A typical mainstream media claim is the March decline was “the bear market,” and the next bull market cycle has begun. Unfortunately, March was not a “bear market,” but just a correction within the ongoing bull market that started in 2009. As such, the 5-ingredients for another market “event” remains.

A History Of Crashes

Throughout history, there are numerous “financial events,” which have devastated investors. The major ones are marked indelibly in our financial history: “The Crash Of 1929,” “The Crash Of 1974,” “Black Monday (1987),” “The Dot.Com Crash,” and the “The Financial Crisis.”

The belief that each of these previous events would be the last is common. Each time the “culprit” was addressed, it assured the markets the problem would not occur again. For example, following the crash in 1929, Congressed rushed to establish the Securities and Exchange Commission and the 1940 Securities Act. The goal was to prevent the next crash by separating banks and brokerage firms and protecting individuals against another Charles Ponzi. (In 1999, Congress passed legislation to allow banks and brokerages to reunite. 8-years later, we had a financial crisis and Bernie Madoff. Coincidence?)

Reactionary Response

In hindsight, the government always acts to prevent the “cause” of the previous crash “after the fact.” Most recently, Congress passed the Sarbanes-Oxley and Dodd-Frank legislation following the market crashes of 2000 and 2008.

Such a “reactionary” response to a crisis is specifically what Bob Bronson previously alluded to:

“It can be most reasonably assumed that markets are efficient enough that every bubble is significantly different than the previous one. A new bubble will always be different from the previous one(s). Such is since investors will only bid prices to extreme overvaluation levels if they are sure it is not repeating what led to the previous bubbles. Comparing the current extreme overvaluation to the dotcom is intellectually silly.

I would argue that when comparisons to previous bubbles become most popular, it’s a reliable timing marker of the top in a current bubble. As an analogy, no matter how thoroughly a fatal car crash is studied, there will still be other fatal car crashes. Such is true even if we avoid all previous accident-causing mistakes.”

Instability

But legislation isn’t the cure for what causes markets to crash. The legislation only addresses the visible byproduct of the underlying ingredients. For example, Sarbanes-Oxley addressed faulty accounting and reporting by companies like Enron, WorldCom, and Global Crossing. Dodd-Frank legislation primarily addressed the “bad behavior” by banks. (Since the banks have successfully lobbied a repeal of the majority of the act).

While faulty accounting and “bad behavior” certainly contributed to the result, those issues were not the cause of the crash. To quote John Mauldin on this issue:

“In this simplified setting of the sandpile, the power law also points to something else: the surprising conclusion that even the greatest of events have no special or exceptional causes. After all, every avalanche large or small starts out the same way, when a single grain falls and makes the pile just slightly too steep at one point. What makes one avalanche much larger than another has nothing to do with its original cause, and nothing to do with some special situation in the pile just before it starts. Rather, it has to do with the perpetually unstable organization of the critical state, which makes it always possible for the next grain to trigger an avalanche of any size.“

While the idea is correct, this assumes that at some point, the markets collapse under their weight when something gives.

The Ingredients

Think about it this way. If I gave you a bunch of ingredients such as nitrogen, glycerol, sand, and shell, you would probably stick them in the garbage can and think nothing of it. There are innocuous ingredients and pose little real danger by themselves. However, when they are combined, and a process is applied to bind them, you make dynamite. But even dynamite, while dangerous, does not immediately explode as long as it is stored properly. Only when dynamite comes into contact with the appropriate catalyst does it become a problem.

“Mean reverting events,” bear markets, and financial crisis are all the result of a combined set of ingredients to which a catalyst was applied. Looking back through history, we find similar elements every time.

