The short answer is that the Bank of Japan (BOJ) is letting the market set yields. For years, the BOJ has run an extremely loose monetary policy, including capping yields at extremely low levels and negative interest rates. Limited economic growth and disinflation made such a policy possible. However, inflationary pressures and a weak yen have prompted the BOJ to shift its stance. Policy normalization started in 2023, when the BOJ allowed 10-year JGB yields to rise above 1% for the first time in over a decade.

Today, 10-year and 30-year bond yields are 1.60% and 3.20%, respectively. They better reflect expectations of continued tighter monetary policy as inflation lingers above the BOJ’s 2% target. Moreover, the yen’s persistent weakness, exacerbated by low interest rates versus the U.S., forces the BOJ to encourage higher interest rates to stabilize the currency.

Japan’s improving economy and higher inflation lead many to anticipate that the BOJ may entirely abandon interest rate caps and negative interest rates. Additionally, with public debt exceeding 250% of GDP, concerns about long-term fiscal sustainability are percolating. Consequently, these factors add to the upward pressure on yields.

The risk to US and global stock and bond investors is that higher Japanese yields and a stronger yen force a reversal of the yen carry trade. If you recall, we saw what that may look like in August 2024.

What To Watch Today

Earnings

- No notable earnings reports

Economy

Market Trading Update

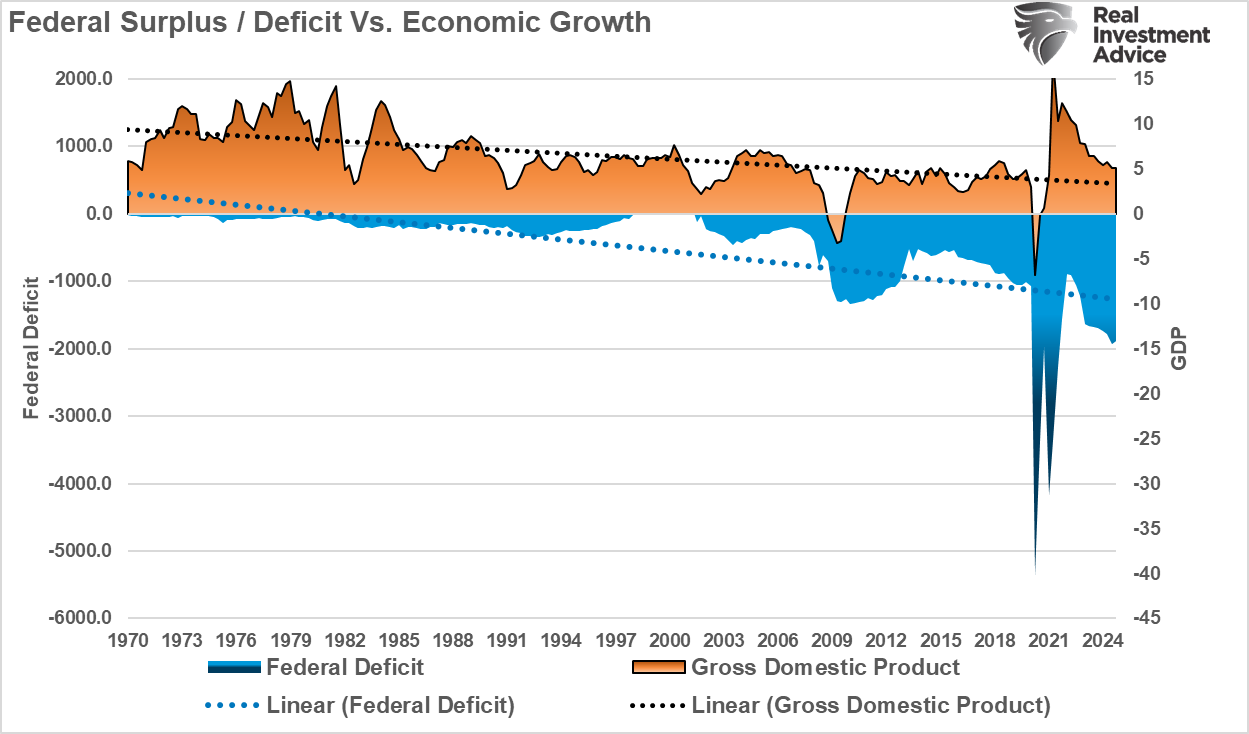

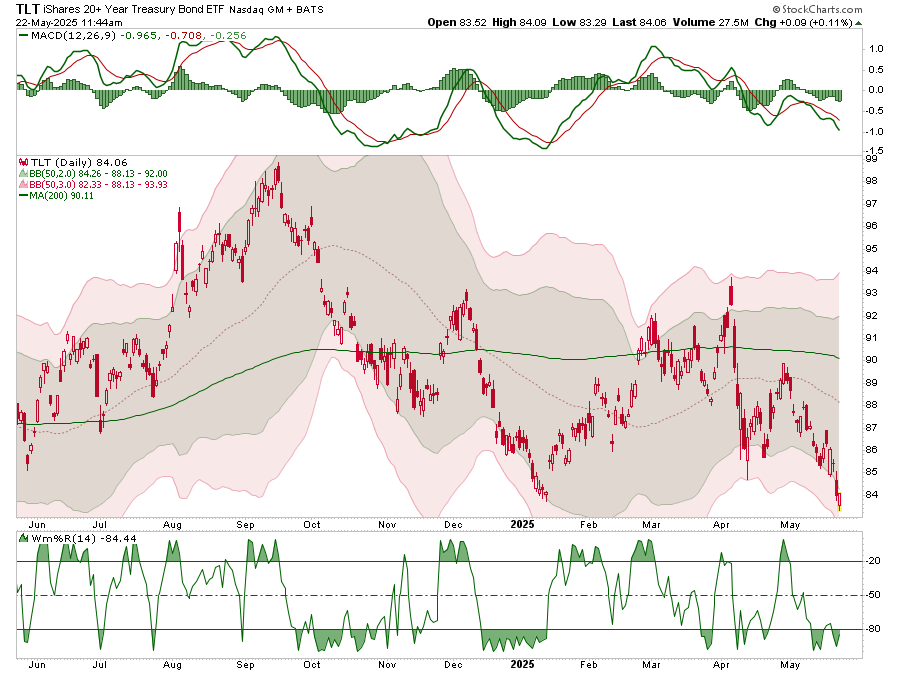

Yesterday, we discussed the back drop to bonds. We also added to our longer-duration bond holding in portfolios due to the deep oversold condition. However, there is a rather large, and glaring mistake, between the current narrative that “deficts” are causing yields to rise. The problem is that we have been running deficits for more than 40-years, and deficits today are lower than they were 5-years ago. But therein lies the key has to why rates are currently higher than they were in 2020.

As shown, correlation between deficits and rates makes sense. The reduction in the deficit since 2020 has been a function of stronger growth and less debt issuance. As deficits decline, and economic growth strengthens borrowers are able to ask for more yield. Conversely, when economic growth is declining sharply, and deficits increase due to increased debt issuance, yields fall. You can see this correlation in the chart below.

As discussed yesterday, in the short-term narratives drive yields along with massive short-positioning and NO central bank interventions. When the Federal Reserve and the Treasury begin to intervene to control the rise in yields, which they will to protect financial stability, the reversal in yields will be rather sharp. However, that could be months or quarters away.

