Crude oil prices spiked by over $10 on the initial news that Israel was bombing Iran’s nuclear facilities and targeting its key military leaders. The price surge should be expected, given that Iran accounts for slightly over 3% of global production and, more importantly, holds 12% of the world’s proven crude oil reserves. For context, OPEC recently increased its output by 411,000 barrels per day to help marginally lower oil prices. Iran produces 3 million barrels a day, about 8 times that amount.

Israel’s actions raise numerous questions for oil investors. First and foremost is how long this “war” will last and how much it will curtail Iran’s production. If we knew those answers, we might be able to better handicap how oil prices could be impacted. At this point, no one can answer those questions. But it is worth looking at recent activity involving Israel and Iran to help gauge what might be in store.

The table and graph below show six major incidents involving the two countries since the October 7, 2023, attack on Israel. The table above the graph highlights the immediate reaction of oil prices and the follow-through over the preceding week and months. As shown, the initial price reactions to the prior events are minor versus those seen last Thursday night. Moreover, within a month, the prices had erased any short-term gains that occurred following the events. We caution that this time appears to be different. It’s possible that the Israel-Iran conflict could be resolved in short order, and Iran’s oil facilities and production would not be impacted, as was the case in the examples below. However, it’s also possible that this could be a prolonged event, and Iran’s oil production may be curtailed indefinitely.

