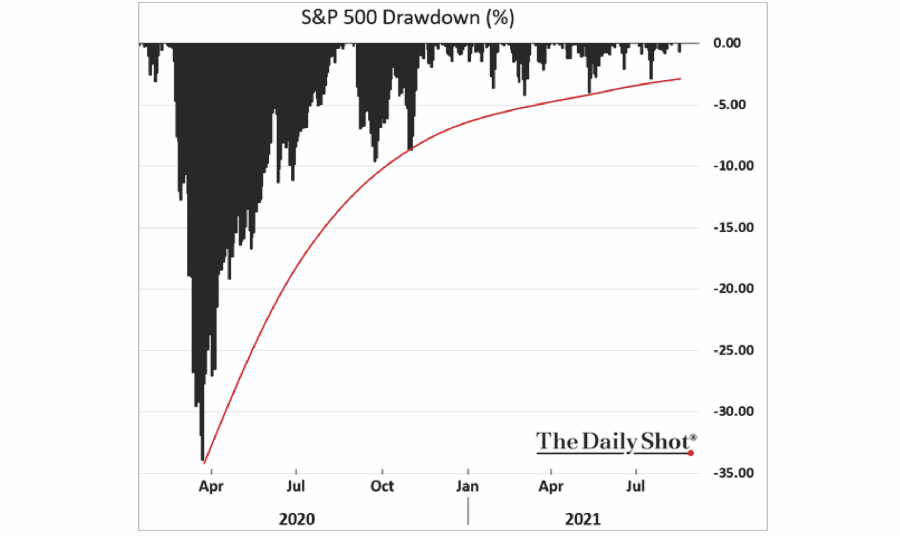

As the Fed started to talk about “taper,” the “bulls” sent a stern warning with a 2% “crash” they shouldn’t.

After a couple of weeks of several Fed speakers discussing the need to reduce monetary accommodation, a quick sell-off brought had Powell singing a “dovish” tone at the recent Jackson Hole summit.

- We said that we would continue our asset purchases at the current pace until we see substantial further progress toward our maximum employment and price stability goals, measured since last December, when we first articulated this guidance. My view is that the “substantial further progress” test got met for inflation. There is also clear progress toward maximum employment. At the FOMC’s recent July meeting, I was of the view, as were most participants, that if the economy evolved broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year.

- The timing and pace of the coming reduction in asset purchases will not be intended to carry a direct signal regarding the timing of interest rate liftoff, for which we have articulated a different and substantially more stringent test.

Notably, the “delta variant” gives the Fed the perfect cover to ignore their two primary mandates of “price stability” and “full employment.” As noted last week, the underlying economy is slowing following the contraction of stimulus into the economy.

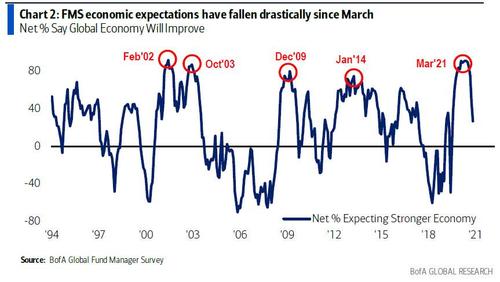

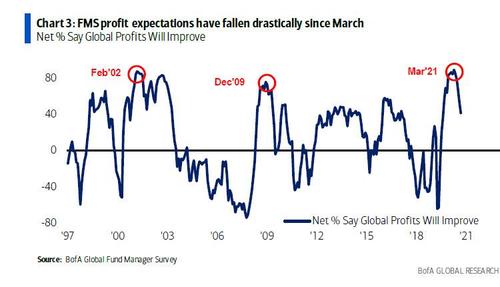

“As BofA recently noted, global expectations are beginning to roll over from very high levels. Such has typically not worked out well for investors.“

