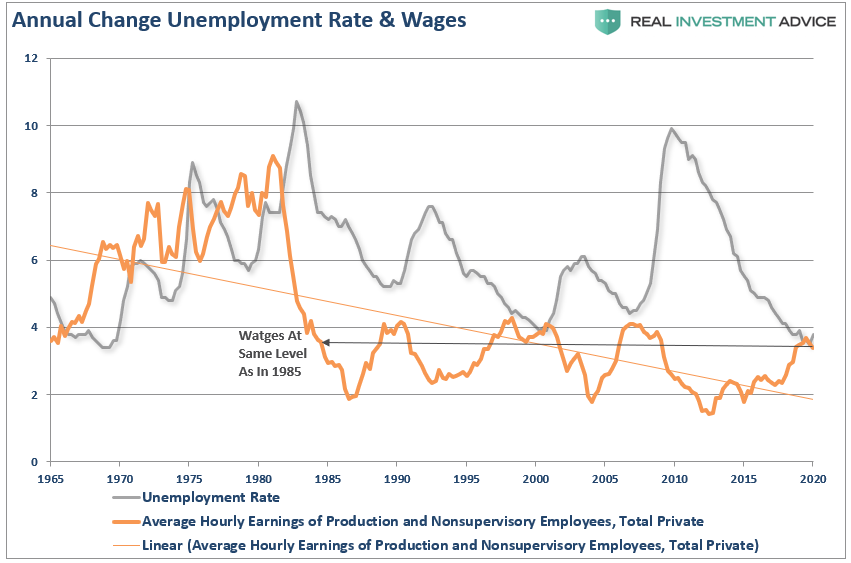

Why Full Employment Won’t Create Inflation

However, let’s assume for a moment that the economy returns back to the same historically low unemployment rate we were enjoying at the end of 2019. As shown in the chart

This is crucially important to understand why the Fed’s actions are “deflationary.”

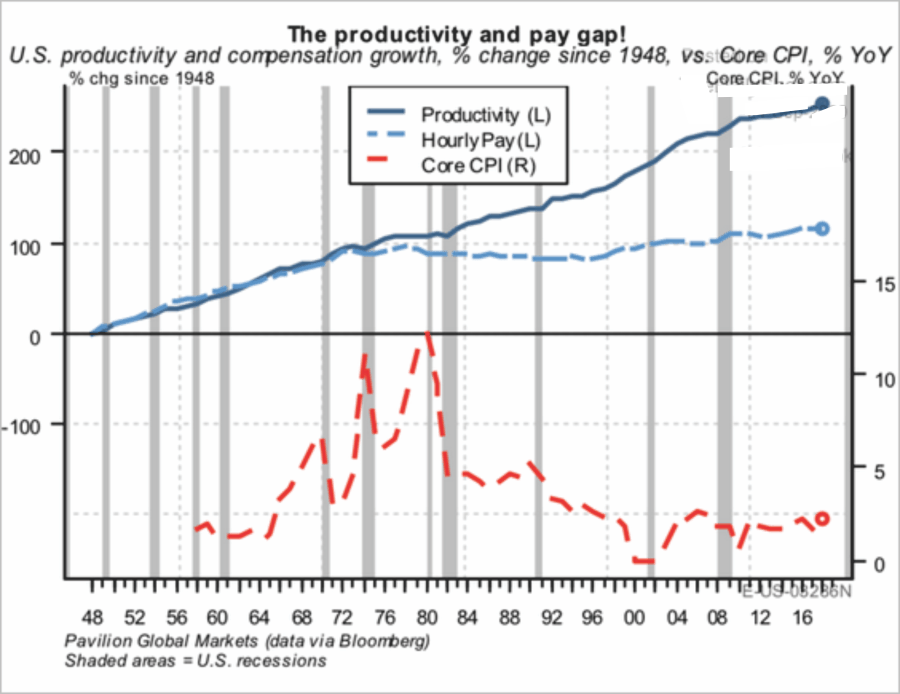

As noted, in order to generate “real inflation,” economic growth must be strong enough to support employment that exceeds the rate of population growth. That employment must ALSO be productive (manufacturing based) employment which leads to higher wages. (Service jobs are deflationary as they go to the lower cost of labor.) Higher wages lead to increased consumption which allows producers to increase prices (inflation) over time.

This has not been the case for nearly 40-years as technology continues to reduce the demand for labor by increasing productivity. This is the “dark side” of technology that no one wants to talk about.

