Inside This Week’s Bull Bear Report

- The One-Two Punch Knocks Out The Bulls

- Powell’s Testimony Kills Pivot Hopes

- How We Are Trading It

- Research Report – Bullish Investors Continue To Fight The Fed

- Youtube – Before The Bell

- Stock Of The Week

- Daily Commentary Bits

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

The One-Two Punch Knocks Out The Bulls

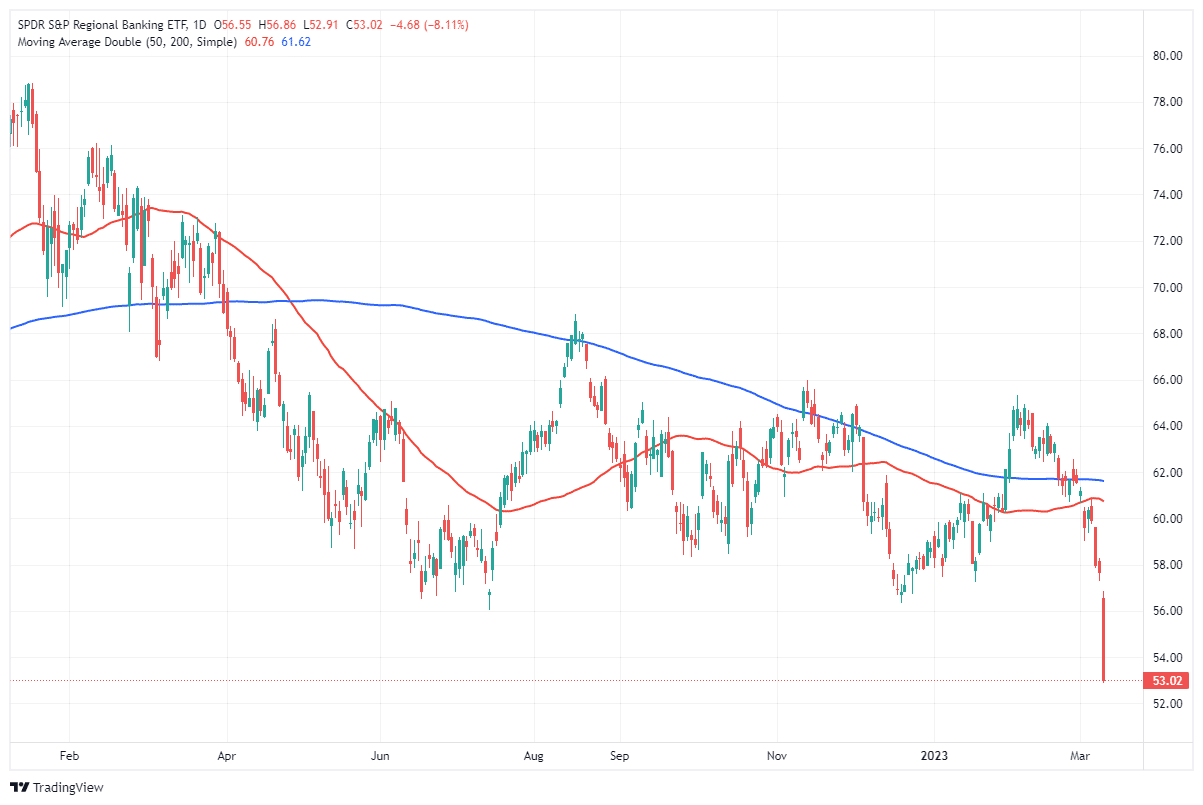

This past week, the market took a double whammy from Jerome Powell’s testimony and concerns about a crack in the regional bank sector. We discussed the latter in yesterday’s Daily Market Commentary (subscribe for daily pre-market delivery).

“Yesterday, news that SVB Financial Group was taking “steps to bolster its financial position.” That included a highly dilutive stock offering and a panicked asset sale that sparked fears of a liquidity crisis at one of the biggest and original funding providers to the Venture Capital industry. The fear spread through other regional banks as a concern of “one roach in the kitchen” may mean a lot more at risk. The ETF of Regional Banks (KRE) dropped sharply.”

The crack in regional banks is likely only starting as the Fed continues to hike interest rates, leading to more underperforming loans and reduced funding. Unlike the big banks, which have access to capital markets and trading revenues to offset traditional banking incomes, smaller banks have exposure to real estate, consumer, and small business loans that are more sensitive to increased borrowing costs.

“Banks – and especially small banks – are now sitting with reserves pretty much at their lowest comfort level, There is not much of a cash-to-asset cushion left for small banks as a whole, so a funding crisis can easily get rolling if large depositors decide too many loans in commercial real estate and other areas are about to go bad. The Fed will make funds available to keep these banks afloat, but that alone will get some push-back from Congress because of the increased concentration of bank deposits in an increasingly smaller number of banks.” – Steven Blitz, TS Lombard

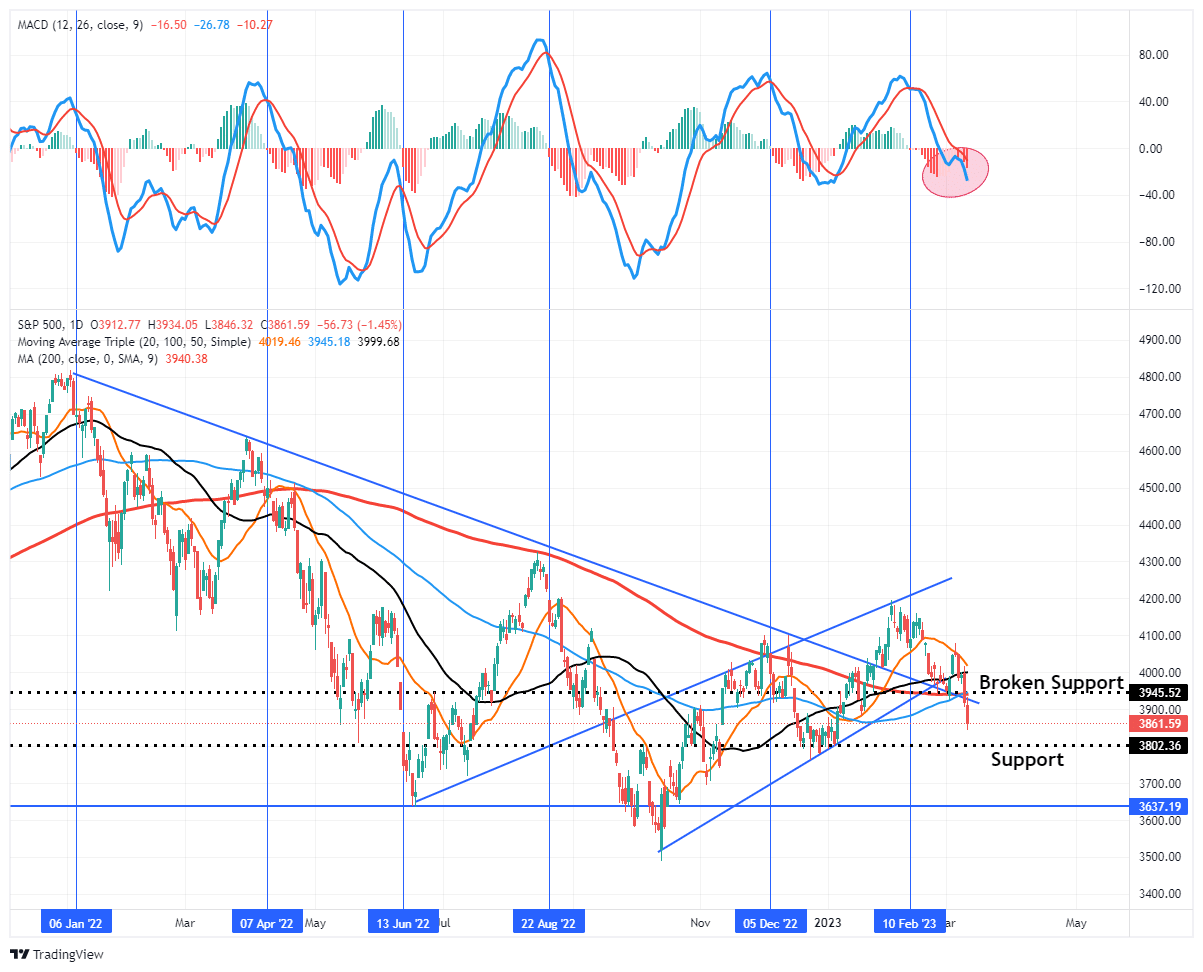

With that, the market took out the support at the rising trend line and the 200-DMA, which violated our stop-loss levels, where we reduced exposure to equities. With all of the previous bullish support levels broken, the next logical level of support is the December lows. A failure there will then set supports at the June and October lows.