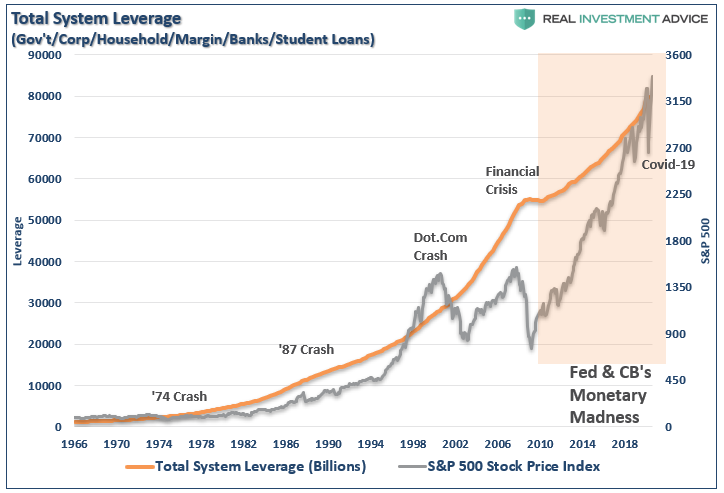

Leverage

There is a consensus that “debt doesn’t matter” as long as interest rates remain low. However, it was the ultra-low interest rate policy of the Federal Reserve, which fostered the “yield chase.” The extremely accommodative policies also led to a massive surge in debt since the “financial crisis.”

Importantly, debt and leverage, by itself is not a danger. Leverage is supportive of higher asset prices as long as rates remain low, and the demand and return on other assets remain high.

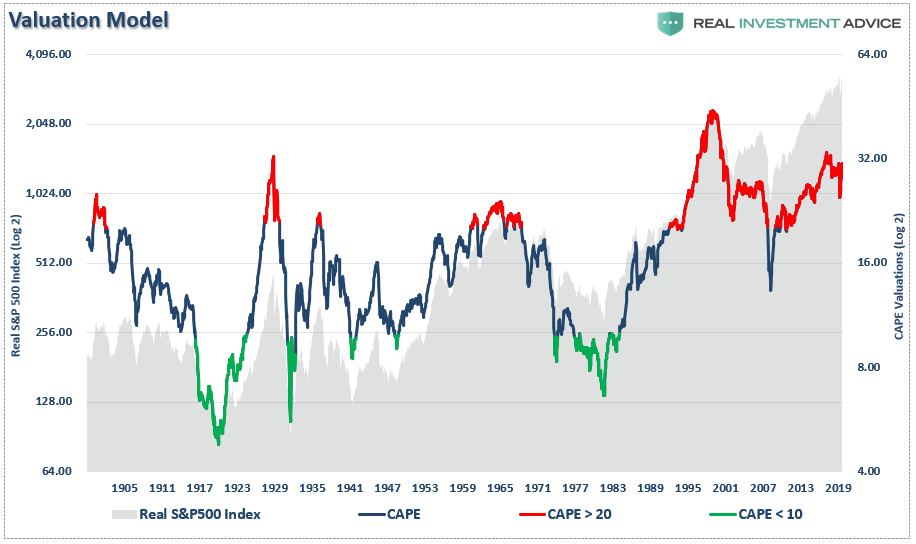

Valuations

Likewise, high valuations are also “inert” as long as everything asset prices are rising. Rising valuations are supportive of the “bullish” thesis as higher valuations represent a rising optimism about future growth. In other words, investors are willing to “pay up” today for expected further growth.

The chart shows both the peaks and troughs in valuations. Peak optimism about the markets also come with peak valuations and vice versa.

The same applies to the secular cycles of the market. As asset prices rise, there is an eventual decoupling from the underlying value that can be generated by economic growth. Those overvaluations eventually must revert during the second half of the full-market cycle.

While valuations are a horrible “timing indicator” for managing a portfolio in the short-term, valuations are the “great predictor” of future investment returns over the long-term.

