While I remain long and invested in the markets on behalf of my clients, I focus and write about the significant risks that are currently present. I am fully aware a laissez-faire attitude towards these risks is ultimately likely to destroy large portions of my clients hard-earned, and irreplaceable, investment capital.

Note: Myself, and everyone that writes for Real Investment Advice, do so under our actual name. We pride ourselves on our transparency, and our responsibility, to all that read our work. We value our loyal following and work diligently to improve upon the original ideas and research we share.

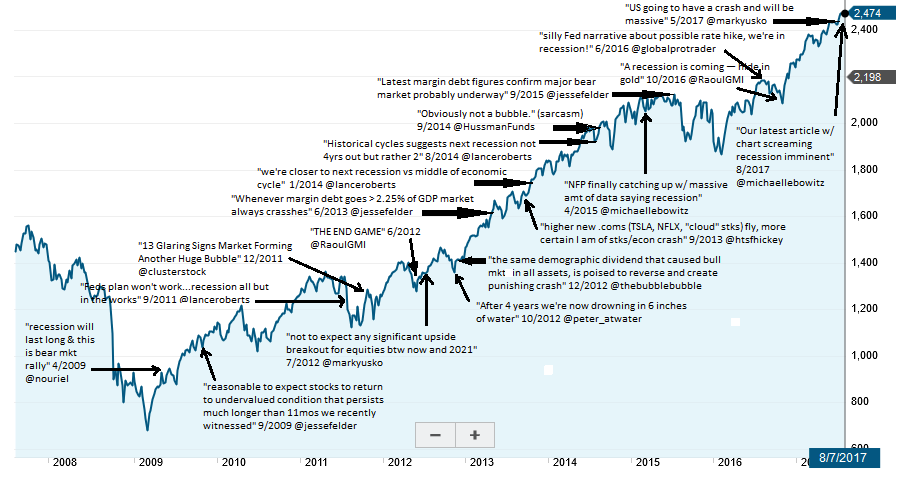

This past week, I was treated to a chart from “The Fat Pitch” blog, by Urban Carmel, which took several pieces of my previous writings out of context to try and suggest that I somehow had “missed the market.”

“Yet, throughout this period, investors with even a passing interest in financial news have regularly seen commentary from experienced managers that the stock market is highly likely to plunge now. The irony of equity investing is this: if you knew nothing about the stock market and did not follow any financial news, you have probably made a very handsome return on your investment, but if you tried to be a little bit smarter and read any commentary from experienced managers, you probably performed poorly.”

While I certainly appreciate the “buy and hold” crowd trying to justify why you should just take a blind approach and hold on for the ride, I struggle because I am all too aware when market shifts occur, as proven in 2000 and 2008, years of gains can be wiped out in months.

By taking commentary out of context from the managers noted above, it misses the actual investment management process being undertaken by myself as well as some of the other individuals listed. What he left off the chart above from myself are prescient market calls such as:

- December 2007: “We are, or are about to be, in the worst recession since the ‘Great Depression.'”

- February 2009: “Here are 8-reasons for a bull market.”

- March 2012: “Coming This Fall, The Best Time To Invest”

- March 2013: “Time to get out of Gold.”

- June 2013: “Pimco says bond bull market is over, I say it is still alive”

- April 2014: “Time to get out of Energy.”

- August 2015: “Why This Time Could Be Different” (Warned of the coming 2015-16 correction)

- October 2016: Technically Speaking: 2400 or Bust

You get the idea.

And yes, as noted in the chart above, I did warn about things that didn’t come to pass, such as the correction in 2015-2016 was only a 20% decline, and despite plenty of economic evidence which suggests it was a “mini-recession,” it was never officially labeled that way…yet.

So, I was wrong. I apologize.

Importantly, however, by reducing equity risk during the 2015-2016 period, I saved my clients the stress of the decline and preserved their investment capital which was reallocated back to the equity markets when the correction passed.

There have also been times along the way that portfolios I manage were underweight equity when, in hindsight, completely ignoring risks, would have provided a slightly better rate of return. That too, is an acceptable outcome given the potentially devastating consequences. Successful investment professionals must adhere to discipline and respect one’s evaluation of risk, even at the cost of missing some upside.

That is what “managing a portfolio” means, and also why client’s pay me to do it.

If simply “buying and holding” an index is indeed the way to manage money, as suggested by Carmel, then why would you ever “pay a fee” to someone to do that for you? You can do it yourself from roughly 0.25-0.30% at Vanguard.

You Don’t Have The Time

The reason this is so important, as I have exhaustively written about, is the math of loss, and time.

