I recently penned an article on “Money Supply Growth,” which elicited a very thoughtful response from Garrett Baldwin via Substack. He argued that labeling Federal Reserve operations as “money printing” is not rhetoric, but rather a reality. He points to Ben Bernanke’s 2010 interview, where Bernanke described how the Fed marks up digital accounts.

But Garrett’s view, while valid in parts, overlooks how the system functions. To understand money supply growth, it is essential to distinguish between reserve creation and deposit creation.

Garrett argues that referring to the Federal Reserve’s operations as “money printing” is not merely rhetorical but structurally accurate. He states:

“When I refer to ‘money printing,’ I’m describing the Fed’s ability to create unlimited digital reserves to purchase government debt … and how Treasury operations affect leverage in the financial system.”

Garrett believes this process functions equivalently to printing money and should be treated as such. While this perspective highlights the scale and potential consequences of monetary interventions, it risks misrepresenting the process by which money is created in a modern banking system. To unpack this, it’s critical to distinguish between reserve creation by the Federal Reserve and the creation of broad money (such as deposits) by commercial banks.

Let’s start with how the Fed creates “reserves.”

The Creation Of Reserves

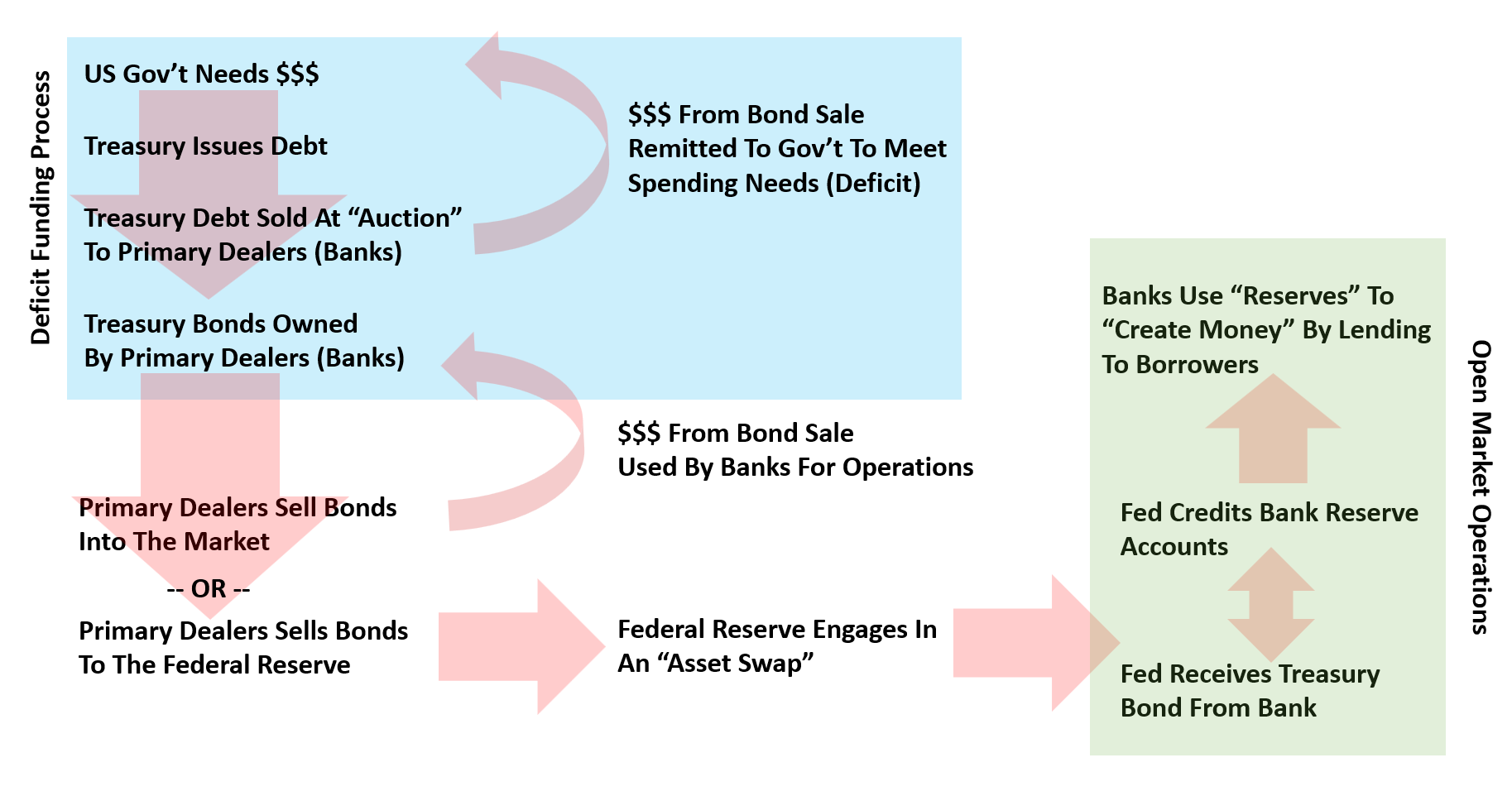

The Federal Reserve conducts open market operations to create bank reserves. It buys Treasury or mortgage-backed securities from commercial banks. In return, it credits those banks’ reserve accounts.

