The first part of our 2022 outlook looks through the front windshield and contrasts 2021s tailwinds with 2022s growing headwinds. While no one knows what 2022 holds in store for investors, our concern is that it should not foster the same optimism as 2021. The economic and financial environments are shifting rapidly making the 2022 outlook much more difficult than this past year.

Part 2 of the 2022 outlook, coming out next week, will cover our thoughts on the stock and bond markets.

“The more extended the advance, and the higher valuations become, the more stable and promising the investment can appear to be, when judged through the rearview mirror.” John Hussman

It’s All About Growth

Before looking forward, it’s worth explaining how economists assess economic activity.

Most economic activity is measured in percentage growth terms and not nominal terms. To stress the importance of this nuance, consider the following:

If the government gives consumers $1 trillion to spend, it will boost GDP by at least $1 trillion. In our example, the stimulus will boost GDP to $21 trillion from $20 trillion, equating to 5% growth. Without government stimulus and excluding any new economic activity, GDP will retreat to $20 trillion in the following year. As a result, GDP will decline by 5%. While nothing changed with the economy, the 5% decline will be considered a recession. To avoid zero or declining economic growth, again assuming no other activity, the government will need to provide at least $1.01 trillion of stimulus.

As we show above, stimulus boosts economic activity. However, it detracts from economic growth rates unless it grows each year. This fact will become important in our 2022 outlook as the government will not likely replicate the massive amount of stimulus doled out over the prior two years. Can the economy make up for it?

Covid TailWinds

In hindsight, the rearview mirror showing the period from March 2020 to the present paints an unusual picture. What started so poorly ended up being one of the greatest periods for investors. The S&P 500 total return since the March 2020 lows is +115%.

In March 2020, the sky was falling, and investors aggressively sold stocks. It turns out buying stocks in the face of such a unique calamity was the right thing to do. The justification was not a coming cure or vaccine for Covid or an imminent return to normal, but the government with their fiscal guns blazing.