While writers like Urban Carmel, and many others promulgate the idea of “buy and hold” investing, they misunderstand, and more importantly dismiss, the mathematics of the investing cycle despite claiming an “evidence based investing” approach.

To wit from Urban Carmel:

“In the past 193 years, US equities have suffered an annual loss greater than 20% just 9 times, a “base rate” of 4.7%. The “base rate” is the probability you would assign to an outcome if you knew nothing other than how often it was statistically likely to happen (from basehitinvesting.com).”

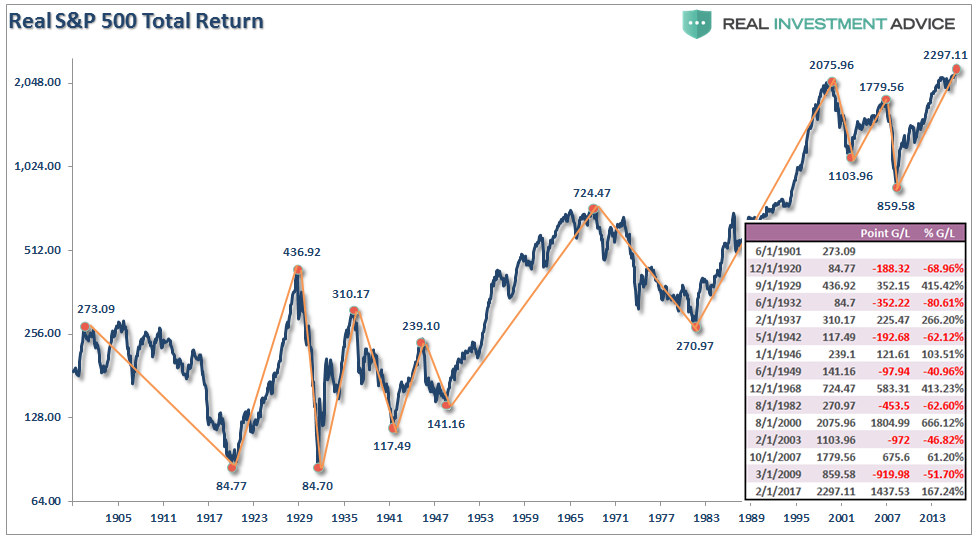

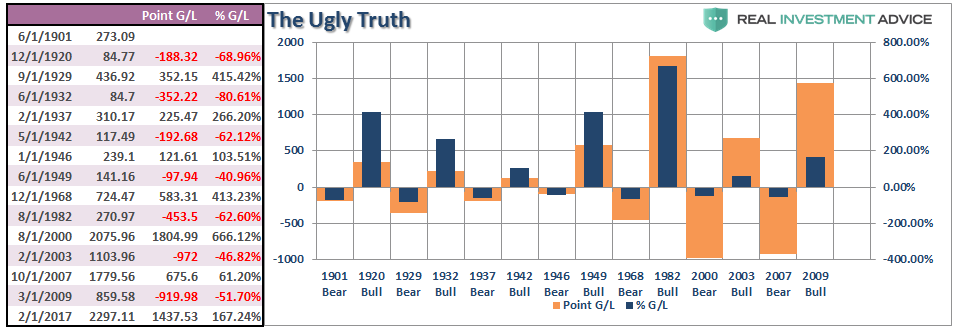

Now, those statistics are absolutely right. The issue is that looking at percentages is incredibly deceiving. Being up 80%, and then down 50%, doesn’t leave you 30% ahead, but rather 10% behind. More importantly, you have lost precious time, often measured in years, in your wealth accumulation process. As I previously discussed in “The World’s Most Deceptive Chart.”