These reserves are digital entries. No physical money is printed. The bank ends up with more reserves and fewer securities. Its balance sheet doesn’t grow. Nothing in this step directly increases the money supply.

Here’s the basic flow:

The Federal Reserve increases reserves through open market operations (OMO), most notably through large-scale asset purchases often referred to as quantitative easing (QE). The Fed purchases assets from commercial banks or primary dealers, primarily U.S. Treasury securities or mortgage-backed securities. The Fed pays for these assets not with cash or printed money, but by crediting the selling bank’s reserve account at the Federal Reserve.

The last sentence is most important with respect to “money printing.” There is money creation, as it is only a digital accounting system of debits and credits to the banks’ reserve accounts and the Fed’s balance sheet.

Here’s the step-by-step:

- The Government issues debt to cover spending that exceeds the revenue collected. (This is the deficit.)

- The “primary dealers” attend the Government debt auction and are required to purchase the issued debt. The banks now own the debt, and the Government has money to spend.

- The “primary dealers” can now sell the bonds to other buyers (institutions, hedge funds, etc.) OR they can sell the debt (Treasuries or mortgage-backed securities) to the Fed.

- In the latter case, the Fed increases the bank’s reserve balance at its district Federal Reserve Bank in exchange for the purchase of the debt.

- The bank now holds more reserves and fewer securities, but there is zero change to its overall asset level. (There was no creation of money)

- On the Fed’s balance sheet, the asset side increases (as the securities it now holds) and the liabilities increase (as new reserves are created).

Critically, these reserves are not physical currency. They are digital entries on the Fed’s balance sheet, and their use is only for transactions between banks or to meet reserve requirements. They are not spendable by households or businesses.

Why Reserve Creation Is Not the Same as “Money Printing”

The phrase “money printing” traditionally evokes an image of the central bank creating currency and injecting it directly into the economy. But in practice, the vast majority of money in circulation is bank deposits, not paper notes. As the Bank of England explains,

“When a bank makes a loan, it does not typically hand out physical cash … instead, it credits the borrower’s account with a bank deposit of the size of the loan.” (bankofengland.co.uk)

As noted above, what the Fed creates during an “asset swap” is reserves, not deposits. Banks holds these reserves and are not directly spendable in the real economy. The creation of deposits, which expands the broad money supply, occurs when commercial banks make loans.

This is a crucially important point. As we stated in our previous article:

“ALL Money is LENT into existence.”

Once a bank holds excess reserves (reserves above what it needs to meet regulatory requirements or settle interbank transactions), it has more capacity to extend credit. However, and this is critical, reserves do not directly cause loan creation.

Banks do not lend out reserves. Instead, they make lending decisions based on creditworthiness, demand for loans, regulatory capital requirements, and profitability. When a bank makes a loan:

- It creates a new asset (the loan) on its balance sheet.

- It simultaneously creates a new liability (a deposit in the borrower’s account).

- That deposit increases the money supply, as measured by aggregates such as M1 or M2.

This is why, as we explained in our “Myths Of Gold” article, the money supply (M2) must grow with the economy.

“It’s easy to point to M2 charts and scream debasement. However, the money supply must grow as the economy grows. If it doesn’t, deflationary risks emerge. Therefore, the key is whether money creation exceeds economic growth in a sustained way. Since 1959, the money supply has grown in alignment with economic growth.”

If the bank later needs reserves (to settle a payment or meet reserve requirements), it can obtain them from the Fed or through the interbank market. Thus, reserves are not a constraint in the lending process; they are supplied elastically by the central bank to support the payments system.

This is why economists emphasize that “loans create deposits”—not the other way around. The Fed’s reserve creation enables banks to lend more comfortably by providing ample liquidity and reducing funding stress, but it does not force them to lend. Lending depends on borrowers’ demand, credit conditions, and regulatory considerations—not the mere availability of reserves.

Because reserves are not directly lent out to consumers or businesses, their creation does not inherently lead to inflation. Between 2008 and 2020, the Federal Reserve expanded its balance sheet by trillions of dollars, dramatically increasing reserves. Yet, broad money growth remained moderate and consumer price inflation stayed below the Fed’s 2% target for much of that time. Only when the Government sent checks directly to households (increasing demand) while shuttering the economy (reducing supply) did inflation become a temporary problem. As supply and demand return to normalcy and M2 as a percentage of GDP reverses, inflation is likely to follow suit.

This shows that expanding reserves through QE does not automatically result in spending or price increases. It can, however, lower interest rates, raise asset prices, and encourage credit expansion if lending conditions are favorable.

