ZeroHedge published an article I found interesting called “For Silicon Valley’s Startups, The Bill Is Finally Coming Due“:

Silicon Valley startups like Hustle, an ad-messaging company that spent lavishly on things like on-tap kombucha and arcade games for employees, are learning the hard way that party is coming to an end and the bill is finally due. Earlier this month, the company announced mass layoffs according to the WSJ . This depressing scene is now playing out across countless Silicon Valley startups, which sprung up like mushrooms when the money was easy and which are now starting to fold as the decade-long credit cycle tests the limits of the current bubble.

Startup investors and company founders warn that the unchecked growth of the past several years—which by some metrics exceeded heights from the dot-com boom—is hitting a limit. A rout of publicly traded technology companies is fostering newfound restraint for investors in Silicon Valley, especially for younger, cash-strapped startups like Hustle.

Startup investor Sunny Dhillon told the WSJ: “The unbridled optimism that inhabits our world is getting a shot of realism.”

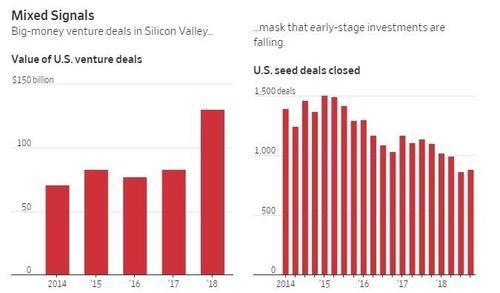

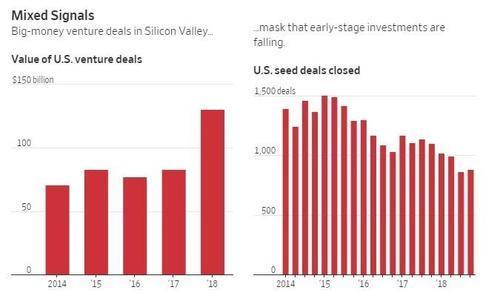

To be sure, the warning signs were easy to spot, starting with the shrinking number of seed deals, which fell to just 882 in Q4 versus more than 1500 that took place three years ago.

Because VCs have a tendency to follow technology stocks, the NASDAQ’s recent 12% pullback from its Sept 2018 highs put pressure on many startups: scooter companies Bird Rides and Lime both had to lower their valuation targets in order to raise capital during their last funding round. Other startups are failing outright, like Munchery, a meal kit service that had raised more than $100 million from VCs.

The latest events in the Silicon Valley startup world confirm the warnings I made a few months ago in a piece called “The Startup Bubble Is A Derivative Of The Stock Market Bubble”:

The world has gone completely startup crazy over the last several years. Spurred by soaring tech stock prices (a byproduct of the U.S. stock market bubble) and the frothy Fed-driven economic environment, countless entrepreneurs and VCs are looking to launch the next Facebook or Google. Following in the footsteps of the dot-com companies in the late-1990s, startups that actually turn a profit are the rare exceptions. Unfortunately, today’s tech startup bubble is going to end just like the dot-com bubble did: scores of startups are going to fold and founders, VCs, and investors are going to lose their shirts.

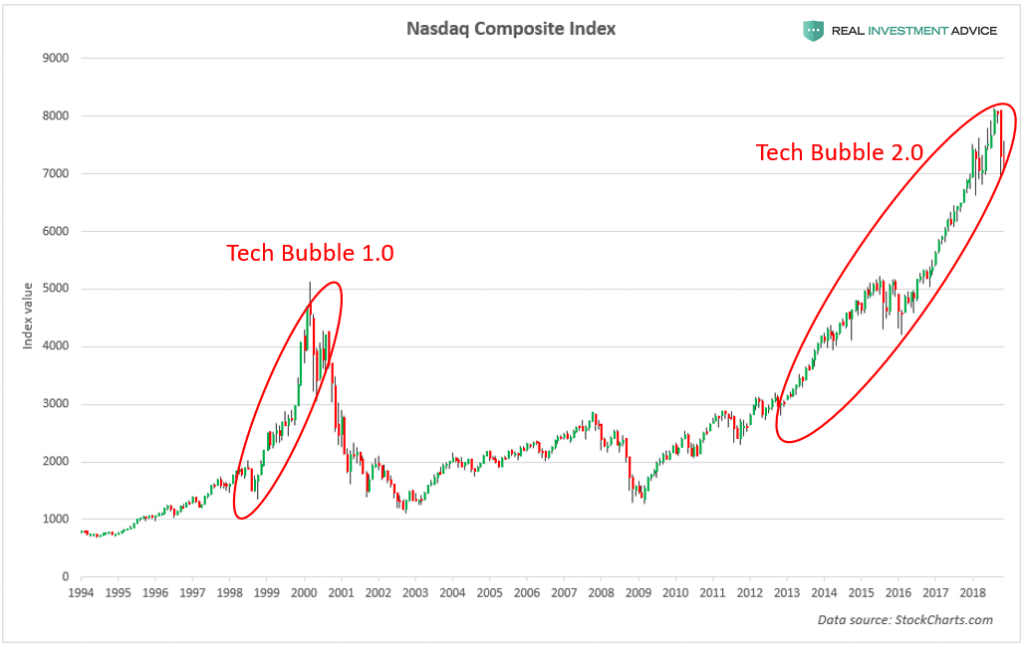

The chart below shows the Nasdaq Composite Index and the two bubbles that formed in it in the past two decades. Lofty tech stock prices and valuations encourage the tech startup bubble because publicly traded tech companies have more buying power with which to acquire tech startups and because they allow startups to IPO at very high valuations.

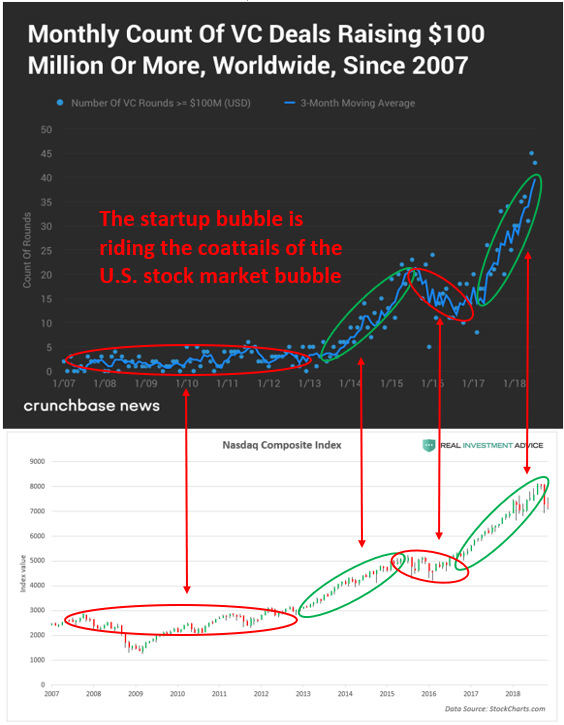

In the chart below, I compared TechCrunch’s monthly global VC deals chart to the Nasdaq Composite Index and they line up perfectly. Surges in the Nasdaq lead to surges in VC deals, while lulls or declines in the Nasdaq lead to lulls or declines in VC deals (yes, I’m aware that correlation is not necessarily causation, but there is a causal relationship in this case).

Unsurprisingly, the decline of the Nasdaq over the past few months is putting a damper on the tech startup bubble. I believe that much more extensive declines are ahead as the stock market bubble unravels, which will lead to even more pain for the tech startup bubble.

Please follow me on LinkedIn and Twitter to keep up with my updates.