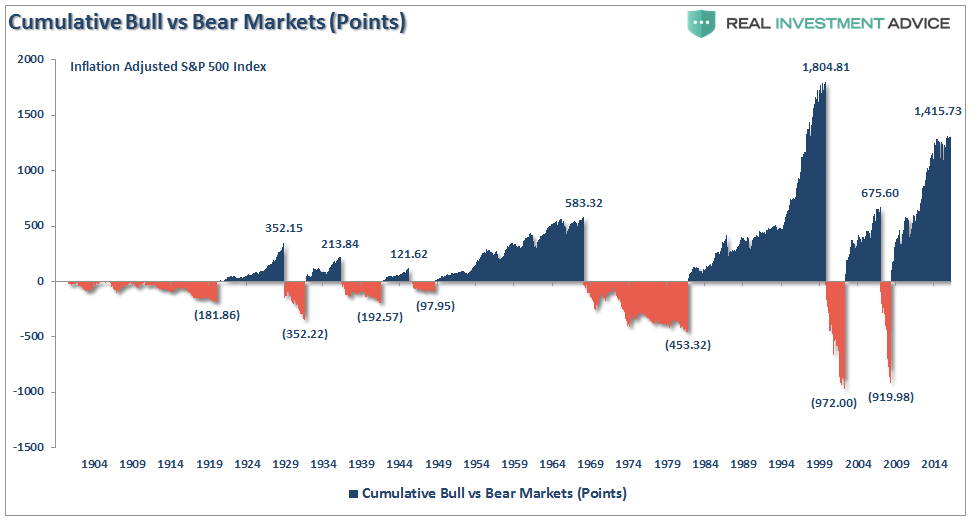

“The first chart shows the S&P 500 from 1900 to present and I have drawn my measurement lines for the bull and bear market periods.”

“The table to the right is the most critical. The table shows the actual point gain and point loss for each period. As you will note, there are periods when the entire previous point gains have been either entirely, or almost entirely, destroyed.

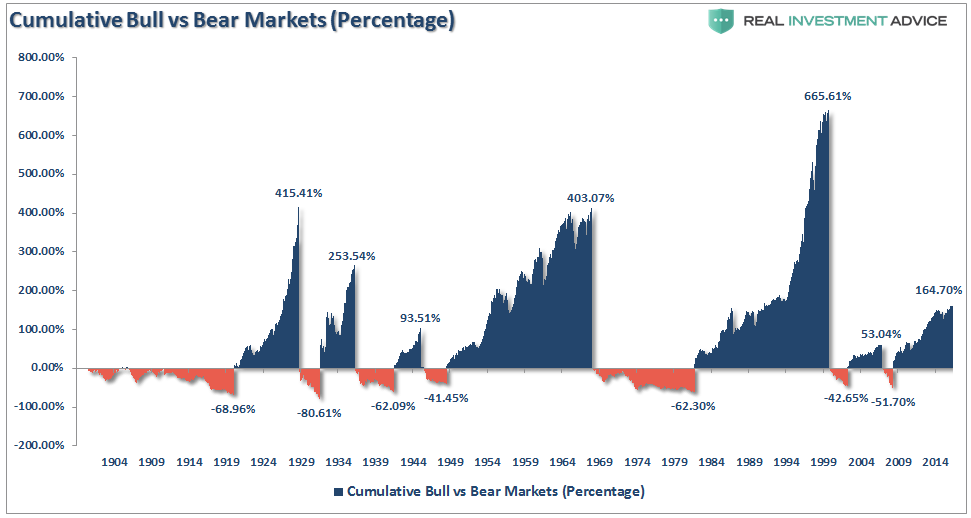

The next two charts are a rebuild of the first chart above in both percentage and point movements.

Again, even on an inflation-adjusted, total return, basis when viewing the bull/bear periods in terms of percentage gains and losses, it would seem as if bear markets were not worth worrying about.”

“However, when reconstructed on a point gain/loss basis, the ugly truth is revealed.”

This was a point Michael Batnick addressed, but dismissed:

“However, ‘stocks usually go up’ also implies that sometimes stocks go down, and sometimes they go down a lot, which is supported by the *chart below. This is why it can also pay for financial pundits to play on the bearish side. Usually they’re wrong, but when they’re right, they get to say “I told you so.” They saw what few others did, and this can provide them with an open invite from the media for the rest of their career.”

“The fact that stocks usually go up makes permabulls look like idiots once in a while and permabears look like geniuses once in a while.”

What Michael misses is that while markets DO rise the majority of the time, the drawdowns that follow wipe out a large chunk, and sometimes all, of the previous gains.

No Excuses

For actual portfolio managers, it is never about being able to say “I told you so.”

It is about NOT having to face a client who are in, or near, retirement and trying to explain how the loss of 20, 30 or 40% of their capital will eventually come back.

Why should the client be upset they just witnessed a significant chunk of their life savings vanish? The mainstream “buy and hold” crowd will simply rely on the excuse:

“Well…NO ONE could have seen that coming.”

Not only is that oft-used comment simply not true, it is complete negligence of their duty as the clients fiduciary.

Me…I am no one important. I run a small portfolio of clients in Houston and simply write about what I am doing for them. However, there are many very smart managers from Ray Dalio, to James Grant, Jeremy Grantham, Howard Marks, Mark Yusko, Jesse Felder, and Michael Lebowitz all suggesting “something wicked this way comes.”

You have been sufficiently warned.

It may not be today, next month or even next year.