The one-two punch of Jerome Powell and SVB has put the bears back in control of the market. Unfortunately, the problem for the regional banks, corporate earnings, and the market was found in Powell’s testimony this past week.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Powell’s Testimony Kills Pivot Hopes

This week was the annual testimony of the Federal Reserve before the Senate Banking Committee, followed by the House Financial Services Committee. As expected, Jerome Powell’s testimony tilted to a more “hawkish” posture, given that inflation has not subsided as quickly as hoped.

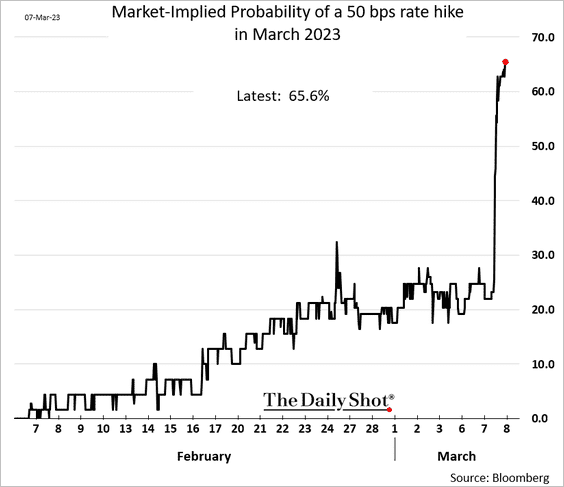

During his testimony to the Senate Banking Committee, Powell made two critical statements that sent stocks tumbling on Tuesday.

“If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”

That statement sent the odds of a 0.50% increase at the March meeting to nearly 70%. Just a month ago, those odds were ZERO.

While a more aggressive rate hike in March was certainly not what the markets wanted to hear, the following testimony killed the hopes for a “pause.”

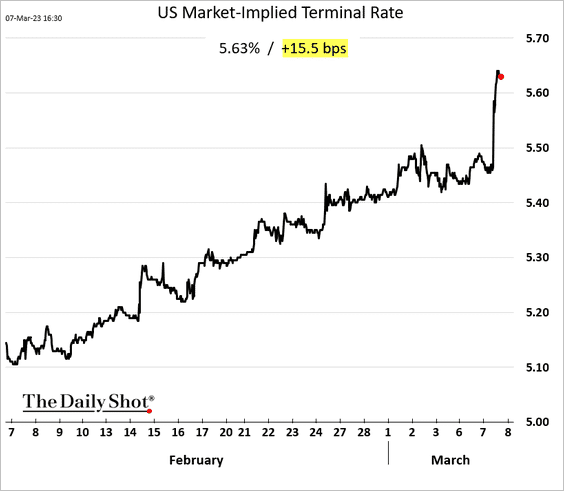

“The latest economic data have come in stronger than expected, suggesting that the ultimate interest rate level is likely to be higher than anticipated.”

Much of the rally in stocks from the October lows was based on the hope the Fed would cease, or pause, its aggressive rate-hiking campaign. Many investors started to equate a “pause” to an immediate “pivot” where a reversal to monetary accommodation would be equity friendly.

Unfortunately, Powell’s testimony demolished that hope, sending “terminal rate expectations,” the level where the Fed will cease hiking, to 5.6%.

While that terminal rate and the odds of a 0.50% March rate hike decreased on Friday, the estimates still range between 5.25% and 6%.

While “video killed the radio star,” Powell’s testimony, and the SVB debacle, dashed the bullish dreams for now.

No Recession?

Powell’s testimony reaffirms our previous expectations that the Fed would “break something” which may have started with SVB. However, it is too soon to tell whether this was an isolated event or the beginning of a credit event.

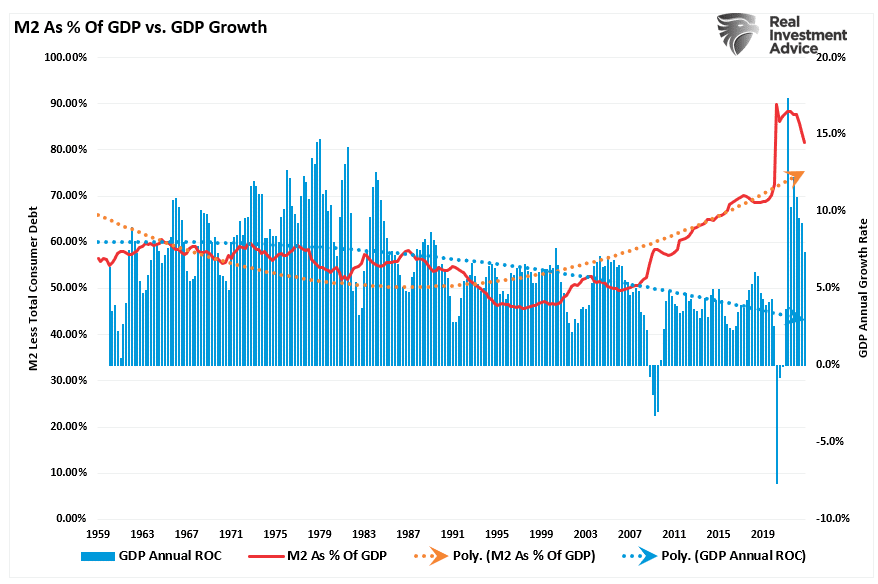

The problem between the bears and the bulls is that the economy still shows plenty of strength, from recent employment numbers to retail sales. However, much of this “strength” is an illusion from the “pull forward” of consumption following the massive fiscal and monetary injections into the economy.