What To Watch Today

Earnings

Economy

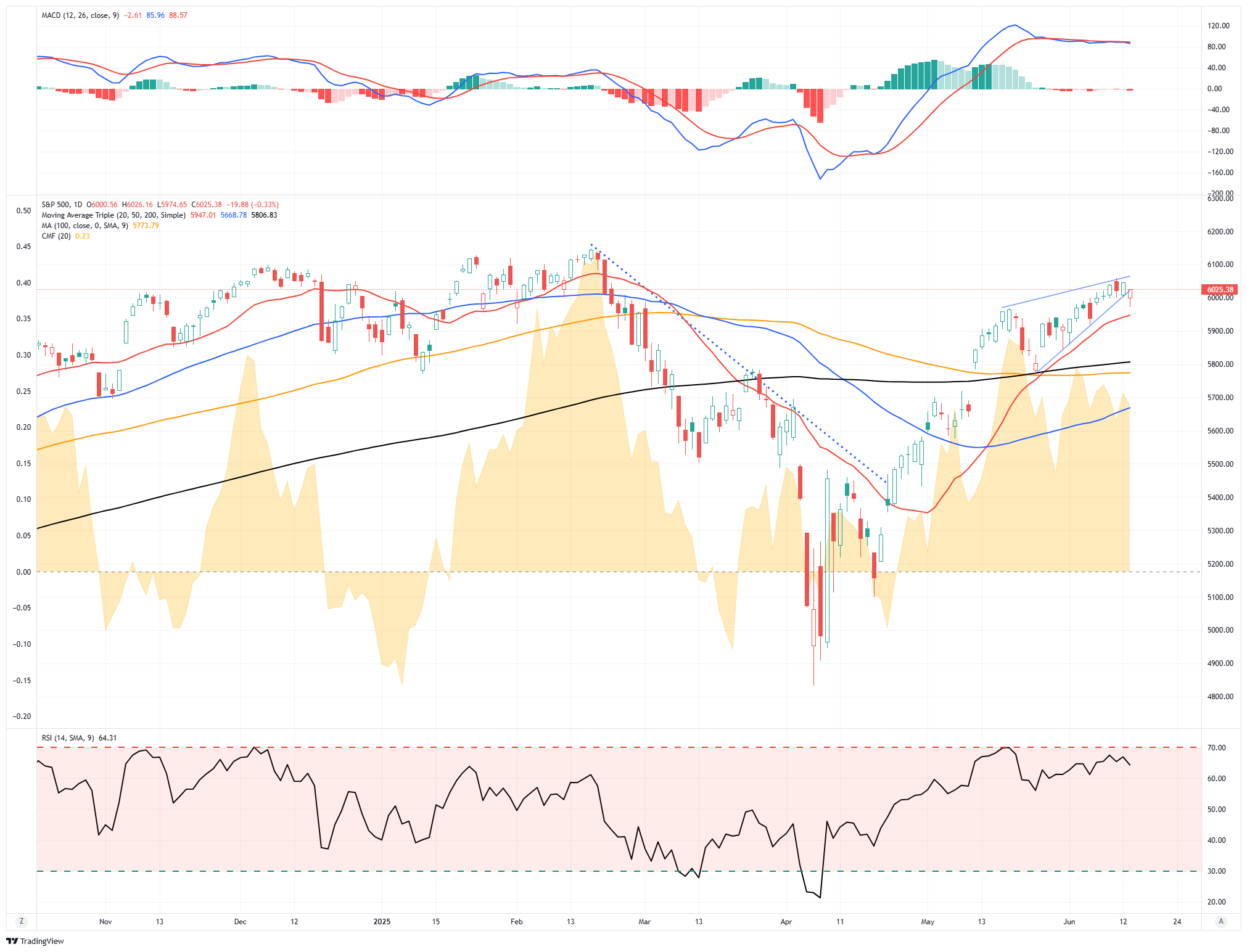

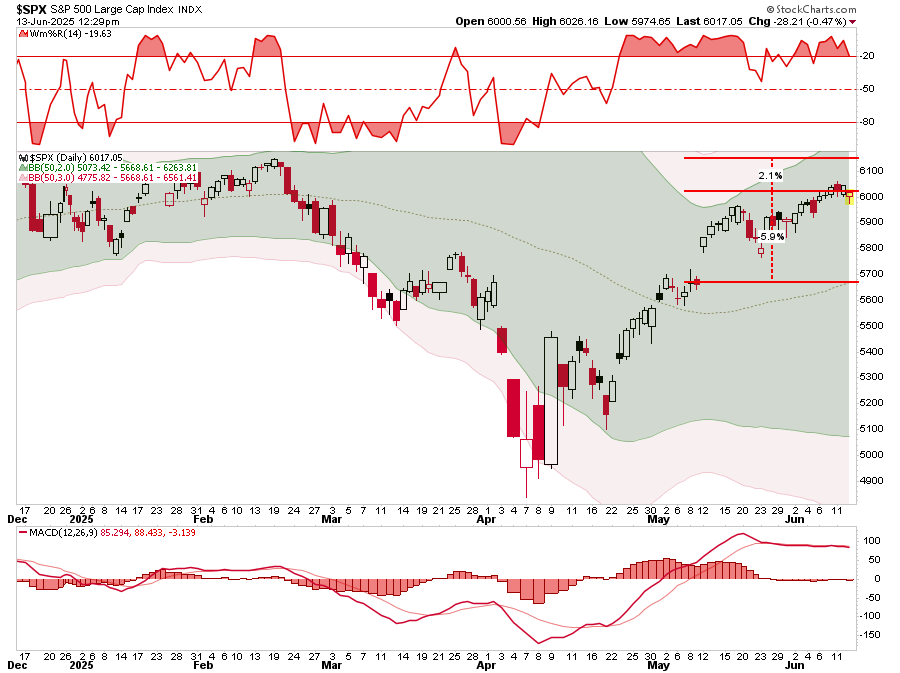

Market Trading Update

Let’s start with where we left off last week.“

“Despite a weakening unemployment report, a spat between President Trump and Elon Musk, a resurgence in the Ukraine/Russia conflict, and remaining tariff uncertainty between China, Europe, and the U.S., the markets continued their bullish ways this past week. Notably, the market broke out of the ongoing consolidation process that has been in place since May 12th. The good news is that bullish breakouts confirm bullish momentum and suggest markets will trade higher into the next resistance level. That next resistance level is 6100, the previous topping process before the March and April decline.”