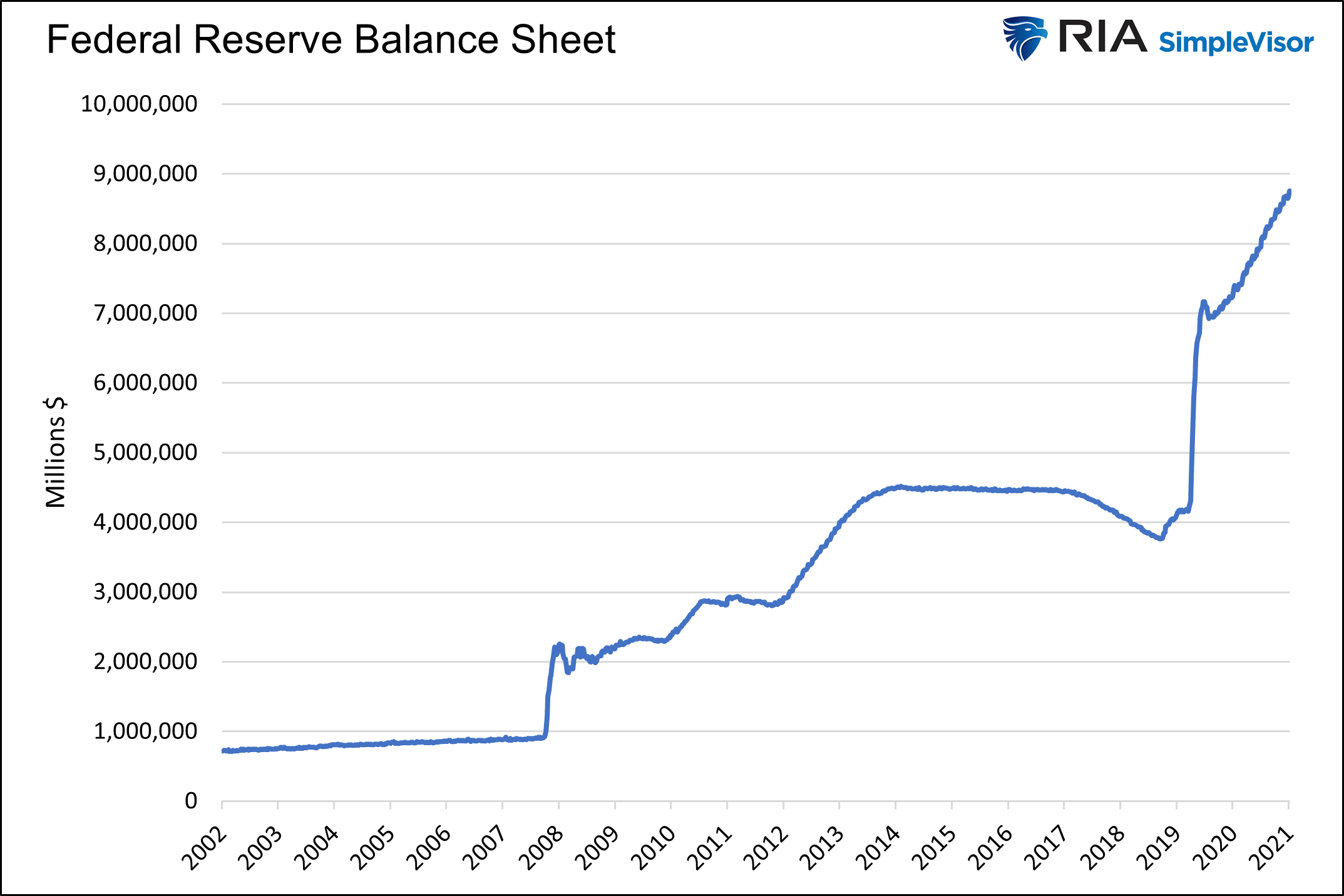

Since March 2020, the government has run a $5.6 trillion deficit, dwarfing any prior instance. Such massive spending was only possible with the Treasury’s trusty sidekick, the Federal Reserve.

As we show, the Fed has bought nearly $5 trillion of bonds since the pandemic began. In doing so, it came close to absorbing 100% of the net new debt issuance from the government.

While the government was doling out money to boost economic activity, the Fed spewed liquidity, supported asset prices, and kept interest rates low. Despite Covid shutting down large segments of the economy, economic data quickly recovered to pre-Covid levels.

Record low interest rates, massive consumer and corporate stimulus, and enormous liquidity gusted at investors’ backs producing double- and triple-digit gains. Not only did most asset prices regain March 2020 levels, but many have well surpassed those levels.

In the latter half of 2021, vaccines, increased consumer demand, and a record amount of savings added further oomph to the tailwinds. However, the ominous winds of inflation began picking up at that point.

2022 Headwinds

The perfect fiscal and monetary storms are petering out. As a result, headwinds for 2022 are mounting. Let consider how that weighs on our 2022 outlook.

Fiscal Spending

Over the last 3 months, the federal deficit grew at a $1.6 trillion annualized rate. That is historically high but well below 2020 and 2021 levels. Further, Joe Biden and the Democrats are struggling to pass the Build Back Better (BBB) social infrastructure program. We think it will pass in time, but the fiscal stimulus and spending related to it will not be as immediate or significant as initially planned.

The coming election in November poses more hurdles for spending bills. West Virginia Senator Joe Manchin and other Senators and Representatives from red and purple states face a growing risk of losing their seats. Some may take a page from Manchin’s playbook and voice deep concern for growing budget deficits to appease their voting bases.

Throughout later 2021 and even into 2022, Covid related stimulus programs ended or will end shortly. The closure of these programs will further reduce the flow of stimulus to consumers. For example, the recently extended student loan deferment program ends in a few months. In this case, many student debtors consume goods and services with money that should be servicing student debt. Once the deferment period ends, spending, in many cases, will decline. The child tax credit will also end shortly, resulting in a shortfall of funds for those receiving the benefit. Likewise, those that did not pay rent are now left with back payments or higher rents to make their landlords whole.