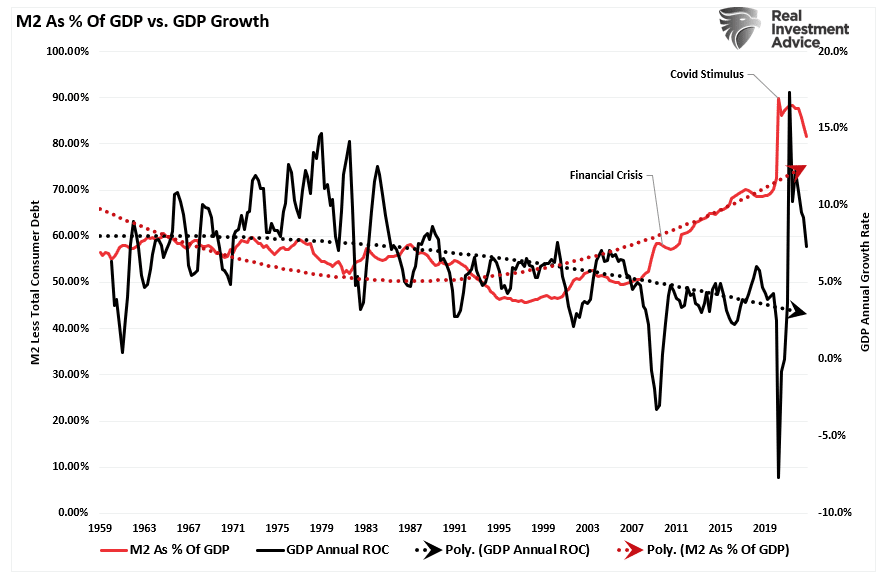

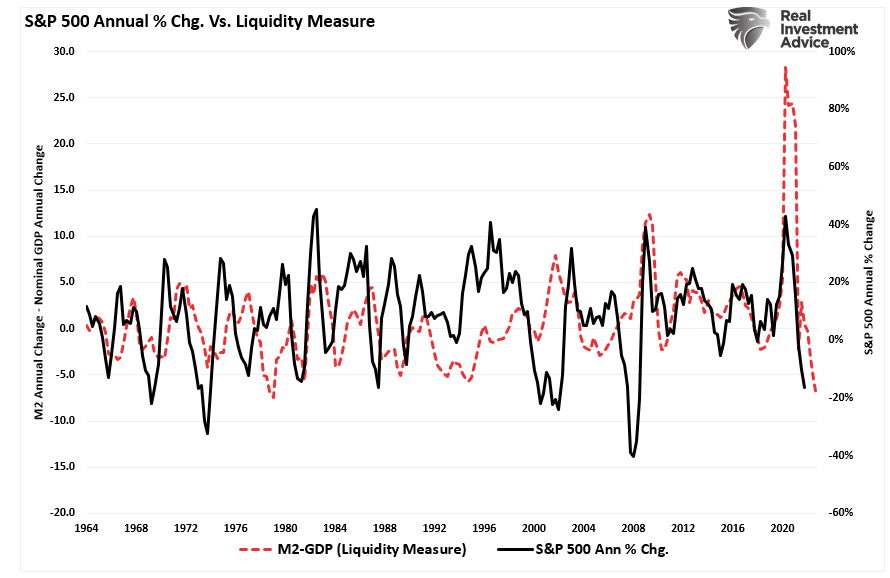

As shown, M2, a measure of monetary liquidity, is still highly elevated as a percentage of GDP. This “pig in the python” is still processing through the economic system. Still, the massive deviation from previous growth trends will require an extended time frame for reversion. Such is why calls for a “recession” have been early, and the data continues to surprise economists.

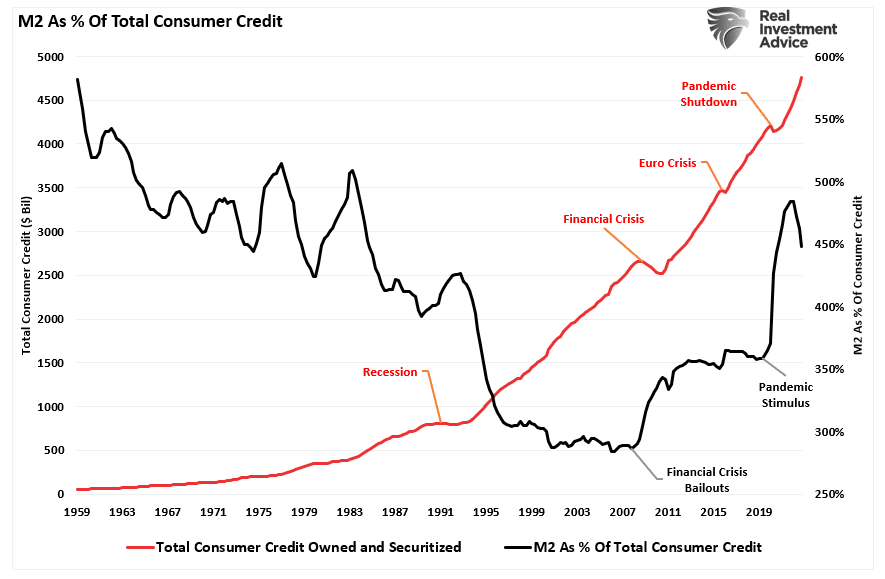

Given that economic growth is comprised of roughly 70% consumer spending, the ramp-up in debt to “make ends meet” as that liquidity impulse fades is not surprising. You will note that each time there is a liquidity impulse following some crisis, consumer debt temporarily declines. However, the inability to sustain the current standard of living without debt increases is impossible. Therefore, as those liquidity impulses fade, the consumer must take on increasing debt levels.

Monetary & Fiscal Policy Is Deflationary

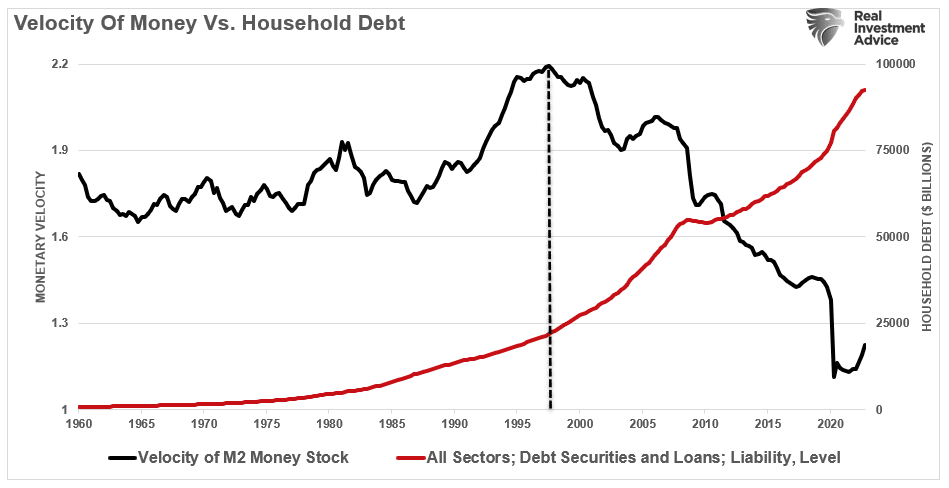

The problem is that the Federal Reserve and the Government fail to grasp that monetary and fiscal policy is “deflationary” when “debt” is required to fund it.

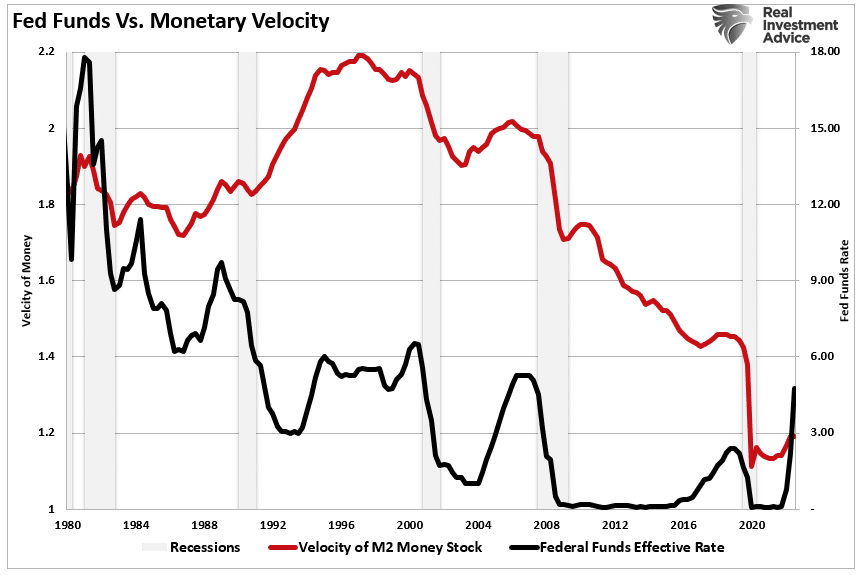

How do we know this? Monetary velocity tells the story.

What is “monetary velocity?”

“The velocity of money is important for measuring the rate at which money in circulation is used for purchasing goods and services. Velocity is useful in gauging the health and vitality of the economy. High money velocity is usually associated with a healthy, expanding economy. Low money velocity is usually associated with recessions and contractions.” – Investopedia

With each monetary policy intervention, the velocity of money has slowed along with the breadth and strength of economic activity. While, in theory, “printing money” should lead to increased economic activity and inflation, such has not been the case.

Beginning in 2000, the “money supply” as a percentage of GDP exploded higher. The “surge” in economic activity is due to “reopening” from an artificial “shutdown.” Therefore, the growth is only returning to the long-term downtrend. The attendant trendlines show that increasing the money supply has not led to more sustainable economic growth. It has been quite the opposite.

