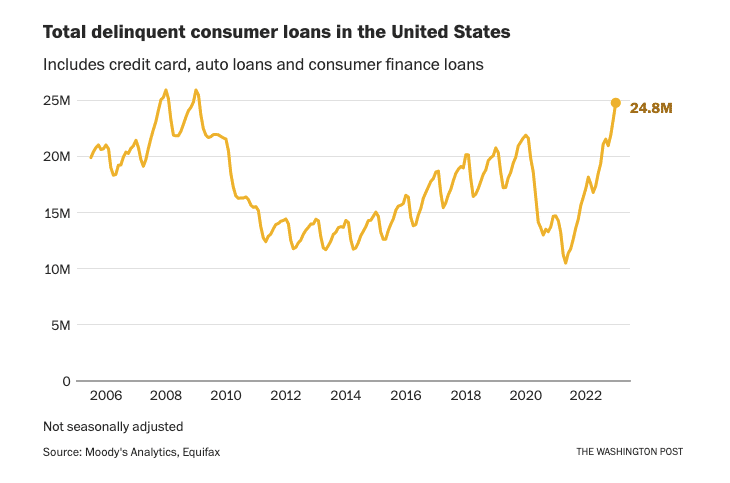

The chart below showing delinquent consumer loans is concerning but misleading. At first blush, the number of delinquent consumer loans is nearing the peak of the 2008 recession. That stat should be very worrisome on its own. However, the amount of consumer loans has more than doubled since 2008. Therefore, the percentage of delinquent consumer loans is only half of the 2008 peak.

While the percentage of delinquent consumer loans is not problematic, the sharply rising trend is. Further, Heather Long of the Washington Post notes, “Many households are also behind on their utility bills: 20.5 million homes had overdue balances in January, according to the National Energy Assistance Directors Association.” Per the article, the bottom 60% of earners contribute about 40% of GDP growth. People delinquent on loans are likely getting financially squeezed due to falling real wages and will be forced to reduce their consumption. If the unemployment rate rises, the problem will worsen. The article ends as follows: “The flares are going off. If the economy does fall into a recession, it will only get more perilous for those at the bottom.“

