Higher energy prices worrying you? Be afraid because Congress is coming to the rescue. Legislators are introducing a new bill called the “Big Oil Windfall Profits Tax Act.” The bill’s objective is to reduce the price of oil. The bill pans to tax the windfall profits of large energy companies at a 50% rate. They define windfall profits as profits above and beyond those in the year before Covid. The proceeds from the tax would be returned to consumers earning less than $75k through direct payments.

If Congresses goal is to inflate oil prices further and generate more inflation in the process, the bill, as currently written, is right on track. This article walks through the proposed legislation to better understand why it is grossly flawed. As we will discuss, the bill will not only generate higher prices at the gas pump, but the premise behind the bill, windfall oil profits, is dubious.

But first, it is worth looking beyond Russia’s effect on energy prices and reviewing another reason oil prices have been rising.

The Supply Side Backdrop

In High Gas Prices and Recessions, we discussed how the push toward Green Energy is resulting in oil supply shortfalls. To wit:

“Energy companies and their customers are increasingly under heat to reduce their carbon footprint. Assuming the push toward green energy continues, oil executives must carefully consider new long-lived projects not only from an environmental perspective but from a profit perspective. Higher taxes on oil and oil exploration and increasing sources of green energy will potentially make future drilling less profitable. Unknowns such as these result in a lack of investment into the oil infrastructure.”

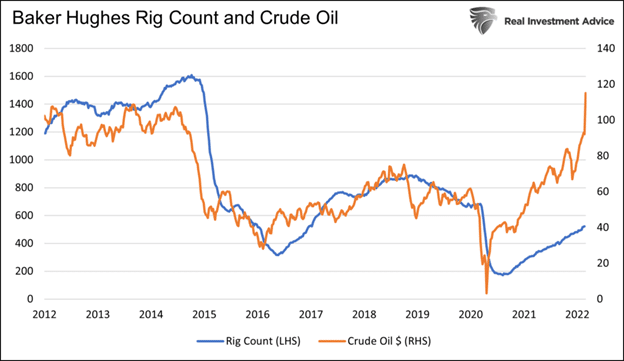

Shown below is evidence that energy companies are holding back on new investments. The chart compares the number of oil rigs in operation and oil prices. If you notice, the rig count has only modestly improved since the Pandemic, yet the oil price is much higher. We should expect the rig count to be at least twice current levels based on the past.

The following quote from CNBC provides a little more context to the growing shortfall of oil: “investment in new wells has dropped 60%, causing U.S. crude oil production to plummet by more than 3 million barrels per day or nearly 25%.”

Yes, the Russian invasion of Ukraine is temporarily pushing energy prices higher. Still, the more concerning longer-term problem is the lack of a lucid transition plan from carbon-based energy to greener energy sources.

Further Disincentivizing Oil Production and Exploration

With that base macro understanding of why the supply of oil supply is and will be compromised, we can now consider how energy companies will react if the new bill passes.

The bill disincentivizes energy companies to explore for oil and drill new wells. Exploration is expensive and can often result in losses. Now throw a 50% profit tax into their decision-making, along with more confirmation of Congressional attitudes toward “big oil”, and we must assume they will be even less likely to explore for new oil.

Similarly, some energy companies may shut down current operating wells that are not profitable enough with the tax.

Even if the bill is not passed, it further cements the rationale to reduce investment into exploration and current drilling operations. Their fear of future government actions against them is further affirmed.

The bottom line is that even though oil prices are high, the supply of oil and investments into production and exploration will fall further because of the bill.

More Inflation

As the bill is currently written, the proceeds from the tax are to be returned to consumers earning less than $75k through direct payments.

One of the primary reasons for the current bout of inflation is the massive pandemic fiscal stimulus programs. Unlike other periods of fiscal stimulus, the most recent sent checks directly to the public. As we saw, consumers spent this money. The extra consumption and compromised supply line problems is resulting in the greatest rate of inflation in over 40 years.

Should we expect it to be different this time?

What Windfall Profits?