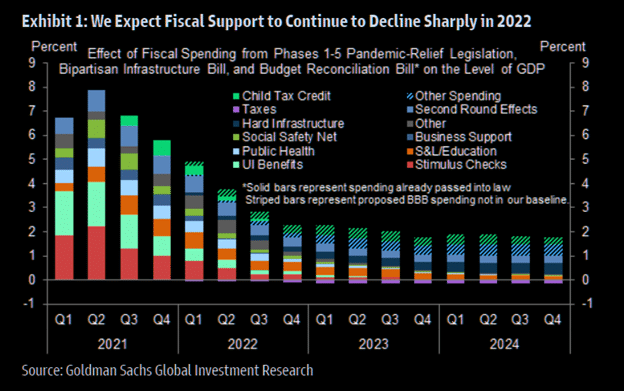

The graph below from Goldman Sachs helps quantify the sharp decline in fiscal spending related to the pandemic.

As we discuss later, the savings rate has fallen back to normal levels, meaning many of those affected will have to reduce consumption.

Monetary Stimulus

The Fed is tapering QE, expecting to end new purchases by March 2021. QE provides vast amounts of liquidity to the financial markets. As the Fed backs away, not only will it reduce liquidity to markets, but reduce the power of the world’s largest holder of U.S. Treasury debt. Someone will take the Fed’s place but must shed other assets to do so.

To help better understand this concept, we suggest reading The Fed Is Juicing Stocks. In particular, the section titled “Draining the Asset Pool.”

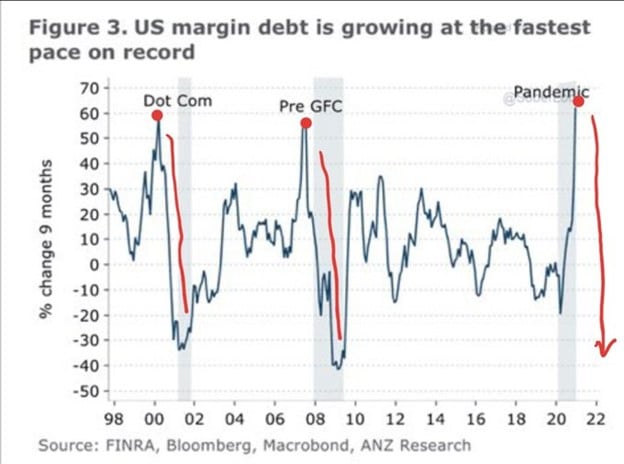

The Fed is also hinting at raising interest rates. Higher interest rates will increase interest expenses for debt-laden companies, consumers, and the government. Additionally, those using loans to leverage assets will have to pay more for the leverage. This will undoubtedly cause some investors to reduce or remove leverage as the potential returns diminish.

The graphs below highlight that margin debt has proliferated and sits at or near record levels. The last two times margin debt grew this rapidly was in 1999 and 2007.

Elections and the Fed

Further pressuring the Fed is politicians. Consider the following from the Financial Times:

“The Fed needs to start tapering immediately and then they need to raise interest rates. Both those things can be done by March,” Jake Auchincloss, a Democrat from Massachusetts and member of the House of Representatives financial services committee, which oversees monetary policy, told the Financial Times. “I think chair [Jay] Powell would do well to end the decade of easy money,” he added.

Political pressure from the President and legislators may force the Fed to remove liquidity too quickly or raise rates too fast. Both are likely to be problematic for asset prices and economic recovery.

Savings Rate

The combination of direct government stimulus and the inability to spend money during the lockdowns resulted in unprecedented savings rates. As we show below, the savings rate jumped to levels that were twice as high as any previous level since at least 1959. Note that the two recent peaks result from the two rounds of personal stimulus checks.

