There appears to be a frequently repeated myth on social media that foreigners are selling US Treasury bonds in large quantities. Often, the myth is supported by the belief that certain foreign governments, such as China, Japan, and Saudi Arabia, are rapidly selling down their US Treasury securities. Concerns about trade deficits, inflation, and geopolitical tensions are used to support the rationale. Furthermore, some believe their US bond holdings give these countries significant political leverage. The myths are false. As shown below, the reality is that foreign ownership of US Treasury debt continues to increase steadily. In fact, the growth of Treasury debt ownership is running at 10%, decently above the pace of the ten years prior.

This falsehood stems from a misunderstanding of how international finance operates. A large majority of foreign trade occurs in dollars. Accordingly, foreign nations must hold dollars. Whether in a bank or through direct purchases of bonds, a significant percentage of the dollars, also known as reserves, end up in the Treasury market. Unless another currency usurps the dollar’s reserve status, this will continue to be the case. Moreover, global economic growth and inflation lead to increased dollar trade, resulting in more dollar reserves and, ultimately, more US Treasury holdings by foreign investors.

Selling large amounts of Treasuries, as some claim, would likely lead to significant losses for the sellers due to the impact it would have on the bond market and their remaining bond holdings. Thus, the myth of a mass sell-off is unfounded, as it would be financially counterproductive for foreign investors, who rely on the stability and interest payments provided by Treasuries.

What To Watch Today

Earnings

Economy

Market Trading Update

Technically, markets remain extended relative to long-term averages, though early cracks show. As noted, money flows have shown some weakness, and with the S&P 500 closing Friday at ~6644, modestly below its recent peak, but still comfortably above its 50-day moving average at ~6460 and its 200-day moving average at ~6014. The trend remains intact, but the distance above moving averages suggests limited upside without consolidation. For perspective, a retracement to the 200-DMA would entail a 10% decline. However, a retracement to the running bull trend line near the April lows would encompass a 24% decline, and we would still be in a bull market.

Furthermore, breadth remains weak, with only about 49% of S&P components above their 20-day average and only 56% above their 50-day average. With markets consistently hitting new highs, the breadth should be much stronger. Negative divergences continue in momentum and relative strength oscillators (RSI, MACD), hinting at waning upside pressure.

Equal-weighted indexes lag cap-weighted peers, further underscoring the leadership concentration. Lastly, as measured by the VIX, volatility ticked up toward 15.29, which is still low historically but suggests that hedging demand is picking up.

Support and Resistance Levels:

- Support: 20-DMA ~6568; 50-DMA ~6459; 200-DMA ~6014.

- Resistance: Prior highs near 6666-6700.

- Volatility: VIX remains subdued but rising off the floor.

OUTLOOK: Neutral / Slightly Bearish – The uptrend is intact, but divergences and stretched conditions argue for caution. Quarter-end flows may push markets toward support zones before setting up a potential rebound into October.

The Week Ahead

The quarter-end on Tuesday should bring some volatility to markets as institutional investors rebalance and window-dress their portfolios. Often, securities that are impacted in one direction prior to the quarter end are affected in the opposite direction following the quarter end.

Jobs data will headline the week with JOLTs on Monday, ADP on Tuesday, and the BLS employment report on Friday. The Wall Street consensus is a mere 39k new jobs, which appears to be a low bar for the report. Thus, a surprise to the upside would not be unexpected. Moreover, a number over 100k may lead some investors to downgrade the odds of more Fed cuts this year. Also of interest will be the ISM manufacturing and services reports. In particular, we will focus on the employment and prices subcomponents. In both surveys, jobs have been in contraction, but prices are running hot.

Slowdown Signals: Are Leading Indicators Flashing Red?

Lately, there’s been a growing sense of confidence among investors that the U.S. economy has dodged the proverbial bullet. Despite a historic rate-hiking cycle by the Federal Reserve, two years of stubborn inflation, and signs of strain in global trade, the dominant Wall Street narrative is now a curious mix of “soft landing,” “no landing,” and even “re-acceleration.” For example, look at forward earnings estimates for the companies most susceptible to economic growth: small and mid-capitalization stocks. Over the last two years, earnings growth was meager when the economy was “booming” due to massive fiscal and monetary stimulus flows. However, as we head into 2026, Wall Street expects corporate earnings to increase sharply, which can only occur if the economy reaccelerates.

While the market is betting on an economic revival to support current valuation levels, the real economy is suggesting things are slowing down. Notably, the evidence isn’t coming from obscure corners. It’s showing up in the indicators designed to give us a heads-up before a storm arrives.

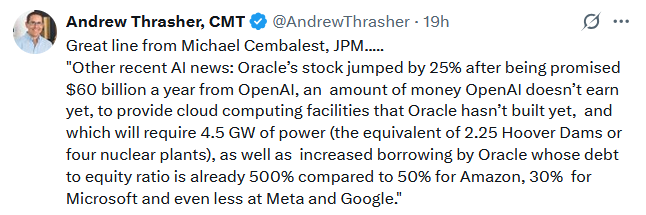

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.