A Traders’ Secret For Buying Munis

Believe it or not, any domestic bond trader under the age of 55 has never traded in a bond bear market. Unlike the stock market, which tends to cycle between bull and bear markets every five to ten years, bond […]

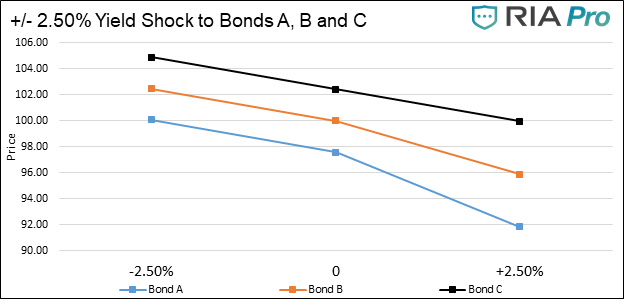

Believe it or not, any domestic bond trader under the age of 55 has never traded in a bond bear market. Unlike the stock market, which tends to cycle between bull and bear markets every five to ten years, bond […]