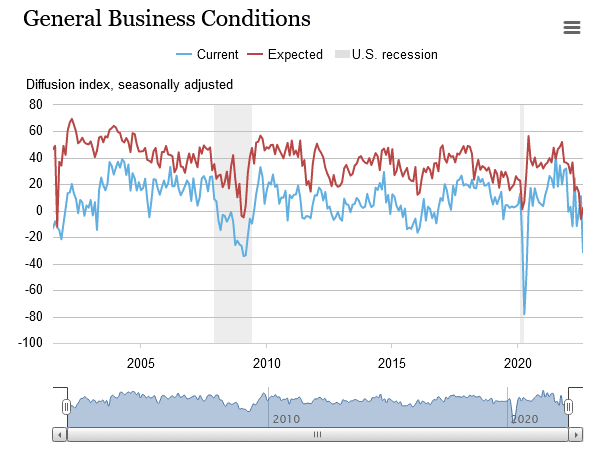

Regional manufacturing indexes tend to correlate strongly with economic activity. More importantly, they are often good leading indicators of economic activity as they report the data in near real-time. The Empire State Index, gauging manufacturing in New York, is the first of the August manufacturing reports to be released. Per the Empire State Survey: “The headline general business conditions index plummeted forty-two points to -31.3. New orders and shipments plunged, and unfilled orders declined.” The 42-point decline was the record’s second-largest decline in the Empire State Index.

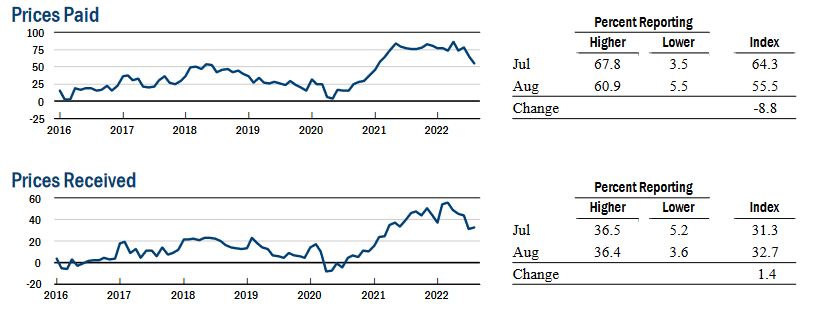

Employment ticked lower to 7.4 but still points to an increasing workforce. That said, the average workweek fell below zero due to reduced hours worked. Often employers will cut hours and temporary employees before laying off full-time workers. The positive news within the Empire State survey is that the prices paid component continues to retreat, as shown in the second graph. However, prices received rose slightly.

What To Watch Today

Economy

- 8:30 a.m. ET: Building permits, July (1.645 million expected, 1.685 prior, upwardly revised to 1.696 million)

- 8:30 a.m. ET: Building permits, month-over-month, July (-3.0% expected, 0.6% prior, downwardly revised to 0.1%)

- 8:30 a.m. ET: Housing Starts, July (1.532 million expected, 1.559 prior)

- 8:30 a.m. ET: Housing Starts, month-over-month, July (-1.7% expected, -2.0% prior)

- 9:15 a.m. ET: Industrial Production, month-over-month, July (0.3% expected, -0.2% prior)

- 9:15 a.m. ET: Capacity Utilization, July (80.2% expected, 80% prior)

- 9:15 a.m. ET: Manufacturing (SIC) Production, July (0.2% expected, -0.5% prior)