The market’s bullish trend continued this week, rapidly approaching all-time highs. However, an Israeli strike on Iran early Friday morning sent stocks tumbling at the open, but as of midday, as I am writing this report, most of the initial decline has fully recovered. We noted that a correction or consolidation process is needed to work off some short-term overbought conditions. But, as seen on Friday, any pullback is quickly bought by investors chasing the market in the near term.

As noted last week, we await a pullback to increase portfolio exposure further. However, given that sentiment and positioning measures are in the middle of their ranges, this suggests the bulls remain in control, and any substantial correction could take a while longer to occur. Let me repeat an essential statement from last week:

“Critically, we are not looking for LOWER prices to add exposure. I am okay with paying higher prices. However, we are searching for a better risk/reward opportunity to add exposure. As such, a consolidation period that allows relative strength or momentum to cool off somewhat will provide a better buying opportunity than under current conditions. We already have sufficient exposure to the market to gain performance when markets rise, but deploying capital at these levels is more “risky” than I prefer.”

If we measure risk/reward technically, there is more downside risk than upside potential. The market could reach all-time highs, about 2% above current levels. Conversely, it would take nearly a 6% decline to retrace to the 50-DMA. That is a negative 3-to-1 bet. Most poker players I know would not take those odds. As such, there is no compelling “bet” for deploying capital. However, with some patience and the willingness to sacrifice some short-term performance, we will get an opportunity where the risk/reward proposition improves markedly. Just not when most expect them.

However, the psychological weight of “missing out” on a bull rally that won’t seemingly stop is hard to fight in the short term. This is usually when most investors make their worst investment decisions. Patience is a virtue in this type of environment, but it is a tough commodity to come by. Those who have it tend to succeed, those who don’t, don’t.

The Week Ahead

The Fed meeting on Wednesday will be interesting, given that the latest round of inflation data continues to indicate little to no impact from tariffs. Will their inflationary concerns ease, or will they say it may take more time to see the full effect? The Fed will release its quarterly economic projections. This should provide further insight into their outlook for inflation and employment, as well as their expectations for the future Fed Funds rate.

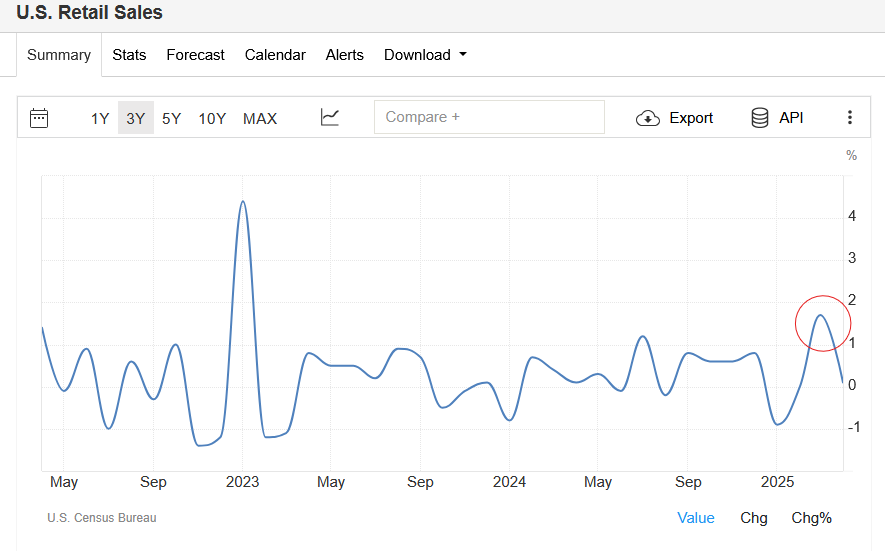

In addition to events related to the Israel-Iran conflict, retail sales data on Tuesday will provide insight into the health of consumers. As we share below, retail sales surged in March as consumers sought to pre-empt tariffs. Given that they pulled consumption forward, Wall Street expects paltry growth of 0.1%. That would be the same as last month’s data.

