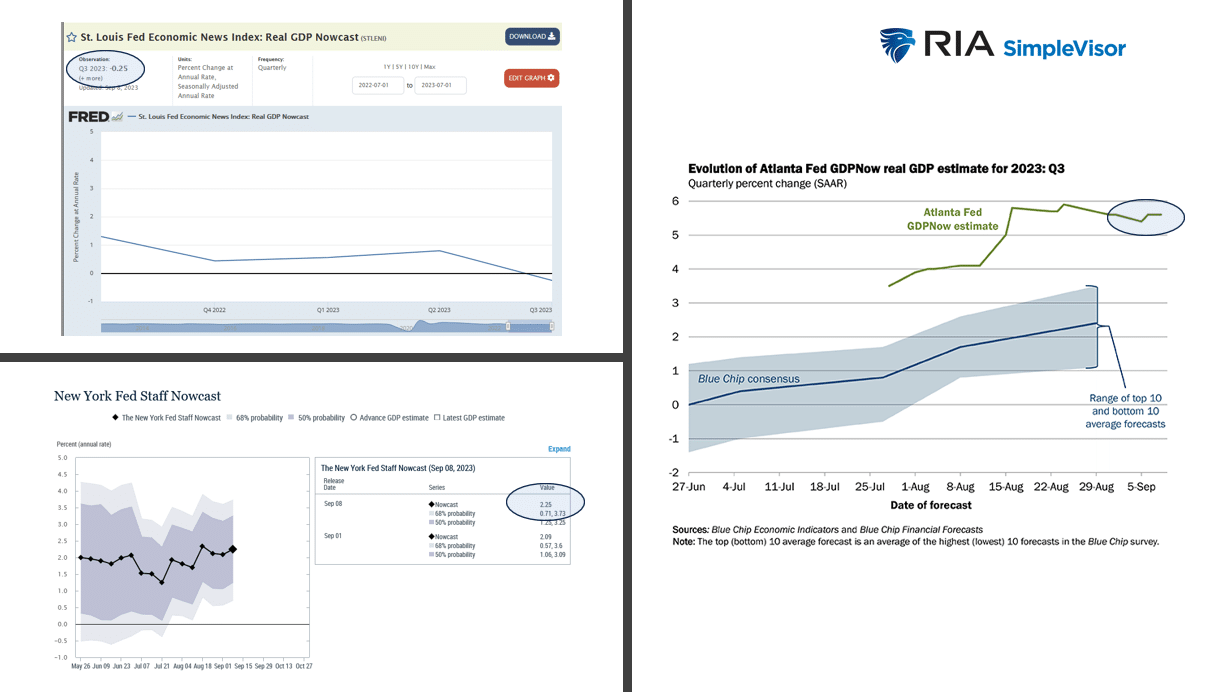

Three Fed branches put out economic forecasts of economic activity throughout the current quarter. These Fed GDP forecasts are called Nowcasts because the Fed branches use current economic data points and not estimates of future data to quantify how GDP is running. The Fed GDP NowCasts tend to be volatile as data and data revisions can significantly impact their predictions. With only a few weeks left in the quarter, three well-followed Fed GDP NowCasts are painting three different economic pictures.

The most followed, the Atlanta Fed’s GDPNow, is shown in the graphic on the right. Currently, it forecasts real GDP is running at +5.6% for the quarter. As shown, its expectation has been in the mid to upper +5% range for over a month. Below their forecast, it shows the Wall Street GDP consensus forecast is below +2.50%. While the Atlanta Fed thinks we are experiencing explosive growth, the St. Louis Fed expects third-quarter GDP growth to be slightly negative. Take theirs with a grain of salt, as they have consistently underappreciated economic growth for the last year. Lastly, the New York Fed expects +2.2% lukewarm GDP growth. We think GDP, barring any economic surprises between now and month’s end, will likely fall somewhere between the Atlanta and New York Fed’s predictions.

