“Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.” That key line from Chairman Powell’s opening speech at the Fed’s Jackson Hole symposium effectively summarizes Powell’s view on monetary policy. Simply, the change in the balance of risks since the BLS jobs revisions warrants consideration for cutting rates.

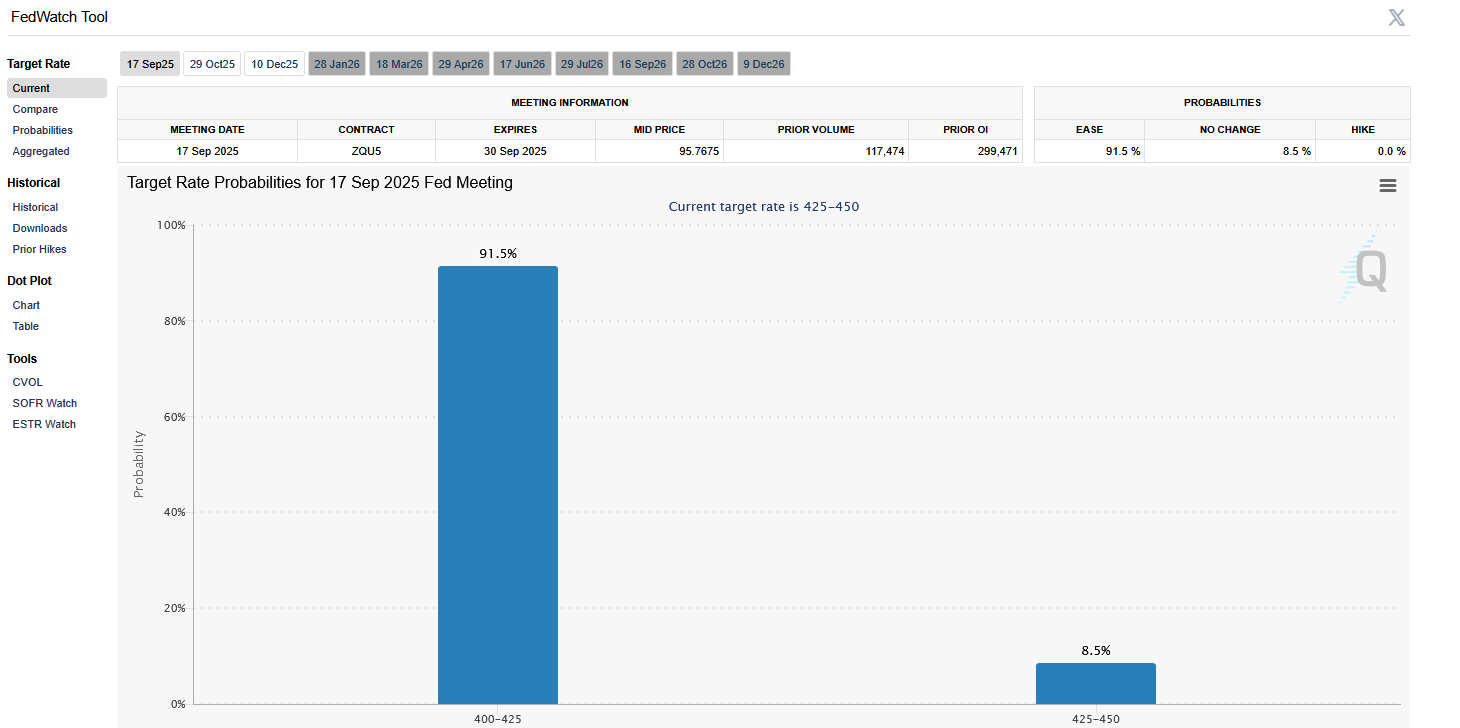

The Fed has two Congressional mandates: maximum employment and stable prices. Below are critical Powell comments on both objectives. He believes the labor market is in balance despite paltry payroll growth because the supply of workers has fallen appreciably. However, while it may be in balance, he thinks the risk of rising unemployment is increasing. The Fed is charged with balancing the risk of rising unemployment with its concerns that tariffs will spark a new round of inflation. To this, in the second paragraph, he notes that he believes tariff-based inflation will be short-lived, albeit it may take a while for it to work its way through the system. Therefore, Powell views the risk of higher unemployment as greater than the risk of lasting higher inflation. As we show below, the market now assigns a 91% chance that the Fed cuts in September. The odds were 70% before Powell spoke.

Overall, while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.

A reasonable base case is that the effects will be relatively short lived—a one-time shift in the price level. Of course, “one-time” does not mean “all at once.” It will continue to take time for tariff increases to work their way through supply chains and distribution networks. Moreover, tariff rates continue to evolve, potentially prolonging the adjustment process.

What To Watch Today

Earnings

- No notable earnings releases on Monday

Economy

Market Trading Update

After the market slid lower all week, testing the 20-DMA on Thursday, Jerome Powell’s speech at Jackson Hole turned sentiment on a dime. The S&P 500 returned to record highs, and the Dow surged 900 points. Investors took his tone as confirmation that a September rate cut is in play. Specifically, Powell noted the slowdown in employment as a key reason for the shift in stance, as noted in the key paragraph from his speech.