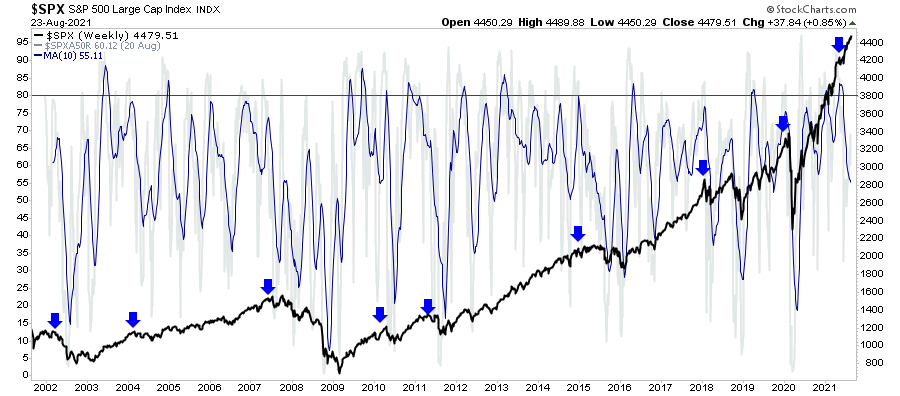

The Bullish Trend Persists

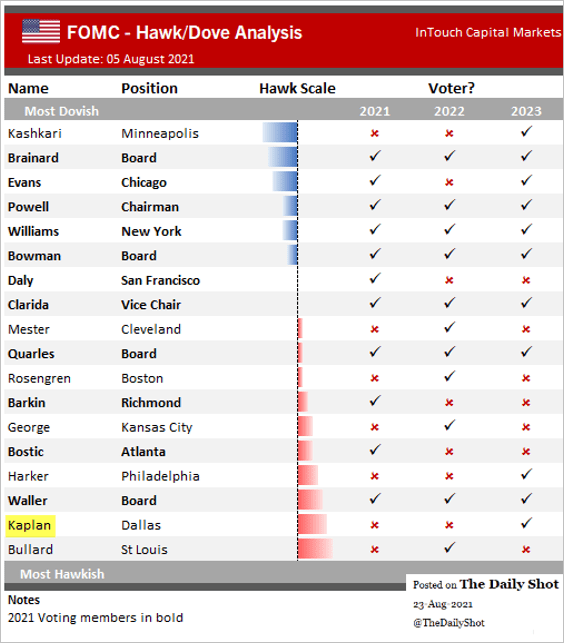

Regardless of the reasoning, our expectation was the Fed would step away from “tapering” their current balance sheet expansion in the near term. Part of the reasoning is that the voting members of the FOMC tilt “dovish,” including Jerome Powell, as shown below. We were not disappointed.

Secondly, the Treasury continues to put pressure on the Fed until a “continuing budget resolution” can get passed along with the $3.5 Trillion “rescue plan.” Such is because treasury balances are rapidly draining as the last remnants of the previous stimulus programs get disbursed.

Lastly, given the Fed linked the success of “monetary policy” to the financial markets. As such, the Fed is now trapped by the “Pavlovian Response” to monetary stimulus.

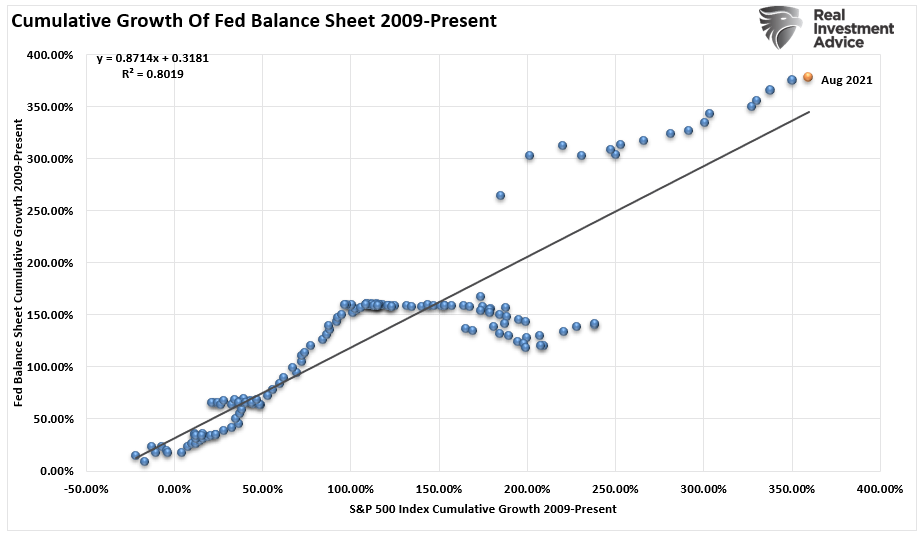

“Importantly, for conditioning to work, the ‘neutral stimulus,’ when introduced, must be followed by the ‘potent stimulus,’ for the “pairing” to be completed. For investors, as each round of ‘Quantitative Easing’ was introduced, the ‘neutral stimulus,’ the stock market rose, the ‘potent stimulus.’”

Much like a “drug addict,” any removal of the stimulus leads to an immediate and severe reaction. Given the high correlation between the Fed’s balance sheet and the stock market, there is no reason to believe this will change soon.

Importantly, while the bulls charge ahead with reckless abandon, there are clear reasons for the bears to remain concerned.