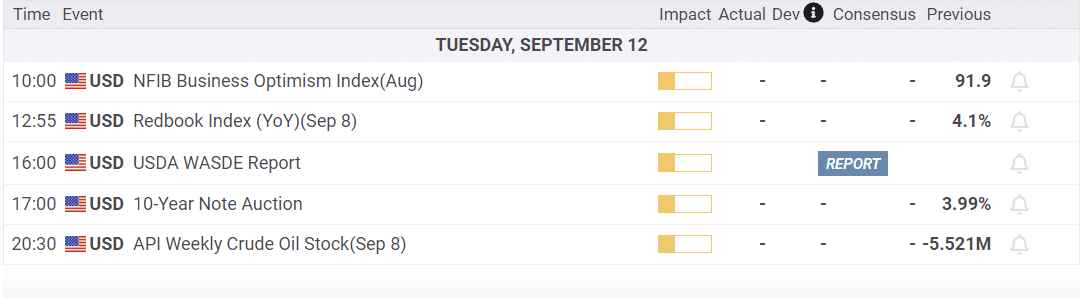

What To Watch Today

Earnings

- No notable releases today

Economics

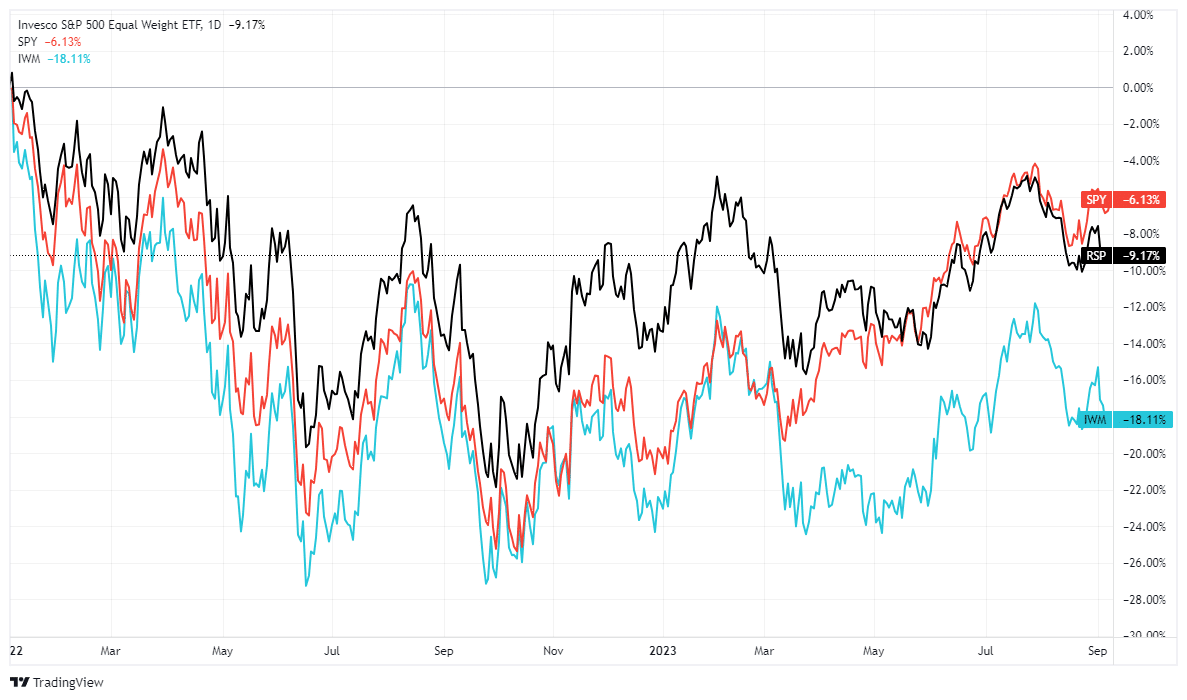

Market Trading Update

While the bulls are certainly prevalent in the financial media, a bit of perspective is needed. Since the beginning of 2022, the S&P 500 Market-Cap Weighted Index is still 6% lower, while the Equal Weighted Index is 9% lower. Given that the S&P 500 has been driven by the advances in the Top-10 Mega-Cap weighted names, the performance is a bit suspect, given the underlying economic strength. That is likely better represented by the Small- and Mid-Cap stocks (we are using the Russell 2000 as a proxy), which remain 18% lower.

Importantly, while the bulls are thumping their chest about this year’s performance, there is an important takeaway that is overlooked.

If you were planning on 6% annualized rates of return to meet your financial planning needs, the problem with making up losses is magnified. While the S&P 500 Market-Cap Weighted Index is down 6% from its peak, your portfolio needs to recover that 6%, plus the 6% you didn’t earn in 2022 AND the 6% for 2023.

This is the problem with most of the analysis that suggests markets AVERAGE 6, 7, or 8% annually. They don’t, and the time lost trying to get back to even is regained.

Be careful about financial projections. They are rarely accurate and explains why 80% or more of the population remains woefully undersaved for retirement.