“Bull markets are built on optimism and die on exuberance.”

But they all die. Simply ignoring history won’t make the damage any less catastrophic

Of course, given that investors are just “mere mortals” and do not have an infinite amount of time to reach their financial goals, the end of bull market cycles matter, and they matter a lot.

While “perma-bulls” may enjoy taking stabs at portfolio managers that take their risk management and capital preservation responsibilities very seriously, it should be done without taking those comments out of context.

Have I warned of risks in the markets?

Absolutely.

Does that mean I have somehow been sitting in “cash” this whole time and “missing out?”

Absolutely Not.

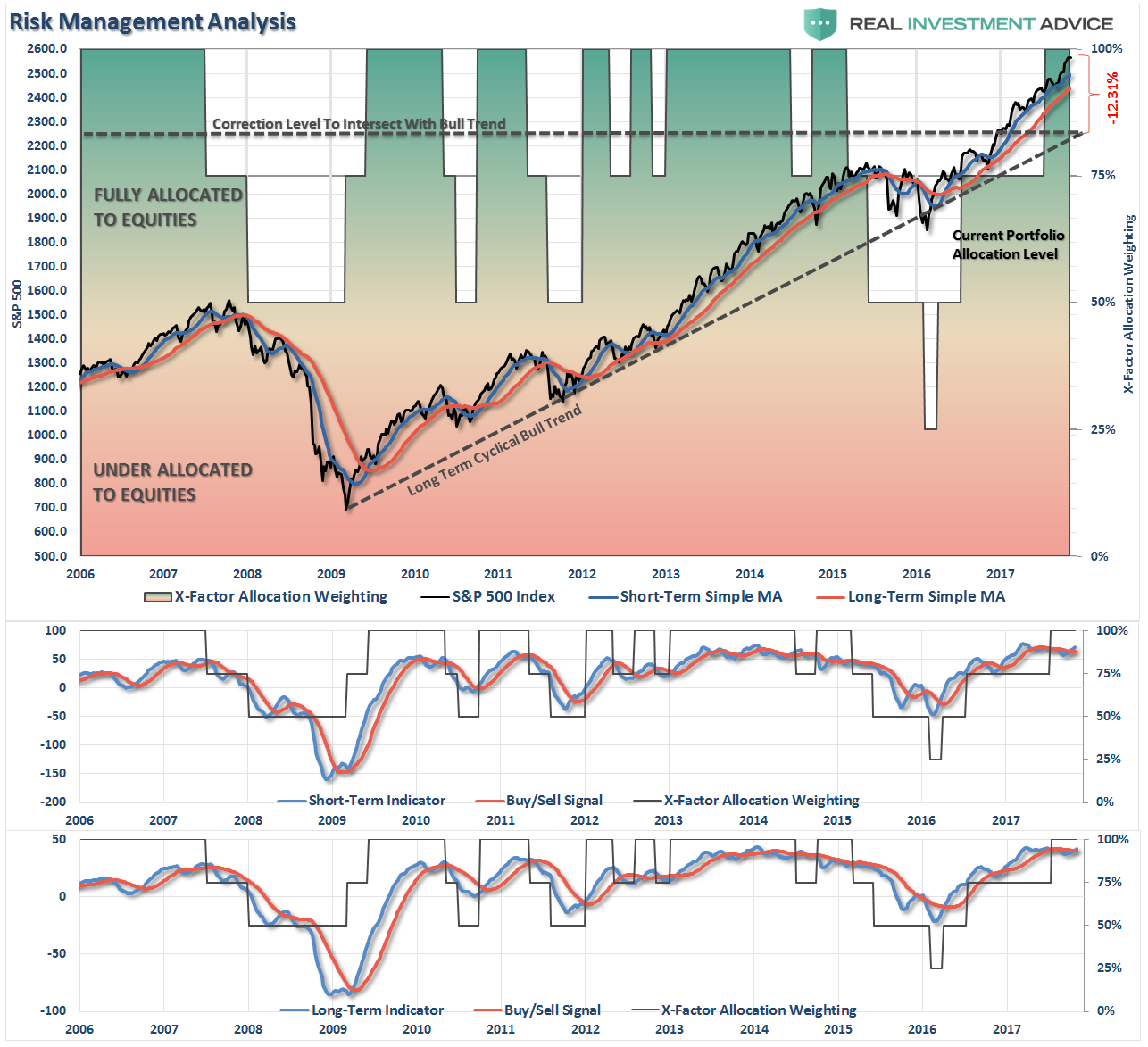

Every single week I publish a newsletter on our site which updates our risk management analysis and exposure model. The model adjusts equity risk relative to the price trends and risks prevalent in the market. As you will notice, more often than not, the risk reduction provided protection against declines, protecting capital and reducing volatility. (If you would like access to it to see for yourself CLICK HERE and it will be in your inbox next week.)