Moreover, it isn’t just the expansion of M2 and debt undermining the economy’s strength. It is also the ongoing suppression of interest rates to try and stimulate economic activity. In 2000, the Fed “crossed the Rubicon,” whereby lowering interest rates did not stimulate economic activity. Therefore, the continued increase in the “debt burden” detracted from it.

It is worth noting that monetary velocity improves when the Fed hikes interest rates. Accordingly, Powell’s testimony says the Fed will do just that.

Interestingly, monetary velocity improves just before the Fed “breaks something.”

Recession Risks

Powell’s testimony is clear that the Fed will continue hiking rates to combat inflation. However, such will increase the risks that the Fed will eventually “break something.” Many “recession indicators” are already ringing alarm bells, from inverted yield curves to various manufacturing and production indexes. But there are two we watch most closely.

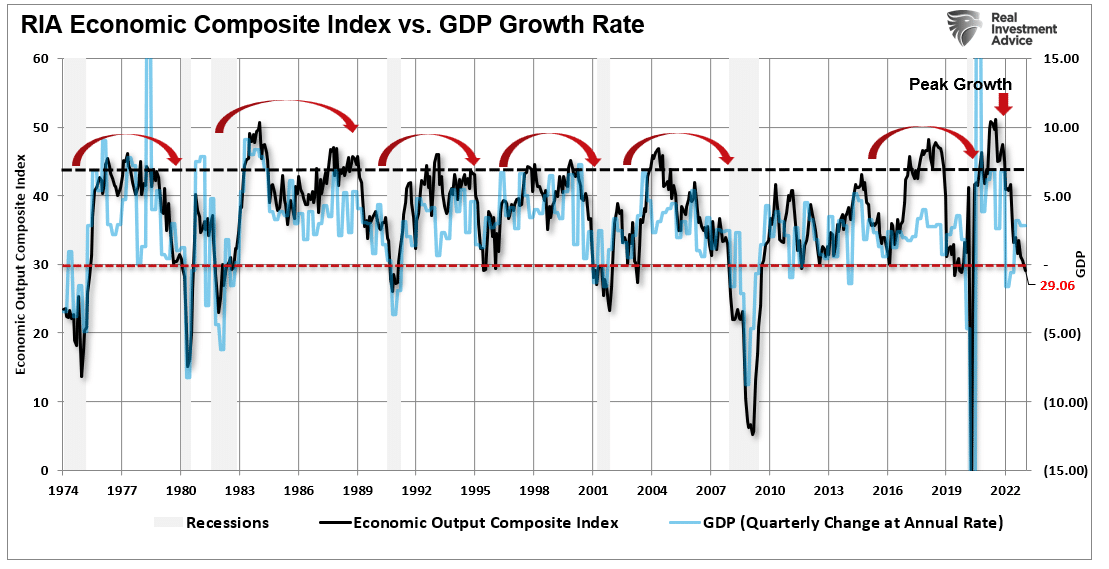

The first is our composite economic index comprising over 100 data points, including leading and lagging indicators. Historically, when that indicator has declined below 30, the economy was either in a significant slowdown or recession. Just as inverted yield curves suggest that economic activity is slowing, the composite economic index confirms the same.

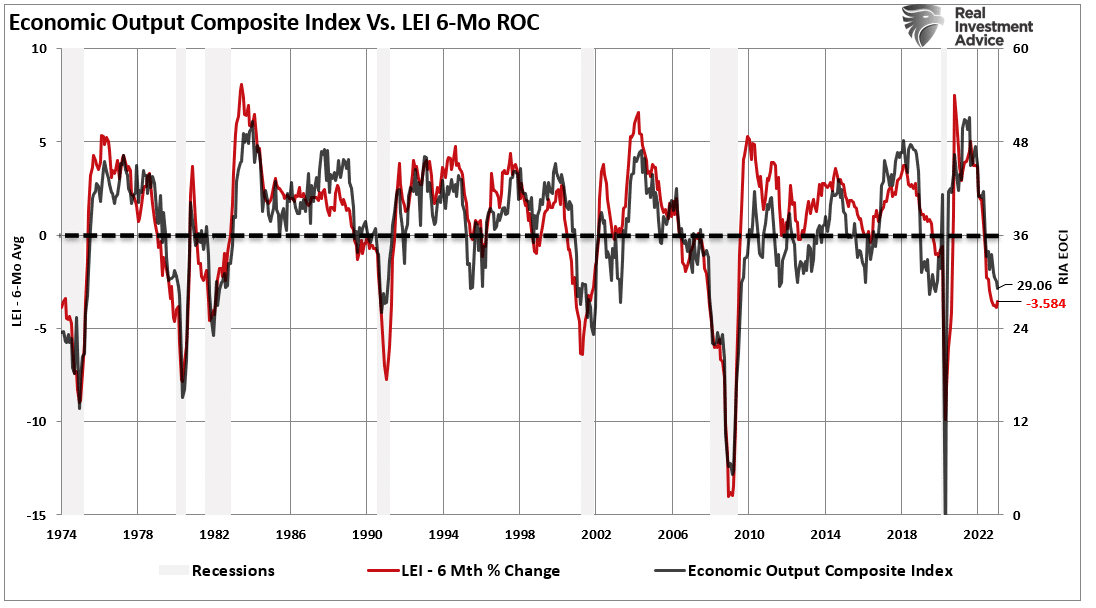

Secondly, the 6-month rate of change of the Leading Economic Index (LEI) also confirms the composite economic index. As a recession indicator, the 6-month rate of change of the LEI has a perfect track record.

Of course, today’s debate is whether these recession indicators are wrong for the first time since 1974. As stated above, the massive surge in monetary stimulus (as a percentage of GDP) remains highly elevated, which gives the illusion that the economy is more robust than it likely is.

Those economic data points support the Fed’s testimony of keeping rates elevated longer. The risk, however, is the lag effect of monetary tightening. As previous rate hikes take hold this year, the reversion in economic strength will probably surprise most economists.

For investors, the implications of reversing monetary stimulus on prices are not bullish. As shown, the contraction in liquidity, measured by subtracting GDP from M2, correlates to changes in asset prices. Given there is significantly more reversion in monetary stimulus to come, such suggests that lower asset prices will likely follow.

Of course, such a reversion in asset prices will occur as the Fed “breaks something” by over-tightening monetary policy.

How We Are Trading It

As noted last week, from a portfolio management perspective, we are caught between the improving bullish technicals and the bearish fundamentals. That obviously changed this past week, and longer-term, the fundamentals always win out. According to Powell’s testimony, it is hard to imagine a scenario where continued rate hikes do not eventually cause an economic recession or further bank failures.

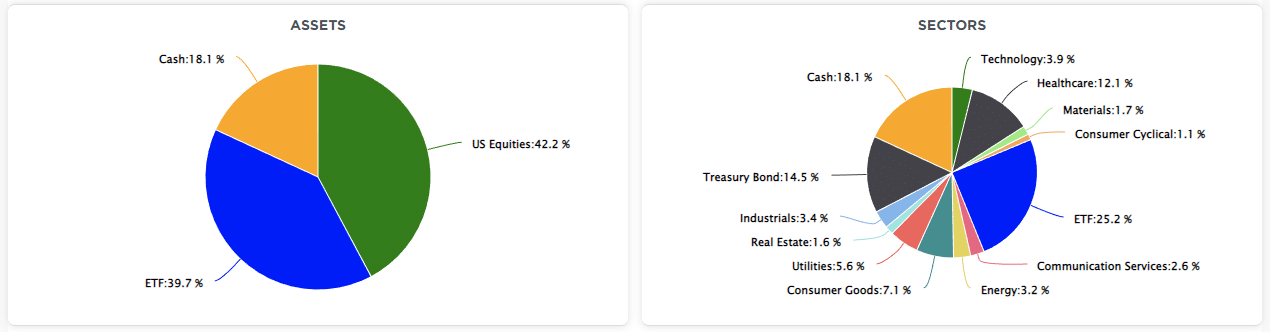

From that view, we remain underweight in stocks and bonds and overweight cash and short-term Treasuries. (The ETF allocation comprises short-duration Treasury bonds and floating rate Treasuries, with a lesser allocation to long-dated Treasuries. You can view our models in real-time at SimpleVisor.com) However, we will now start to increase the duration of our bond portfolio.