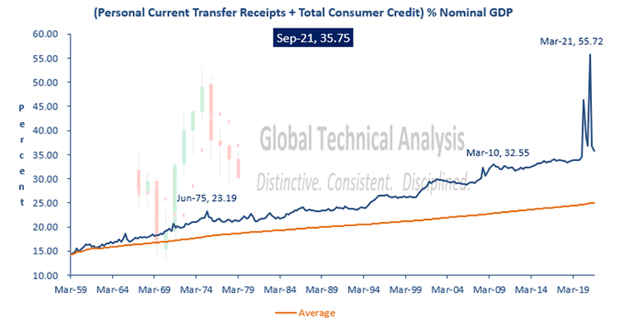

The following graph, courtesy of Brett Freeze, shows how government stimulus to consumers (transfer receipts) and credit provided a bonanza of spending power for consumers. Like the bloated savings rate above, that too has normalized.

The savings rate is back to pre-Covid levels. Most consumers, especially those in the middle to lower-income classes, have fully exhausted extra savings and must either reduce spending or increase their use of debt.

Credit card debt and home equity withdraws are both increasing. While such funds can propel additional spending, it will not be nearly the same as the enlarged savings rates. Further, higher interest rates will make debt less appealing. Inevitably credit card and home equity are limited based on wage growth and the ability to service their debt.

Inflation

Prices are on the rise. Higher prices mean consumers spend more to get the same amount of goods. If wages keep up with inflation, the consumer is indifferent.

Inflation is running at 6.9%, over three times higher than the Fed’s stated 2% objective. At the same time, wages are growing but at a lesser rate than inflation. Average hourly earnings are up 4.8%. While historically robust, real wages, factoring in inflation, are down 2%.

As we note earlier inflation is pressuring the Fed to prioritize their fight against inflation. Might the Fed have to choose between inflation and asset prices? Ohio Democrat Sherrod Brown recently shared thoughts on that- “The Fed should make sure our economy works for workers and their families, not Wall Street.”

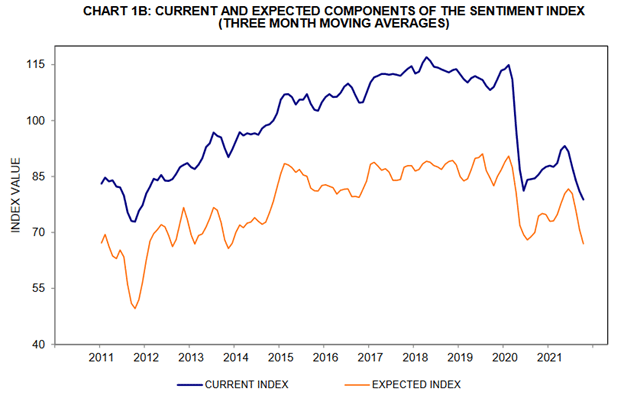

Also, consider inflation is highly responsible for the recent string of poor consumer sentiment. People usually spend more when they have a positive outlook. As the graph below shows, the University of Michigan’s current and expected consumer sentiment indexes are at or near ten-year lows. The current index sits at 70.6. In April 2020, during the peak of Covid lockdowns, it was 71.8. In September 2008, when Lehman and others were failing, it was 70.3.

Pent up Demand and Mid-Life Crisis

Having been deprived of vacations, eating out, and a host of other activities, people were hungry to return to normal. Vaccines further raised comfort levels and allowed many stores and venues to return to normal.

Consumers splurged as they bought those things they couldn’t buy during lockdowns. Not only did they travel and go out to dinner, but some bought cars and houses and other big-ticket items. It was as if many consumers had a mid-life crisis simultaneously.

Most of that pent-up demand is quickly diminishing. The bills from those spending sprees are mounting, and life is slowly becoming more normal by the day. This additional source of spending is fading quickly.

Summary

“Prepare for the unknown by studying how others in the past have coped with the unforeseeable and the unpredictable.” -George S. Patton

As you just read in part one of our 2022 outlook, this year’s monetary and economic environment will not be as friendly for asset prices as last year. While that may seem problematic for investors, if we learned anything in 2020 and 2021, it is that stock prices can climb a wall of worry efficiently.

In part two of our 2022 outlook, coming next week, we share our thoughts on how stocks and bonds might perform in the new year.