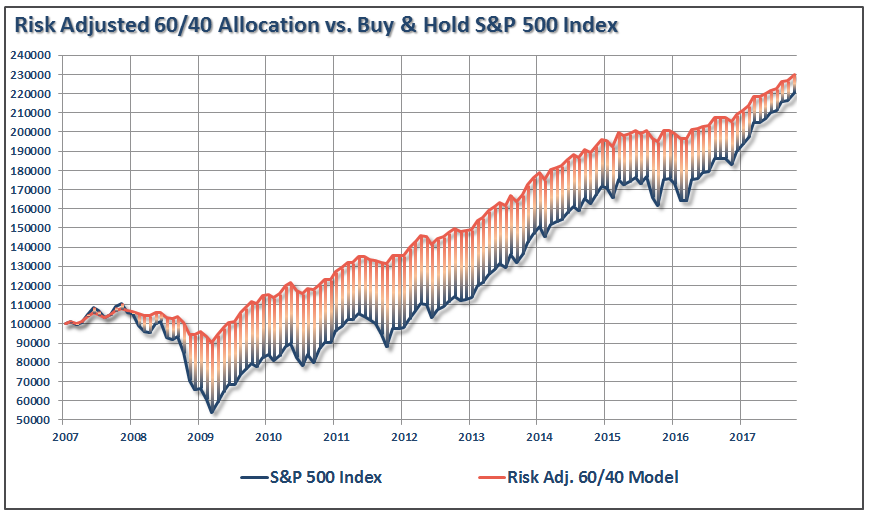

I have constructed an analysis of the model above showing a 60/40 stock/bond allocation risk-adjusted as compared to just “buying and holding” an index.

To date, the “buy and hold” crowd still have not made up for the ground they have repeatedly lost along the way. Sure, they made money, but not as much as by just simply managing risk to some degree along the way with significantly reduced volatility.

Importantly, we are all trying to predict the future. No one will ever be right all the time.

Lord knows I have more than once in my career written a “mea culpa,” and I am sure that I will write many more before I am done with this business.

However, what I will never have to do is look at a client across my desk and tell them “not to worry” about the 40% decline in their portfolio.

Yes, you will eventually get back to even if you don’t die first. But, getting back to even is NOT the same as achieving your financial goals.

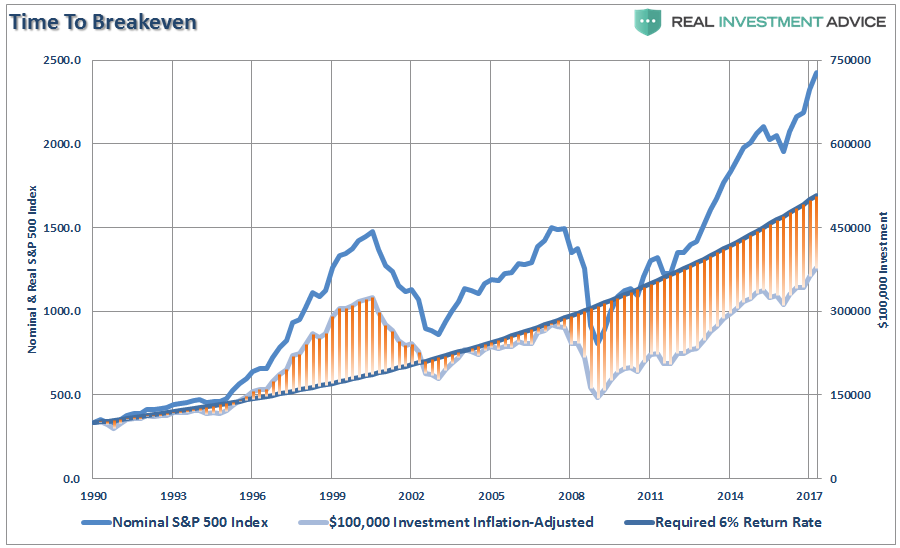

Chasing an arbitrary index that is 100% invested in the equity market requires you to take on far more risk than you most likely want or can afford. Two massive bear markets over the last decade have left many individuals further away from retirement goals than they ever imagined. Furthermore, all investors lost something far more valuable than money – the TIME that was needed to reach their retirement goals.

But when you begin to see and hear the excuses of:

“Well….no one could have seen that coming.”

Just remember, you deserve better.