As noted last week:

“There is little reason to chase risk, particularly ahead of the upcoming FOMC meeting later this month. We expect the Fed to hike interest rates by another 0.25%, but their language regarding further rate hikes will remain hawkish. The inflation data remains “sticky,” and the employment data, although lagging, remains too strong for the Fed to stop hiking rates.

That data has pushed market-based expectations to 5.5% for the terminal rate, and rate cuts are now getting pushed off into the latter part of this year. Such does not bode well for risk assets or economic growth.”

Such is what we saw happen this past week. While the bulls continue to ignore the impact of further rate increases, it is a war the bulls will eventually lose. As such, we suggest using any rallies to reduce equity risk, raise cash levels, and rebalance bond portfolios. The opportunity to increase equity risk will come, but such could be later this year.

While being cautious will likely underperform near term, reducing capital destruction allows for a quicker return to profitability.

Have a great week.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates (Formerly 3-Minutes)

We have set up a separate channel JUST for our short daily market updates. Be sure and subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our Youtube Channel To Get Notified Of All Our Videos

Stock Of The Week In Review

A few subscribers have recently asked if we could screen for stocks offering good dividends and stable stock prices. They are concerned about the broad equity markets but do not want to over-allocate to T-bills or money market funds despite their risk-free status and tempting 5% yields.

To help answer the request, we use Finviz. They provide the ability to screen for volatility. Unfortunately, Finviz only allows us to filter volatility for the last month. To help compensate, we added low Beta to the screen. Lastly, we only include stocks with dividend yields of 3% or greater and added a size requirement.

Here is a link to the full SimpleVisor Article For Step-By-Step Screening Instructions.

Login to Simplevisor.com to read the full 5-For-Friday report.

Daily Commentary Tidbits

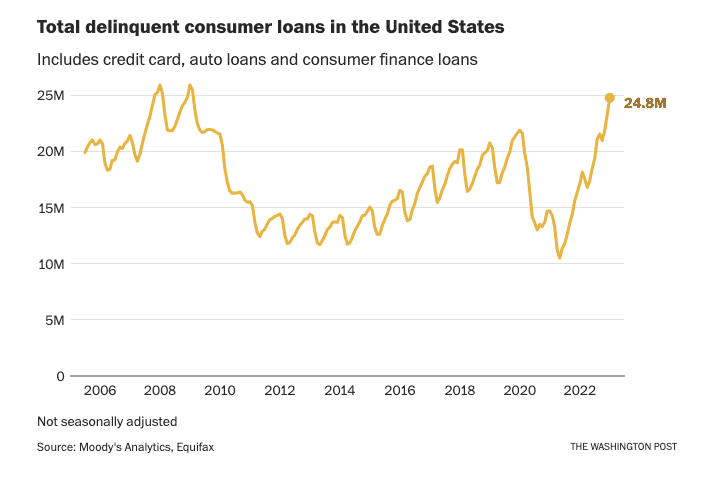

Delinquent Consumer Loans On The Rise

The chart below showing delinquent consumer loans is concerning but misleading. At first blush, the number of delinquent consumer loans is nearing the peak of the 2008 recession. That stat should be very worrisome on its own. However, the amount of consumer loans has more than doubled since 2008. Therefore, the percentage of delinquent consumer loans is only half of the 2008 peak.

While the percentage of delinquent consumer loans is not problematic, the sharply rising trend is. Further, Heather Long of the Washington Post notes, “Many households are also behind on their utility bills: 20.5 million homes had overdue balances in January, according to the National Energy Assistance Directors Association.” Per the article, the bottom 60% of earners contribute about 40% of GDP growth. People delinquent on loans are likely getting financially squeezed due to falling real wages and will be forced to reduce their consumption. If the unemployment rate rises, the problem will worsen. The article ends as follows: “The flares are going off. If the economy does fall into a recession, it will only get more perilous for those at the bottom.“

Click Here To Read The Latest Daily Market Commentary (Subscribe For Pre-Market Email)

