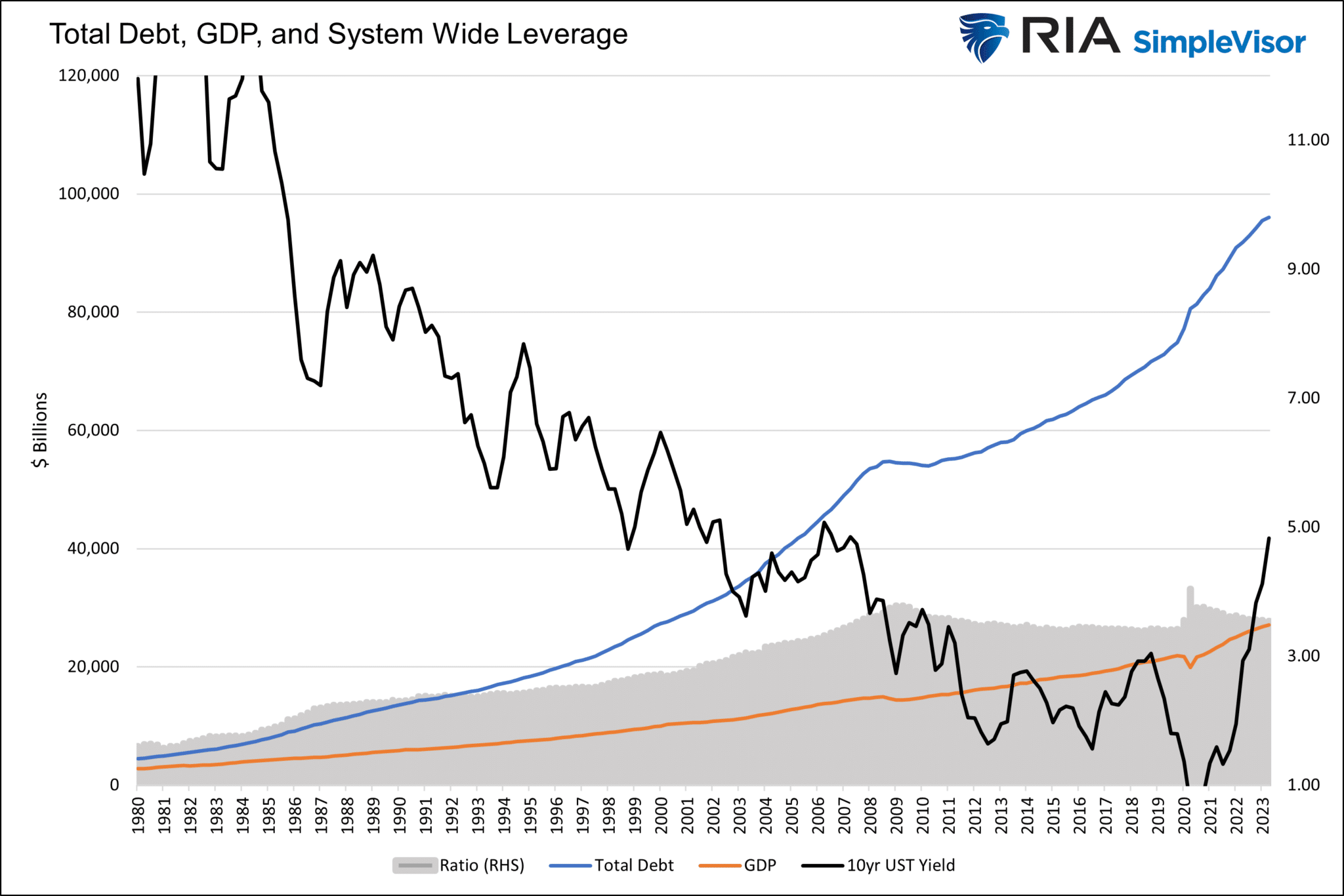

The growth of the global economy and the value of the world’s financial assets are a function of interest rates. Interest rates are the cost of money. The cheaper money gets, the more investments into all sorts of assets make sense. Politicians and central bankers clearly understand this relationship. As we have seen since the Fed was formed, when economic growth is insufficient, they reduce interest rates and make money cheap. Low-cost financing incentivizes consumers to buy cars and houses, businesses to build factories and purchase equipment, and governments to spend more while reducing taxes. Equally important, cheap money allows investors to leverage up their investments, making their potential rewards even greater.

As interest rates steadily decline, the financial and economic incentives to borrow further stimulate the economy and financial markets. Think of cheap money as a virtuous cycle. The problem is the economy and financial markets are now reliant on cheap money. Today, the Fed and bond markets are rapidly extracting that fuel from the economy and markets. Like all other instances when the Fed Fed raised rates, this, too, will likely end in a crisis. The cost of money is too important to the economy and politicians’ economic goals to sustain at current levels for much longer. The graph below shows lower interest rates have led to more system-wide leverage.

What To Watch Today

Economy

Earnings

Market Trading Update

The market sold off yesterday morning but rallied back into Jerome Powell’s comments. It then sold off, then rallied, then sold off…what a roller coaster. Initially, the message from Powell was dovish, confirming what other Fed speakers had said all week. To wit:

“Financial conditions have tightened significantly in recent months, and longer-term bond yields have been an important driving factor in this tightening. We remain attentive to these developments because persistent changes in financial conditions can have implications for the path of monetary policy.”

However, his hawkish comments spooked the stock and bond markets, suggesting that the inflation risk remains near term until the economy slows.