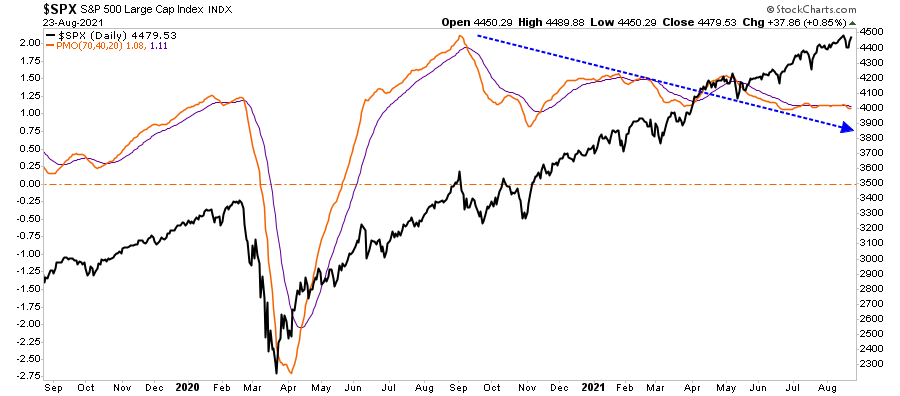

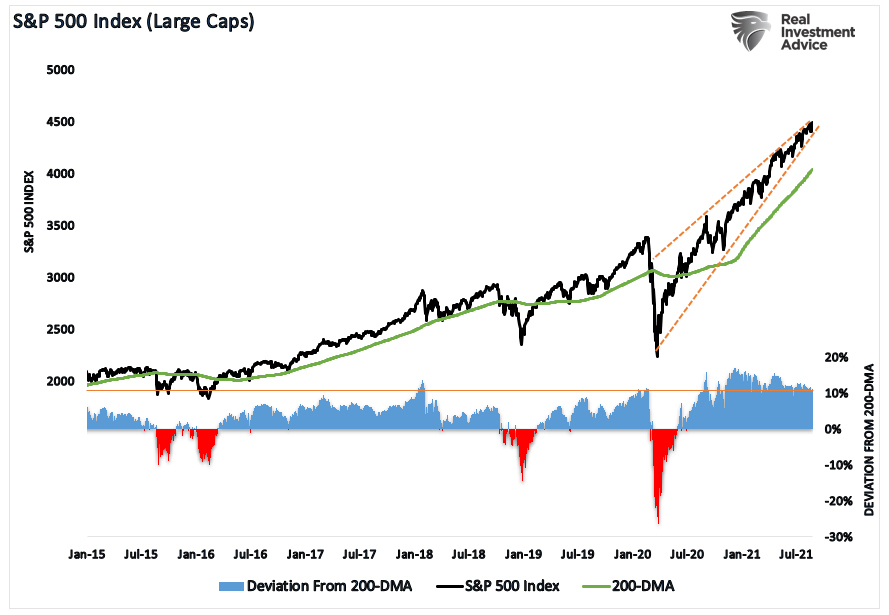

Technicals Remain Weak

As noted in “Bulls Buy The Dip” the bullish trend remains exceptionally strong. Importantly, each “dip” gets bought at shallower levels despite deteriorating internal measures.

There are several primary indicators of market breadth and strength investors pay attention to.

Advance-Decline Line

Number Of Stocks Above The 50-DMA

Price Momentum

Number Of Stocks At 52_week Highs

Notably, such weak internal measures suggest the current market advance remains at risk. While such does not mean the market will correct tomorrow, it does indicate the potential has increased.

Liquidity Risk

For investors, the biggest risk remains the “liquidity” risk.

Every transaction in the market requires both a buyer and a seller, with the only differentiating factor being at what PRICE the transaction occurs. Since this is necessary for there to be equilibrium in the markets, there can be no “cash on the sidelines.”

In the current bull market advance, few people are willing to sell, so buyers must keep bidding up prices to attract a seller to make a transaction. As long as this remains the case, and exuberance exceeds logic, buyers will continue to pay higher prices to get into the positions they want to own.

Such is the very definition of the “greater fool” theory.

However, at some point, for whatever reason, this dynamic will change. Buyers will become more scarce as they refuse to pay a higher price. When sellers realize the change, there will be a rush to sell to a diminishing pool of buyers. Eventually, sellers begin to “panic sell” as buyers evaporate and prices plunge.

Sellers live higher. Buyers live lower.

What causes that change? No one knows.

But that is how bear markets begin.

Slowly at first. Then all of a sudden.

It’s “Party On Garth”

For now, there is seemingly no risk to being long equities. As long as the Fed remains trapped into accommodative policy it is “Party On Garth” for the markets.

However, realizing the liquidity risk that exists, we recommend adjusting exposures to defend against a potential “lack of liquidity” when the eventual “rush for the exits occurs.

There are several actions we have been making in client portfolios to mitigate such a risk:

- Raise cash levels slightly.

- Increase the duration of our bond allocations.

- Reduce overall portfolio “beta” by swapping out higher beta stocks.

- Shift from smaller and mid-size capitalization stocks into large capitalization.

- Rebalance overall portfolio allocations by reducing winners (taking profits) and selling laggards.

These actions will still allow the portfolio to participate in the market’s advance but will mitigate the draw when a downside “gap” occurs to allow for further risk reduction measures.

The goal of portfolio management is to never get forced into making emotionally based decisions. Such always leads to the worst possible outcomes over time.

Currently, there is a near-uniform consensus the market can only go higher. The chart below certainly makes it appear that way.

However, these are precisely the points throughout history where the “party ended” swiftly.

Continue to enjoy the party for now.

Just don’t forget to leave before the cops show up.