Bull Bear Report Market Statistics & Screens

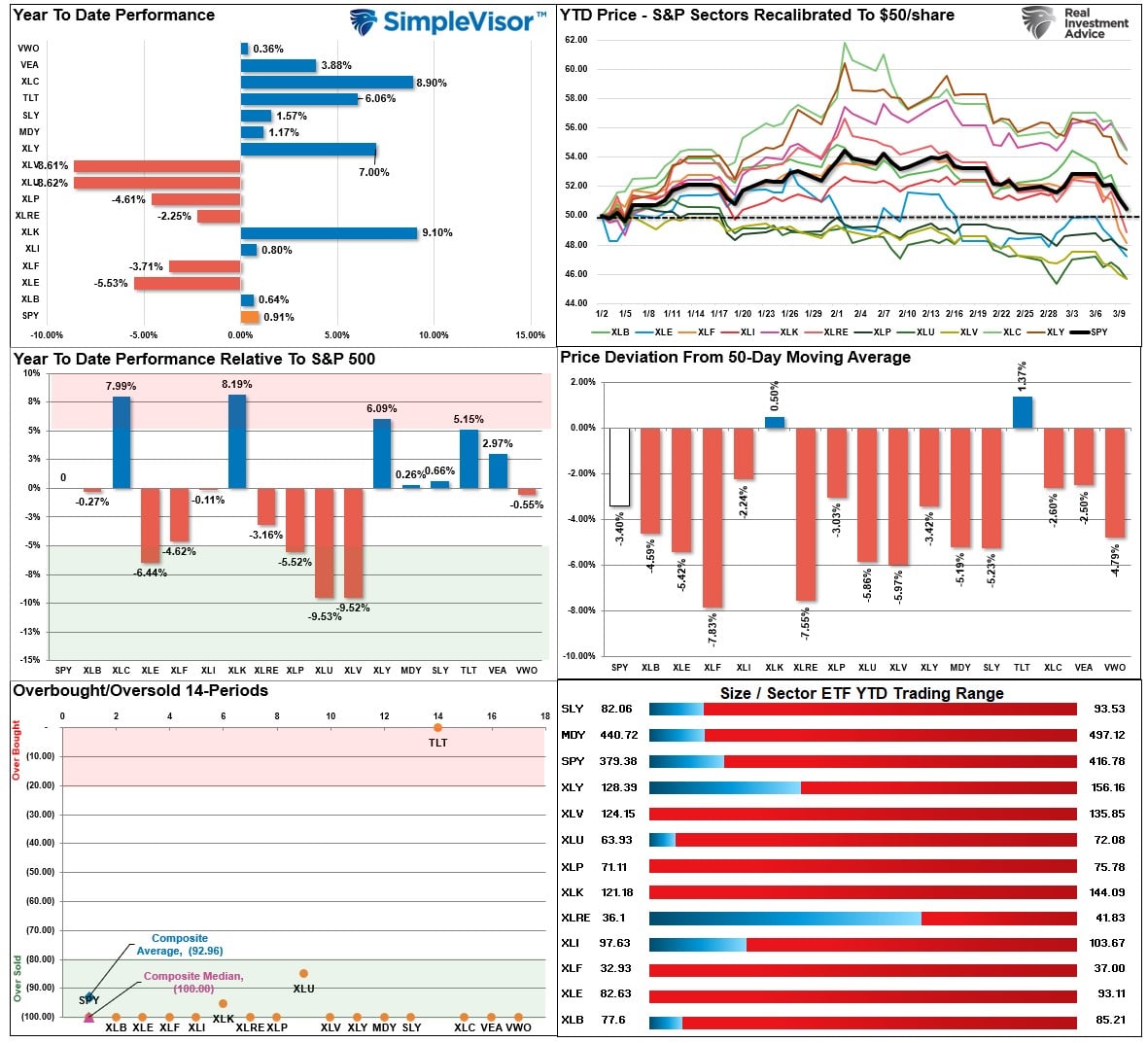

SimpleVisor Top & Bottom Performers By Sector

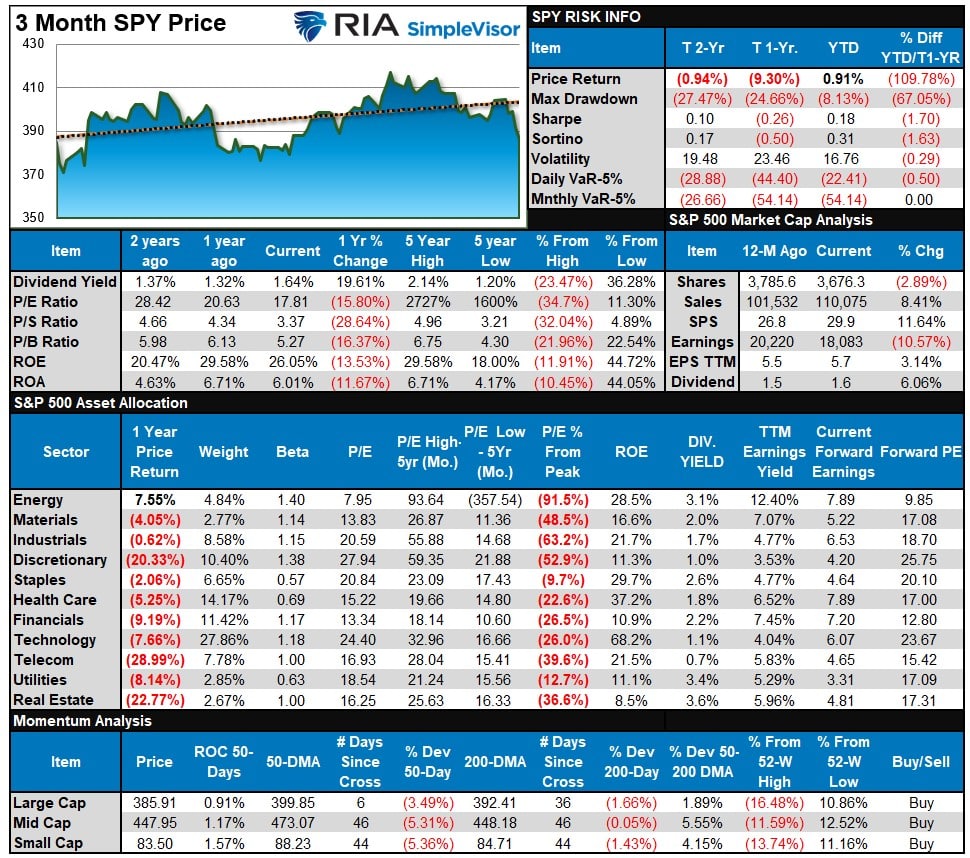

S&P 500 Weekly Tear Sheet

Relative Performance Analysis

The one-two punch of Powell’s testimony and the failure of Silicon Valley Bank to the wind out of the bull market this past week. The market is short-term oversold in every sector except for Bonds which are now very overbought. Look for a reflexive bounce next week to sell into to raise cash and reduce risk until the bullish trends are retaken.

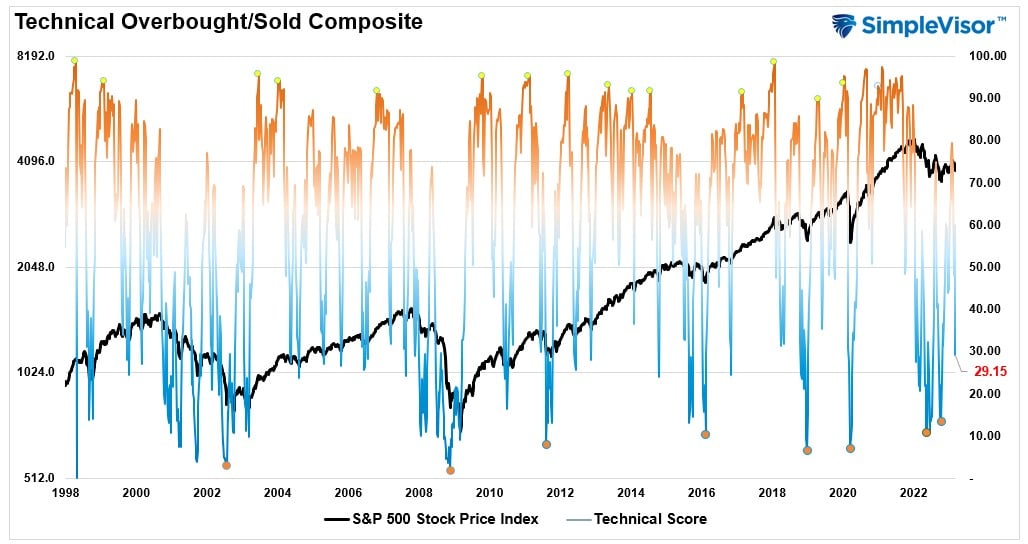

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. Markets peak when those readings are 80 or above, suggesting prudent profit-taking and risk management. The best buying opportunities exist when those readings are 20 or below.

The current reading is 29.15 out of a possible 100.

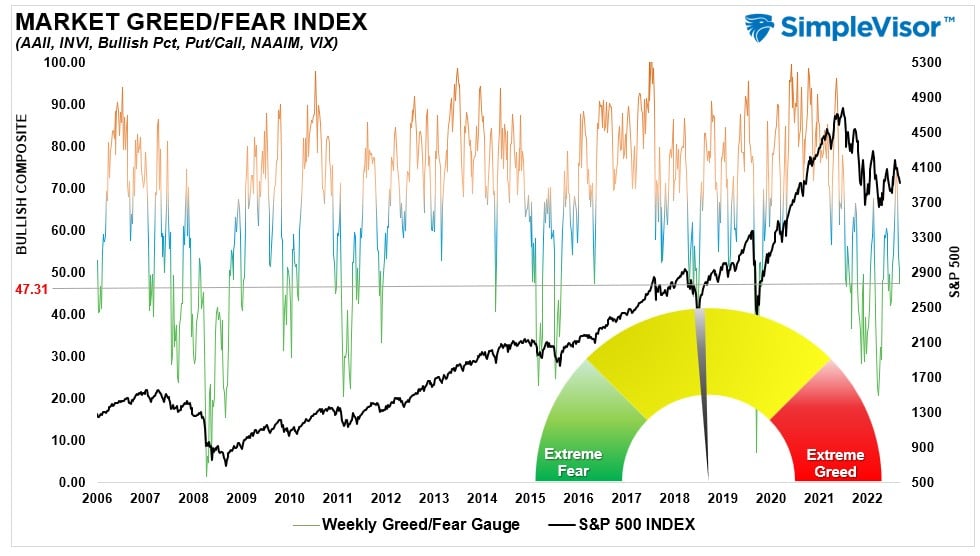

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” Gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 47.31 out of a possible 100.

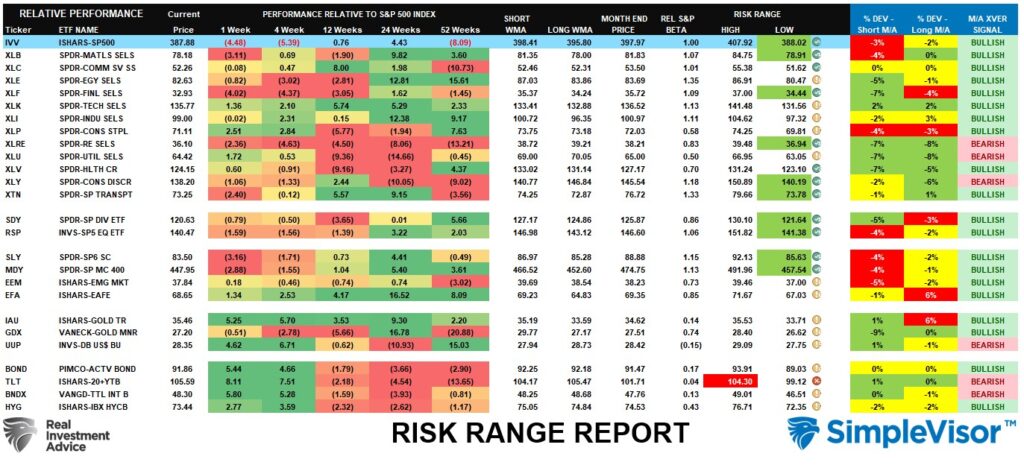

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “M” XVER” “Moving Average Cross Over) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

As noted above, the one-two punch of Powell and Silicon Valley Bank pushed all sectors and markets lower this week. While the bears have regained control of the narrative for now, expect a bounce next week, given the current oversold conditions. Bonds are overbought after a big spike on Friday, so some profit-taking there is advised.