A Few Other Points On Money Printing

Garrett argues that our article underestimates the role of collateral supply, wholesale funding, shadow banking, and repo markets. He writes that:

“Collateral quality and abundance determine whether loans are made,” that “most credit creation now happens through collateralized wholesale markets that dwarf traditional deposits,” and that the shadow banking chain is central to liquidity transmission outside M2.

Garrett makes valid observations about the evolving financial structures in today’s economy. For instance, the Bank for International Settlements (BIS) recognizes that non-bank financial intermediaries play a significant role in global liquidity and credit. The rise in collateral reuse, repo, and leverage in non-bank segments is well-known. However, this does not nullify the foundational mechanism of “money creation“ via bank lending. Nor the role of central bank reserves in supporting the settlement system.

In fact, Governor Andrew Bailey’s Bank of England lecture emphasized:

“Commercial banks can create money simply by extending loans to their customers.”

He further states that reserves are the “ultimate means of settlement” but do not directly create broad money themselves. Therefore, it overstates the argument that shadow‑banking channels dominate. While shadow channels matter for liquidity and risk, they sit atop a base framework in which commercial bank lending and deposits remain central.

Sectoral Balances, Fiscal Mechanics and Distribution

Notably, Garrett accepted the sectoral identity that government deficits create private surpluses. However, he then argues that what matters is who captures the surplus and how it is deployed. To wit:

“When the government deficit becomes a hedge fund’s Treasury arbitrage profit, that’s not the same as money reaching productive investment.”

He further asserts that financing methods (Federal Reserve purchases, foreign savings, and domestic rollover) reshape risk flows, distort incentives, and facilitate financialization.

His argument is sensible and certainly touches on wealth inequality. However, it does not change the accounting identity (government deficit = private surplus + foreign balance), which remains valid regardless of distribution. As we noted, deficits provide net financial assets to the private sector. While one must consider the use of those assets, not just the quantity, such is a different discussion.

The financing channel does matter. When the Fed monetizes deficits through asset purchases or via regulatory demand, it alters risk premia and credit flows. The “private sector surplus” shorthand does not capture that channel nuance. The reality is that since 2009, there has been a definite shift toward speculative assets. That shift increased wealth inequality in the U.S., rather than productive investment that would have generated a broader economic outcome.

While Garrett’s arguments are undoubtedly valid and emphasize that distribution, allocation, and financing channels matter for outcomes, they do not change the fact that the Fed’s “money printing” does not occur.

Dollar Strength, Collateral Demand, and Debasement Fears

Garrett advances the idea that the dollar’s strength and significant Treasury demand reflect structurally mandatory safe-asset pipelines, regulatory incentives, and portfolio mechanics, rather than purely global confidence. As he noted:

“The dollar is still dominant… but let’s focus on… structurally enforced requirements.”

He also claims that asset‑price inflation, leverage, and collateral expansion are hidden forms of debasement even if consumer prices remain subdued.

The reality is that it is well documented that Treasuries serve as global safe assets; banks’ liquidity regulations (Basel, liquidity coverage rules) imprint demand on those assets. Yes, part of the dollar’s dominance does stem from the fact that these mandated pipelines are supported by literature on safe‑asset demand. However, while it is not incorrect that demand reflects confidence and liquidity preference, it just omits part of the story.

Putting it differently, the dollar’s dominance is partly explained by network effects and partly by regulation; however, it is also essentially a function of a lack of alternatives. For Central Banks globally that need to store reserves, there are no choices for “safe assets” that provide the rule of law, military prowess, liquidity, and depth of the market supplied by the U.S. Treasury bond market. Such is why, despite “narratives to the contrary,” foreign holdings of U.S. Treasuries continue to climb higher.

The expansion of reserves does not guarantee inflation, as banking behavior, lending, spending, and velocity also play a role. Yes, while QE and Zero Interest Rate Policy (ZIRP) did feed into asset price inflation, it did not translate into economic growth rates, which reduced monetary velocity (the speed at which money moves through the economy). In other words, I agree with Garrett’s premise that the monetary transmission system is “broken,” which is why, as noted, wealth inequality continues to grow.

While Garrett makes some valid points worthy of discussion, the macro logic stands. “Money printing” and debasement fears are largely unfounded, as noted in our previous article, and the demand for dollars remains evident in the rising demand for U.S. Treasuries by foreign buyers.

Garrett adds nuance with his focus on collateral, funding chains, and distribution. Those factors shape liquidity. But the basics still matter.

- All money is lent into existence.

- Reserves are not spendable by the public.

- The growth in the money supply stems from loans and fiscal spending.

- Asset swaps by the Fed change the form of money, not its quantity.

For readers seeking to understand inflation, liquidity, and wealth, these fundamentals form the foundation. Shadow banking and distribution come later. Start with the mechanics.