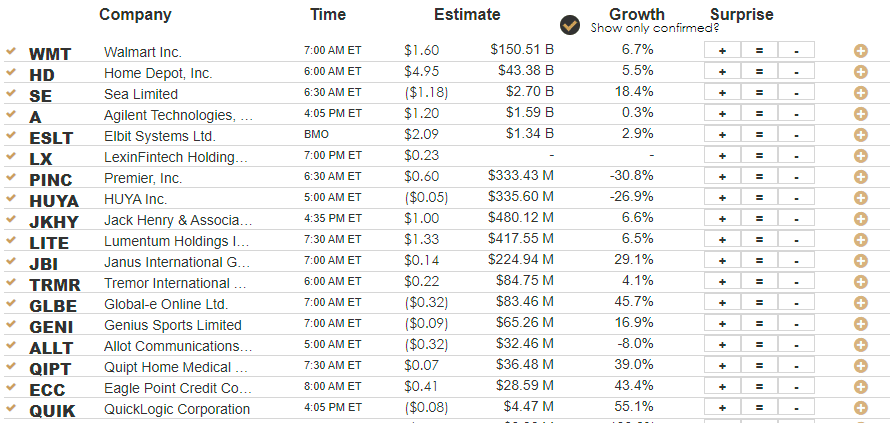

Earnings

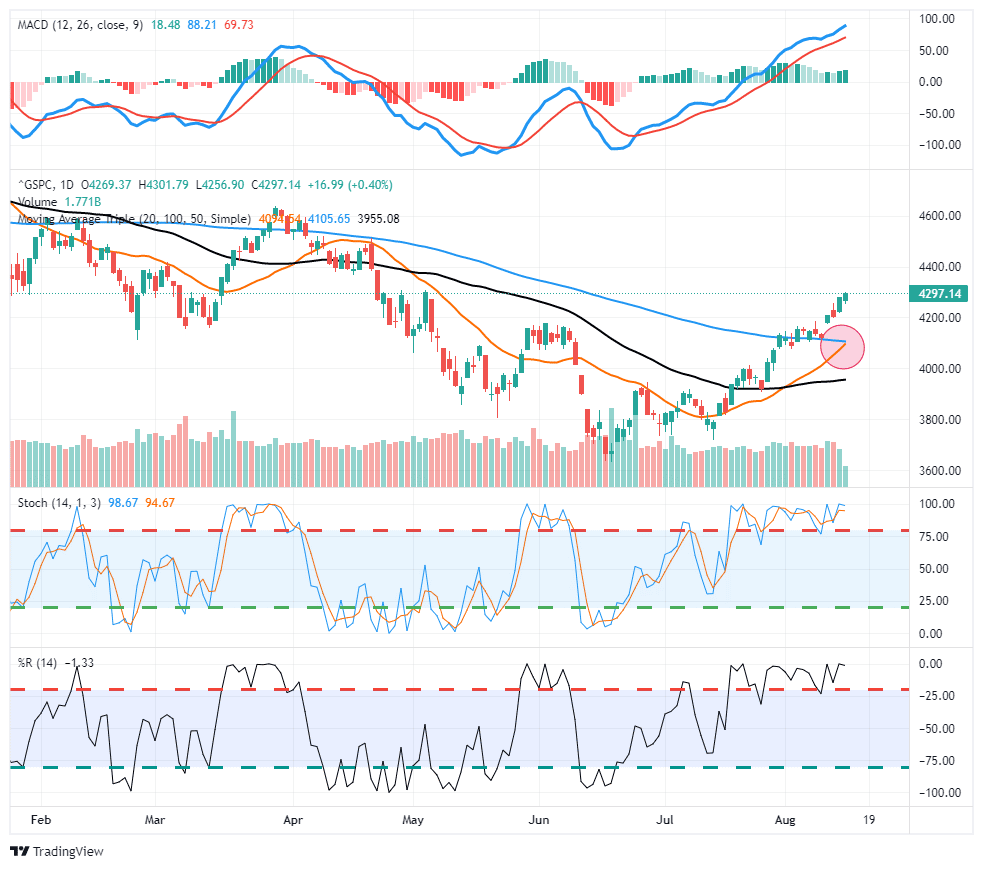

Market Trading Update – Another Bullish Confirmation

More technical bullish signals are confirmed as the market continues to power higher. The latest will occur soon as the 20-dma crosses above the 100-dma, increasing that support level for investors. Any pullbacks to that initial level are likely good points to add some equity exposure, with any pullback to the 50-dma being another good opportunity. The 50-dma is now critical support, and the market is pushing to challenge the 200-dma.

With the market very overbought, be patient and wait for a pullback of some sort to increase exposure. However, the time to be “bearish” is likely behind us for the time being.