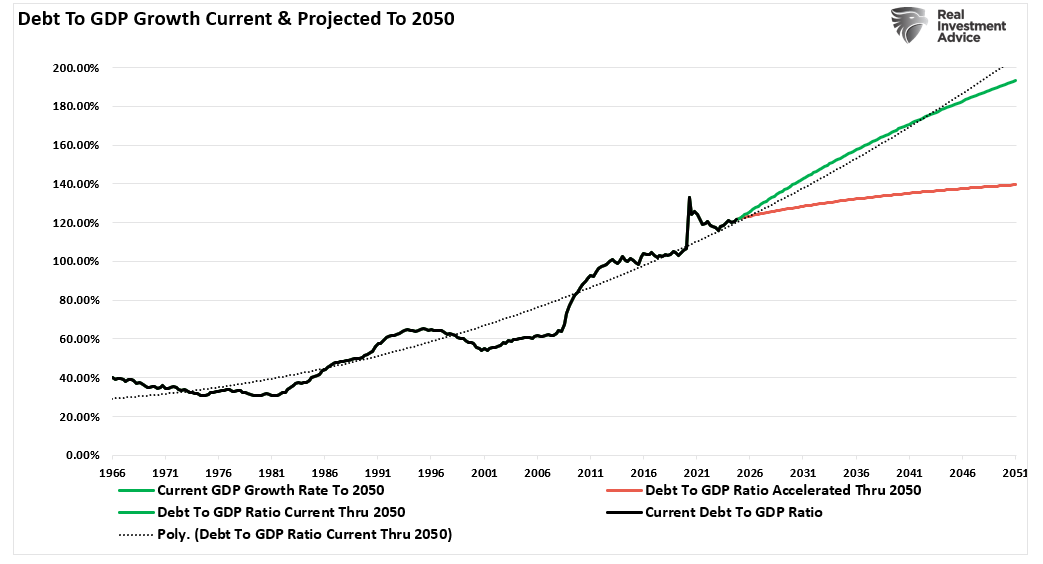

The Deficit Narrative May Find Its Cure In AI

While investors can profit from the coming infrastructure boom, the deficit narrative will also be positively impacted.

From the deficit narrative perspective, this all suggests that the future is potentially much brighter than most imagine. The infrastructure buildout for AI data factories can drive economic growth by creating jobs, stimulating industries, and enabling AI-driven productivity gains. As noted above, increasing growth only marginally would stabilize the current debt-to-GDP ratio. However, boosting GDP growth to 2.3%- 3% annually would vastly improve outcomes. Furthermore, if interest rates drop by just 1%, this could reduce spending by $500 billion annually, helping to ease fiscal pressures.

Significant money-making opportunities are on the horizon for investors. For individuals, the coming strategic investments, workforce development, and sustainable energy policies could improve economic outcomes while resolving deficit concerns.

Don’t let misplaced deficit fears rob you of a potentially fantastic wealth-building opportunity.

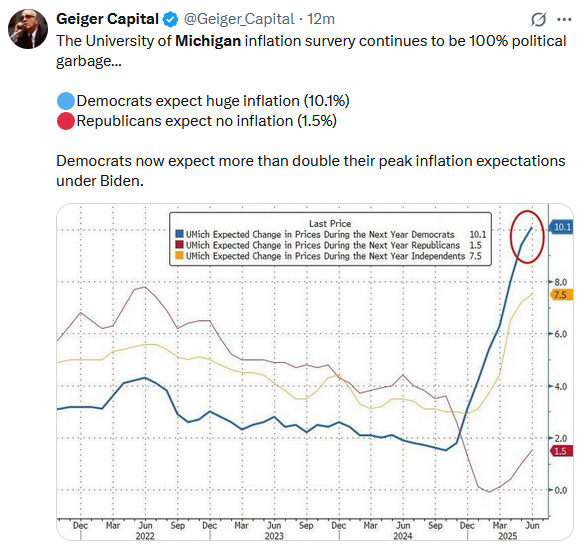

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.