Why Debt Won’t Create Inflation

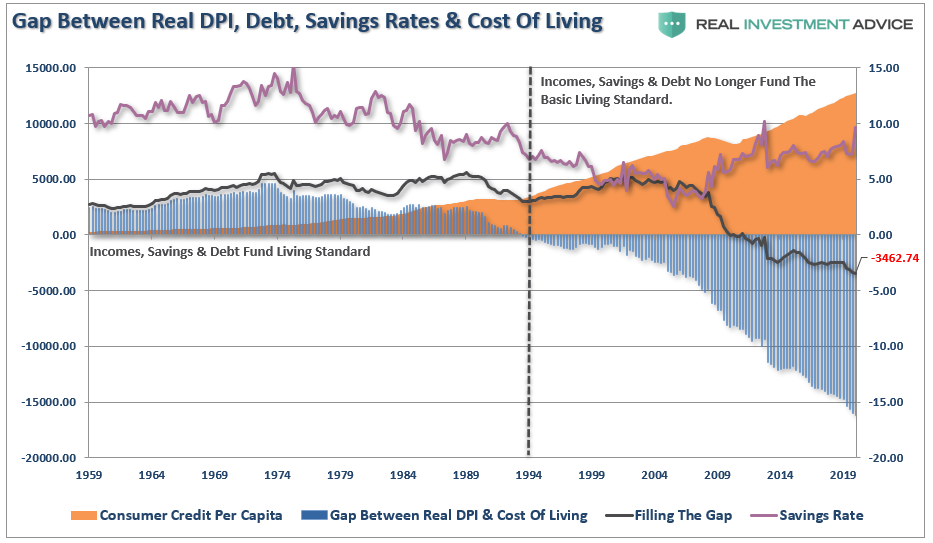

However, this cannot be achieved in an economy saddled by $75 Trillion in debt which diverts income from consumption to debt service. This is why “monetary velocity” began to decline as total debt passed the point of being “productive” to become “destructive.”

The decline in velocity coincides with the point that consumers were forced into debt to sustain their standard of living.

The problem for the Federal Reserve is that due to the massive levels of debt, interest rates MUST remain low. Any uptick in rates quickly slows economic activity, forcing the Fed to lower rates and support it.

With the economy set to push a $4.2 Trillion deficit in 2020, the deflationary pressure alone from the deficit will continue to erode economic activity. As noted, even if the Fed does manage to get a spark of inflation, which would push interest rates higher, the debt burden will lead to an economic recession and deflationary pressures.

Why Sending Money To Households Won’t Create Inflation

If the Government keeps sending money to households, it is going to create inflation.

Such is the underlying sentiment behind a universal basic income and its impact on economic growth. Unfortunately, it simply isn’t true.

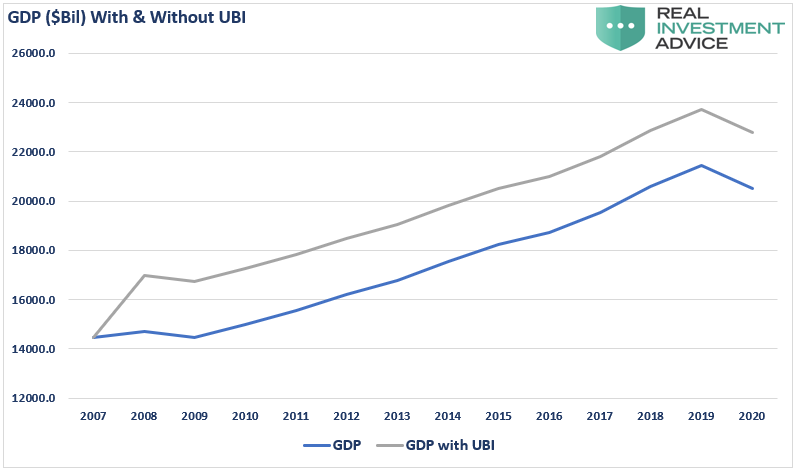

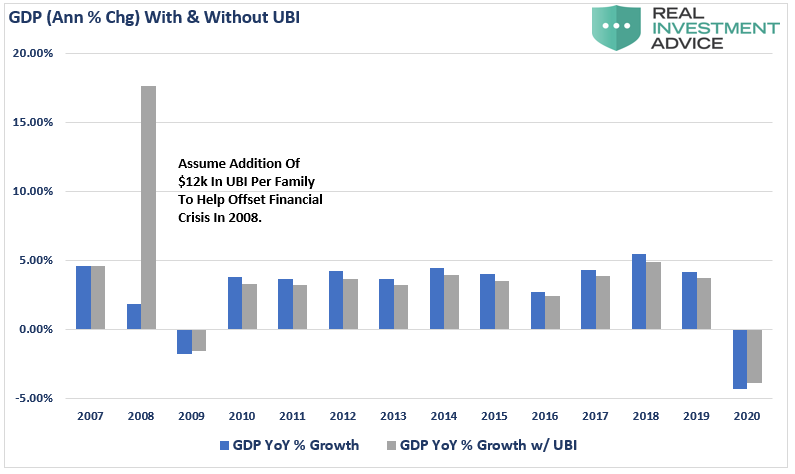

Let’s run a hypothetical example using GDP from 2007 to the present. (I am using estimates of -4.3% for 2020 GDP growth) In 2008, in response to the “Financial Crisis,” Congress passes a bill providing $1000/month ($12,000 annually) to 190 million families in the U.S.

The chart below shows the economy’s annual GDP growth trend assuming the entire UBI program shows up in economic growth. For those supporting programs like UBI, it certainly appears as if GDP is permanently elevated to a higher level.