“In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation. When our goals are in tension like this, our framework calls for us to balance both sides of our dual mandate.

Our policy rate is now 100 basis points closer to neutral than it was a year ago, and the stability of the unemployment rate and other labor market measures allows us to proceed carefully as we consider changes to our policy stance.

Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.“

Wall Street also noticed the shift in tone. Krishna Guha of Evercore ISI called it a “clear pivot to risk management.” He added the speech “gave markets permission to rally.” Bank of America’s Michael Gapen noted Powell’s comments were “dovish without overcommitting,” keeping pressure off the Fed to act immediately while softening market fears.

While stocks had been under pressure earlier this week, specifically in the overbought Technology sector, Powell opened the door for the bulls. The rally lifted risk-based sectors. Small caps led. Bitcoin and bonds bid, and homebuilders, airlines, and regional banks surged. The dollar fell as yields dropped sharply.

However, risks remain. Inflation is not yet anchored. Powell downplayed tariff impacts, but new trade policies could stoke price pressures. If data surprises to the upside, markets could whiplash. BlackRock’s Rick Rieder warned the Fed “must still see inflation trending toward target,” and cautioned that easing too fast “could reignite instability.” Don Carter at Fort Washington Investors also remained concerned, stating, “Even with Powell’s more dovish tone, the data in the coming weeks still pose some risks. The market will like this change in tone. But I think we must be careful not to get too far ahead. There is still a lot of data between now and the next FOMC meeting.”

As we will discuss in today’s newsletter, while earnings season was solid, valuations are clearly stretched. The risk to investors is that with the Fed’s next move priced in, any hesitation could lead to stocks giving back recent gains.

📈Technical Backdrop

Price remains in a primary uptrend as the S&P 500 held its initial test of the 20-DMA on Thursday. Daily, the market remains well above the 20, 50, and 200 DMAs, with the top of the current trend channel rising toward 6600. Such keeps the trend constructive as long as pullbacks hold support. Short‑term pivots for the next session cluster around 6,470, with resistance being the recent all-time highs from two weeks ago.

Furthermore, daily momentum is positive but edging hot. RSI(14) sits in the low‑60s, MACD, however, remains on a “sell,” and several faster oscillators (Stoch/RSI variants) registered overbought readings into Friday’s rebound. One note is that relative strength, momentum, and money flows remain in a “negative divergence” to the market, increasing near-term investor risk. However, the “buy‑the‑dip” strategy continues to perform well for now.

Participation improved, but it’s not euphoric. Roughly 61% of S&P constituents are above their 50‑DMA and about 63% above their 200‑DMA, which is healthy, but not yet stretched. For now, breadth is supportive, but still something to monitor for confirmation via higher highs in the A/D lines.

Despite the sell-off this past week, volatility remained subdued and closed near 14 into the close, consistent with a risk‑on term structure. Options appetite is still very bullish: the 10‑day average Cboe total put/call sits near 0.84. Positioning is mixed across cohorts: NAAIM equity exposure remains high while AAII shows a cautious retail stance. After this week’s close, we will see if retail begins to chase more aggressively.

Under the surface, the week’s rebound broadened: small caps and cyclical pockets outperformed on Friday, with the Russell 2000 ripping ~4% as yields fell. Equal‑weight (RSP) has begun to show short‑term relative improvement versus cap‑weight (SPY). Even though RSP still trails YTD, it is an encouraging sign of incremental broadening. Sector‑wise, weekly performance tilted toward cyclicals (energy/materials/industrials) with defensives mixed, while megacap tech cooled earlier in the week and rejoined late.

Key Levels & Risk Markers (near‑term)

- Support: 6,385 (20‑DMA), 6,269 (50‑DMA), 6,269 (200‑DMA). A close below the 50‑DMA would signal loss of short‑term trend grip.

- Momentum guardrails: Daily RSI mid‑60s; a rollover with negative divergence would raise pullback odds.

- Internals to confirm: S&P %>50‑DMA pushing sustainably >65–70%.

- Sentiment: Watch if VIX ≤13 and put/call MA pushes lower, would increase risk of a shakeout.