“Additional evidence of persistently above-trend growth, or that tightness in the labor market is no longer easing, could put further progress on inflation at risk and could warrant further tightening of monetary policy. In any case, inflation is still too high, and a few months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal.”

None of this is “new” news, but traders reacted negatively to the comments. We suspect they will calm down and realize that nothing has changed since the last meeting, and the Fed will remain on hold at the next meeting.

The break of the 20-DMA sets up a potential for a test of 4200, and today is options expiration, which potentially increases the risk of a volatile trading session. Continue to manage risk for now, but be careful making significant changes on an OpEx day. Most likely, much of the noise will filter out by early next week.

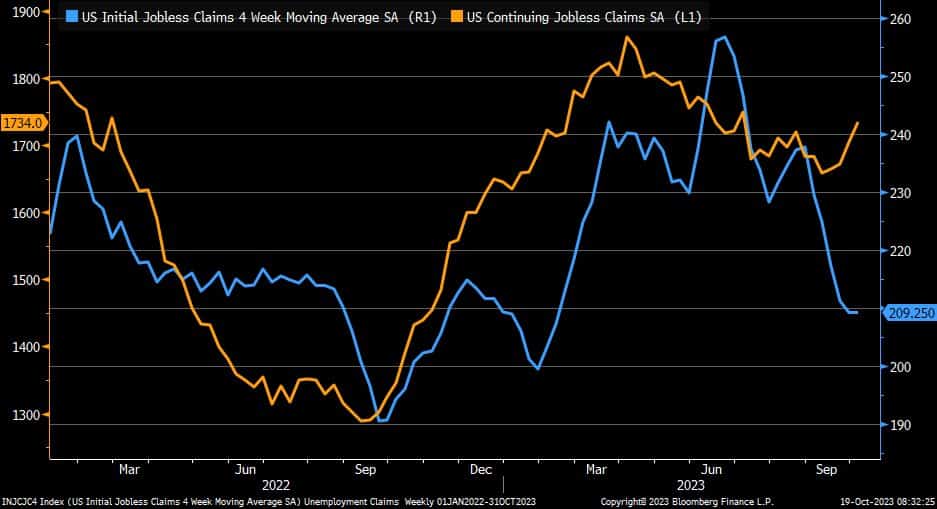

Jobless Claims Fall, But Continuing Claims Rise

The number of people filing initial jobless claims weekly hovers around historical lows. However, continuing joblessness has started rising. The divergence signals that those filing for claims are not finding employment as quickly as they were. The sheer number of those in the continuing claims ranks is not concerning, but rising continuing claims often lead to increased jobless claims.

As the graph below shows, continuing claims reached their highest level since June. Further data for continuing claims lag jobless claims by one week. Again, this is not a concerning data point, but if the trend continues, jobless claims will likely follow.

Jerome Powell Follows The New Fed Mantra

As we have written a couple of times in the last few days, the Fed is moving towards a more dovish stance. It appears that orchestrated statements from numerous Fed members alluding to the financial tightening due to higher long-term rates will keep the Fed on the sidelines. Powell followed in their footsteps with the following comment:

Financial conditions have tightened significantly in recent months, and longer-term bond yields have been an important driving factor in this tightening. We remain attentive to these developments because persistent changes in financial conditions can have implications for the path of monetary policy.

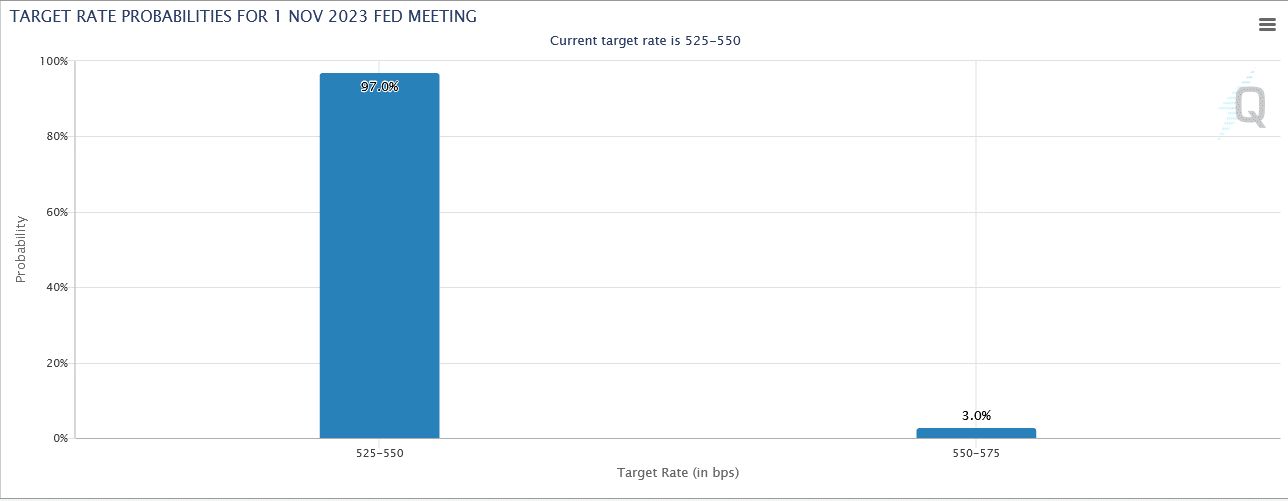

While the Fed seems to be moving to a more dovish stance, Powell doesn’t leave any doubts that 2% is his inflation target and the Fed will do whatever is needed to get there. The graph below shows the market assigns a small 3% chance the Fed tightens at the coming meeting.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.