What To Watch Today

Economy

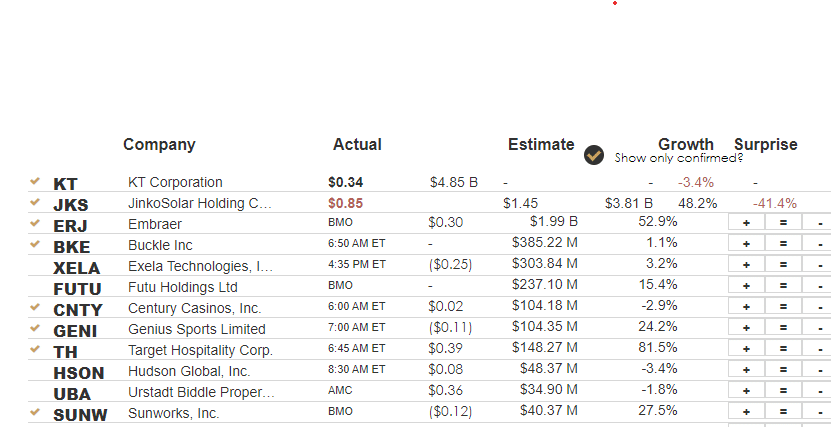

Earnings

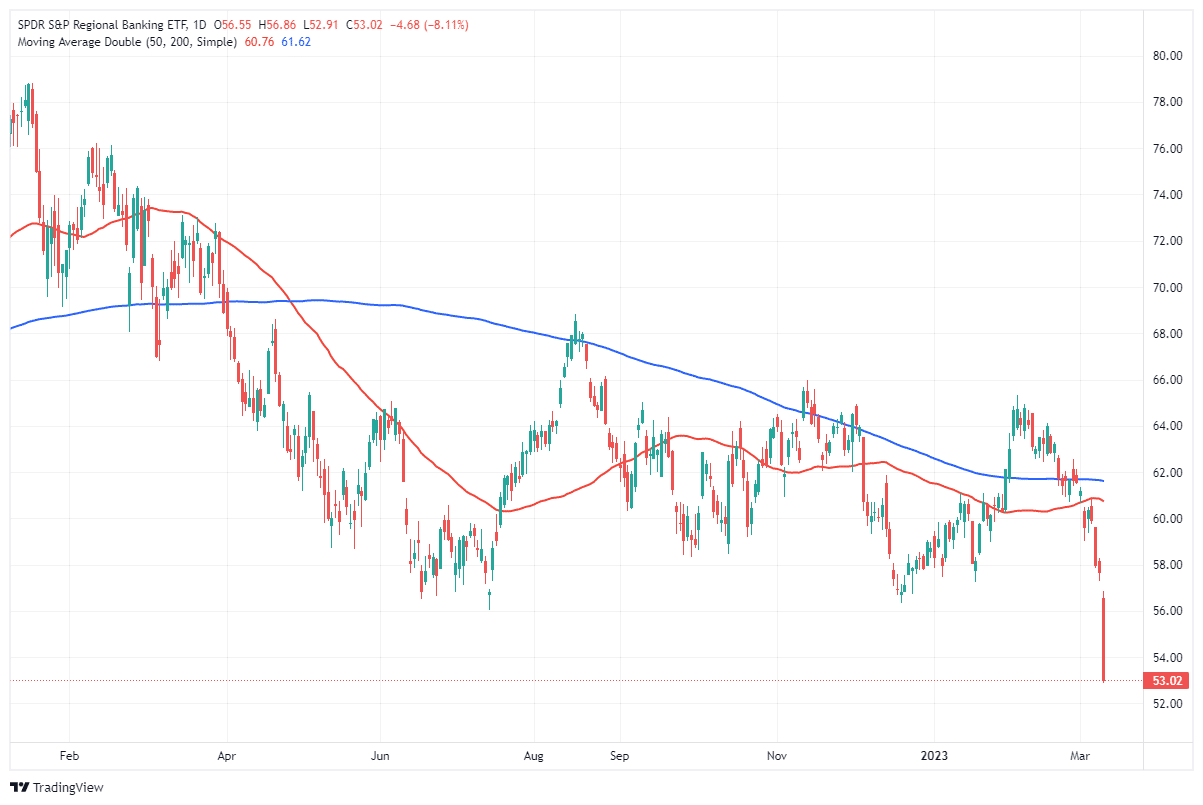

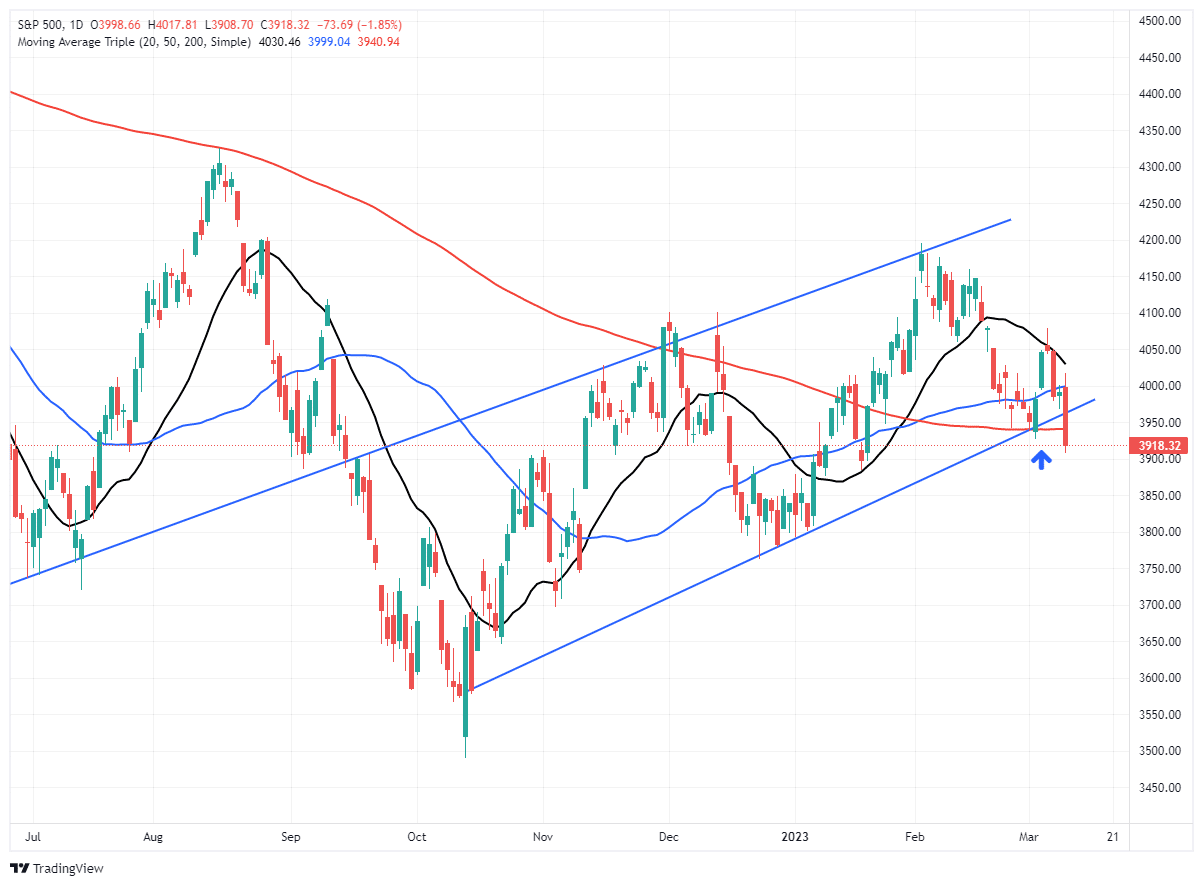

Market Cracks Important Support

Yesterday, news that SVB Financial Group was taking “steps to bolster its financial position.” That included a highly dilutive stock offering and a panicked asset sale that sparked fears of a liquidity crisis at one of the biggest and original funding providers to the Venture Capital industry. The fear spread through other regional banks as a concern of “one roach in the kitchen” may mean a lot more at risk. The ETF of Regional Banks (KRE) dropped sharply.

The crack in regional banks is likely only just starting as the Fed continues to hike interest rates, leading to more underperforming loans and reduced funding. Unlike the big banks, which have access to capital markets and trading revenues to offset traditional banking incomes. smaller banks have a lot of exposure to real estate, particularly commercial.

“Banks – and especially small banks – are now sitting with reserves pretty much at their lowest comfort level, There is not much of a cash-to-asset cushion left for small banks as a whole, so a funding crisis can easily get rolling if large depositors decide too many loans in commercial real estate and other areas are about to go bad. The Fed will make funds available to keep these banks afloat, but that alone will get some push-back from Congress because of the increased concentration of bank deposits in an increasingly smaller number of banks.” – Steven Blitz, TS Lombard

With that, the market dropped about 1.85% yesterday as concerns of a contagion spread through the financial sector, and given its large weight in the index, contributed to the selloff.

Today is critical for the markets to muster a bit of a reflexive rally to retake the broken trend line and the 200-DMA, which is key support. The selloff yesterday also kept sell signals intact. A weaker-than-expected employment number could provide a lift if the bulls get any data to support the hope of a “pivot” by the Fed.

Today will be a critical test of broken support. Stay tuned.