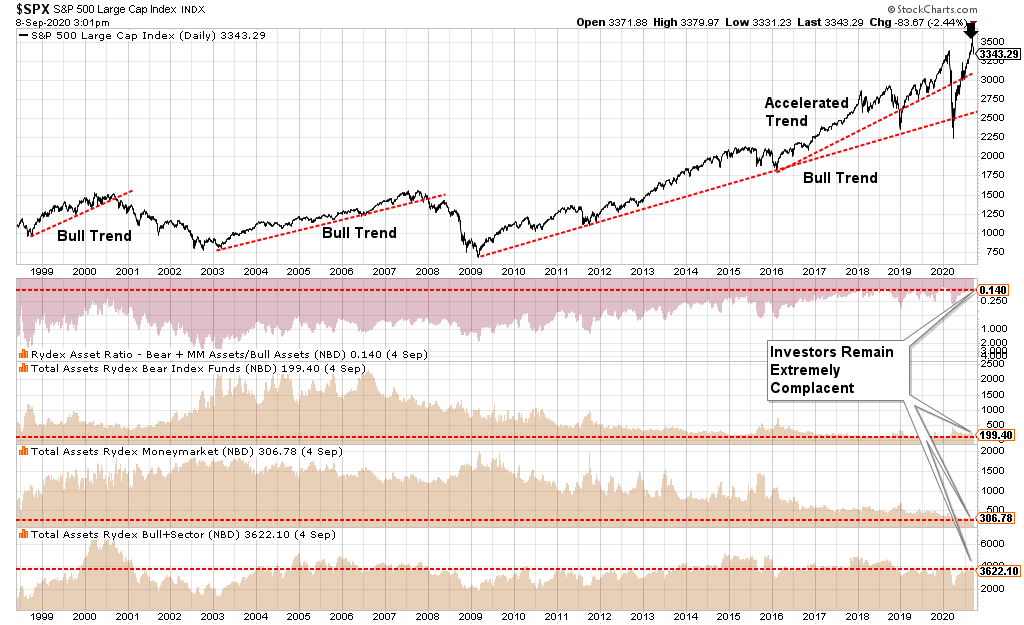

Psychology

One of the critical drivers of the financial markets in the “short-term” is investor psychology. As asset prices rise, investors become increasingly confident and are willing to commit increasing levels of capital to risk assets. The chart below shows the level of assets dedicated to cash, bear market funds, and bull market funds. Currently, the level of “bullish optimism,” as represented by investor allocations, is near the highest level on record.

Again, as long as nothing adversely changes, “bullish sentiment begets bullish sentiment,” which is supportive of higher asset prices.

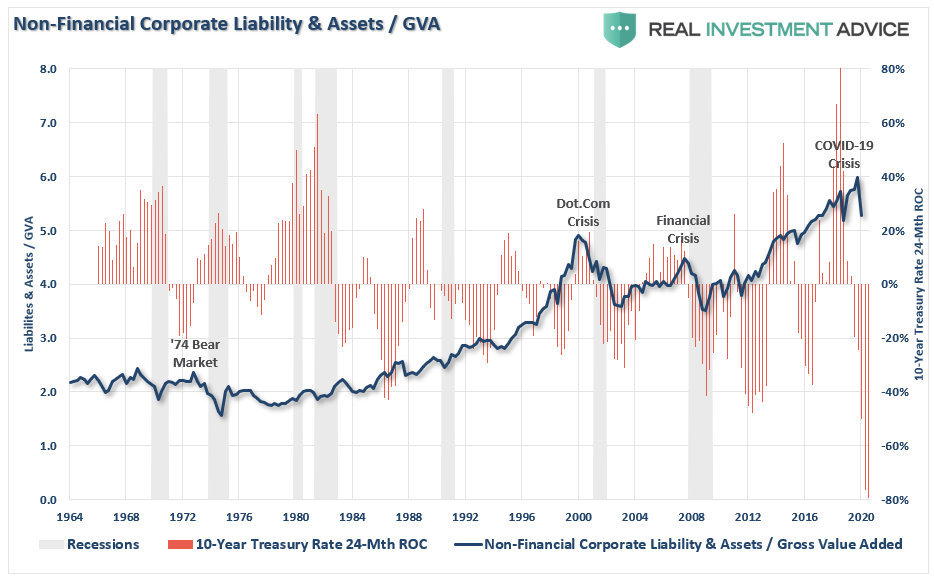

Ownership

Of course, the critical ingredient is ownership. High valuations, bullish sentiment, and leverage are utterly meaningless if there is no ownership of the underlying equities. The two charts below show both household and corporate levels of equity ownership relative to previous points in history.

Once again, we find rising levels of ownership are a good thing as long as prices are rising. As prices rise, individuals continue to increase ownership in appreciating assets, which, in turn, increases the purchase price of the assets.

Momentum

As prices rise, demand for increasing assets also rises, which creates a further demand for a limited supply of assets, increasing the prices of those assets at a faster pace. Growing momentum is supportive of higher asset prices in the short-term as investors get sucked into a “speculative frenzy” phase near market peaks.