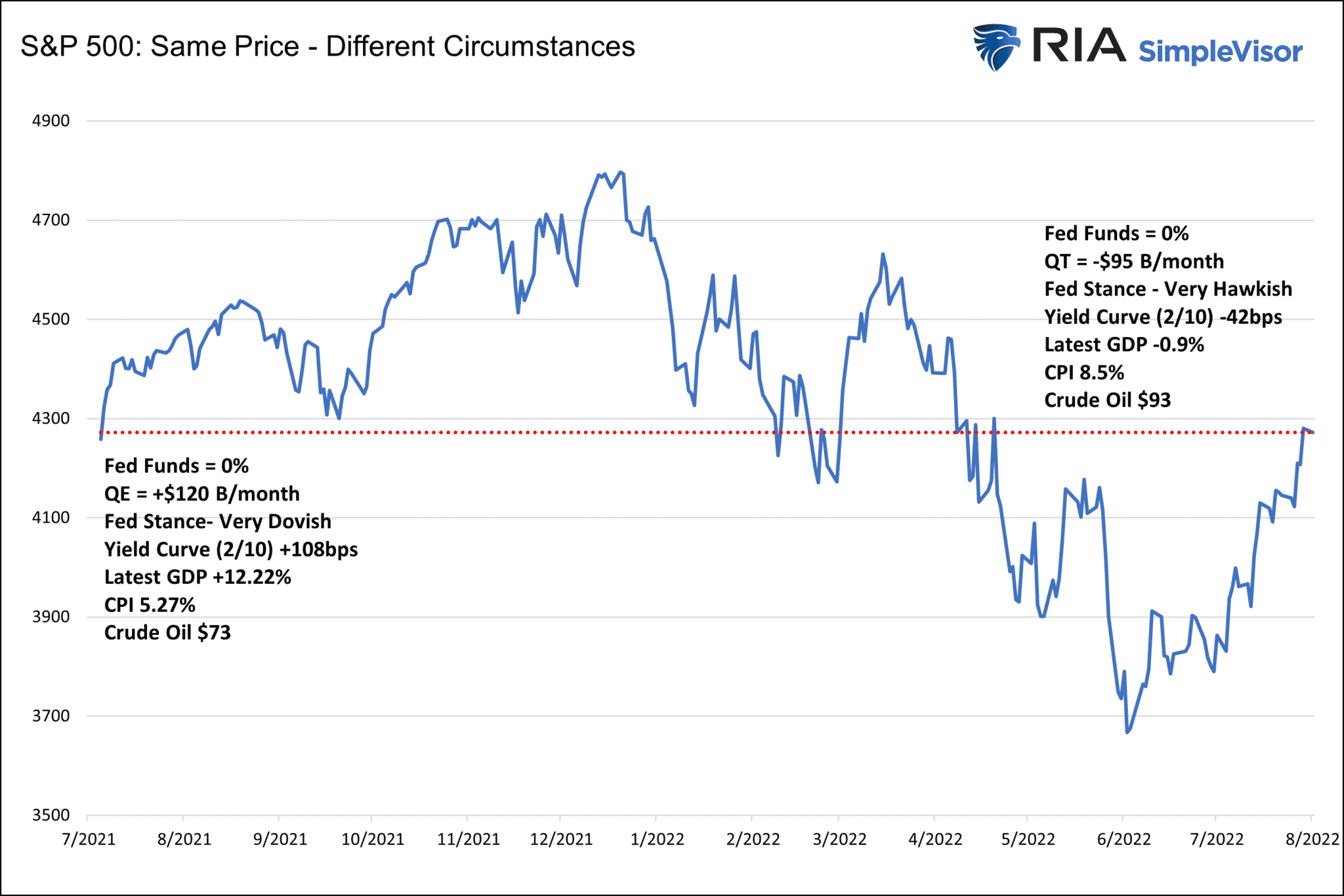

S&P 500– Same Price Different Circumstances

The graph below shows that the S&P 500 is back to the same price as it was about 13 months ago. While the price is the same, the environment could not be more different. Most importantly, the Fed’s policy stances between July 2021 and today are polar opposites.