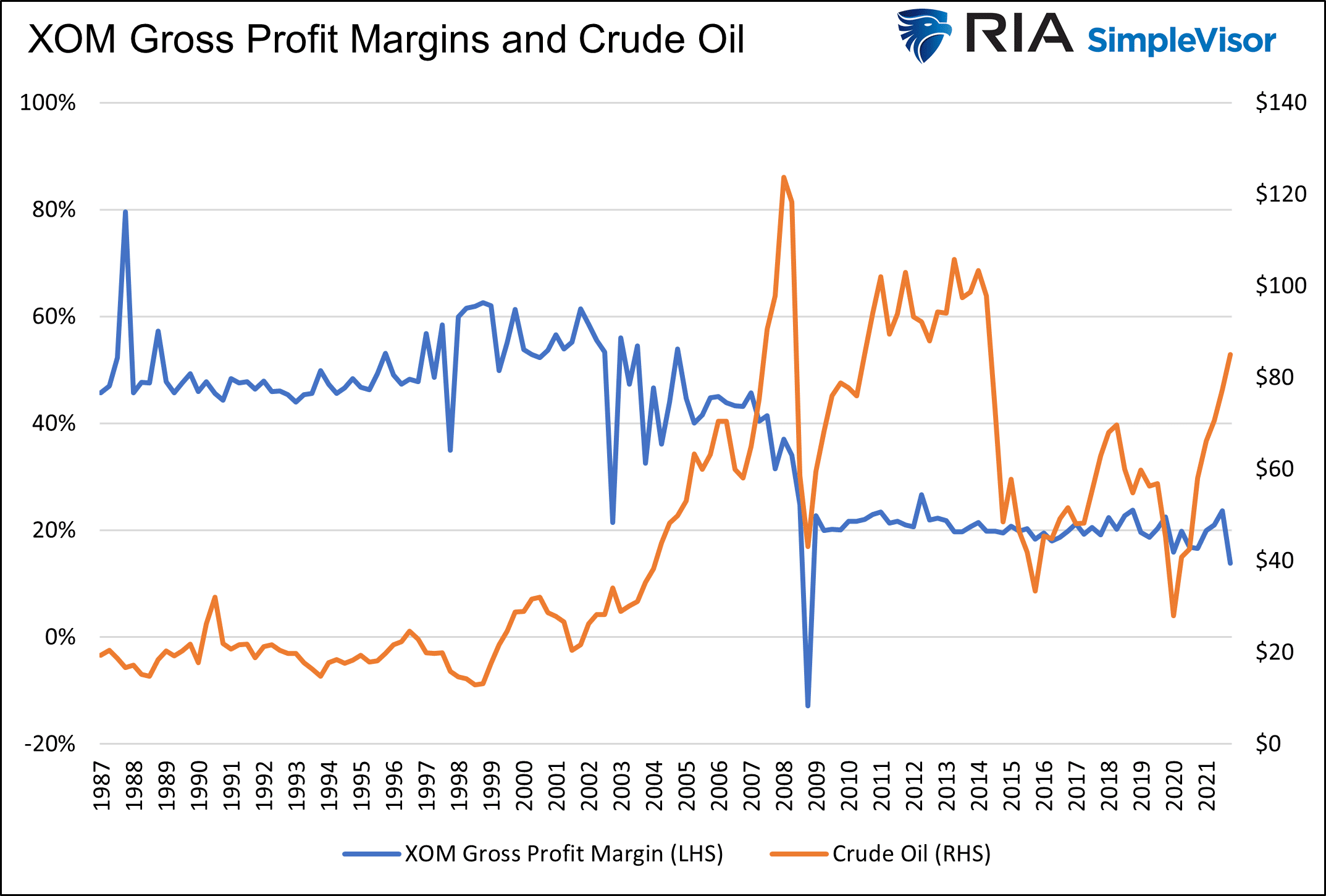

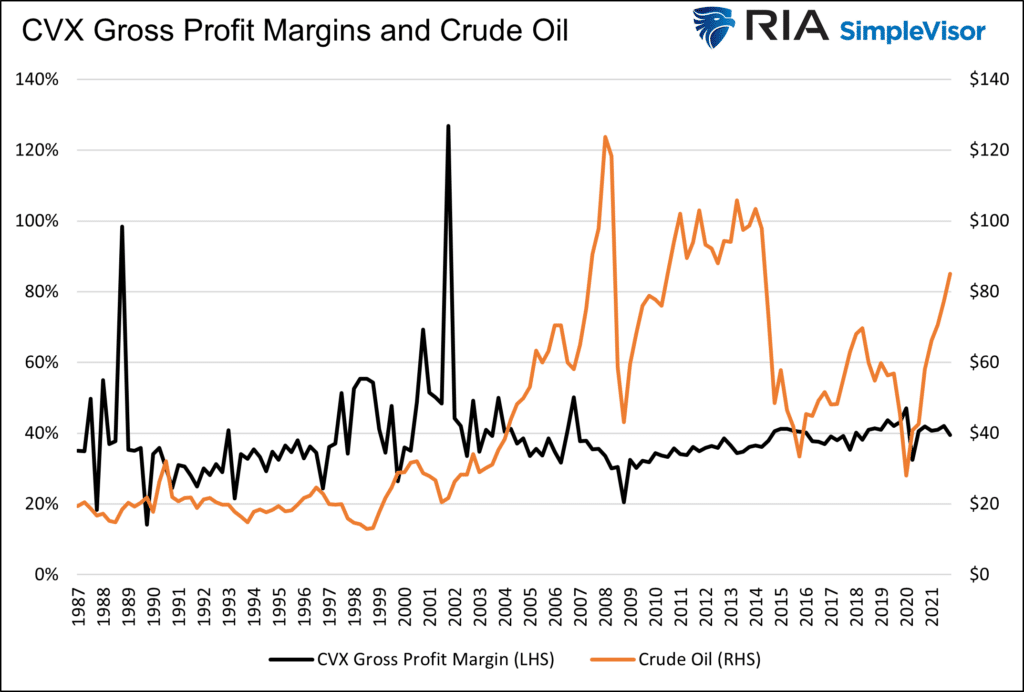

The other problem with the bill is the premise that large energy companies are profiting from the recent spike in oil prices. Below we share data comparing the gross profit margins of Exxon (XOM) and Chevron (CVX) versus the oil price. The definition of gross profit margin is gross profits divided by total sales. This measure eliminates most other expenses and helps us better assess how sales affect the bottom line.

As both graphs highlight, there is little to no correlation between profit margins and oil prices. Exxon’s profit margin rose in the second quarter of 2020 when oil prices fell to a negative $35 a barrel!

Energy companies hate volatility in oil prices because shareholders pay up for predictable profits and growth. To limit earnings volatility, all energy companies lock in future prices via contracts with buyers to sell oil in the future at specific prices. They also hedge with oil futures to further manage oil price volatility. The graphs above show both companies have significantly reduced the volatility of margins over the last 20 years.

Summary

The Windfall Profits Tax Bill doesn’t truly penalize energy companies. It punishes consumers with more inflation. Further, it uses a faulty assumption to help gain support from the public.

If passed, the bill will likely further amplify the growing divergence between the supply and demand for oil. The proceeds may initially help the lower-income classes but ultimately hurt them with more inflation.

Other than those in Congress seeking to boost their reelection odds, we are unsure who this bill benefits.