Over the last week there have been quite a few questions surrounding IRA contribution deadlines and Roth Conversions. In this week’s piece we thought we’d address those questions here publicly since many of you may be wondering these same things.

When is the cutoff deadline to make IRA contributions for 2019?

This too, just like the tax filing date has been extended until July 15th, 2020.

What amount can I convert from a Traditional IRA to a Roth IRA?

You can convert any amount you would like.

However, for our clients we run a very specific Roth Conversion Analysis detailing the amount that should be converted each year. Roth Conversions are not beneficial for everyone and there is no “one size fits all”. We typically like to extend conversions out over multiple years to minimize the overall tax impact. Depending on age there are other tax considerations that should be considered such as Medicare surcharges and Social Security taxation.

Why would I convert from a Traditional IRA to a Roth IRA?

Distributions from a Traditional IRA or 401k will be fully taxable upon retirement. Distributions on earnings from a Roth IRA are tax free as long as they are considered qualified distributions. We are currently experiencing one of the lowest tax brackets we think we’re likely to experience in our lifetimes and many don’t retire in a lower tax bracket as promised. Now with the additional stimulus packages of the last month, higher taxes are all but inevitable. Having funds in the Roth gives you and your family flexibility in determining the best way to recreate a paycheck in retirement and minimizing taxes.

Traditional IRA’s also must make Required Minimum Distributions at the age of 72 which further reduces the control over how and when you pay taxes. Roth IRA’s are currently under no stipulations and even if they were distributions would not be considered taxable income.

Not to mention the SECURE Act which was passed over the holidays all but eliminated the STRETCH IRA for non-spousal beneficiaries. This means heirs will be required to distribute all funds out of an IRA within a 10-year window, potentially escalating their own taxes and reducing the legacy gift. Roth IRA’s still must distribute all funds within that 10-year window, but distributions will not be taxable.

Why would we take a depressed asset like a stock we own and convert from a Traditional IRA to a Roth IRA?

Let’s assume Joe owns XOM inside his Traditional IRA and that he really likes the company and doesn’t want to sell because inevitably he thinks it will go higher. Exxon closed at $43.13 on Thursday and Joe believes it will get back to its old 52 week high in no time of $83.49. That’s an increase of $40.36 per share. Assume Joe owns 100 shares so that’s an increase of $4,036.

If Joe made a conversion today and converted the XOM stock to his Roth IRA he would owe taxes on $4,313. BUT what if he waited and took a distribution after the stock appreciated back to it’s 52-week high of $83.49? He would owe taxes on the growth of that stock as well and now his tax liability would be on $8,349 if he made a distribution.

Do you think Joe would rather have that growth inside his Traditional IRA account that is fully taxable when he has to make distributions or would he rather have the funds in an account (ROTH) that is completely tax free upon withdrawal assuming he makes a qualified distribution?

This is why we believe you could have a nice opportunity to convert an asset you own (and like) that has gone down and realize that appreciation in the Roth. If you factor in potential higher taxes down the road that argument becomes even stronger.

(This is not a recommendation for XOM, but rather an illustration. We have owned XOM in the past and may in the future)

Do I have to pay the 10% penalty on the conversion if you are under 59 ½?

No, the 10% penalty doesn’t apply to the conversion only ordinary income taxes on the amount you convert.

The new CARES Act allows for penalty free distributions from IRA’s and 401k’s in 2020 with the ability to pay the taxes over the next 3 years. Does this include Roth Conversions?

The CARES Act does allow for individuals to withdraw up to $100,000 in total from retirement accounts without the 10% penalty for those under 59 ½ — if you have suffered financial consequences such as reduced income from COVID-19. It also offers the ability for you to pay taxes on the distribution over a 3-year time frame and gives you the ability to pay the funds back within that 3-year time frame to avoid some or all of the taxes.

The CARES Act allows those who are taking RMD’s the ability to not take them for 2020. Should I reduce or stop my RMD? (RMD: Required Minimum Distribution)

This depends on several factors and I have several thoughts on this strategy, but here’s my main suggestion.

I’m going to assume this individual doesn’t need the funds to live on which I know for many is not the case. If you have other assets you can live on consider a Roth Conversion on the amount you would normally distribute. It may not be the full RMD amount but could work for at least some of your funds. This one is very circumstantial as your current and future income and expenses should be considered as you may be able to avoid additional stealth taxes by not making a distribution or converting funds. I’d recommend you visit with your advisor over the best strategy for you.