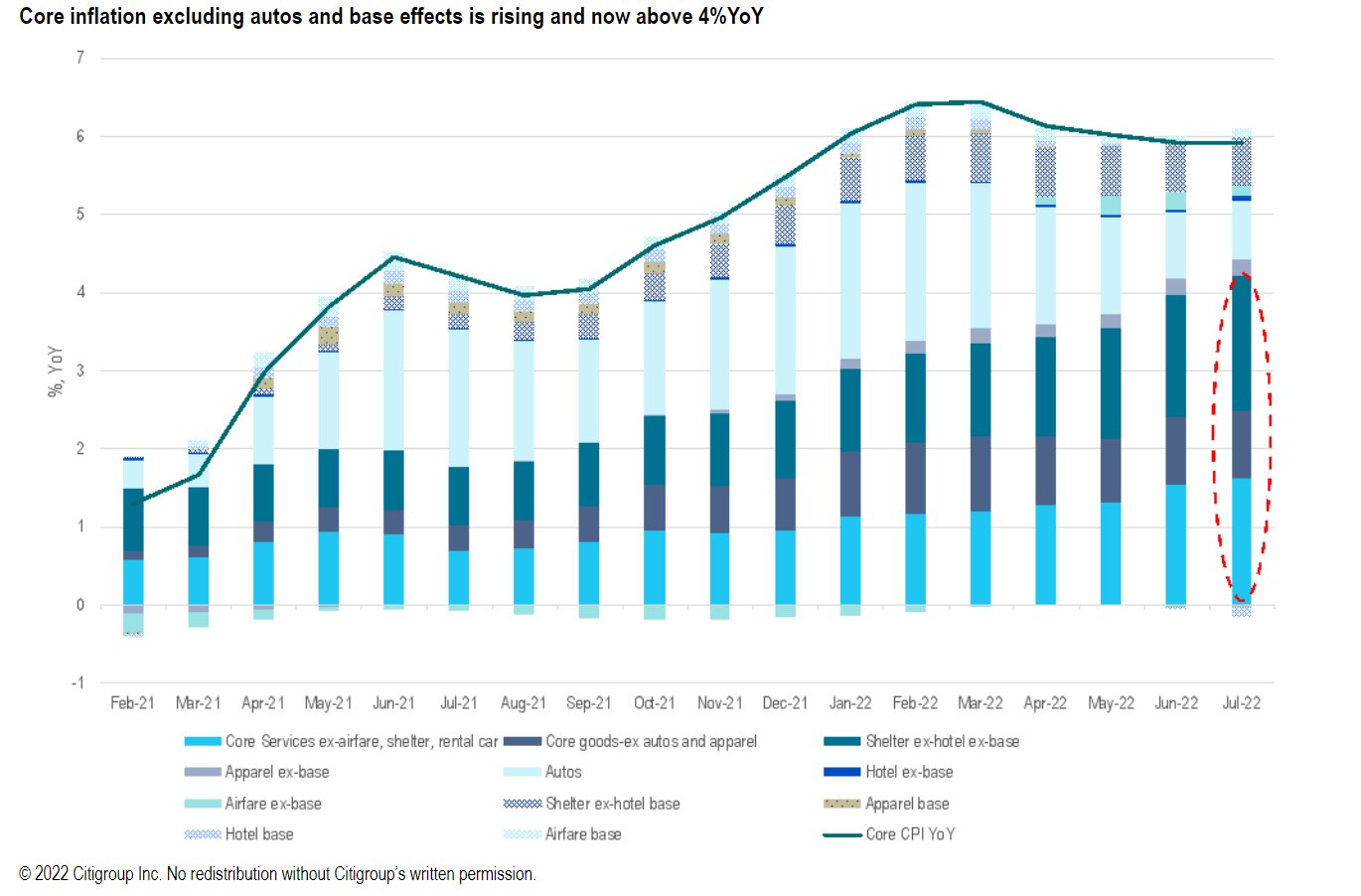

Citigroup Cautions on Peak Inflation Exuberance

The Citigroup graph below shows that despite the recent decline in CPI, core prices continue to rise and constitute a larger percentage of inflation. The circled area highlights core prices. The Fed has made it clear they care more about core prices than the broader indexes. Core prices tend to be much less volatile than non-core goods and services. As such, they are slower to increase but also slower to decline. While broad price indexes are starting to flatline or decline, core goods and services prices are still increasing. Without core goods prices falling, inflation will likely stabilize well above the Fed’s 2% target.