In the mean time, we will have to take advantage of swings in the bond market to increase returns from our fixed income holdings. Currently, as shown, longer-duration bonds are deeply oversold and due for a reflexive rally. What causes that rally? Who knows, but some headline will emerge suggesting lower inflation or slower economic growth and yields will respond accordingly.

As shown, TLT is currently trading 3-standard deviations below the mean which suggest a rally to 88 (the mean) is possible which is a decent short-term trade setup.

In the mean time we get to clip a 4.5% coupon while we wait for a short-term gain.

The 20-Year Auction Was Not As Bad As Its Headlines

- The Terrifying Implications From Today’s Dismal 20-Year Auction- Twitter/X

- The U.S. just held a 20-year Treasury bond auction, and it went terribly- Twitter/X

- 20-Year Treasury Auction Goes Badly – Barrons

Social and traditional media made Wednesday’s 20-year auction out as one of the worst Treasury auctions ever. We, however, would categorize it as tepid. Let’s review a few facts and let you make up your own mind.

For starters, the 20-year Treasury is an orphan bond of sorts. The demand and supply of 20-year bonds are not as large as the more liquid 2-year, 3-year, 5-year, 10-year, and 30-year bonds. As such, the reduced liquidity and smaller auction sizes tend to lead to more volatile auction results.

The Tweet of the Day shows that the “tail” on the auction was 1.2 bps. Thus, the auction rate was 1.2 bps higher than where it was trading prior to the auction. The graph shows that a +/- 1bps result is somewhat normal.

Consider that indirect bidders, predominantly central banks, took 88% of the auction. Direct bidders, the backstop for auctions, took a relatively low 8%. In other words, the auction did not need the largest banks to support it. The graph below shows that the direct bidder allotment was on the low side of recent auctions.

Indeed, the auction could have been better, but the media exaggerates the outcome to feed their current bearish bond narrative.

The Role of Bonds in a Well-Balanced Investment Portfolio

When building a strong and diversified portfolio, most investors focus heavily on stocks. But bonds play an equally important role—especially when it comes to managing risk and providing consistent income. Incorporating bonds into your investment portfolio can lead to more stable investment strategies and long-term financial resilience.

Whether you’re just beginning to invest or looking to rebalance your asset allocation, understanding how bonds work and how to use them effectively is key to building a well-rounded portfolio.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.