Stocks jumped out of the gate yesterday morning as lower-than-expected inflation readings led investors to think the Fed will curtail its rate hikes and possibly start debating when to cut rates. Today’s FOMC announcement and Powell press conference will tell us if the bulls are on to something.

Monthly CPI inflation was .2% lower than expectations at +.1%. The core inflation number, excluding food and energy, was .2%, lower than expectations of .4%. The data generally points to a clear peak in inflation and a declining trend. The question for investors is how long it will take for inflation to fall to levels that please the Fed. If the Fed lowers rates too soon, financial conditions will ease, and inflation might easily be stoked.

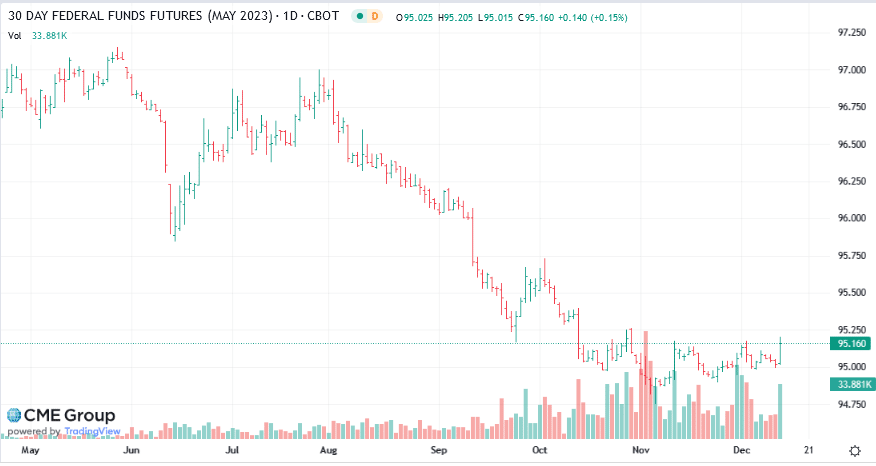

The graph below shows the May 2023 Fed Funds futures contract bottomed at 94.86, equating to 5.14% Fed Funds in May. It now stands at 95.16 or 4.84%. Therefore, the market expects lower prices and a less hawkish Fed. Will Powell deliver today?

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended Dec. 9 (-1.9% prior)

- 8:30 a.m. ET: Import Price Index, month-over-month, November (-0.5% expected, -0.2% prior)

- 8:30 a.m. ET: Import Price Index excluding petroleum, MoM, November (-0.5% expected, -0.2% prior)

- 8:30 a.m. ET: Import Price Index, year-over-year, November (3.2% expected, 4.2% prior)

- 8:30 a.m. ET: Export Price Index, month-over-month, November (-0.5% expected, -0.3% prior)

- 8:30 a.m. ET: Export Price Index, year-over-year, November (5.7% expected, 6.9% prior))

- 2:00 p.m. ET: FOMC Rate Decision (Lower Bound), Dec. 14 (4.25% expected, 3.75% prior)

- 2:00 p.m. ET: FOMC Rate Decision (Upper Bound), Dec. 14 (4.50% expected, 4.00% prior)

- 2:00 p.m. ET: Interest on Reserve Balances Rate, Dec. 15 (4.40% expected, 3.90% prior)