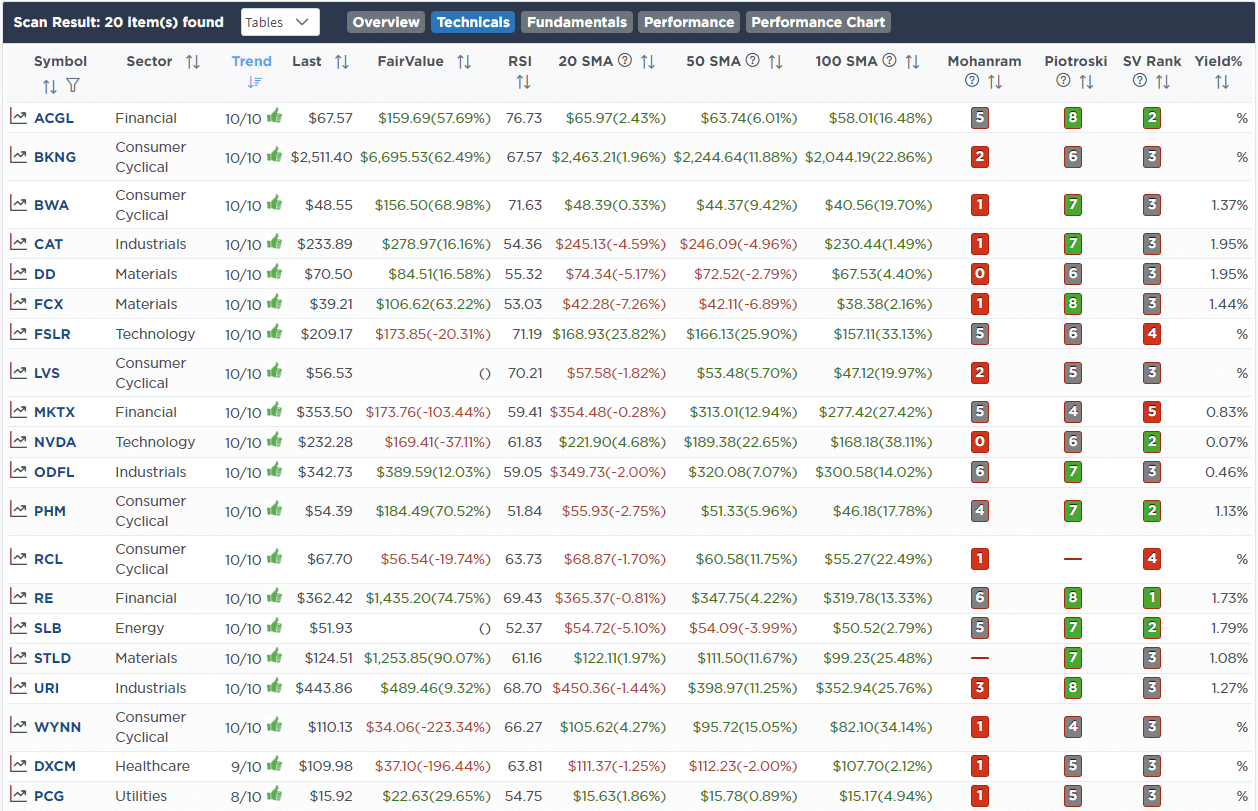

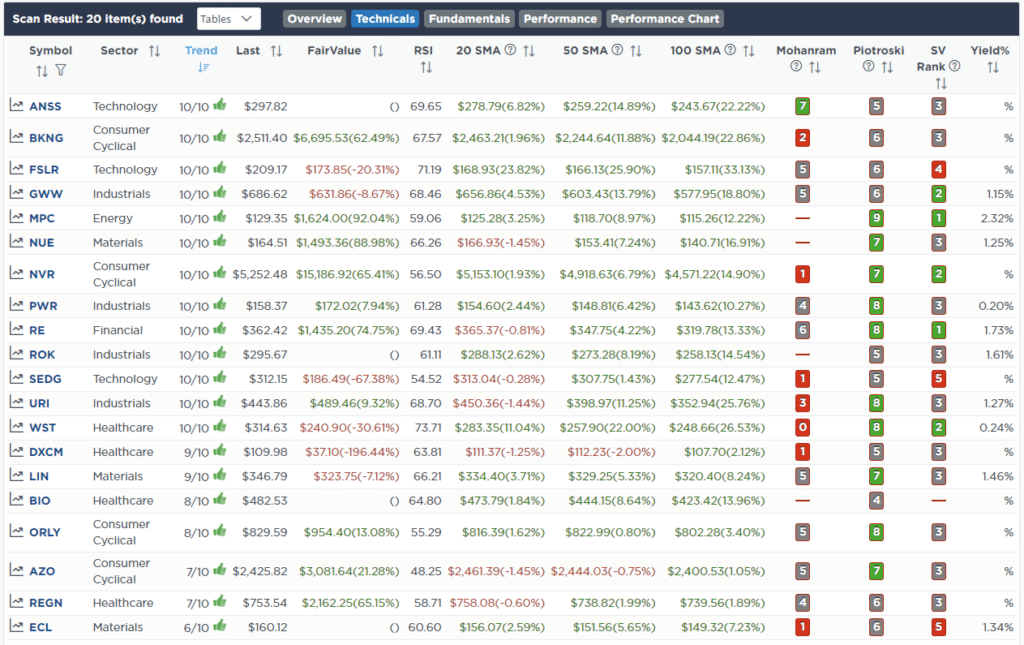

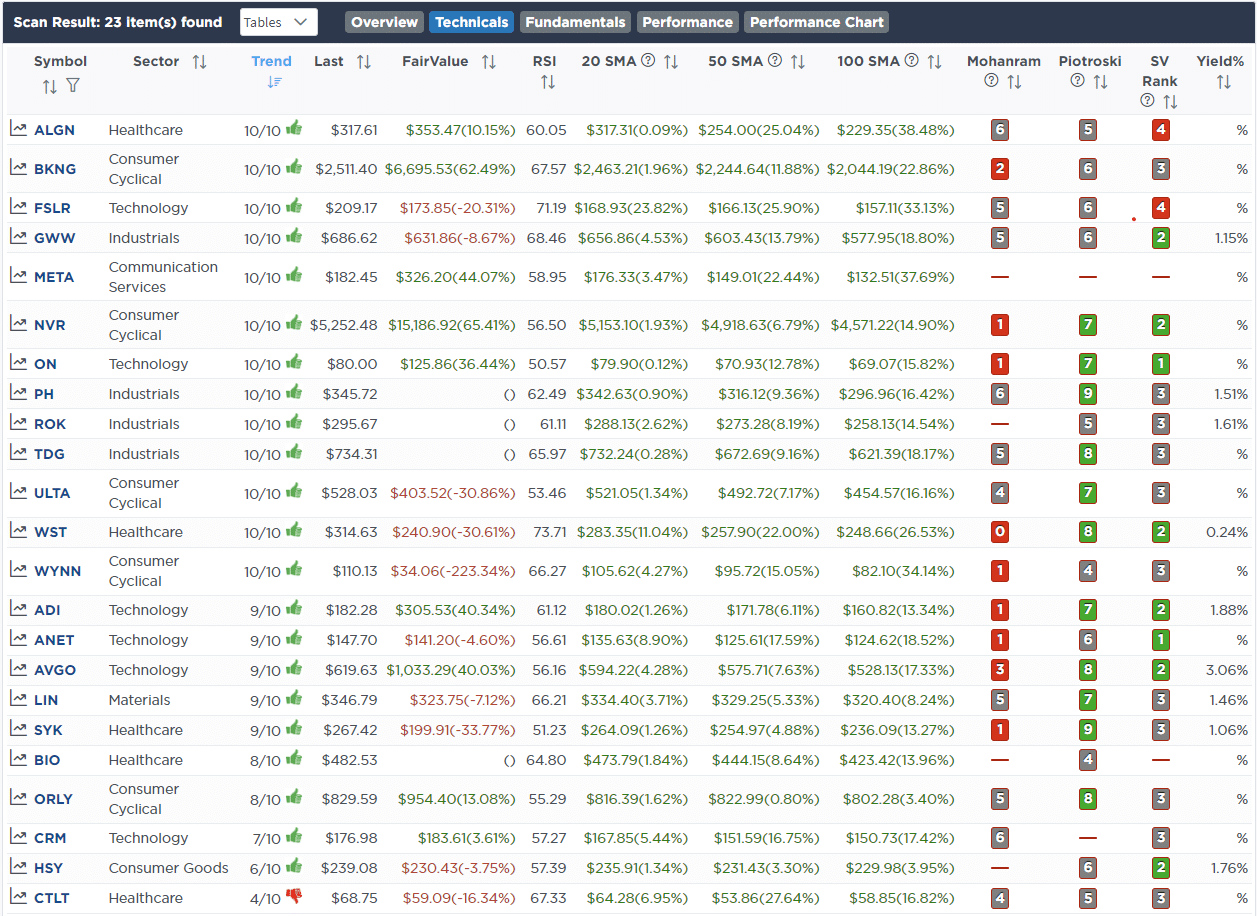

Weekly SimpleVisor Stock Screens

We provide three stock screens each week from SimpleVisor.

This week we are searching for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Fundamental And Technically Strong Stocks

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Fundamental Stocks With Strong Technicals

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

March 7th

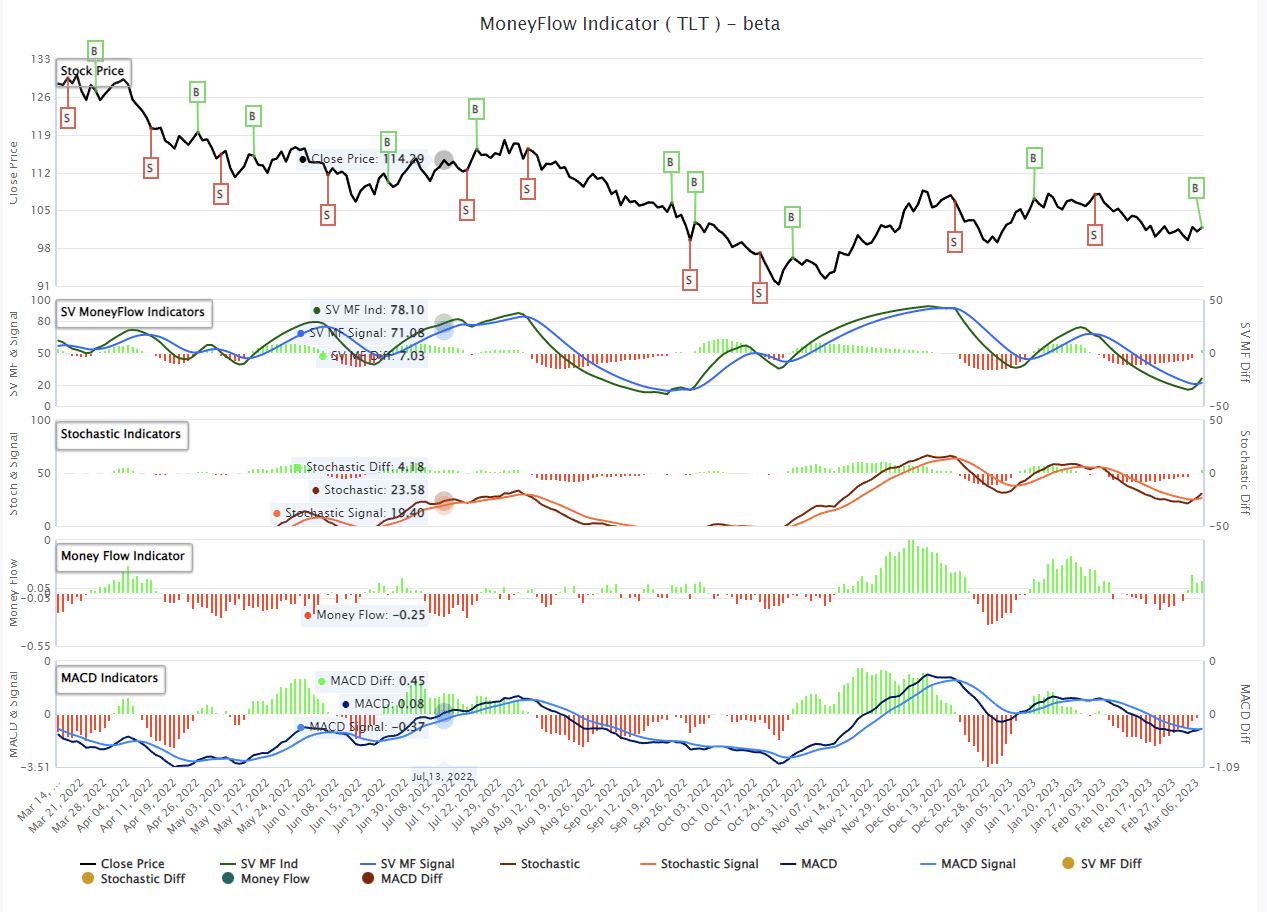

We have recently discussed beginning to shift the duration of our bond holdings to a longer-term time frame in anticipation of economic weakness and an eventual reversal of Fed policy. We started by shifting 1-3 month Treasuries (BIL) to 1-3 year Treasuries (SHY). Today, with our “money flow buy signal”triggering from an oversold level, we are bringing the iShares 20-Year Treasury ETF (TLT) to target weight. We will build on this small move as we continue to slowly lengthen the duration of the overall bond holdings in our portfolios.

Both Models

- Rebalance iShares 20-Year Treasury Bond ETF (TLT) To 10% Of The Portfolio

March 9th

This morning we added 2.5% SPY to both models. We also bought CVS and XLV back up to their model weights.

SPY is closing in on a buy signal. We may ultimately buy 5-7.5% over the next week. Given the risk with the employment report tomorrow and CPI on Tuesday, we decided to leg into the trade. Despite Powell’s hawkishness, we found it encouraging the market held up yesterday and this morning. If we are wrong, there are clear stop levels in various moving averages and the rising lower trend line.