Outlook for Next Week: Neutral

The primary trend is up (price above rising key MAs; breadth decent), and Friday’s broad snap‑back helps. But short‑term momentum is warm, volatility is compressed, and pro exposure is already high while seasonality turns less friendly. Netting those, the risk/reward into next wee

The Week Ahead

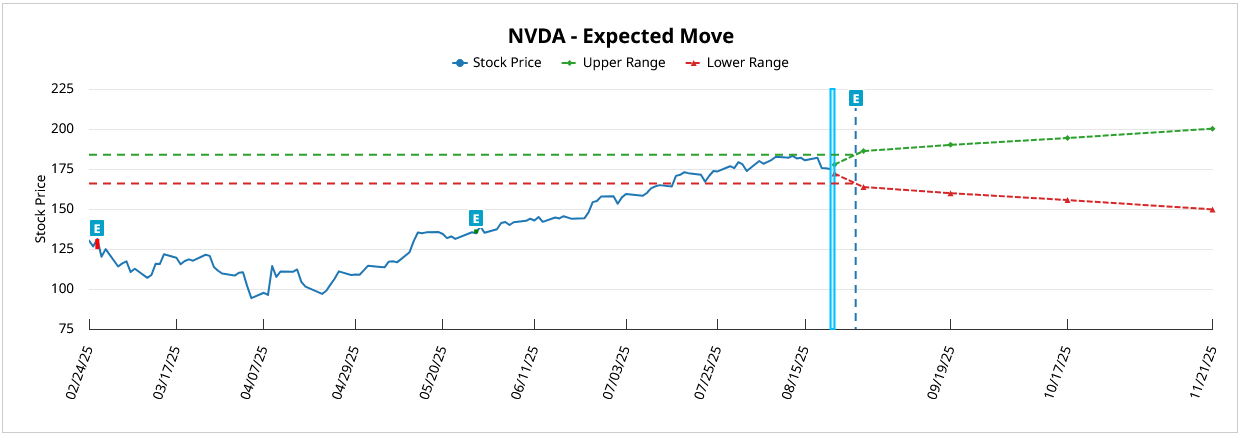

Nvidia earnings will headline this week. Given how the AI industry has driven corporate profits and the infrastructure buildout, their earnings report on Wednesday and, importantly, their forward guidance, could greatly impact stocks that have been leading the way higher. This includes some of the Magnificent Seven stocks, but a slew of high-beta, low-profitability companies. Currently, options prices suggest the stock could move up or down by $11 or 6.5%. Historical swings have been around 11% on average over the last eight reports. The graph below, courtesy of Barchart, shows the options’ expected outcomes.

Heading into Labor Day, the economic news will be diminished. However, PCE prices on Friday will shed more light on how tariffs are impacting inflation. Furthermore, given that tariff-based inflation seems to be the only thing that may keep the Fed from cutting rates, a weak print could assure a rate cut in September and future meetings.

US Economy: Recent Data Suggests Risk To Earnings

The latest economic data suggests the US economy is decelerating. That means growth is slowing, jobs are shrinking, and households are spending less. As we showed in a recent #BullBearReport, economic growth, inflation, and personal consumption are trending lower.

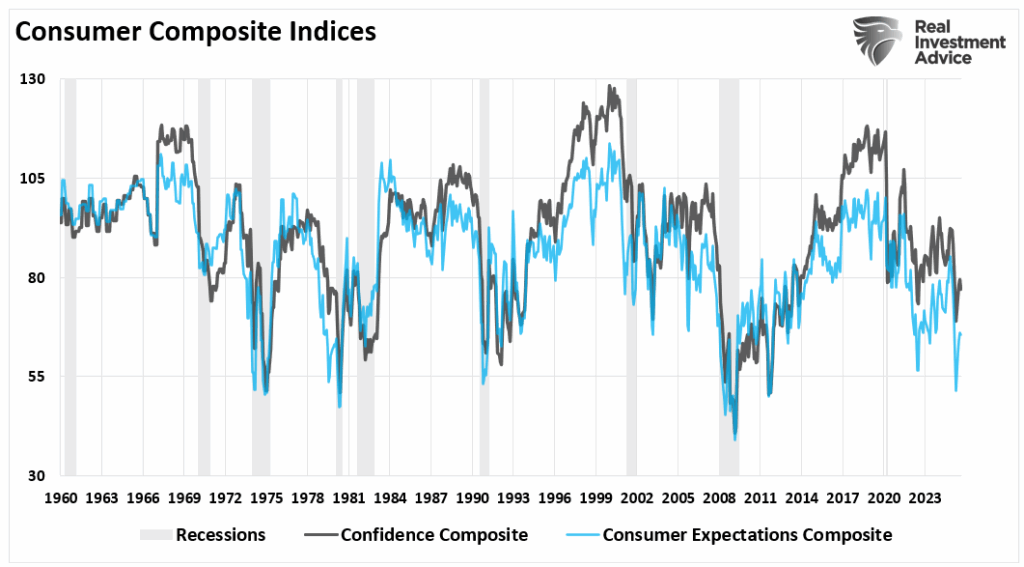

Unsurprisingly, with job growth weakening, consumer sentiment also took a hit in the latest report, with future expectations remaining very weak.

While the financial markets got very excited over the data, as it creates pressure for rate cuts in the US, it bodes poorly for future returns. So far in 2025, there have been 88 central bank rate cuts, the fastest cut cycle since the 2020 COVID crash. That is not a sign of burgeoning economic growth. While stocks and credit anticipate the Fed joining the easing party, the pace of cuts suggests that weakness is spreading globally.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.