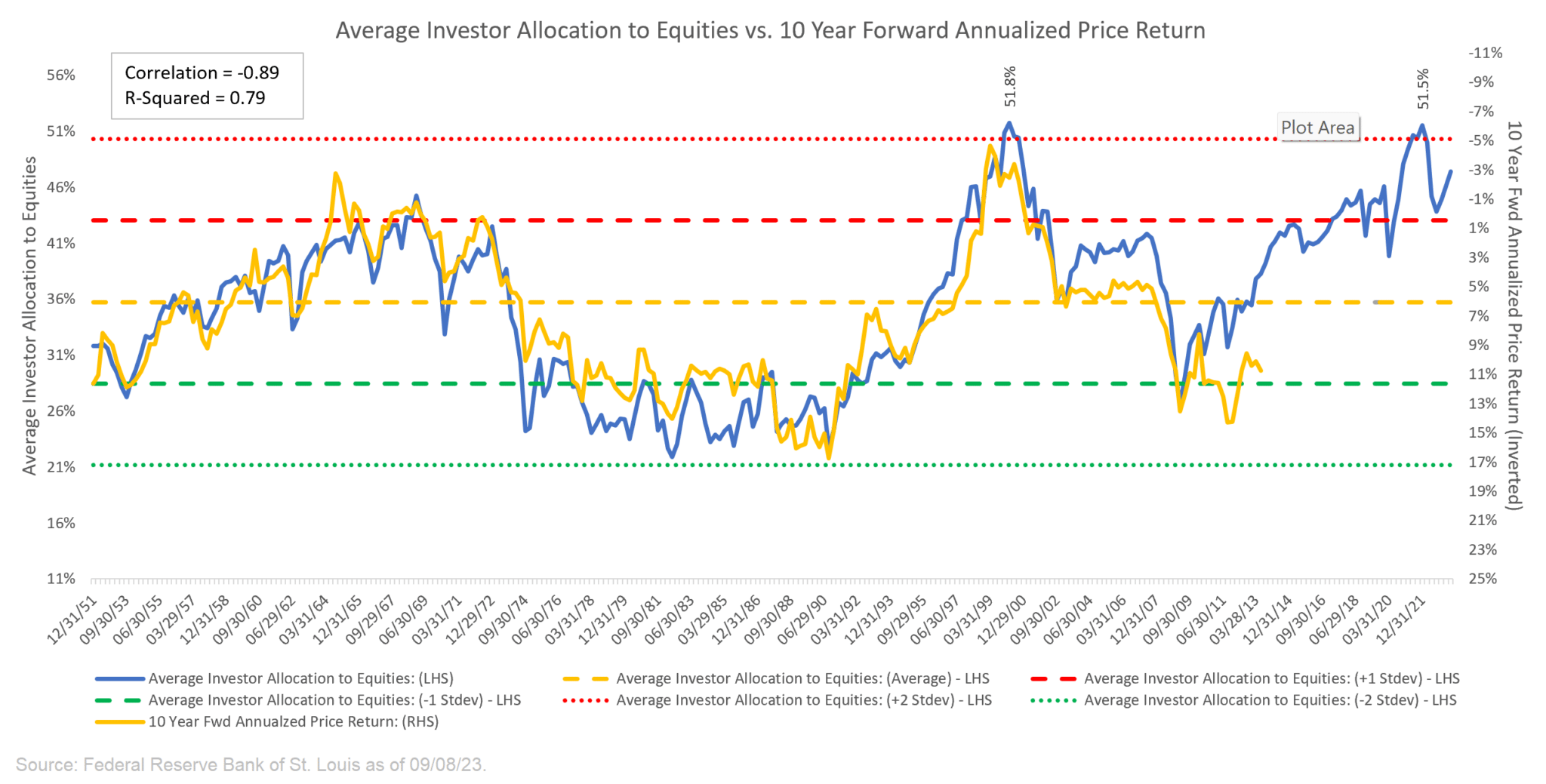

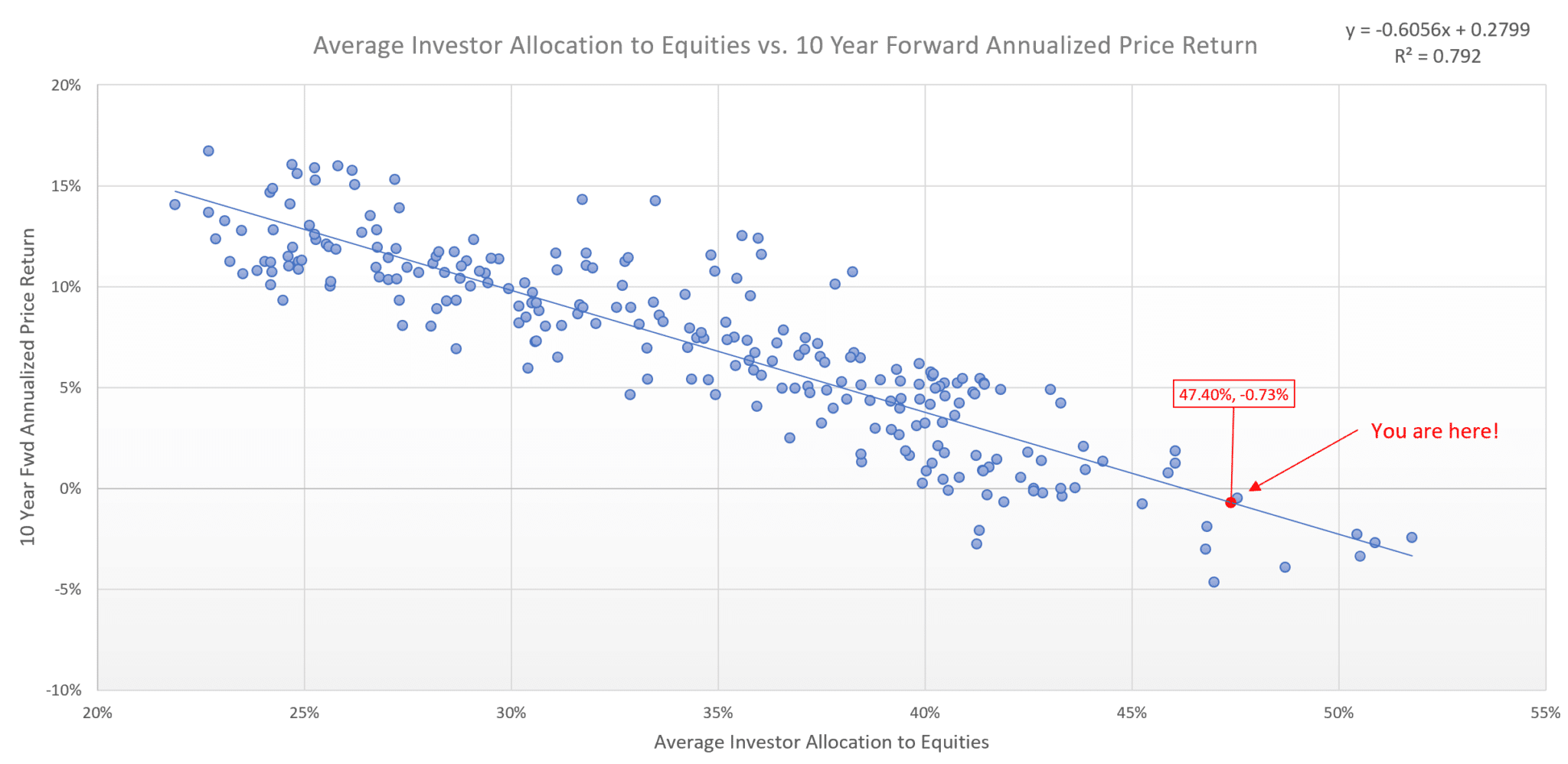

Investor Allocations Bode Poorly For Future Returns

The graphs below from Jim Colquitt’s latest Weekly Chart Review warn that equity returns over the next ten years may be poor. His forecast is based on the robust relationship between investor allocations to equities and the ten-year forward annualized returns for each corresponding allocation reading. Currently, investors are highly allocated to equities. Often, when investors are this bullish, equity market returns tend to suffer. Therefore, if the two lines in the graph below maintain their relationship, we should expect ten-year equity returns to be slightly negative. The scatter plot below the graph shows the strength of the relationship and the return expectations.

With risk-free yields north of 4% for ten years, it may be tempting to sell equities and buy bonds.

However, as Jim cautions:

It is important to remind readers that this does not mean that we should expect a return of approximately -0.73% every year for the next 10 years. Instead, what it means is that over the next decade, we will likely see a market that has very dramatic sell-offs followed by very dramatic rallies which will net out to effectively a return of -0.73% over the next 10 years.

Prospects For Rent Deflation Are Strengthening

Per ApartmentList, rental prices are down 1.2% annually after reaching 18% in November 2021. The second chart below shows similar rental price disinflation according to RealPage. Both actual and imputed rental prices account for about 40% of CPI. Therefore, assessing rental prices is crucial to getting CPI forecasts correct. Therefore, as we have written, CPI rental prices tend to lag real rental prices by half a year or even longer. Ergo, the actual rent disinflation/deflation may not show up in CPI until 2024.

The recent price trends may continue based on the coming supply of apartment buildings. The first graph below shows that multi-family housing construction is at an all-time high. This should continue to put a lid on rent prices and possibly be outright deflationary. So, if almost half of CPI is flat to negative, the remaining 60% has to run at 4% to get inflation to the Fed’s 2% target. The third graph shows CPI less shelter is running at 1% annually. Consequently, even if other prices rise a little, as we are seeing, it’s hard to imagine that CPI inflation won’t fall as CPI-computed rent prices catch up with reality.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.