However, that is an illusion. When you look at the annual rate of change in economic growth, which is how we measure GDP for economic purposes, a different picture emerges. In 2008, when the $12,000 arrives at households, GDP spikes, printing a 17% growth rate versus the actual 1.81% rate.

Beginning in 2009, however, the benefit disappears.

The reason is that after UBI is injected into the system, the economy normalizes to the new level after the first year. Also, notice that GDP grows at a slightly slower rate as the dollar changes to GDP at higher levels print a lower growth rate.

Not Unprecedented

The Federal Reserve’s new policy tool is nothing more than a “do anything” excuse. The reality is the Fed has no actual ability to create employment, control inflation, or create economic prosperity. The only thing they do have the ability to continue to create is the “wealth gap.”

While many suggest the current situation is “unprecedented,” it really isn’t. Japan has been an ongoing experiment for nearly 30-years with the same economic outcome the U.S. is currently experiencing.

Furthermore, we have much more akin to Japan than many would like to believe.

- A decline in savings rates

- An aging demographic

- A heavily indebted economy

- A decline in exports

- Slowing domestic economic growth rates.

- An underemployed younger demographic.

- An inelastic supply-demand curve

- Weak industrial production

- Dependence on productivity increases

The lynchpin to Japan, and the U.S., remains demographics and interest rates. As the aging population grows becoming a net drag on “savings,” the dependency on the “social welfare net” will continue to expand. The “pension problem” is only the tip of the iceberg.

Failure To Launch

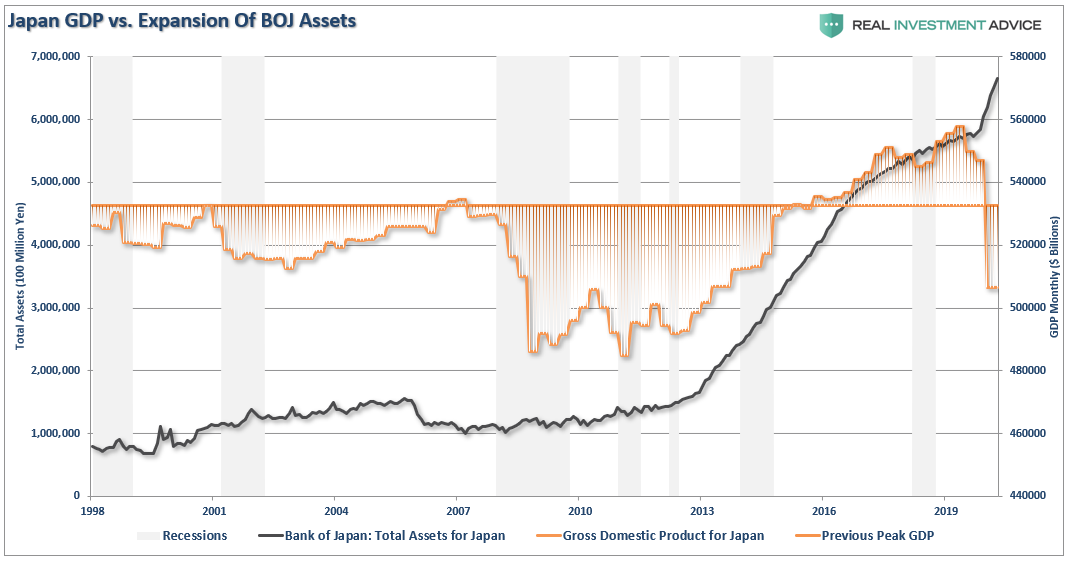

Since the financial crisis, Japan has been running a massive “quantitative easing” program which, on a relative basis, is more than 3-times the size of that in the U.S. However, while stock markets have performed well with Central Bank interventions, economic prosperity is less than it was prior to the turn of the century.

Furthermore, despite the BOJ’s balance sheet consuming 80% of the ETF markets, not to mention a sizable chunk of the corporate and government debt market, Japan has been plagued by rolling recessions, low inflation, and low-interest rates. (Japan’s 10-year Treasury rate fell into negative territory for the second time in recent years.)

While financial engineering clearly props up asset prices, I think Japan is a very good example that financial engineering not only does nothing for an economy over the medium to longer-term, it actually has negative consequences.” – Doug Kass

Summary

There is no evidence the Fed’s “new policy” tool will create inflation, lead to stronger economic growth, or generate better economic equality.

What we are pretty sure of is that their “new policy” is very much the same as the “old policy,” which will likely continue to foster economic inequality, inflated assets, and a further widening of the “wealth gap.”

Most telling is the inability of the current economists who maintain our monetary and fiscal policies to realize the problem of trying to “cure a debt problem with more debt.”

The Keynesian view that “more money in people’s pockets” will drive up consumer spending, with a boost to GDP being the result, has been wrong. It hasn’t happened in 40 years.

We fear the Fed’s new policy will only lead to further social instability and populism. Such has been the result in every other country which has run such programs of unbridled debts and deficits.

As Dr. Woody Brock aptly argues:

“It is truly ‘American Gridlock’ as the real crisis lies between the choices of ‘austerity’ and continued government ‘largesse.’ One choice leads to long-term economic prosperity for all; the other doesn’t.”

Take your pick.