Equity Model

- Initiate a 2.5% position in the S&P 500 Index ETF (SPY)

- Bring CVS Health (CVS) to the model weight of 3% of the portfolio.

ETF Model

- Initiate a 2.5% position in the S&P 500 Index ETF (SPY)

- Bring iShares Health Care ETF (XLV) to the model weight of 8% of the portfolio.

March 10th

As you may or may not know, the FDIC put Silicon Valley Bank (SVB) into receivership. Deposits will be moved to another bank, and the FDIC will work off the remaining assets and liabilities.

SVB is the second-largest bank default ever, so yes. Banks are heavily reliant on deposits and capital. If deposits start leaving banks, there may be more failures. A few S&P 500 regional banks (FRC and SBNY) are down more than 20% today, forewarning more potential problems.

This event happened extremely fast. Was the FDIC overly aggressive, or was the situation dire? We don’t know much yet. As you can tell, there are a lot of unanswered questions. We will learn a lot more in the coming days.

Bonds are surging today, and quite a few of our conservative stocks are holding up, protecting our portfolios well.

Equity Model

- Sell 100% of iShares S&P 500 ETF (SPY)

- Sell 100% of T. Rowe Price (TROW)

ETF Model

- Sell 100% of iShares S&P 500 ETF (SPY)

- Sell 100% of iShares Financial Sector ETF (XLF)

Lance Roberts, CIO

Have a great week!