Hope For The Best, Plan For The Worst

Around 46 BC, Cicero wrote to a friend saying, “you must hope for the best.” To be happy in life we must always have “hope.” It is “hope” which is the beacon that lights the pathway from the darkness that eventually […]

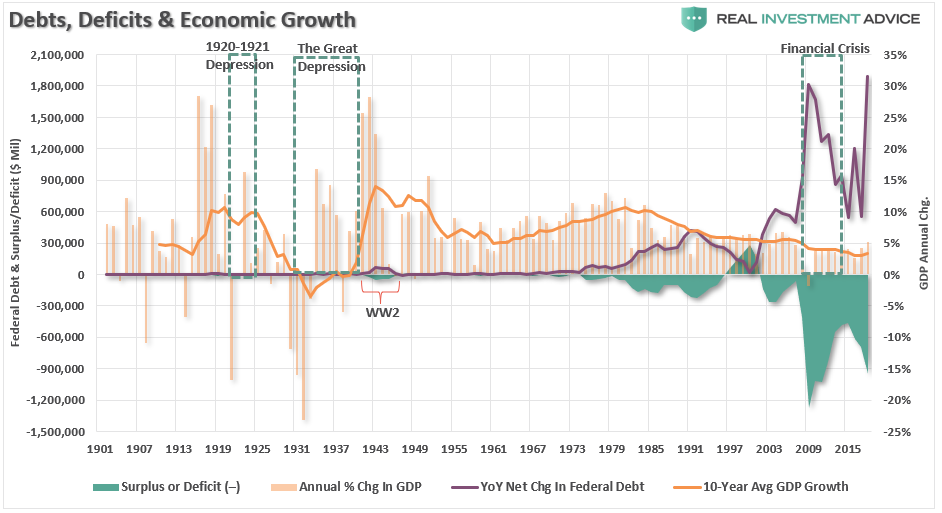

Economic Theories & Debt Driven Realities

One of the most highly debated topics over the past few months has been the rise of Modern Monetary Theory (MMT). The economic theory has been around for quite some time but was shoved into prominence recently by Congressional Representative […]

Democrats Should Start Worrying About The Deficit.

Democrats should start worrying about the level of debt and the increasing deficit. I previously discussed this issue when President Obama held the White House, when Marshall Auerback, via the Nation, wrote: “Delivering on big progressive ideas like Medicare for […]

CFNAI: The Most Important & Overlooked Economic Number

The Chicago Fed National Activity Index (CFNAI) is arguably one of the most important and overlooked economic indicators. Each month, economists, the media, and investors pour over various mainstream economic indicators, from GDP to employment and inflation, to determine what […]

#WhatYouMissed On RIA This Week: 03-27-20

Here is what you might have missed from the RIA Crew last week. A compilation of our best blogs, newsletter, podcasts, the daily radio show and commentary from RIAPRO.NET.

#WhatYouMissed On RIA This Week: 03-20-20

Here is what you might have missed from the RIA Crew last week. A compilation of our best blogs, newsletter, podcasts, the daily radio show and commentary from RIAPRO.NET.

Margin Call: You Were Warned Of The Risk

"Stocks down, Bonds down, credit down, gold down, oil down, copper down, crypto down, global systemically important banks down, and liquidity down...Today was the worst day for a combined equity/bond portfolio... ever..."This is what a "Margin Call," looks like.

#WhatYouMissed On RIA This Week: 03-13-20

Here is what you might have missed from the RIA Crew last week. A compilation of our best blogs, newsletter, podcasts, the daily radio show and commentary from RIAPRO.NET.

#WhatYouMissed On RIA This Week: 03-06-20

Here is what you might have missed from the RIA Crew last week. A compilation of our best blogs, newsletter, podcasts, the daily radio show and commentary from RIAPRO.NET.