Technically Speaking: The 4-Phases Of A Full-Market Cycle

Throughout history, bull market cycles make up on one-half of the “full market” cycle. During every “bull market” cycle, the market and economy build up excesses which must ultimately be reversed through a market reversion and economic recession. In the other words, “What goes up, must come down.”

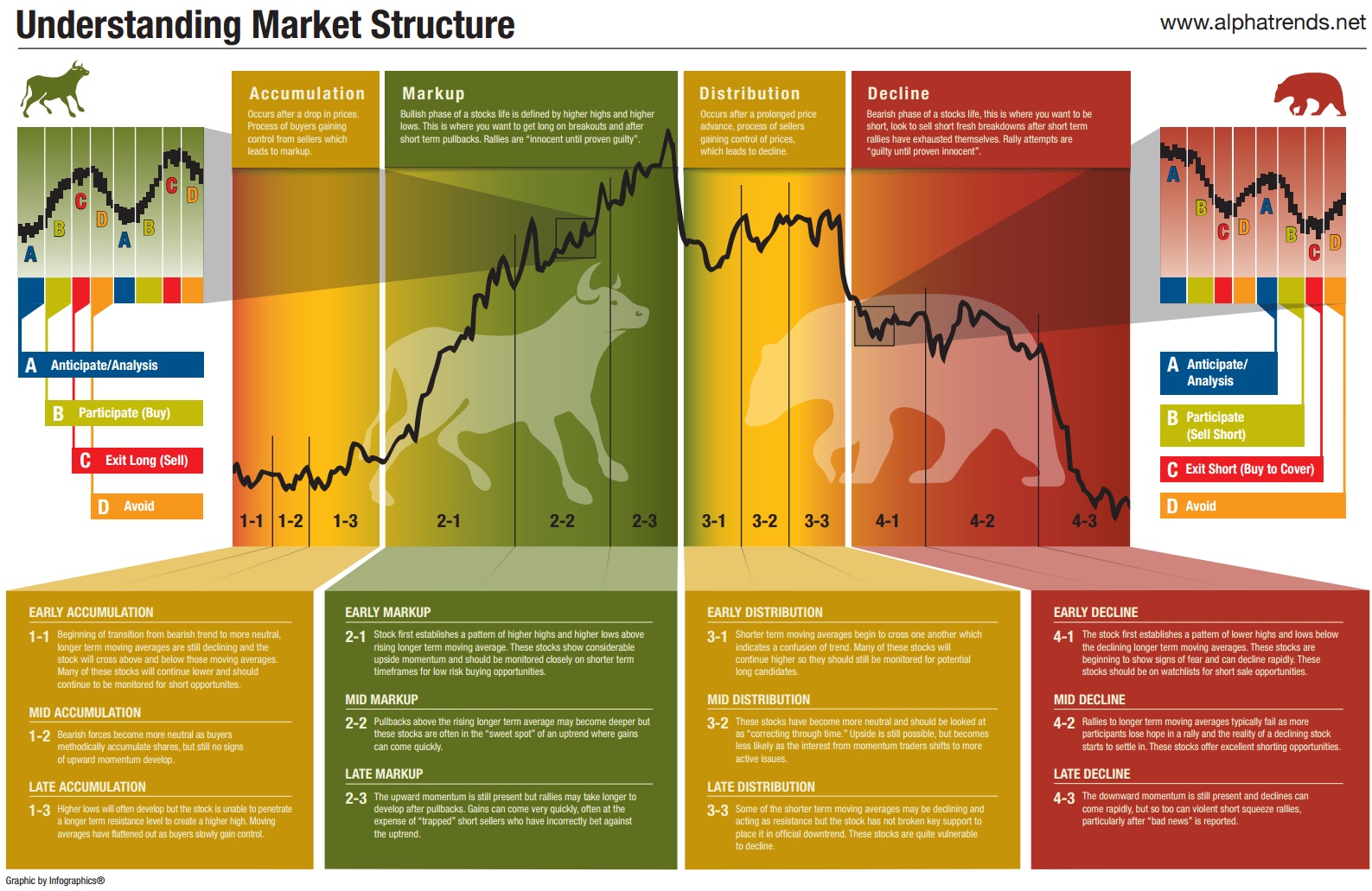

Understanding Market Cycles

I was digging through some old charts over the weekend and stumbled across this gem from AlphaTrends which explains the “best time to buy stocks.” “Is it possible to time the market cycle to capture big gains? Like many controversial topics in […]