Earnings

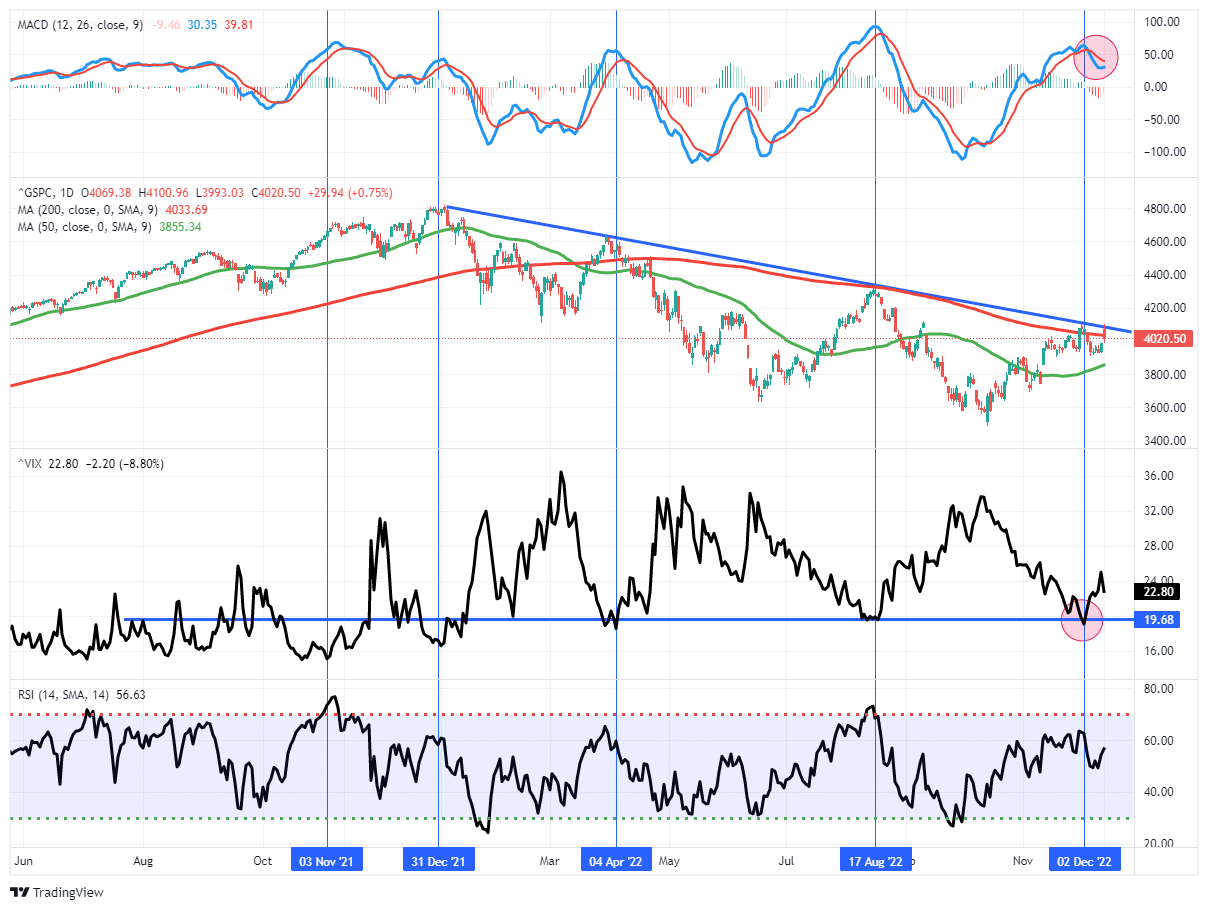

Market Trading Update

The market shot out of the gate yesterday on the softer CPI inflation print. However, the initial surge didn’t last long as markets now realize that the Federal Reserve doesn’t want bullish markets, which eases financial conditions. With Jerome Powell on deck to speak this afternoon, expect a more “hawkish” statement reiterating the Fed will continue to hike rates to bring inflation down to its goals.

Technically, the day’s action was not great. The reversal of the opening spike kept the market below its trend line, and the 200-DMA remains resistance. The good news is the market did clear and hold above the 20-DMA and is sitting on the 200-DMA. That 200-DMA has acted as trend resistance all year, but if the market can turn that into support, a move higher is possible.

The market is not extremely overbought, so there is still room for “Santa” to visit “Broad and Wall” by year-end. The market’s next move, higher or lower, will depend on what Jerome Powell says this afternoon. A “dovish” statement and the market will surge higher. If it’s more “hawkish,” a retest of the 100-DMA is likely.

Buckle up. Today will be interesting.