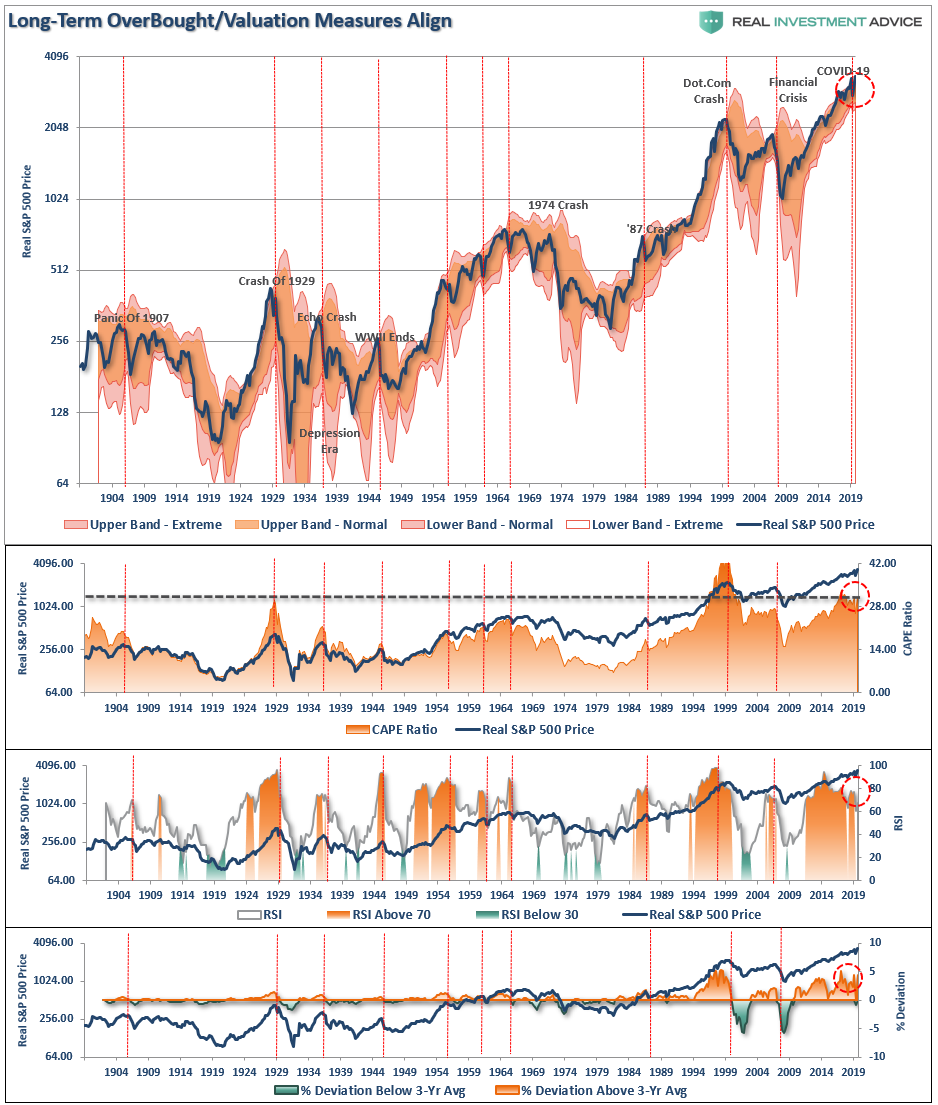

The chart below shows the real price of the S&P 500 index versus its long-term Bollinger-bands, valuations, relative-strength, and its deviation above the 3-year moving average. The red vertical lines show where the peaks in these measures historically peaked.

Conclusion

Like dynamite, the individual ingredients are relatively harmless. However, when the ingredients are combined, they become potentially dangerous.

Leverage + Valuations + Psychology + Ownership + Momentum = “Mean Reverting Event”

Importantly, in the short-term, this particular formula does indeed remain supportive of higher asset prices. Of course, the more prices rise, the more optimistic investors become.

While the combination of ingredients is indeed dangerous, they remain “inert” until exposed to the right catalyst.

What causes the next “liquidation cycle” is currently unknown. It is always an unexpected, exogenous event that triggers a “rush for the exits.”

Many currently believe “bear markets” and “crashes” are a relic of the past. Central banks globally now have the financial markets under their control, and they will never allow another crash to occur.

Maybe that is indeed the case. However, it is worth remembering that such beliefs were always present, to quote Irving Fisher, “stocks are at a permanently high plateau.”