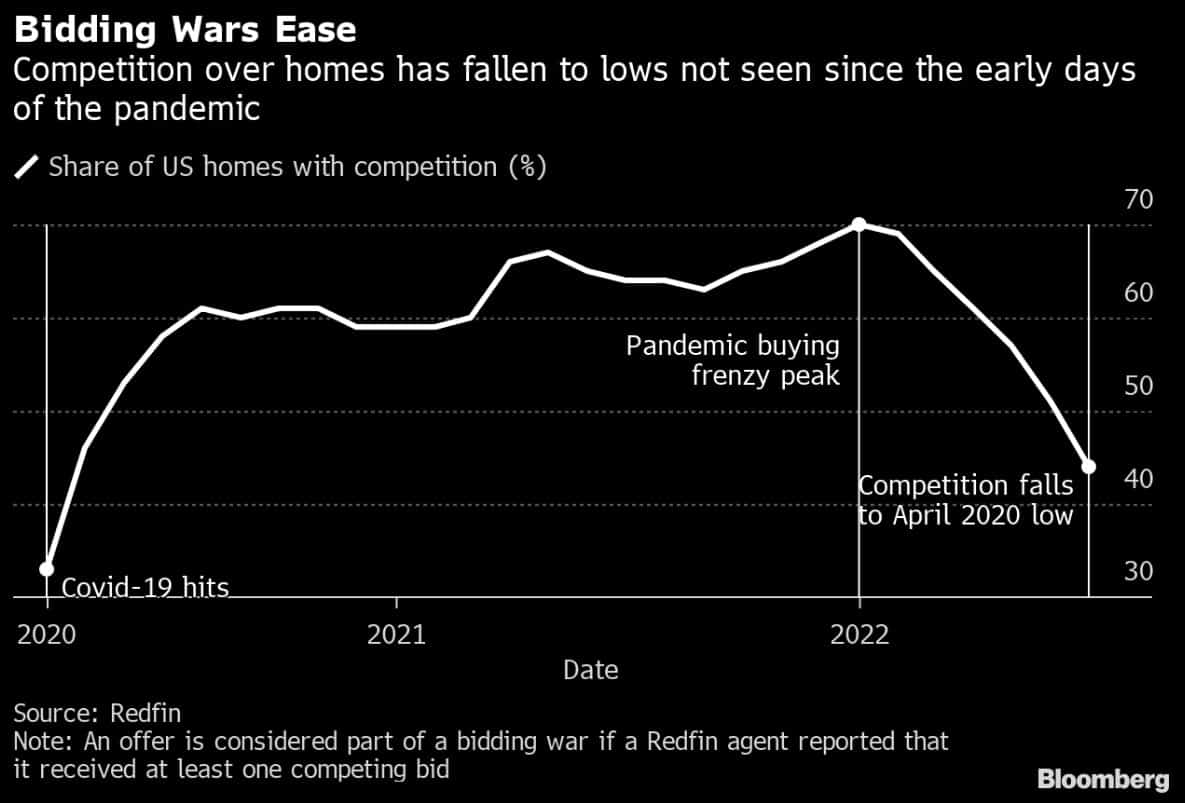

Home Bidding Frenzy is Ending

The Redfin graph below from Bloomberg shows that in July, there was more than one bid for just 44% of U.S. homes for sale. That marks a steady decline correlating with the surge in mortgage rates. This graph serves as yet another warning that the steep pace of home price appreciation is likely peaking. It may still take a month or two before Case-Shiller and other home price indexes reflect the cooling-off reported by large national real estate brokerages like Redfin.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.