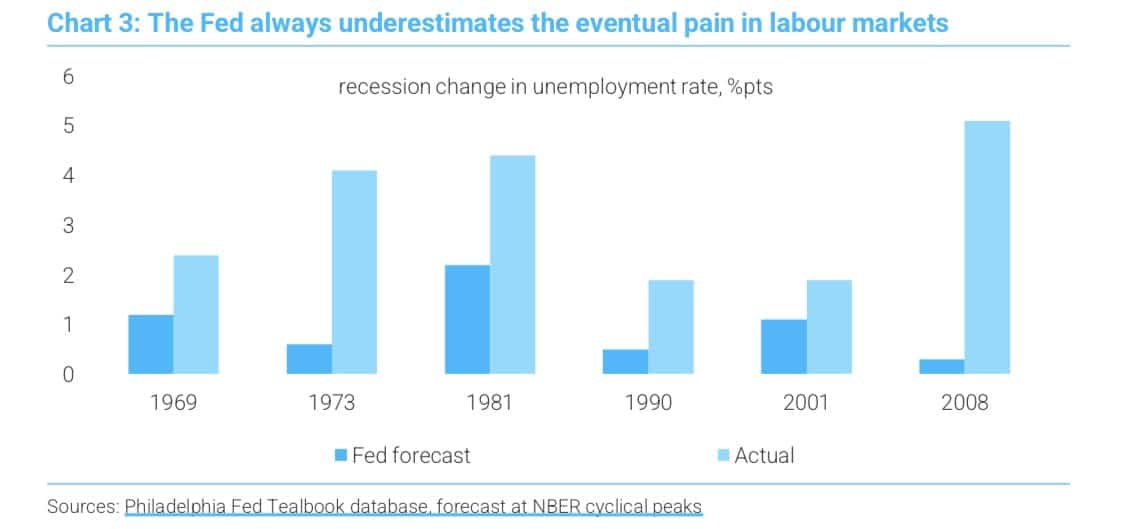

The Fed and the Labor Market

The Fed contends they need to weaken the labor market to bring inflation back to target. Simply, they believe the labor market is too tight. The Fed fears a price-wage spiral, as we have discussed numerous times. We tend to agree with their mindset, but the graph below makes us question their ability to manage and forecast the labor market.

The graph shows that the Fed has grossly underestimated the increase in the unemployment rate in four of the last five recessions. It is quite possible the rate hikes we have already seen, and those still coming, will do more damage to the unemployment rate than the Fed thinks. That said, a jump in unemployment will bring prices lower and possibly below its 2% goal. The Fed has two objectives- full employment and stable prices. Might they have to choose between the two in 2023?