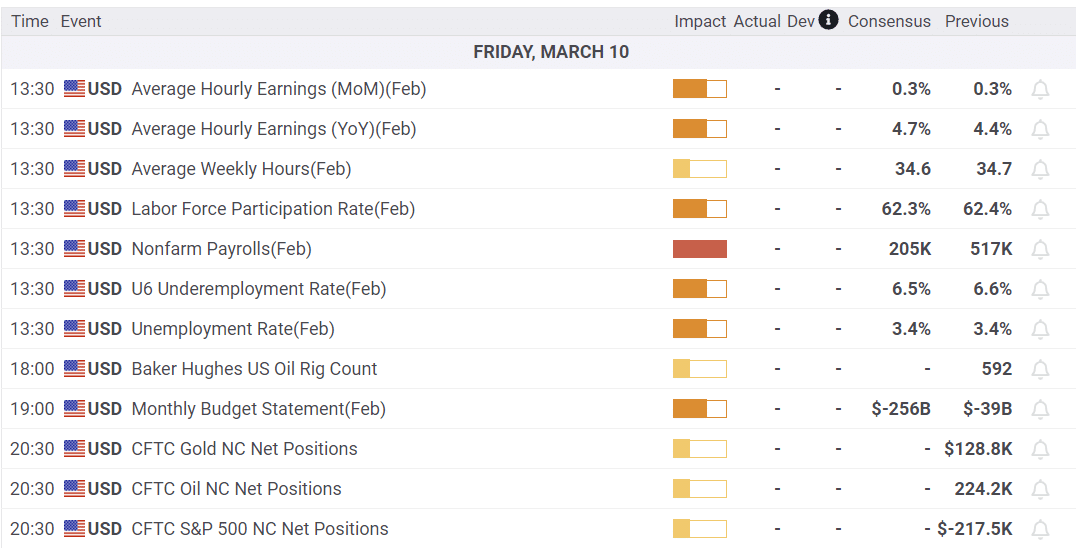

Employment Preview

On Wednesday, ADP and the JOLTs report gave investors a preview of what to expect in this morning’s BLS labor report.

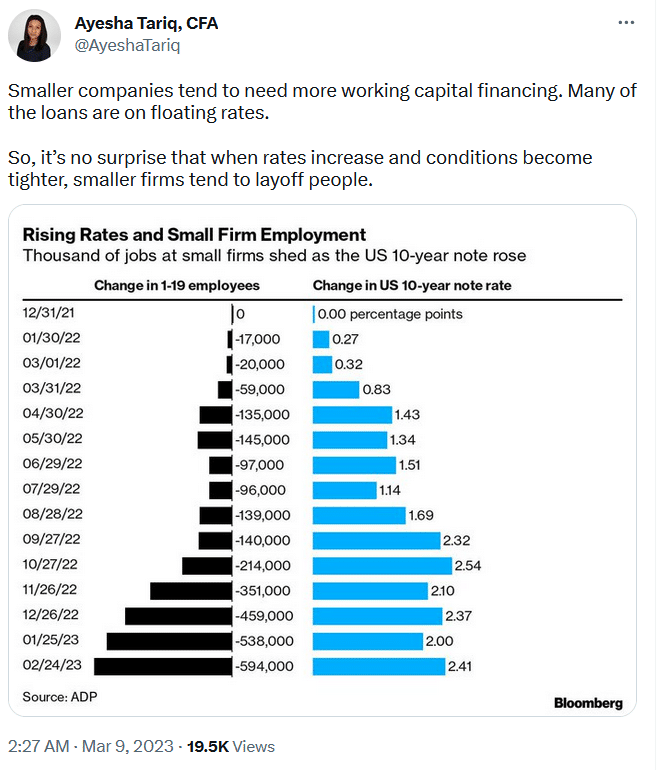

ADP reported payrolls grew by 242k, more than double last month’s +119k and estimates of 200k. Small businesses lost employees, while large ones added jobs. Today’s Tweet of the Day, shown below, sheds light on why small business employment continues to decline while employment is generally rising for midsize and large companies. Once again, the leisure and hospitality sectors added the most jobs. ADP wage growth showed a year-over-year gain of 7.2%, .10% below last month’s level, but likely way too high for the Fed’s liking.

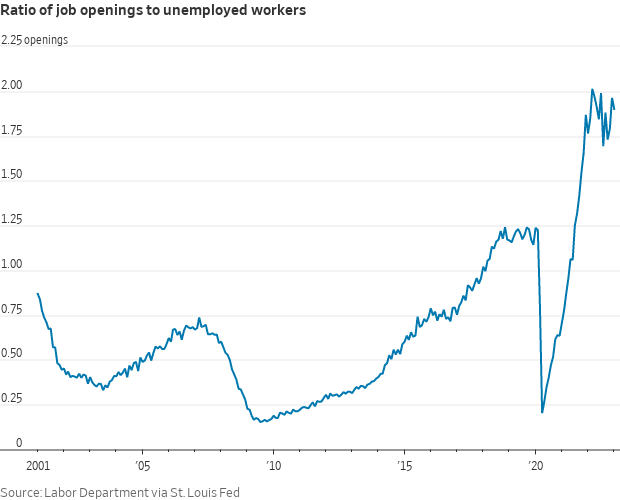

JOLTs showed similar strength but contained concerning data points. The number of job openings fell from 11.234 million to 10.824 million. The graph below shows that the ratio of job openings to unemployed workers remains well above the levels of the last 20 years.