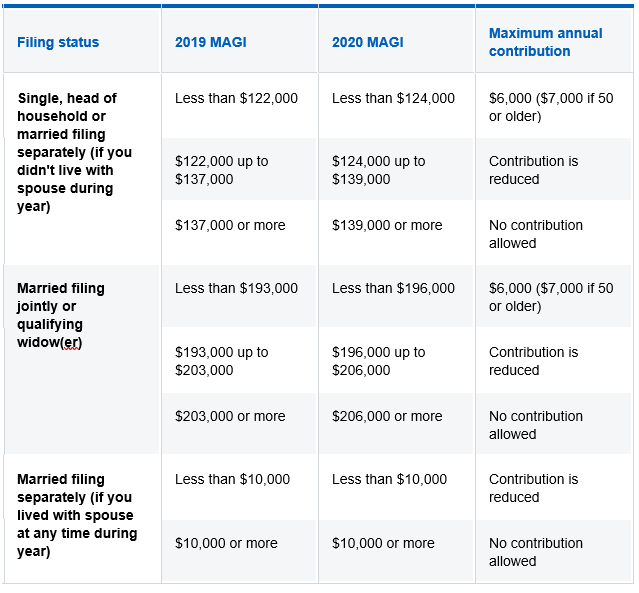

I make too much to contribute to a Roth IRA can I contribute to my Roth 401k?

It’s true, you can make too much to contribute to a Roth IRA (see the chart below,) but there are no income limitations to contribute to a Roth 401k.

Why do you think we’ll pay more in taxes in the years to come?

The government already had a spending problem, but as we at Real Investment Advice try to wrap our head around the enormous amount of stimulus packages and government spending the Fed and Treasury have created over the last month, one thing has become extremely apparent: someone will have to pay for this. Unfortunately, that someone will be you, me and our kids.

Below is a list of all the stimulus over the last month.

- March 6th – $8.3 billion “emergency spending” package.

- March 12th – Federal Reserve supplies $1.5 trillion in liquidity.

- March 13th – President Trump pledges to reprieve student loan interest payments

- March 13th – President Trump declares a “National Emergency” freeing up $50 billion in funds.

- March 15th – Federal Reserve cuts rates to zero and launches $700 billion in “Q.E.”

- March 17th – Fed launches the Primary Dealer Credit Facility to buy corporate bonds.

- March 18th – Fed creates the Money Market Mutual Fund Liquidity Facility

- March 18th – President Trump signs “coronavirus” relief plan to expand paid leave ($100 billion)

- March 20th – President Trump invokes the Defense Production Act.

- March 23rd – Fed pledges “Unlimited QE” of Treasury, Mortgage, and Corporate Bonds.

- March 23rd – Fed launches two Corporate Credit Facilities:

- A Primary Market Facility (Issuance of new 4-year bonds for businesses.)

- A Secondary Market Facility (Purchase of corporate bonds and corporate bond ETF’s)

- March 23rd – Fed launches the Term Asset-Backed Security Loan Facility (Small Business Loans)

- April 9th – Fed launches several new programs:

- The Paycheck Protection Program Loan Facility (Purchase of $350 billion in SBA Loans)

- Main Street Business Lending Program ($600 billion in additional Small Business Loans)

- The Municipal Liquidity Facility (Purchase of $500 billion in Municipal Bonds.)

- Expands funding for PMCCF, SMCCF and TALF up to $850 billion.

The government has also said they will have an open checkbook should the need arise. I’m not here criticizing the Fed’s actions, but rather trying to illustrate the potential need for Roth conversions or finding alternative ways to accumulate savings to further reduce your tax exposure in retirement.

Remember, 401k’s and Traditional IRA’s are not all yours. I want you to look at them as a business partnership, but instead of your traditional business where partners have defined rolls and ownership this business has one caveat. Your partner is Uncle Sam and unlike any other partnership they can change the rules at any time. They can decide to own more of your business, more of your hard-earned funds by raising taxes or changing distribution requirements.

Will that require lifestyle changes for you and yours in retirement? Will this derail your plans?

Last question to address for the week.

On one of our podcast’s we had a listener bring up the notion that we advocate for you to make Roth Conversions because that’s how we make money and we have a product to sell.

First and foremost, if you are a client and your money is in a Traditional IRA or a Roth IRA we are paid the exact same as we operate under an Assets under Management Fee. We do care where funds are because it is our job to take a holistic approach and leave no stone uncovered in finding ways to keep more money in your pocket.

We also already make these considerations for our clients within our Financial Plans, so I would consider it more of a Public Service Announcement of things you should consider for those we don’t work with. These ideas are not exclusive to us, but something every advisor can and should be considering for their clients. These ideas are also not a one size fits all strategy and should be considered and reviewed with your tax advisor.

In regards, to the product we sell. WE ARE THE PRODUCT. Clients hire us for our expertise surrounding portfolio management and financial planning. Our goal is to add additional value to each client and bring them security and piece of mind-especially in these volatile and uncertain times.

Thank you for all of the questions and feedback we receive-Please keep them coming, we’re happy to help!