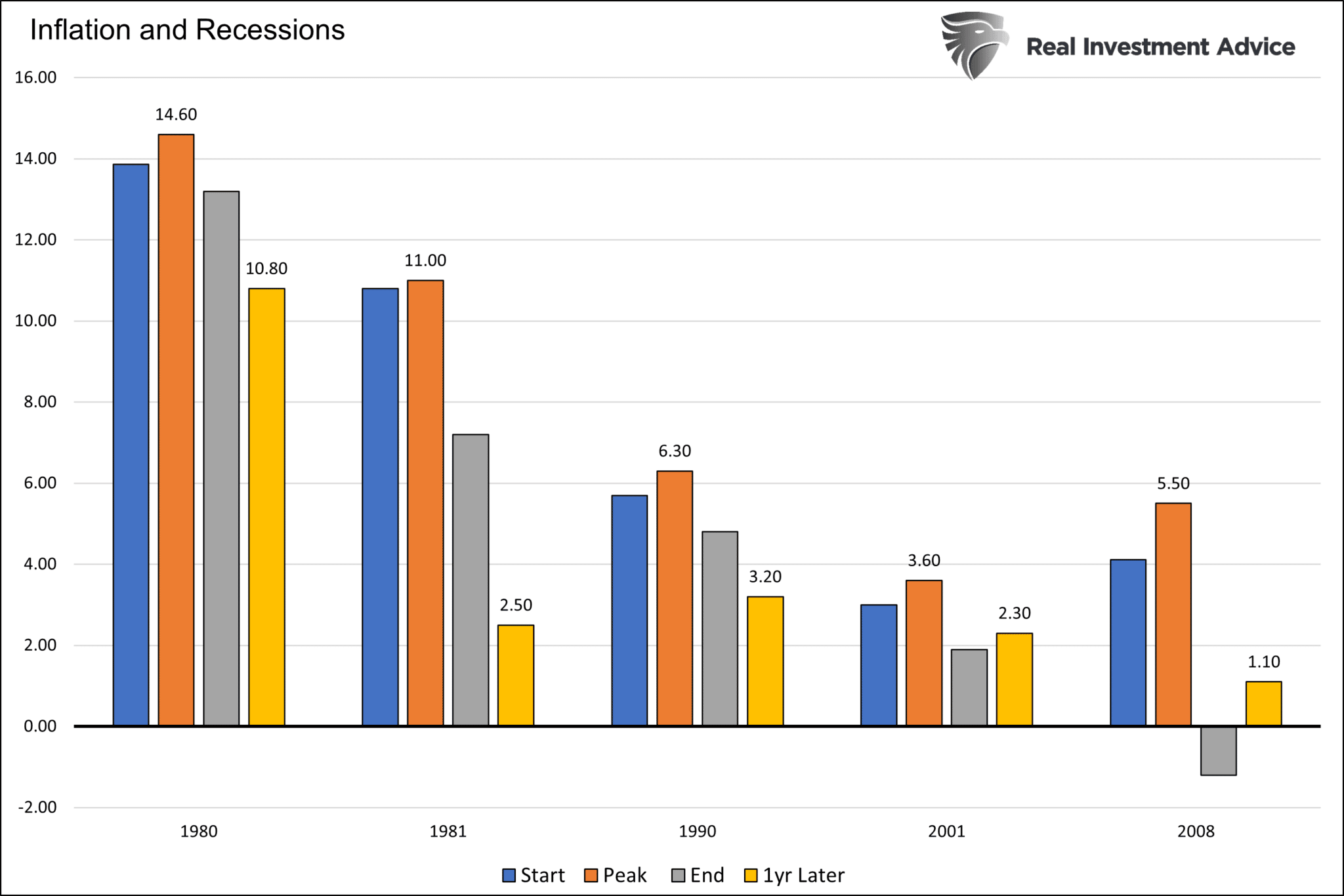

CPI and Recessions

The graph below shows how CPI has reacted during the last five recessions, excluding the 2020 instance. In all cases, CPI peaked after the recession began but fell by the end of the recession and a year after the recession officially ended. Given the massive fiscal and monetary stimulus and the Fed’s aggression to remove monetary stimulus, the 1981 recession may be the model to follow. If it is, inflation will return to the Fed’s target a year after a recession ends. The problem, however, a recession hasn’t started.

Dissecting Inflation

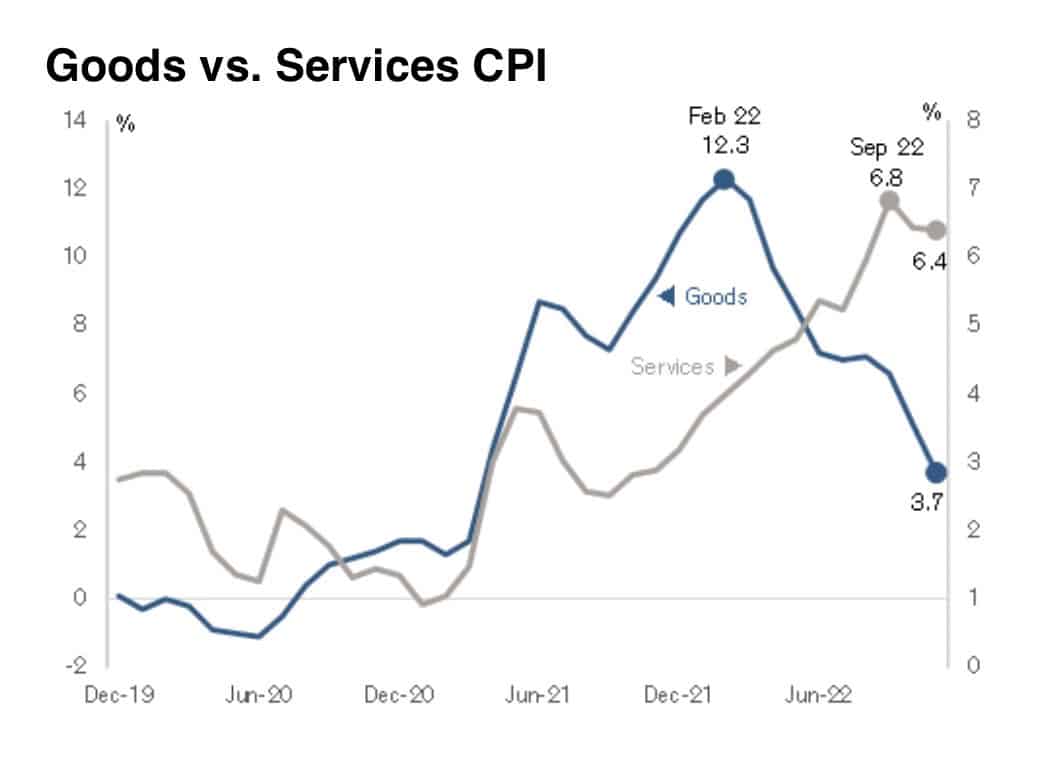

The CPI print was undoubtedly positive, but as noted above, our focus is on how long until inflation falls to levels acceptable to the Fed. Herein lies a problem with yesterday’s data. The graph below compares services inflation to goods inflation. Goods inflation tends to be more volatile, while services inflation is stickier. Economic normalization brings down goods inflation, but services inflation remains near the peak. If we are to get inflation back to the Fed’s objective, services prices will need to follow goods prices. The following quote comes from Credit Suisse.

“It is important to note that today’s results were driven by a precipitous decline in goods inflation from 5.1% to 3.7%, the result of previous pandemic distortions and supply chain challenges.”

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.