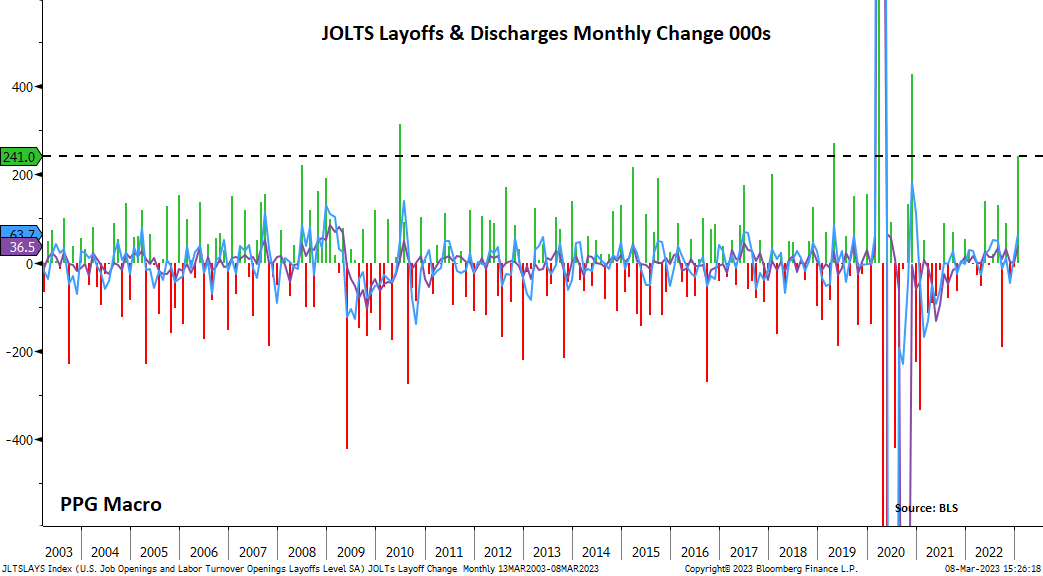

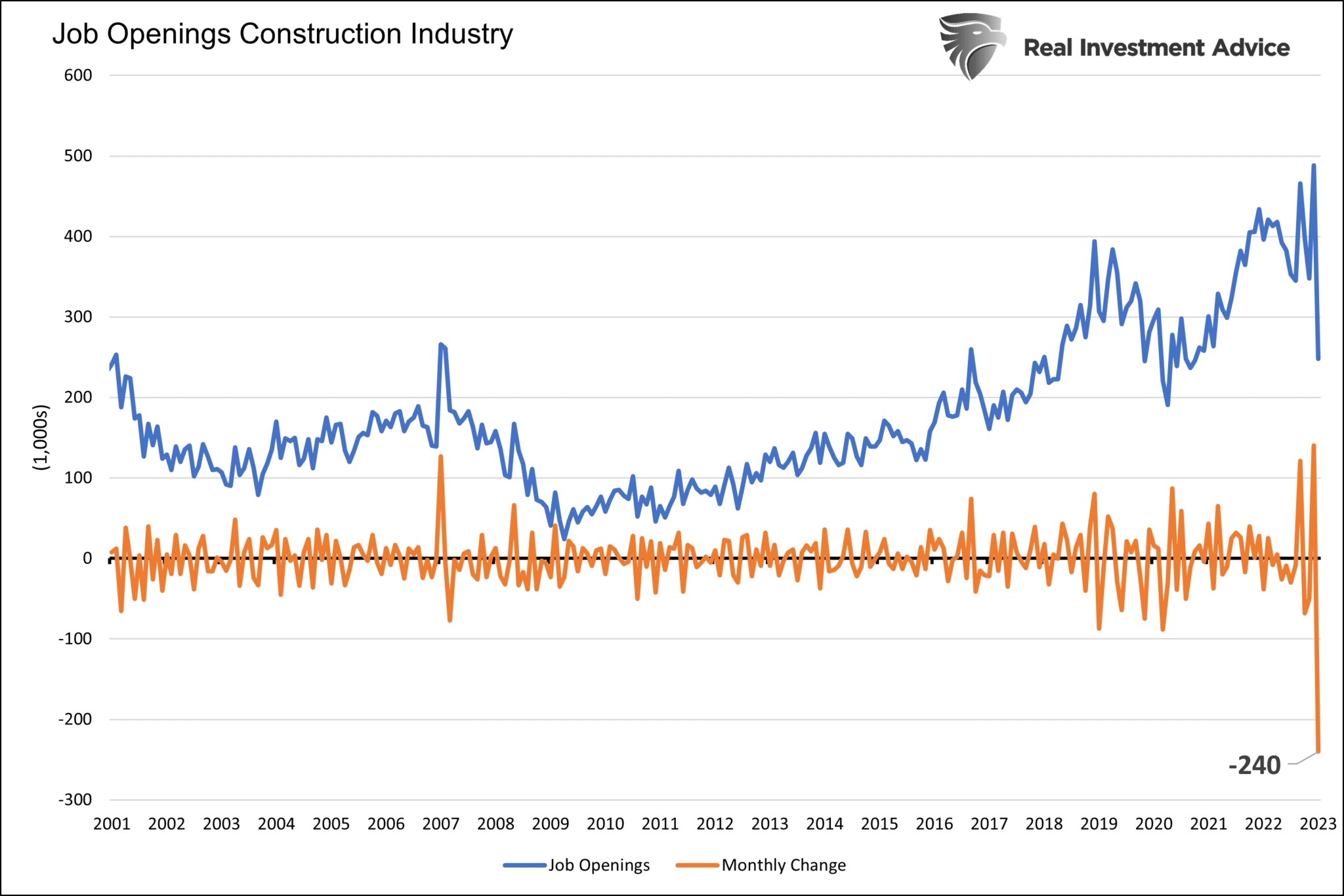

Of concern, 241k people were laid off last month. That is the fourth-highest monthly increase in 20 years. Also worrisome, construction job openings fell by 240k. The third graph below shows that last month’s decline in construction job openings is almost three times larger than the second-worst decline in the last 20 years. Construction employment usually leads the broader labor market because it is very interest rate sensitive. Might the interest rate hike lag finally be catching up to the economy? Keep an eye on the construction employment in today’s BLS report.

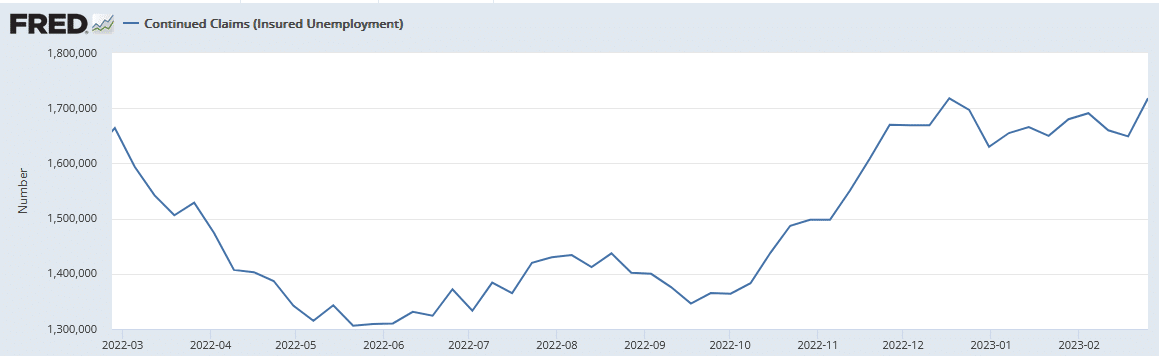

Continuing Jobless Claims

Continuing jobless claims is the number of people that filed initial jobless claims but unable to find a new job. Increasing continuing claims is often a leading indicator of weakness in the labor market.

Continuing claims rose this week to 1.718 million from 1.649 million. The matches the high we saw in mid-December. One number does not make a trend. But, if continuing claims continue upward, we should expect the unemployment rate to increase.

The graph below shows that continued claims match their highest level in over a year. However, today’s data is only on par with pre-pandemic levels.

Will Economists Come Up Short Again on Payrolls?

The graph and tweet below point to the amazing streak economists have had in underestimating the strength of the labor market. After reporting 517k new jobs last month, will today’s 223k estimate be short again?

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.